So, what's the actual damage? For most small businesses in the UK, you’re likely looking at somewhere between £60 and £450 per month for an accountant. It's a broad range, I know. A sole trader just starting out will naturally sit at the lower end, while a bustling limited company with a few employees will creep towards that higher figure.

Pinpointing What You Should Expect to Pay

Getting a handle on the typical investment for professional financial help is a smart first move for any business owner. While the final number on an invoice will always be unique to you, we can definitely establish a solid baseline of what to expect.

An accountant's fee isn't just a number plucked from thin air. It’s directly linked to your business structure, how complicated your finances are, and exactly how much support you need.

Think of it like paying your energy bill. A small, one-bedroom flat is going to have a much lower bill than a sprawling five-bedroom house. It's the same principle here. A freelance designer with a handful of invoices each month will have a far smaller accounting bill than an e-commerce shop juggling hundreds of orders, VAT returns, and payroll. The goal is to find a service that fits what your business actually needs.

Comparing Typical UK Accountant Fees

Let's get down to brass tacks and look at some real-world price points. In the UK, how much you pay an accountant depends on things like your business type, the specific jobs you need them to do, and their level of experience.

Generally speaking, a sole trader can budget for around £100 to £150 a month. For small to medium-sized businesses, that figure often lands somewhere between £60 and £450 per month. For a deeper dive into these numbers, it's worth checking out some detailed insights on UK accounting fees.

To give you a clearer snapshot, I've put together a table that breaks down the typical costs. This should help you benchmark any quotes you get against the industry averages.

Typical UK Accountant Costs by Business Type

| Business Type | Typical Monthly Fee Range | Typical Annual Fee Range | Common Services Included |

|---|---|---|---|

| Sole Trader | £30 – £150 | £300 – £1,500+ | Self-Assessment Tax Return, Basic Bookkeeping Advice, Annual Accounts Summary |

| Partnership | £70 – £250 | £800 – £2,500+ | Partnership Tax Return, Individual Partner Tax Returns, Annual Accounts |

| Small Ltd. Company | £100 – £350 | £1,200 – £4,000+ | Corporation Tax Return, Annual Accounts, Confirmation Statement, Director's Payroll |

| Growing SME | £250 – £600+ | £3,000 – £7,000+ | All of the above plus VAT Returns, Full Payroll, Management Accounts, Cash Flow Forecasting |

Remember, these are ballpark figures. A quote can easily go higher if your business has particularly complex needs, like dealing with international sales or intricate tax schemes.

How Accountants Actually Price Their Services

When you start looking for an accountant for your small business, you'll notice pretty quickly that the quotes you get can look very different. There isn't a one-size-fits-all approach. Most accountants use one of three main pricing models, and getting your head around these is the first step to finding a setup that works for your budget and what you actually need.

A good way to think about it is like picking a mobile phone plan. You could go for a predictable monthly contract with everything bundled in, a flexible pay-as-you-go option, or just a one-off payment for a specific need. Accountant pricing follows a similar logic, giving you choices that can match your cash flow and how much help you think you'll need.

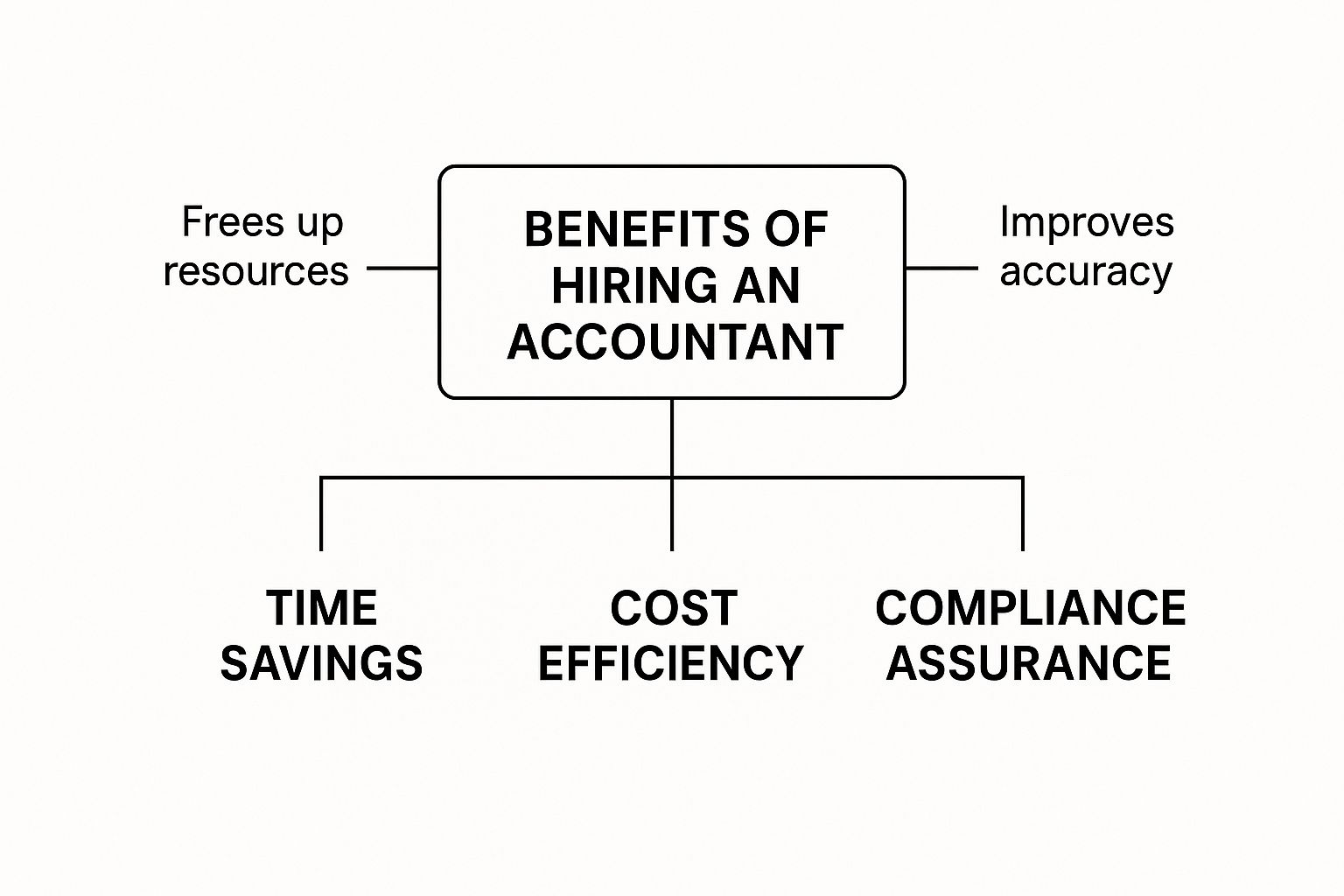

No matter which model you choose, the investment is about more than just number-crunching. This infographic gives a great overview of the real value you get back.

As you can see, it boils down to saving you time, making your business more cost-efficient, and ensuring you stay on the right side of the taxman.

The Fixed Monthly Fee Model

This is easily the most popular choice for small businesses, and for good reason. You pay a set amount every month for a clearly defined package of services. This bundle typically includes the essentials like year-end accounts, tax returns, payroll processing, and having an expert on hand for advice.

The beauty of this model is predictability. Your costs are fixed, so there are no nasty surprises when the bill arrives. It also fosters a better relationship with your accountant; you're more likely to pick up the phone for a quick question without worrying that the meter is running. For a small business owner, that financial certainty is gold.

The Hourly Rate Model

Some accountants stick to the traditional method of charging for their time by the hour. It’s a pure "pay-as-you-go" system where you’re billed for the exact time spent working on your accounts. These rates can swing quite a bit depending on the accountant's seniority and how tricky the work is.

This model makes sense in specific situations:

- One-off advice: Perfect if you just have a single, burning question or need help with a very small, specific task.

- Complex projects: A good fit for things like a business valuation or a complex tax investigation where it's tough to estimate the total work involved.

- Minimal support: If you do most of the bookkeeping yourself but just want a professional to cast an eye over it, this can be cost-effective.

The big downside here is the lack of predictability. A task you thought was simple can easily spiral, leading to a much higher bill than you budgeted for. It can make forecasting your accounting costs a real challenge.

The One-Off Project Fee

The third option is a fixed fee for a single, well-defined project. This could be anything from preparing your annual accounts and Corporation Tax return to helping you migrate to a new accounting platform like Xero or QuickBooks.

This model offers a fantastic middle ground for specific jobs. You get a clear, upfront cost so you know exactly where you stand, but without being tied into a long-term contract. It’s also a brilliant way to try out a new accountant before committing to a monthly plan.

For example, you could hire an accountant for a one-off project to get your first year's accounts filed. If you love their work and communication style, you can then move onto a monthly package with confidence. This approach gives you total clarity and control over the accountant costs a small business faces for specific, standalone tasks.

What Actually Goes into Your Accounting Bill?

Ever looked at a quote from an accountant and wondered, "Where did they get that number from?" It’s a fair question. The truth is, your bill isn’t just a figure plucked from thin air. It’s built on a few core factors that directly reflect the amount of work your business needs.

Think of it like getting an extension built on your house. A simple, single-room job is going to cost a lot less than a complex, two-storey project with custom fittings. Accounting works the same way. The more moving parts your business has, the more time and expertise it takes to manage, and the price will reflect that.

Getting your head around these key drivers is crucial. It helps you understand exactly what you’re paying for and allows you to have a much better conversation with a potential accountant about the value they’re bringing to the table.

Let’s pull back the curtain on the main things that shape your bill.

Business Structure and Complexity

Right out of the gate, the biggest factor influencing your bill is how your business is legally set up. A sole trader, for instance, has the simplest set of requirements, mostly centred on getting that annual Self-Assessment tax return filed. The work is fairly straightforward, which keeps the fees down.

A limited company, on the other hand, is a different beast entirely. It brings a much heavier compliance load. Your accountant has to prepare and file annual accounts with Companies House, a Corporation Tax return with HMRC, and the annual Confirmation Statement, not to mention dealing with director payroll. All these extra statutory duties mean a higher fee is pretty much unavoidable.

Your business structure sets the baseline for your accounting costs. The legal and tax obligations of a limited company are fundamentally more complex and time-intensive than those of a sole trader, and the price will always reflect this reality.

This is the main reason you’ll see such a wide range of prices out there. The more compliance boxes an accountant has to tick to keep you on the right side of the law, the more the service is going to cost.

Transaction Volume and Bookkeeping Quality

Once the business structure is set, the next big thing is the sheer volume of your financial activity. Your accountant has to process and make sense of every single transaction your business makes. A freelance consultant sending out five invoices a month is in a completely different league to an e-commerce shop with hundreds of daily sales and supplier payments.

Here’s a simple breakdown of how this affects your costs:

- More Transactions, More Time: It’s a simple equation. A higher volume of sales, purchases, and expenses directly translates to more hours spent on bookkeeping and reconciliation.

- The State of Your Records: This one’s huge. If you hand over a perfectly reconciled bank statement from cloud software like Xero, the job is quick. If you arrive with a shoebox full of crumpled receipts, your accountant has to spend hours sorting it all out—and that time will absolutely be on your bill.

Honestly, keeping clean, digital records is one of the single best things you can do to keep your accounting costs in check. The less tidying up your accountant has to do, the lower your fee will be.

Payroll and VAT Requirements

Adding services like payroll and VAT administration will always push the price up, simply because they introduce more complexity and recurring deadlines throughout the year.

Managing payroll isn’t just about paying people. It involves calculating salaries, National Insurance, and pension contributions for every employee, then submitting regular, time-sensitive reports to HMRC. It has to be precise. Likewise, preparing and filing quarterly VAT returns demands careful tracking of every sale and purchase to ensure you’re paying (and reclaiming) the right amount.

Your annual turnover also plays a massive role. In fact, many accountants structure their packages based on your gross income. For example, a common package might sit around £95 per month for businesses with a turnover of up to £150,000. Once you pass that threshold, the complexity and risk both go up, which pushes you into a higher service bracket. You can discover more insights about how turnover affects pricing and find a package that fits your business.

Each of these factors—structure, transaction volume, and extra services—adds another layer to the job. By understanding how they all contribute to the final bill, you can better appreciate the value you’re getting and make a much more informed decision when you’re looking at quotes.

What Services Should Your Accountant Actually Provide?

Getting a handle on the accountant costs a small business will face is only one part of the puzzle. The other, arguably more important piece, is understanding what you’re actually getting for your money. A good accountant does far more than just file your taxes once a year; their services can range from essential legal duties to advice that genuinely changes the game for your business.

I like to think of it like hiring a builder. One might just lay the bricks and mortar, making sure the structure is sound and meets all the regulations. Another will not only build the walls but also help you design the layout, choose the right materials, and even plan for future extensions. Both are useful, of course, but they deliver vastly different kinds of value.

Accountancy works in much the same way. The services you'll encounter generally fall into two big categories: compliance and advisory. Nailing the difference between them is the key to picking a package that doesn’t just meet your needs today but also helps you get where you want to go tomorrow.

Compliance Services: The Absolute Must-Haves

Compliance is the bedrock of any accounting service. These are the non-negotiable tasks required by law to keep your business on the right side of HMRC and Companies House. At its core, compliance work is about looking backwards, making sure all your financial history is reported accurately and on time.

Skimp on these, and you're asking for fines, penalties, and some serious legal headaches. For most small businesses, a basic package will always cover these core duties:

- Annual Accounts Preparation: Getting your financial statements compiled and ready for the year to be filed with the authorities.

- Tax Return Filing: This covers your Corporation Tax return if you're a limited company or your Self-Assessment as a sole trader.

- Basic Bookkeeping: Making sure every penny of income and every expense is recorded properly throughout the year.

- Payroll Administration: Managing employee salaries, NI and tax deductions, and pension contributions.

Think of these tasks as the foundation. They give you peace of mind that all your legal boxes are ticked, but on their own, they don't do much to help you grow.

Advisory Services: Where the Real Value Is

This is where a good accountant stops being a necessary cost and becomes a powerful investment. Advisory services are all about looking forward. They use your financial data to help you make smarter, more profitable decisions for your business. It's all about strategy, growth, and optimisation.

Advisory work is what separates a simple number-cruncher from a true financial partner. It’s about interpreting the story your numbers are telling and using that insight to build a better, stronger business.

These services move beyond just reporting what happened last year; they actively help you shape what happens next year. A great example is an accountant helping you with strategies for maximizing your work-from-home tax deductions, which can have a real impact on your bottom line. If you want a deeper dive, our guide on what services an accountant can provide offers a brilliant overview.

Comparing Accounting Service Packages

To make this distinction crystal clear, it helps to see what a basic compliance-focused package includes versus a more comprehensive advisory plan. The table below really shows the jump in value you get when you start investing in proper strategic support.

| Service Feature | Basic Compliance Package | Comprehensive Advisory Package |

|---|---|---|

| Focus | Historical Reporting & Legal Duties | Future Growth & Strategy |

| Tax Services | Annual Tax Return Filing | Proactive Tax Planning & Optimisation |

| Financial Reports | Year-End Accounts | Monthly/Quarterly Management Reports |

| Business Planning | None | Cash Flow Forecasting & Budgeting |

| Strategic Input | Limited to Basic Queries | Regular Strategy Meetings & Growth Advice |

| Value Proposition | Keeps you legally compliant | Helps increase profitability & efficiency |

Ultimately, the right choice really hinges on your business's current stage and future goals. A brand-new sole trader might only need a simple compliance package to get started. But a growing limited company with ambitions to scale will find that an advisory plan delivers a far greater return on investment.

How to Reduce Your Accountant Costs Without Sacrificing Quality

Controlling your accountant's fees doesn't mean you have to settle for a lower-quality service. In fact, by adopting a few simple habits, you can often lower your bill while actually getting more strategic value from your accountant. The secret is to make their job easier.

Think of it like paying a mechanic. If you bring your car in clean and well-maintained, they can get straight to the real issue. But if the car is caked in mud and cluttered inside, they first have to spend time cleaning just to access the problem—and you can bet that extra time will show up on your invoice.

When you become a more organised client, you cut down on the time your accountant spends on basic admin. This frees them up to focus on the high-value advice that can save you serious money in the long run, directly impacting the final accountant costs a small business has to pay.

Embrace Cloud Accounting Software

The single most effective way to cut down on billable hours is to ditch the spreadsheets and shoeboxes full of receipts. Modern cloud accounting software, like Xero or QuickBooks, is an absolute game-changer for small business owners and their accountants.

These platforms automate a huge amount of the manual data entry that used to eat up an accountant's day. When you link your business bank account directly to the software, transactions are pulled in automatically, making reconciliation a breeze instead of a headache.

Giving your accountant clean, organised, and real-time data from a cloud accounting platform is the ultimate win-win. It drastically reduces their time spent on manual bookkeeping, which directly lowers your fees and allows them to focus on smart tax planning instead of tedious data entry.

This simple shift from manual to automated record-keeping transforms you from a time-consuming client into an efficient one, which is always reflected in a more favourable bill.

Maintain Clean and Up-to-Date Records

Even with the best software in the world, good habits are essential. Your goal should be to keep your financial records as tidy as possible throughout the year, not just in a mad panic before a tax deadline.

Here are a few practical steps you can take:

- Reconcile Regularly: Don't let bank reconciliations pile up. Set aside 30 minutes each week to match up your bank transactions in your accounting software. This stops small queries from snowballing into big, expensive problems.

- Go Digital with Receipts: Use an app like Dext or AutoEntry to snap photos of receipts the moment you get them. This eliminates the risk of losing them and creates an organised digital paper trail your accountant can easily access.

- Keep Business and Personal Separate: Use a dedicated business bank account and credit card for all company transactions. Mixing personal and business expenses creates a huge, costly mess for your accountant to untangle.

For small businesses aiming to streamline operations and lower expenses, exploring options like outsourcing finance and accounting functions can also be a viable strategy. This approach can ensure your records are consistently well-managed by professionals from the get-go.

Ultimately, the decision to manage your accounts yourself or hire an expert comes down to your confidence and your business's complexity. If you're a limited company owner, understanding your obligations is key; our guide on whether you can file your limited company accounts yourself can provide some valuable context. By being proactive and organised, you aren't just saving money—you're investing your accountant's time where it truly counts.

Why a Cheap Accountant Can Be a Costly Mistake

When you're looking at the accountant costs a small business will face, it's incredibly tempting to just go for the cheapest quote you can find. But treating professional accounting like it's just another commodity, where the lowest price always wins, can backfire spectacularly. In fact, it can be one of the most expensive decisions you ever make.

A bargain-basement fee often means you're getting a corner-cutting service, leaving your business wide open to risk.

Think of it like hiring a builder. You wouldn't just hire the cheapest one to build a wall without checking their work, would you? They might throw it up quickly, but a few months down the line, you find cracks appearing because they used cheap materials. The cost to fix that mess will dwarf what you initially "saved". It's the exact same principle with your finances. A cheap accountant might tick the basic compliance boxes, but they almost never see the bigger picture.

That kind of short-sighted thinking can lead to a world of financial pain later on.

The Hidden Price of a Bargain Accountant

Sure, a low-cost accountant can probably file a basic tax return. But what are they not doing? The real value an accountant brings isn't just in submitting forms on time; it's in the proactive advice that saves you money and helps your business grow. A cheaper service simply doesn't have the experience or the time to give you that kind of strategic support.

Here’s a story I’ve seen play out time and time again: a business owner goes for a budget service, only to get hit with a surprise HMRC investigation. Their "cheap" accountant missed a load of allowable expenses and categorised income incorrectly, which set off all sorts of red flags. The owner ends up facing not just hefty penalties and back-taxes, but also has to pay a more experienced (and more expensive) professional to sort out the chaos.

Choosing an accountant based solely on price is an expense. Choosing one based on expertise is an investment. The return on that investment comes from proactive tax planning, strategic business advice, and the invaluable peace of mind that your finances are in safe hands.

This isn’t just a cautionary tale; it's a common reality that shows the true cost of cutting corners.

Shifting Focus From Price Tag to ROI

Instead of asking, "How much do you cost?", you should be asking, "What return on investment can you give me?". A great accountant is a partner in your success, not just a number-cruncher. Their value is measured in the tax they save you and the growth opportunities they help you spot.

A quality accountant delivers a tangible return in a few key ways:

- Strategic Tax Planning: They don't just record what happened last year. They help you structure your business to legally minimise your tax bill going forward.

- Business Growth Guidance: By getting under the bonnet of your numbers, they can pinpoint ways to boost your profitability and improve cash flow.

- Compliance & Peace of Mind: They make sure you’re playing by HMRC's rules, shielding you from stressful audits and costly fines.

Investing in a reputable, qualified professional is non-negotiable. Before you sign on the dotted line, it's vital to understand what professional qualifications your accountant should have, as this is a huge indicator of their expertise. A higher fee almost always pays for itself many times over through smart tax savings and strategic insights that a cheaper alternative would simply never offer.

A Few Common Questions About Accountant Costs

Stepping into the world of business finance can feel a bit like learning a new language. To help you get your bearings, here are some plain-English answers to the questions we hear most often from business owners.

Do I Actually Need an Accountant for My Small Business?

Legally speaking, it depends on your business structure. But from a practical standpoint? Absolutely.

For limited companies, an accountant is non-negotiable. They’re the ones who’ll ensure your annual accounts and Corporation Tax returns are filed correctly with HMRC and Companies House, saving you from some very steep penalties.

If you’re a sole trader, you might think you can get by on your own. While you can, an accountant is your secret weapon. They don’t just keep you compliant; they actively find tax-saving opportunities you'd likely never spot yourself. That expertise brings incredible peace of mind.

When Should I Hire an Accountant?

The best time is right at the start. Seriously. Before you’ve even made your first sale. Bringing an accountant on board from day one is one of the smartest moves you can make.

Why so early? Because they can help you:

- Pick the right business structure (sole trader vs. limited company) for maximum tax efficiency.

- Get your bookkeeping system set up properly from the get-go.

- Make sure you’re registered for all the right things, like VAT or PAYE, if needed.

Getting this foundation right prevents a world of future headaches and costly mistakes that are a nightmare to unravel later on.

"The U.S. tax code is complicated, and most business owners are not tax experts. Misunderstanding tax regulations may lead to severe legal issues, audits and debts."

That quote hits the nail on the head, and the same is true here in the UK. HMRC's rulebook is just as complex, which makes having an expert in your corner from the beginning a crucial part of your defence.

What's the Difference Between a Bookkeeper and an Accountant?

This is a classic point of confusion, but the two roles are quite different. Think of a bookkeeper as the person who meticulously records your business's day-to-day financial story as it happens. They handle invoices, track bills, and reconcile your bank statements to create a clean, accurate record.

An accountant then takes that organised data and uses it for bigger-picture thinking. They’re the ones who analyse the numbers, prepare your year-end accounts, file your tax returns, and offer strategic advice on how to grow your business and be more tax-efficient.

Here’s a simple way to remember it: a bookkeeper records your financial past, while an accountant helps you plan for a more profitable future.

At Stewart Accounting Services, we do more than just tick the compliance boxes – we become a strategic partner in your financial journey. If you’re ready to reclaim your time, boost your profits, and gain real clarity, it’s time to talk. See how our expert team can fuel your business growth by visiting us at Stewart Accounting Services.