Picture this: instead of drowning in receipts and complex calculations for your VAT return, you could handle it all with one simple multiplication. That’s the core idea behind the Flat Rate VAT scheme. It allows small businesses to pay a fixed percentage of their turnover to HMRC, cutting down the paperwork significantly.

The catch? You trade this simplicity for the ability to reclaim VAT on most of your business expenses.

Understanding the Flat Rate VAT Scheme

At its heart, the Flat Rate VAT scheme is a straightforward deal. You wave goodbye to the traditional method—tallying up all the VAT you've charged customers and then subtracting all the VAT you've paid on your purchases. Instead, you just apply a single, fixed-rate percentage to your total sales (including the VAT).

This system was rolled out back in April 2002 specifically to give smaller businesses a break from complex bookkeeping. To be eligible, your VAT-taxable turnover needs to be £150,000 or less (excluding VAT) for the upcoming year. It's a lifesaver for freelancers, consultants, and any business that doesn't buy a lot of stock or materials.

Essentially, the scheme is designed to estimate what you’d owe HMRC without you needing to track every single VAT-able purchase. You can read more about how it stacks up against standard VAT on no-worries.co.uk.

Key Features of the Scheme

So, how does it actually work in practice? A few core principles set it apart from standard VAT accounting. Getting your head around these is the first step in deciding if it’s the right fit for you.

- A Fixed Percentage: HMRC gives you a flat rate percentage based on your industry. This rate is calculated to reflect the typical expenses a business like yours would have.

- No Reclaiming VAT: For the most part, you can't reclaim the VAT you spend on goods and services. The lower flat rate percentage is meant to compensate for this.

- Simple Sums: Calculating your VAT bill is as easy as it gets: just multiply your total VAT-inclusive turnover by your flat rate percentage.

- First-Year Discount: As a welcome bonus, most businesses get a 1% discount on their flat rate for their first year of being VAT registered. This can make it particularly appealing for new businesses.

The official GOV.UK page is the best place to find the full details, rules, and how to apply.

As you can see from the government's site, the first step is always checking that your turnover is £150,000 or less. From there, you'll need to find the specific rate for your business type, which is the cornerstone of the whole scheme.

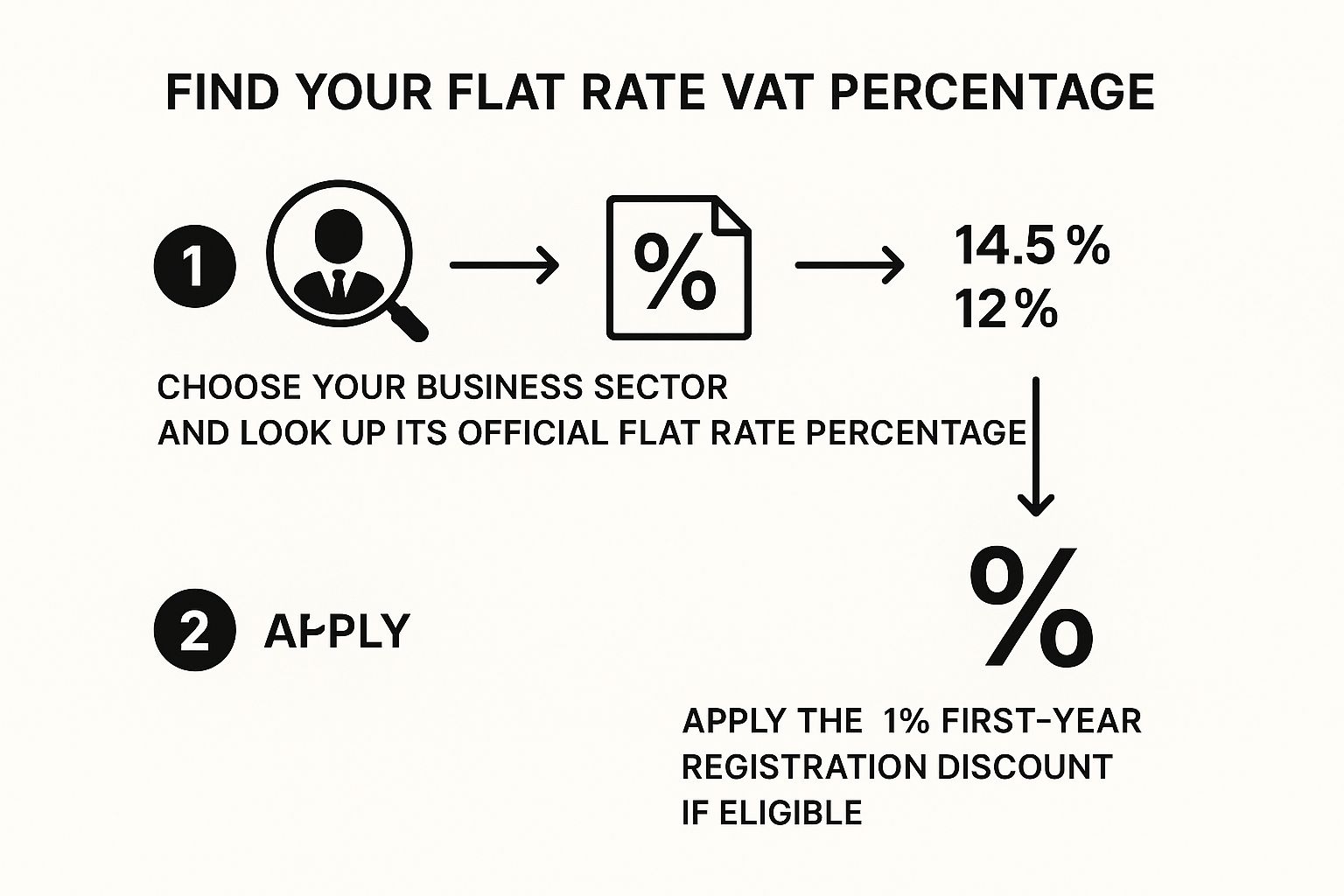

Finding Your Flat Rate VAT Percentage

The whole Flat Rate VAT scheme hinges on one number: your specific flat rate percentage. This isn't a one-size-fits-all figure. Instead, HMRC has a list of different percentages for different business sectors, which are designed to reflect the typical expenses a business in that industry would have.

Getting this right is absolutely critical. The business category you choose directly sets the percentage you'll pay, so picking the wrong one is a classic misstep that can lead to you paying too much or too little VAT. Take the time to find the description that genuinely matches what your business does day-to-day.

How to Find Your Rate

To work out what you’ll pay, you need to find your business on HMRC's official list of categories. For example, an IT consultant would look for "Computer and IT consultancy or data processing" and find their rate is 14.5%. A freelance writer would fall under "Journalism or artist" with a rate of 12.5%.

The process is pretty simple once you know where to look.

This infographic lays out the three key steps: finding your business type, grabbing the right percentage, and remembering to apply that handy first-year discount.

As you can see, it boils down to identifying your sector correctly, finding the matching rate, and making sure you don't miss out on that valuable first-year reduction.

The First-Year Discount: Don't Miss Out

To encourage businesses to join, HMRC offers a nice little incentive. For your first year of being VAT registered, you get a 1% discount on your flat rate. It's a simple way to give your cash flow a bit of a boost right when you need it.

So, if your standard rate is 12%, you'd only pay 11% for the first 12 months. Just remember, this discount starts from the date your VAT registration becomes effective, not necessarily from the day you join the scheme.

It’s a straightforward but effective way to ease you into the world of VAT. Forgetting to apply this discount is a common mistake, and it's like leaving cash on the table that could be put to much better use in your business.

This introductory offer is a clear sign that the scheme is built to help smaller businesses. But it's vital to remember it's a one-off. Once your first anniversary of being VAT registered passes, you'll need to start using the standard percentage for your sector. Make sure you factor that change into your financial planning.

Common Flat Rate VAT Percentages by Business Type

To give you a better idea, we've pulled a selection of official HMRC flat rate percentages for various business types. This should help you get a feel for where your business might fit. And remember, you can knock a further 1% off these rates for your first year.

| Business Type | Flat Rate Percentage | First-Year Rate |

|---|---|---|

| Accountancy or bookkeeping | 14.5% | 13.5% |

| Advertising | 11.0% | 10.0% |

| Business services not listed elsewhere | 12.0% | 11.0% |

| Computer and IT consultancy or data processing | 14.5% | 13.5% |

| Estate agency or property management | 12.0% | 11.0% |

| Journalism or artist | 12.5% | 11.5% |

| Management consultancy | 14.0% | 13.0% |

| Photography | 11.0% | 10.0% |

| Pubs | 6.5% | 5.5% |

| Retailing food, confectionery, tobacco, newspapers or children’s clothing | 4.0% | 3.0% |

| Secretarial services | 13.0% | 12.0% |

This is just a small sample, so be sure to check the complete list on the GOV.UK website to find the exact category and rate that applies to your business activities.

How to Calculate Your Flat Rate VAT

Working out what you owe HMRC under the Flat Rate Scheme is one of its biggest perks – it's incredibly straightforward. Forget the usual headache of tracking and subtracting VAT on every purchase. Here, it’s all about one simple multiplication.

https://www.youtube.com/embed/7mzDyPw7Jk8

The magic formula is: VAT-Inclusive Turnover x Your Flat Rate Percentage = VAT Due to HMRC.

The key thing to remember is that you apply your flat rate percentage to the total gross amount you've invoiced, which includes the 20% VAT you added. It’s a common mistake to apply it to the net amount, so getting this right from the start is crucial.

A Practical Calculation Example

Let's walk through an example to see how this plays out in the real world.

Imagine you're an IT contractor and your industry's flat rate is 14.5%. You've just finished a project and you're raising an invoice for £5,000 plus VAT.

Here’s how the numbers stack up:

- Net Invoice Amount: £5,000

- Add Standard VAT (20%): £1,000

- Total Gross Invoice: £6,000

To figure out what you owe HMRC, you just apply your flat rate to that total figure of £6,000.

- Calculation: £6,000 x 14.5% = £870

So, for this invoice, you'd pay £870 to HMRC. The difference between the £1,000 VAT you collected and the £870 you paid – in this case, £130 – stays in your business. This is the scheme's way of compensating you for the input VAT you can't reclaim on your expenses.

For a deeper dive into different VAT calculations, you can explore our guide on how to calculate VAT.

The Limited Cost Trader Test

Before you lock in your industry's flat rate percentage, there’s a vital check you need to perform: the Limited Cost Trader test. HMRC introduced this to stop businesses with very few physical expenses from getting an unintended windfall from the scheme.

You'll be classed as a limited cost trader if your spending on 'relevant goods' is either:

- Less than 2% of your VAT-inclusive turnover in a given period.

- More than 2%, but still less than £250 per quarter (which works out to £1,000 a year).

If your business falls into this bracket, you can't use your normal industry percentage. Instead, you have to use a much higher rate of 16.5%. For many service-based businesses like consultants, freelancers, and contractors, this can wipe out most, if not all, of the financial benefit of the scheme.

Why the change? HMRC brought this rule in back in April 2017. They were concerned that businesses with virtually no goods to buy (like a consultant working from home) were making a significant profit from the scheme, which wasn't its original intention. This higher rate was designed to level the playing field.

So, what exactly are 'relevant goods'? They have to be physical items used exclusively for your business. Think office stationery, raw materials for a product, or cleaning supplies. Things like accountancy fees, software subscriptions, and rent are services, so they don't count towards the test. Getting this distinction right is absolutely critical to avoid using the wrong rate and facing a nasty surprise from HMRC down the line.

Weighing Up the Pros and Cons

Deciding if the Flat Rate VAT scheme is right for your business means looking at it from all angles. Its simplicity is often what draws people in, but you need to know exactly what you’re giving up in exchange for that convenience.

Let’s dive into the good and the bad to help you make an informed choice.

What Are the Advantages?

The biggest selling point is, without a doubt, how much simpler your bookkeeping becomes. Forget painstakingly logging the VAT from every single purchase invoice. Instead, you just do one simple calculation on your total sales each quarter.

That’s a huge time-saver, freeing you up to focus on what you do best—running and growing your business.

Another major plus is the predictability it offers. A fixed percentage means you know exactly what your VAT bill will look like, making cash flow management a whole lot easier. For some businesses, especially those with very few expenses, there's even a chance you could end up paying less to HMRC than you collect from customers.

Here's a quick rundown of the benefits:

- Dramatically Simpler Bookkeeping: You no longer need to record the VAT on every single purchase, which slashes your admin time.

- Predictable VAT Bills: Your payments are based on a fixed rate, making it much easier to budget and forecast your cash flow.

- A Potential Financial Edge: Depending on your flat rate percentage, you might pay less VAT to HMRC than what you charge, letting you keep the difference.

The real beauty of the Flat Rate VAT scheme is how it cuts down the admin headache. For a small business owner who’s already wearing multiple hats, that alone can be a massive relief.

And the Disadvantages?

Now for the other side of the coin. The scheme isn’t a one-size-fits-all solution, and the drawbacks can be significant.

The biggest stumbling block is that you cannot reclaim VAT on most of your purchases. If your business regularly buys stock, materials, or invests in new equipment, you’ll miss out on claiming back the 20% VAT on those costs. This alone can make the standard VAT scheme a much better financial option.

But the inability to reclaim VAT isn't the only risk. Imagine you have a quarter with unusually high expenses—you’re still stuck paying the same flat rate percentage on your turnover. In that scenario, you could easily end up paying more in tax than you would have under the standard scheme.

Then there are the "Limited Cost Trader" rules. If your business falls into this category, you’ll be bumped up to a much higher flat rate of 16.5%. This can instantly wipe out any financial benefit, turning the scheme into an expensive mistake, especially for service-based businesses.

It's crucial to understand the VAT advantages and disadvantages of the flat rate scheme before you jump in. You've got to weigh both sides carefully to see if it truly fits your business.

Flat Rate VAT vs Standard VAT: A Quick Comparison

To make things clearer, let’s put the two schemes head-to-head. Seeing the key differences side-by-side can really help you figure out which path is the better fit for your company's finances.

| Feature | Flat Rate VAT Scheme | Standard VAT Scheme |

|---|---|---|

| VAT Calculation | Apply a fixed percentage to your gross turnover. | Subtract VAT paid on purchases from VAT charged on sales. |

| Reclaiming VAT | Not allowed on most purchases (except certain capital assets). | You can reclaim VAT on all eligible business purchases and expenses. |

| Bookkeeping | Much simpler; no need to track VAT on individual purchases. | More complex; requires detailed records of VAT on all sales and purchases. |

| Cash Flow | Predictable, as payments are a fixed percentage of sales. | Can fluctuate significantly depending on sales and purchases in a period. |

| Best For | Businesses with low costs and few purchases (e.g., consultants, freelancers). | Businesses with high costs or significant stock purchases (e.g., retail, construction). |

Ultimately, the choice comes down to your specific business model. If you have minimal expenses, the simplicity of the Flat Rate scheme might be perfect. But if you spend a lot on VAT-able goods and services, sticking with the Standard scheme will almost certainly save you more money in the long run.

How to Join the Flat Rate VAT Scheme

So, you've decided the Flat Rate VAT scheme sounds like a good fit for your business. The appeal of simpler bookkeeping and more predictable VAT bills is strong, but how do you actually get started? The process itself is quite straightforward, but it all begins with making sure your business qualifies.

The main hurdle is your turnover. To be eligible to join, your estimated VAT-taxable turnover for the next 12 months needs to be £150,000 or less (excluding VAT). This cap is there for a reason—it keeps the scheme focused on the smaller businesses that benefit most from its administrative shortcuts.

Checking Your Eligibility

Before you jump into an application, it's crucial to double-check that you tick all the boxes. While the turnover limit is the big one, HMRC has a few other rules that could stop you from joining.

For instance, you won't be able to join the scheme if you:

- Have already been on the scheme and left it within the last 12 months.

- Were found guilty of a VAT offence, such as evasion, in the past year.

- Are closely linked with another business or have recently joined a VAT group.

You also need to think about the future. The scheme is designed for smaller businesses, so if your business grows, you'll eventually have to leave. The exit threshold is an annual turnover of £230,000 (including VAT). Keep a close eye on your figures as you approach this mark.

The Flat Rate VAT scheme was first introduced back in 2002. It works by applying a fixed percentage to your turnover, with different rates for various business sectors. These rates are calculated to account for the typical input costs in each industry, simplifying the whole process for businesses with turnovers under £150,000. For a deeper dive, you can read the official government attitudes report.

The Application Process

Once you’re sure that you meet the criteria, the application is refreshingly simple. HMRC gives you a couple of ways to apply, whether you’re registering for VAT for the very first time or just switching over from the standard method.

1. Applying Online: This is by far the quickest and easiest route. You can opt into the scheme directly through your Government Gateway account when you initially register for VAT. If you're new to this, our guide on applying for a VAT number can help you navigate the first steps.

2. Applying by Post or Email: Already VAT registered? No problem. You’ll need to fill out form VAT600FRS. Once completed, you can either email it to HMRC or pop it in the post to the address listed on the form itself.

Common Mistakes to Avoid

The Flat Rate Scheme is designed to make life easier, but a few common slip-ups can catch anyone out. Getting it wrong can lead to a headache-inducing bill from HMRC later on, so it pays to be aware of the pitfalls from the start.

Think of it as learning the rules of a new board game – once you know where the traps are, you can navigate the board with confidence. Let's walk through the three most frequent errors I see and, more importantly, how you can steer clear of them.

Applying the Wrong Percentage

This is probably the most common and costly mistake. When you join the scheme, you have to pick a business category from HMRC’s official list, and each one has a specific flat rate percentage. Choosing the wrong one throws off every single VAT calculation you make.

Take the time to read through the descriptions on the HMRC website and find the one that truly fits what your business does. If your business wears a few different hats, you need to pick the category that represents your main source of income.

Misunderstanding the Limited Cost Trader Rules

The Limited Cost Trader rules are a real tripwire, particularly for consultants, freelancers, and other service-based businesses that don't buy a lot of physical stock.

Here's the deal: if your spending on goods is less than 2% of your turnover (or under £1,000 a year), you’re classed as a limited cost trader. This means you must use the higher 16.5% flat rate, regardless of your industry. It’s not a choice. Getting this wrong means you're underpaying VAT, which can lead to penalties.

The key here is HMRC's strict definition of 'goods'. It means physical items you use in your business—think raw materials, stationery, or cleaning supplies. It does not include things like your accountant's bill, software subscriptions, or digital advertising costs.

Calculating VAT on the Wrong Figure

This one trips people up all the time. You need to apply your flat rate percentage to your VAT-inclusive turnover. That’s the total amount your customer pays you, not the pre-VAT figure.

Let's make that crystal clear with an example:

- You invoice a client for £1,000 (your net fee).

- You add the standard 20% VAT (£200).

- Your total, VAT-inclusive invoice is £1,200.

If your flat rate is 12%, you calculate your payment to HMRC based on the full £1,200. So, you owe 12% of £1,200, which is £144. Calculating it on the £1,000 net figure would be wrong and lead to underpayment. This small difference on each invoice really adds up over a year, so always double-check you're using the right starting number.

Common Questions About Flat Rate VAT

Now that we’ve covered the basics, let’s dig into some of the practical questions that pop up when you're actually using the flat rate scheme. These are the "what if" scenarios that business owners often worry about.

What if I Need to Buy Something Expensive?

This is a big one. What happens if you need to buy a new van, a high-spec computer, or a piece of machinery? Normally, you can't reclaim VAT on your purchases, but thankfully, there's a special rule for major buys.

You can actually reclaim the full VAT on a single purchase of capital goods as long as it costs £2,000 or more (VAT included). Think of it as a safety net that stops the scheme from penalising you for making a big investment to grow your business.

Just be aware that this applies to goods, not services. It also has to be a single item – you can’t bundle a few smaller purchases together to hit that £2,000 mark.

What if My Business Changes Direction?

It's common for a business to evolve. Maybe you started out as a "Management consultant" (at 14.0%) but have since shifted into "Computer and IT consultancy" (at 14.5%).

If the core of what you do changes, your flat rate percentage probably needs to change with it. It’s your responsibility to make sure you’re applying the right rate for your industry. As soon as your main business activity changes, you need to start using the new percentage. It's a good idea to review this every year or so, just to make sure you're still compliant.

What Happens if My Turnover Gets Too High?

The flat rate scheme is brilliant for smaller businesses, but it has its limits. If your business grows, you'll eventually have to leave it behind.

The magic number is £230,000. If your total business income (including VAT) tops this figure over any 12-month period, it’s time to move on. The same applies if you expect your income to go over £230,000 in the next 30 days alone.

Once you cross that line, you need to let HMRC know and switch back to standard VAT accounting at the start of your next VAT period.

Navigating VAT rules can feel like a full-time job. You don't have to figure it all out on your own. The experts at Stewart Accounting Services can take care of preparing and submitting your VAT returns, making sure you stay compliant and freeing you up to run your business. See how we can help at https://stewartaccounting.co.uk.