It’s a classic, and frankly terrifying, business puzzle: the P&L statement is showing a healthy profit, but you look at the company bank account and it’s practically empty. How on earth can you be thriving on paper yet scrambling to pay the bills?

This exact scenario is why getting your head around the cash flow statement isn't just a 'nice-to-have' for business owners—it's absolutely essential.

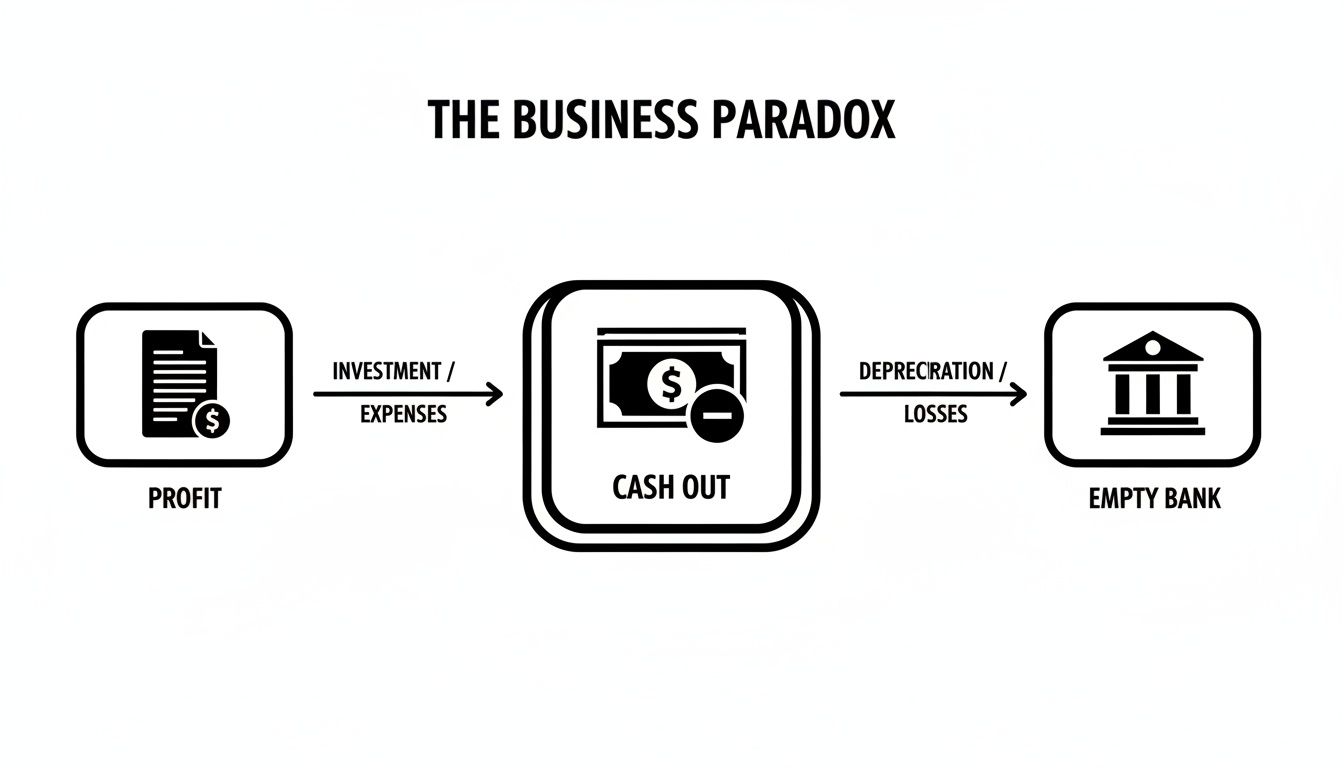

Why a Profitable Business Can Still Run Out of Cash

Let’s imagine you run a small but successful catering company. You’ve just pulled off a huge corporate event, your biggest contract yet. You’ve bought all the premium ingredients, paid your staff for their long hours, and delivered a service that wowed the client. Your profit and loss statement for the month looks incredible, reflecting a significant profit from the gig.

But here’s the rub: your client is on 60-day payment terms.

In the meantime, your own suppliers want paying, and your team's wages are due next week. All of a sudden, despite being very profitable, you have no actual cash in the bank to cover your immediate costs. This is a painfully common situation, and it perfectly highlights the crucial difference between profit and cash. Profit is an accounting measure; cash is the real-world money you need to operate day-to-day. Your survival depends on it.

The cash flow statement is a financial report that tracks the actual movement of cash, revealing the true story behind the numbers. It’s not just an accounting document; it’s your business's pulse monitor, showing its real-time liquidity and operational health.

Learning to read it properly empowers you to make smarter, more sustainable decisions. If you're keen to explore this further, there are some great strategies out there for mastering cash flow problems.

The Core Problem: Profit vs. Cash

So where does this disconnect come from? It all boils down to timing. Standard accounting rules recognise your revenue the moment it's earned (when you do the work), not necessarily when the customer’s money actually hits your account. Likewise, expenses are recorded when they are incurred, not when you pay the bill.

We've written a whole article exploring this in more detail, because it's a concept that trips up so many business owners. Check it out here: cash is not profit, and vice versa.

The cash flow statement is the tool that bridges this gap. It ignores the accounting theory and focuses purely on the cash transactions, organising them into three key areas:

- Operating Activities: The cash that comes from your core business activities—what you actually do to make money.

- Investing Activities: Cash spent on (or generated from) long-term assets, like buying new equipment or selling an old company vehicle.

- Financing Activities: Cash from external sources, such as taking out a loan, getting money from investors, or you putting your own funds into the business.

Understanding this report helps you answer the really important questions. Can we afford that new hire? Do we have enough of a cash buffer to get through a slow month? Without this insight, you're essentially flying blind.

Understanding the Three Pillars of Cash Flow

To really get to grips with a cash flow statement, you need to see it as three distinct stories, not just a jumble of numbers. Each part, or 'pillar', shines a light on a different aspect of your business, showing you exactly where your money is coming from and where it's disappearing to.

Think of it like this: your business is a reservoir. One pipe brings water in from your daily sales, another takes it out for expenses. Other pipes are for bigger, one-off events like buying a new van or getting a bank loan. The cash flow statement lets you measure the flow in every single one of those pipes.

These three pillars are Operating Activities, Investing Activities, and Financing Activities. Looking at them one by one is how you build a complete picture of your financial health.

Pillar 1: Cash from Operating Activities

This is the engine room of your business. The operating activities section shows you the cash generated from your core, day-to-day operations – the very reason you're in business in the first place. For a local bakery, this is the cash coming in from selling bread and cakes.

From that income, you subtract the cash you've paid out just to keep the lights on. This covers everything from buying flour and sugar, paying your staff's wages, to covering the rent and electricity bills.

A consistently positive number here is a fantastic sign. It means your main business activities are self-sufficient and generating enough cash to stand on their own two feet. This section is also a brilliant gauge of your company's liquidity, which is crucial for managing your business's working capital.

Pillar 2: Cash from Investing Activities

The second pillar, investing activities, is all about the future. It tracks how you're using cash to grow and improve your business over the long term. This isn't about the daily grind; it's about big-picture strategic moves.

Think of things like:

- Cash Out: Buying a new delivery van, upgrading your office computers, or paying for a shop refurbishment.

- Cash In: Selling off old machinery you no longer use or an old property.

Don't panic if you see a negative figure here. It often means you're putting money to work by investing in assets that will help you make more money later on. It's a sign of ambition.

Pillar 3: Cash from Financing Activities

Finally, the financing section shows how you're funding the business through debt and equity. It’s the story of the cash moving between the company and its owners, investors, or lenders. This is where you see how you raise money and how you pay it back.

This includes cash movements like:

- Taking out a new bank loan for expansion.

- An owner putting more of their own money into the business.

- Making repayments on existing loans.

- Paying out dividends to shareholders.

Getting your head around this is vital. Poor cash management is a business killer, and this section helps you see potential problems before they escalate. It’s a harsh reality that thousands of UK SMEs become insolvent each year simply because cash runs out, even when they’re profitable on paper.

The image below perfectly captures this common but dangerous paradox.

It’s a powerful reminder that profit is one thing, but having actual cash in the bank when you need it is something else entirely.

To help pull this all together, here's a quick summary of the three pillars.

The Three Pillars of a Cash Flow Statement

| Activity Type | What It Shows | Example Cash Inflow | Example Cash Outflow |

|---|---|---|---|

| Operating | Cash from core, day-to-day business activities. | Sales revenue from customers | Paying suppliers and staff wages |

| Investing | Cash used for long-term assets and investments. | Selling an old company vehicle | Buying new equipment or property |

| Financing | Cash flow between the business, its owners, and lenders. | Receiving a bank loan | Repaying a loan or paying dividends |

Each pillar provides a unique lens through which to view your business's performance. By understanding all three, you move beyond simply looking at profit and start truly managing the lifeblood of your company: its cash.

Choosing Between the Direct and Indirect Methods

When it comes to calculating the cash from your core operations, there are two paths you can take: the direct method and the indirect method. Both will get you to the exact same final number, but they tell a completely different story about how you got there.

Think of it like planning a journey. The direct method is like a detailed, turn-by-turn satnav route, showing every single road you took. The indirect method is more like a summary map, starting from your destination and working backwards to see how it connects to your starting point. Understanding the difference is crucial for interpreting what the numbers really mean.

The Direct Method: A Detailed Cash Tally

The direct method is the most straightforward and intuitive of the two. It’s essentially a simple tally of all the actual cash that flowed in and out of your business from its day-to-day activities.

It lists the major categories of cash movements, such as:

- Cash collected from customers.

- Cash paid to suppliers for stock and materials.

- Cash paid to employees for their wages.

This approach gives you a very clear, granular picture of your cash transactions—almost like an itemised bank statement. The downside? It requires you to track every single cash transaction meticulously, which can be a real headache if your systems aren't built for it from the ground up.

The Indirect Method: The Reconciliation Approach

The indirect method is, by a long shot, the more popular choice for UK businesses. Instead of tracking individual cash payments, it takes a more roundabout route. It starts with the net profit figure from your profit and loss (P&L) statement and then makes a series of adjustments to work back to the actual cash figure.

Imagine your net profit is a theoretical figure. The indirect method reconciles that theory with the cash reality. It adds back non-cash expenses (like depreciation, which reduces profit but doesn't actually involve cash leaving your bank) and accounts for changes in working capital, such as increases in unsold stock or money owed by customers.

The real power of the indirect method is that it explicitly connects your reported profit to your cash position. It brilliantly answers that all-too-common question: "If we made a profit, where did all the cash go?"

Because it bridges the gap between the P&L and the balance sheet, most accountants and financial analysts find it far more insightful. It gives you a deeper analytical view, showing how changes in your operational efficiency are affecting your cash balance.

Deciding which to use often comes down to practicality versus detail. While you can get a detailed walkthrough from this practical guide to preparing a cash flow statement, the consensus is clear. The direct method might be conceptually simpler, but the indirect method’s ability to reconcile profit with cash provides far richer insights into your working capital, making it the standard for any serious financial analysis.

How to Read the Story Your Cash Flow Is Telling

Think of a cash flow statement less as a stuffy accounting report and more as a story about your business’s journey. It reveals its health, its ambitions, and where it’s heading. Learning to read this story is one of the most vital skills you can master as a business owner, taking you beyond surface-level profit to understand what’s really happening with your money.

Each of the three sections—Operating, Investing, and Financing—is a different chapter. When you analyse them together, a clear picture emerges, allowing you to pinpoint problems, seize opportunities, and make decisions with real confidence. The trick is knowing what to look for.

Analysing Cash from Operating Activities

This is the heart of the story. A strong and consistently positive cash flow from your operations is the clearest sign of a fundamentally healthy business. It means your core mission—selling your goods or services—is bringing in more than enough cash to keep the lights on and then some.

On the flip side, a negative number here should set alarm bells ringing. If your day-to-day business is losing cash, it's not a sustainable situation. It could be a symptom of anything from customers paying too slowly to bloated overheads or poor stock management.

The gold standard for any business is to generate enough cash from its operations to cover all its other needs. If you’re constantly relying on loans or selling assets just to pay the bills, something is wrong.

Decoding Investing and Financing Activities

These next two chapters reveal your strategy and your long-term vision. A negative cash flow from investing isn’t always a bad thing; in fact, it's often a sign of ambition. It usually means you're putting money back into the business to fuel growth—buying new equipment, securing property, or developing technology. A positive figure, however, might suggest you're selling off assets, either to raise emergency cash or as part of a strategic pivot.

The financing section tells you how you’re funding everything. A positive flow shows you've brought money in, maybe through a bank loan or by issuing shares. A negative flow means money is going out, perhaps to repay debt or pay dividends to shareholders. The context here is everything. Are you borrowing to fund a smart expansion, or are you taking on debt just to make payroll?

A Quick Example for a UK Startup

Let's look at a fictional UK tech startup, "InnovateUK Ltd," to see how this plays out. Here’s a simplified summary of their cash flow:

| Activity Section | Net Cash Flow | What It Tells Us |

|---|---|---|

| Operating Activities | £45,000 | The core business is generating a healthy amount of cash. A brilliant sign. |

| Investing Activities | -£70,000 | They're investing heavily, likely in new servers or software. This points to a focus on growth. |

| Financing Activities | £30,000 | To support that investment, they've taken on external funding like a loan or investor capital. |

| Net Change in Cash | £5,000 | Despite the big investment, their overall cash balance has still increased. This is controlled, well-managed growth. |

This snapshot tells a powerful story. InnovateUK has a profitable core business that it’s using, along with some smart financing, to invest aggressively in its own future. This is the narrative of a confident, growing company. Once you learn to read your own what is a cash flow statement, you gain this same level of insight, giving you the power to guide your business with true clarity.

Right, let's get one thing straight. Just knowing what a cash flow statement is puts you leagues ahead of many business owners. But knowing isn't the same as doing. The real trick is using that knowledge to sidestep the common traps that sink otherwise healthy businesses.

Think of it this way: awareness is your first line of defence. So many companies make the same handful of mistakes, and the consequences can be brutal. Let's walk through the big ones so you can spot them a mile off.

Mistake #1: Confusing Profit with Cash

This is the big one, the classic blunder we mentioned earlier. Your Profit & Loss statement is glowing, showing a hefty profit, so you assume the bank account must be overflowing. It's an easy mistake to make, but a dangerous one. Profit is an accounting measure; cash is the actual money you need to pay your staff, your landlord, and your suppliers.

How to avoid it: Simple. Get into the habit of reviewing your cash flow statement every single month, right alongside your P&L. Give it the same weight and attention. This alone will give you a much clearer picture of your real financial health.

Mistake #2: Not Forecasting

Trying to run your business by only looking at last month's numbers is like driving a car by staring exclusively in the rearview mirror. It tells you where you’ve been, but not where you're headed. Without a cash flow forecast, you're flying blind, unable to see cash crunches coming or spot the right time to invest in growth.

A cash flow forecast is your financial radar. It lets you play out different 'what-if' scenarios, spot potential gaps in your bank balance, and make smart decisions before a small problem escalates into a full-blown crisis.

How to avoid it: Start with a 13-week cash flow forecast. It’s the gold standard for a reason. Update it every week with what you expect to come in and what needs to go out. This gives you a three-month window, which is usually plenty of time to react if you see trouble brewing.

A Few Other Bear Traps to Sidestep

Beyond those two major pitfalls, a couple of other classic errors can really put the squeeze on your cash.

- Overinvesting in fixed assets: Buying that shiny new van or piece of equipment might feel like a big step forward. But if it drains all your ready cash, you could find yourself unable to cover the day-to-day bills. It’s a surprisingly common way to choke a perfectly good business.

- Letting your invoices gather dust: Customers who pay late are, quite literally, costing you money. If you don't have a solid process for chasing payments, your 'accounts receivable' can swell up, trapping cash that should be in your bank account, working for you.

The solution to both of these comes down to discipline. Before making any large purchase, map out its impact on your forecast. For late payments, set up automated invoice reminders and have crystal-clear payment terms from the outset. Taking these small, disciplined steps transforms your cash flow statement from a historical document into a powerful, forward-looking tool for managing your business.

Proactively Improving Your Business Cash Position

Getting to grips with your cash flow statement is a fantastic first step. It tells you what’s happened. But the real power comes when you move from simply analysing the past to actively shaping the future.

The good news is there are plenty of practical levers you can pull to build a healthier cash reserve.

Many of these strategies revolve around your working capital cycle. Could you tighten up your invoicing terms to get paid faster? What about putting a more structured process in place for chasing overdue payments? On the other side of the coin, you can often renegotiate payment terms with suppliers, giving your own business a bit more breathing room.

Building a resilient, cash-positive business means treating cash flow as an active, manageable resource, not just a historical report. It’s about making small, consistent improvements that compound over time.

Turning Insights Into Actionable Strategy

While these tactics are effective on their own, you’ll see much faster results when you combine them with professional tools and expertise. This is where modern accounting support really becomes a game-changer for any ambitious small business.

Gain Real-Time Visibility: Cloud accounting software like Xero gives you an up-to-the-minute view of your cash position. No more waiting for month-end reports. This live data helps you make smarter decisions, fast.

Forecast with Confidence: A good accountant can help you build and maintain a rolling 13-week cash flow forecast. This is one of the most powerful tools in your arsenal, helping you spot potential shortfalls weeks in advance and plan big expenses without putting the business at risk.

Optimise Your Operations: An experienced advisor will look beyond the numbers, helping you find ways to free up cash tied up in your operations – from managing stock levels more efficiently to structuring finance in a smarter way.

Taking these steps means you stop being a passenger just reading your financial story. You get in the driver's seat and start writing the next, more profitable chapter.

If you’re ready to take control, our detailed guide on how to improve business cash flow is packed with even more practical tips.

Got Questions? We’ve Got Answers

Once you’ve got the basics down, a few common questions always seem to come up. Let's tackle them head-on to help you get comfortable with putting your cash flow statement to work.

How Often Should I Be Looking at This Thing?

For most small to medium-sized businesses, running your eye over the cash flow statement once a month is a great habit. It’s the perfect frequency to catch trends as they're developing, get ahead of any potential issues, and generally avoid nasty surprises.

That said, if your business is going through a period of rapid growth, deals with seasonal peaks and troughs, or is navigating a shaky economy, you’ll want to ramp that up to a weekly review. When things are moving fast, that extra vigilance gives you the real-time insight you need to make smart, nimble decisions.

What's the Difference Between a Cash Flow Statement and a P&L?

It’s a classic question, and here’s a simple way to think about it: your Profit & Loss (P&L) statement tells you if you're profitable, but the cash flow statement tells you if you're liquid.

The P&L is great at showing revenues you’ve earned and expenses you’ve racked up, even non-cash ones like depreciation. The cash flow statement is far more direct – it only cares about actual money hitting or leaving your bank account. You can easily have a fantastic P&L showing healthy profits, but if your clients are slow to pay their invoices, you could still be struggling for cash. You really need to look at both to get the full story of your financial health.

Can I Just Do This Myself?

Technically, yes, you can piece together a cash flow statement with a spreadsheet. But honestly, it gets messy fast, especially if you're using the indirect method. One small mistake can throw all the figures off, potentially leading you to make a poor decision based on bad data.

Accounting software like Xero certainly makes the job easier by automating a lot of the donkey work. But nothing replaces the expertise of a professional. An accountant doesn’t just ensure the numbers are spot on; they help you read between the lines and understand the story your cash flow is telling, turning data into a genuine plan for growth.

Getting to grips with your cash flow is the secret to building a business that can weather any storm. At Stewart Accounting Services, we do more than just crunch the numbers – we help you use them to make confident, forward-thinking decisions.