Think of small business bookkeeping services as your financial command centre. They do far more than just wrangle receipts; they organise your entire financial world, giving you a crystal-clear, up-to-the-minute view of your business's health. This clarity is what allows you to make confident, smart decisions every single day.

Why Bookkeeping Is Your Business’s Financial Compass

Trying to run a business without proper financial records is like trying to navigate a ship in a storm without a compass. You’re essentially guessing, and that’s a massive gamble. For the millions of small businesses that are the lifeblood of the UK economy, having organised finances is often the dividing line between just about surviving and actually thriving.

Good bookkeeping isn't just about ticking a compliance box. It’s the central nervous system that monitors your company's financial wellbeing, and this is especially true for tiny startups trying to manage limited resources during their first crucial growth spurts. It provides the hard data you need to steer the ship, from managing daily cash flow to plotting your next big move.

The Foundation of Smart Decisions

Imagine your bookkeeper is the one laying the foundations for a house. They meticulously place every single brick—every transaction, invoice, and expense—exactly where it needs to be. Without that solid base, any attempt to build on top of it, whether that's a new marketing strategy or a budget for expansion, is going to be shaky at best.

When your financial information is properly structured, you can:

- Track Profitability: Quickly identify which of your products, services, or even clients are bringing in the most money.

- Manage Cash Flow: Get a real handle on the money coming in and going out, helping you avoid nasty cash-flow gaps.

- Secure Funding: Walk into a meeting with a bank or investor with clean, professional financial statements that inspire confidence.

- Simplify Tax Time: Say goodbye to that frantic year-end scramble. Your records will be organised and ready to go.

Precise bookkeeping isn’t about dwelling on the past. It's about giving you a sharp, accurate picture of the present so you can build a better future.

Driving the UK's Economy

It’s impossible to overstate just how important small businesses are. In the UK, small to medium-sized enterprises (SMEs) make up a staggering 99.9% of all businesses, with around 5.5 million registered at the start of 2024. They're a powerhouse, employing nearly 60% of the private sector workforce.

For these vital businesses, professional bookkeeping isn't a luxury—it's a fundamental necessity. It lays the groundwork for a more secure, more profitable future.

What a Bookkeeping Service Actually Does for You

When you hire one of the many bookkeeping services for small businesses, what are you actually paying for? The phrase "doing the books" barely scratches the surface. Think of your business as a high-performance car; a good bookkeeper is the master mechanic who keeps the engine perfectly tuned.

They don't just log what’s already happened. A professional bookkeeper organises your financial present so you have a crystal-clear view of the road ahead. This involves a whole series of connected tasks designed to keep your financial engine running smoothly, helping you dodge costly breakdowns and reach your goals.

Without this expert oversight, it’s like driving with the check engine light flashing—you might be completely unaware of a serious problem until it’s far too late. So, let’s lift the bonnet and see what a professional bookkeeper really delivers.

Core Bookkeeping Services for UK Small Businesses

A bookkeeper’s role is far more than just data entry. They manage the fundamental financial pillars of your company, ensuring accuracy, compliance, and clarity. The table below breaks down the essential services you can expect.

| Service Component | Description | Why It's Important |

|---|---|---|

| Sales Ledger Management | Tracking all sales invoices, monitoring payments from customers, and chasing overdue accounts. | This is all about your cash flow. Without it, you don't know who owes you money, which can starve your business of vital funds. |

| Purchase Ledger Management | Recording all bills and expenses from suppliers and managing payment schedules. | Keeps your supplier relationships strong, helps you manage outgoing cash, and prevents nasty late payment fees. |

| Bank Reconciliation | Methodically matching every transaction on your bank statements with the entries in your accounting software. | This is your ultimate accuracy check. It confirms your financial records are a true reflection of reality, catching errors and potential fraud. |

| VAT Returns | Calculating the VAT you owe to (or can reclaim from) HMRC and submitting your quarterly returns. | Non-negotiable for VAT-registered businesses. Getting this wrong leads to hefty penalties and investigations from HMRC. |

| Payroll Processing | Managing employee wages, calculating tax and National Insurance, issuing payslips, and handling pension contributions. | Ensures your team is paid correctly and on time while keeping you compliant with complex UK employment and tax laws. |

| Financial Reporting | Preparing key reports like the Profit & Loss (P&L) statement and Balance Sheet. | These reports are your dashboard. They tell you if you're making a profit, what your business is worth, and where the money is going. |

These core tasks form the bedrock of sound financial management. They provide the reliable data needed for you to make smart, informed decisions about your business's future.

Diving Deeper: Reconciliation, VAT, and Payroll

Let's unpack a few of those critical tasks. Bank reconciliation, for instance, sounds simple but is one of the most important jobs a bookkeeper does. Think of it like balancing your personal chequebook, but for hundreds or even thousands of business transactions. They ensure every penny is accounted for.

A reconciled bank statement is your proof that the financial records are accurate and trustworthy. It's the ultimate source of truth for your business's cash position.

This process is absolutely essential. It guarantees your financial reports are based on fact, not guesswork. Good bookkeeping also often includes efficient document management for small businesses to keep every receipt and invoice organised and secure.

Then there’s VAT and payroll. For most UK businesses, these are two of the biggest administrative headaches.

A bookkeeper will make sure your sales and purchases are correctly categorised for VAT, applying the right schemes and preparing your quarterly returns for HMRC. This alone saves countless hours and prevents costly compliance mistakes.

If you have staff, payroll is another minefield. A bookkeeper handles it all:

- Calculating wages, tax, and National Insurance.

- Processing payslips and managing pension auto-enrolment.

- Submitting all the required reports to HMRC.

Handing these specialist, compliance-heavy jobs over to an expert doesn't just reduce risk—it frees you up to focus on what you actually love doing: running and growing your business.

Choosing Your Path: In-House vs. Outsourced Bookkeeping

Deciding who manages your company's books is one of the most critical choices you'll make as a small business owner. Should you hire a dedicated bookkeeper in-house, try to wrangle the numbers yourself, or partner with an external service? The answer has a direct impact on your budget, your time, and how easily your business can grow.

There’s no one-size-fits-all solution here. The right path depends entirely on your business model, how many transactions you handle, and where you want to be in a few years. A freelance consultant with a handful of clients has completely different needs from a fast-growing e-commerce shop processing hundreds of orders a month. Getting this right comes down to understanding the trade-offs between cost, expertise, and your own time.

The In-House and DIY Approaches

Handling bookkeeping yourself or hiring an employee gives you direct, hands-on control. For very small businesses or sole traders, DIY bookkeeping with modern software can feel like the most sensible option, especially when every pound counts. You’ll definitely gain an intimate understanding of your financial pulse.

Hiring an in-house bookkeeper takes this a step further. This person becomes a dedicated part of your team, fully immersed in your company culture and day-to-day operations. They’re right there to answer questions and can often handle other administrative tasks beyond just the books.

But both of these routes come with some serious responsibilities.

- Time Commitment (DIY): Even with the most user-friendly software, bookkeeping demands real time and focus. As your business grows, this can quickly eat into the time you should be spending on what you do best—running the business.

- Cost of Employment (In-House): Hiring an employee isn't just about their salary. You have to factor in National Insurance contributions, pension schemes, holiday pay, and ongoing training costs.

- Expertise Limitations: A single person, whether it's you or an employee, might not have the specialist knowledge needed to navigate complex VAT schemes or tricky industry-specific compliance rules.

The Power of Outsourced Bookkeeping Services

Outsourcing means partnering with a professional firm that provides expert bookkeeping services for small businesses. This model grants you access to a team of qualified pros without the overheads and responsibilities of hiring. You pay for the service you need, which can be easily scaled up or down as your business changes.

This approach offers a powerful mix of expertise and flexibility. An outsourced team has seen it all, working with countless businesses in different sectors. They often spot opportunities or flag risks that an in-house person might miss simply because they live and breathe financial regulations every single day.

Choosing to outsource is like swapping a single, all-purpose screwdriver for a full, specialised toolkit. You get the right expert for every specific financial job, from VAT submissions to payroll management.

This kind of specialisation is proving invaluable in the current economic climate. A recent survey revealed that an incredible 83% of UK SMEs found that professional bookkeepers helped them reduce the negative impact of inflation. By providing precise, up-to-date records, these experts help businesses keep a close eye on cash flow, rein in expenses, and find crucial cost-saving opportunities. You can explore the full findings on these UK business trends to understand more.

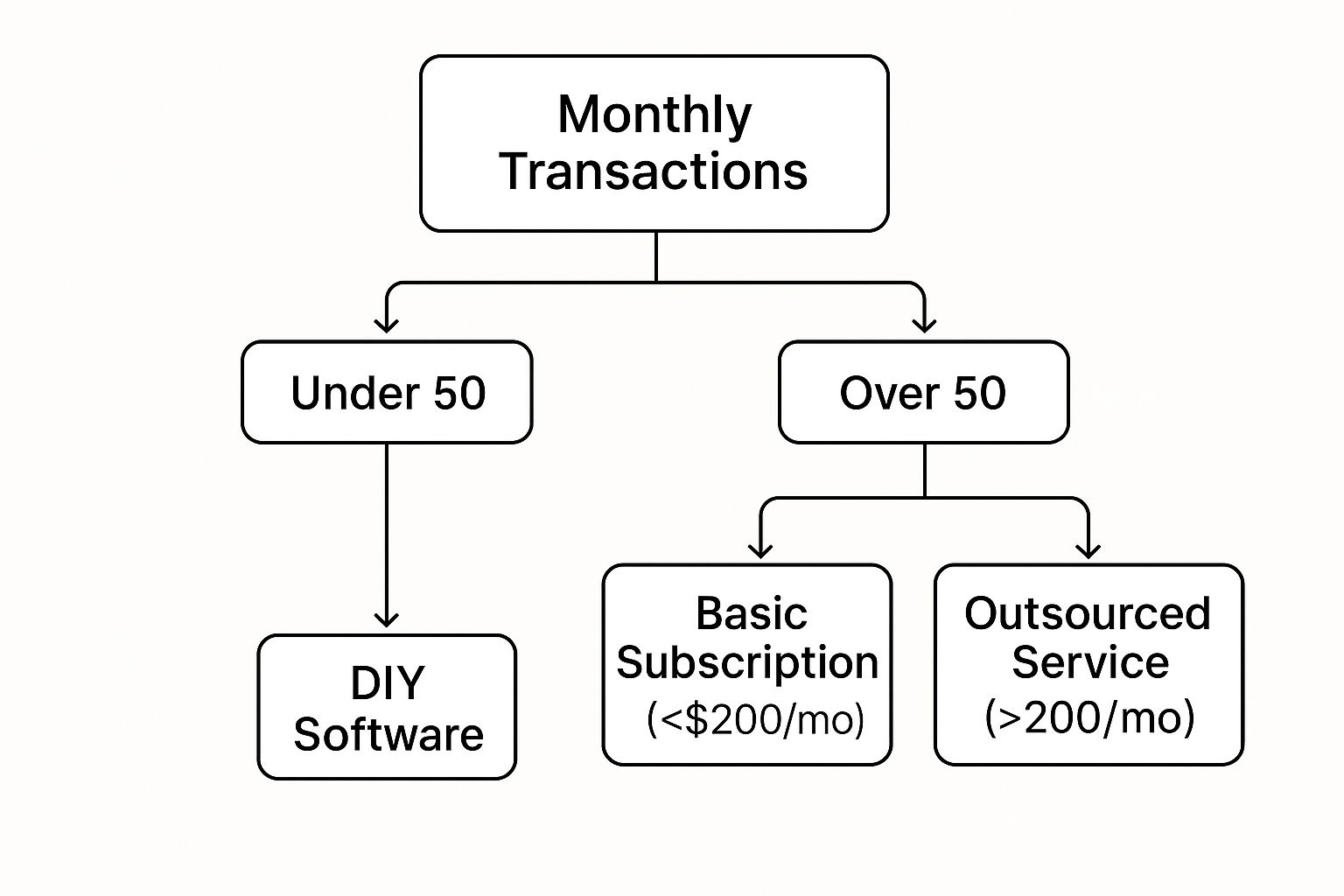

Making the Right Choice for Your Business

To figure out the best path for you, take an honest look at your current situation and your goals for the future. The infographic below offers a simple framework to help you decide, based on your transaction volume and budget.

As the decision tree shows, the more financially complex your business becomes, the clearer the value of a professional, outsourced service gets.

Ultimately, your choice boils down to a strategic look at three core factors: cost, time, and expertise.

| Factor | In-House / DIY Approach | Outsourced Service Approach |

|---|---|---|

| Cost | Seems cheaper at first (DIY) but has high hidden costs (hiring, benefits, training). | Transparent, predictable monthly fees. You avoid all employment overheads and pay only for what you use. |

| Time | Demands a significant chunk of the owner's time (DIY) or requires managing an employee. | Frees up the owner's time completely, letting them focus on core business activities and growth. |

| Expertise | Limited to one person's knowledge. May lack specialist skills in areas like tax or compliance. | Access to a team of certified professionals with broad industry experience and current knowledge. |

For so many small business owners, the real "cost" of doing their own bookkeeping isn't measured in pounds, but in lost opportunities. Every hour spent reconciling accounts is an hour not spent talking to customers, creating new products, or leading your team. An outsourced service isn't just another expense; it's an investment in your own efficiency and the future of your business.

How Modern Cloud Software Powers Your Bookkeeping

Gone are the days of shoeboxes overflowing with receipts and ledgers filled with manual entries. Technology has completely transformed bookkeeping, turning it from a tedious chore into a powerful tool for making smart business decisions. Modern cloud platforms like Xero, QuickBooks, and FreeAgent are at the heart of this change. They’re much more than just digital record books; think of them as a financial co-pilot for you and your bookkeeper.

These tools plug directly into the pulse of your business. They automate mind-numbing data entry, serve up instant financial reports, and connect smoothly with your bank accounts and sales systems. This fundamental shift has changed how bookkeeping services for small businesses work, saving huge amounts of time while delivering far more accurate information.

The Automation That Changes Everything

Imagine your bookkeeper never has to manually type in another transaction from a bank statement. That’s not a dream; it's the reality of cloud software. The star of the show is a feature called automated bank feeds, which securely pulls transaction data straight from your bank into your accounting software every single day.

This connection does more than just save time—it’s a massive step up in accuracy. It slashes the risk of human error, meaning no more typos or missed entries that could throw your entire financial picture out of whack. Your bookkeeper can then spend their valuable time checking and categorising the information, not just inputting it.

The numbers show just how big this shift is. Cloud accounting software is becoming the norm, and it's making life easier for millions. In fact, 64% of business owners now handle their own books, a trend made possible by software that automates key tasks. This explosion in demand has even helped cloud bookkeeping companies see an average 15% revenue bump. You can discover more insights about bookkeeping trends on llcbuddy.com.

Must-Have Features for Your Business

When you’re looking at cloud software, a few features deliver the biggest bang for your buck. These are the tools that genuinely simplify your day-to-day operations and bring real clarity to your finances.

Make sure any platform you choose offers:

- Automated Bank Feeds: As we’ve said, this is non-negotiable. It’s the bedrock of accurate, up-to-date bookkeeping.

- Receipt Capture: Most platforms have a mobile app that lets you just snap a photo of a receipt. The software reads the important details and creates an expense entry for you. Simple.

- Invoice Creation and Tracking: You can create professional invoices, email them to clients, and see when they’ve been opened and paid—all in one place.

- Real-Time Reporting: Need to see your Profit & Loss statement or Balance Sheet? You can generate these crucial reports in a couple of clicks to get an instant snapshot of your business's health.

Think of cloud software as the financial dashboard for your business. It pulls all the vital signs—sales, expenses, cash flow, profitability—into one easy-to-read display.

This screenshot from Xero's UK homepage shows just how cleanly these platforms present your financial overview.

The dashboard instantly gives you the important numbers: bank balances, what you’re owed, what you owe, and more. It’s a financial health check at a glance.

A Shared Workspace for You and Your Bookkeeper

Perhaps the biggest game-changer is how cloud software improves the relationship between you and your bookkeeper. Instead of dropping off a pile of paperwork once a month, you both work within the same system, looking at the same live data.

This collaborative way of working means your bookkeeper can spot potential problems or opportunities as they arise, not weeks after the fact when it might be too late.

How it Works in Practice

- Shared Access: You give your bookkeeper their own secure login. They can access your accounts from their office, and you can see what’s happening from yours.

- Instant Communication: If a transaction looks odd, your bookkeeper can leave a comment right on it inside the software, flagging it for you to clarify. No more back-and-forth emails.

- Proactive Advice: With their finger on the pulse of your finances, your bookkeeper can offer timely advice on managing cash flow, sticking to a budget, or planning for tax season.

This partnership elevates bookkeeping from a backward-looking chore to a forward-looking strategy. Your bookkeeper becomes a true advisor, using live data to help you steer the business toward growth. It’s simply a smarter, more effective way to manage your money.

How to Select the Right Bookkeeping Service

Choosing someone to manage your finances is a big deal. It’s not just about hiring a number-cruncher; it’s about finding a partner who gets your vision and can help you get there. Think of them as a key member of your team. With so many bookkeeping services for small businesses out there, how do you find the one that’s right for you?

It’s tempting to just look at the price, but that’s a mistake. You need a structured approach that looks at qualifications, real-world experience, and even how well you get along. A great bookkeeper gives you the financial clarity to make smart, confident decisions.

Assess Professional Qualifications and Credentials

First things first, check their credentials. In the UK, bookkeeping is a regulated profession, so you’ll want to see affiliations with professional bodies. This isn’t just a formality; it’s your guarantee of quality, expertise, and ethical standards.

Look out for these key qualifications:

- AAT (Association of Accounting Technicians): This is a gold standard, showing a solid, practical grasp of accounting and bookkeeping.

- ICB (Institute of Certified Bookkeepers): As the world’s largest bookkeeping institute, an ICB certification is a global mark of professionalism and integrity.

A certified bookkeeper isn’t just someone who is good with numbers. Their qualification proves they are committed to professional standards, continuous learning, and upholding a strict code of ethics.

These certifications mean your bookkeeper has been properly trained, tested, and is obliged to keep up with ever-changing regulations and tax laws. It’s a simple check that weeds out the amateurs from the pros.

Look for Relevant Industry Experience

Qualifications are the foundation, but industry-specific experience is where the real value lies. The fundamentals of bookkeeping are the same everywhere, but every sector has its own quirks, financial hurdles, and compliance hoops to jump through.

For example, an e-commerce business needs someone who understands payment gateways, stock control, and online sales tax. That’s a world away from a construction firm that has to navigate the complexities of the Construction Industry Scheme (CIS). A bookkeeper who has worked with businesses like yours will hit the ground running, make fewer mistakes, and offer advice that’s actually useful.

As you consider potential partners, it's also vital to ask about their security protocols. Safeguarding your financial data is paramount, so understanding their approach to things like Business Email Compromise prevention is a non-negotiable part of the vetting process.

Key Questions to Ask Potential Providers

Once you've got a shortlist, it's time for a proper chat. This is your chance to see what they’re really like—their process, their communication style, and whether they’ll be a good fit for your company’s culture.

Here are a few questions to get the conversation rolling:

-

Which accounting software are you proficient in? Most pros are masters of cloud software like Xero or QuickBooks. Make sure they use a platform that works with your existing systems, or that they can help you move over smoothly.

-

How do you prefer to communicate, and how often will we be in touch? This is crucial. If you need quick answers over the phone but they only work via email, it’s going to cause friction. Get this sorted out from the start.

-

Can you describe your process for monthly reconciliation and reporting? Ask them to walk you through it. This will clarify what they do each month and what you’ll need to provide, like bank statements or receipts.

-

What reports will I receive, and how will you help me understand them? A good bookkeeper doesn't just email you a spreadsheet and disappear. They should be able to sit down with you and explain what the Profit & Loss statement actually means for your business.

-

How do you structure your fees? Do they charge by the hour or offer fixed-fee monthly packages? For most small businesses, a fixed monthly fee is ideal. It makes budgeting predictable and means you won’t get a surprise bill.

Finding the right bookkeeping service isn't about just ticking a box. It’s about building a relationship with a financial expert who’s genuinely invested in your success. Taking the time to choose carefully will pay off enormously, giving you the clarity and peace of mind you need to focus on growth.

Your Top Bookkeeping Questions Answered

Deciding to bring in a professional bookkeeper is a big step, and it's only natural to have a few questions swirling around. Getting clear answers is the key to feeling confident about your choice. Here, we'll tackle the most common queries we hear from business owners, breaking everything down into plain English.

We'll cover everything from costs to the nitty-gritty of who does what, giving you the practical insights you need to move forward.

How Much Do Bookkeeping Services Cost in the UK?

It’s the question on every business owner’s mind: what’s the damage? The honest answer is, it depends. The price really hinges on your business's size, how many transactions you process each month, and just how complex your financial picture is.

A freelance bookkeeper, for instance, might charge by the hour—typically somewhere between £25 and £40 per hour. This can be handy for a one-off clean-up job, but most small businesses get far more value from a predictable, fixed-fee monthly package.

These monthly plans give you a clear, consistent cost, which makes budgeting a whole lot easier. Here’s a rough guide to what you can expect:

- Basic Package (£100 – £300 per month): This is a great fit for smaller businesses or sole traders. It usually covers the essentials like bank reconciliation and quarterly VAT returns.

- Comprehensive Package (£400 – £700+ per month): If your business is growing, has employees, and a higher volume of transactions, this level of service will often include payroll, more detailed financial reports, and closer support.

Always insist on a detailed, itemised quote before signing anything. This makes sure there are no nasty surprises and you know exactly what you’re paying for. It’s the foundation of a transparent, trusting partnership.

What Is the Difference Between a Bookkeeper and an Accountant?

This one trips a lot of people up, but the roles are actually quite distinct, though they work hand-in-hand. Think of it like building a house: the bookkeeper is the master builder, laying a perfect, solid foundation brick by brick. The accountant is the architect who uses that strong foundation to design the rest of the building and ensure it stands the test of time.

A bookkeeper lives in the day-to-day details of your finances. Their job is to meticulously record, categorise, and reconcile every single transaction your business makes. They are the guardians of your financial present, making sure every penny is accounted for accurately and right now.

An accountant, on the other hand, steps back to look at the bigger picture. They analyse the pristine data organised by the bookkeeper to offer strategic, forward-looking advice. Their world is year-end financial statements, corporation tax returns, and smart tax planning strategies.

In short, a bookkeeper manages the "now," and an accountant helps you plan for the "future." You really do need both for a healthy business.

How Often Should My Books Be Updated?

The perfect rhythm for updating your books really depends on the pace of your business. That said, for the vast majority of small companies, monthly bookkeeping is the gold standard. This regular check-in gives you an accurate, up-to-date snapshot of your financial health.

With monthly updates, you can manage your cash flow properly, make smart decisions based on real numbers, and spot little problems before they snowball into big ones. It’s the sweet spot between staying on top of things and keeping costs reasonable.

Of course, some businesses have different needs:

- Weekly Updates: If you have a high volume of transactions, like a busy retail shop or an e-commerce store, weekly bookkeeping is often a lifesaver. It gives you a much tighter grip on your finances.

- Quarterly Updates: At the bare minimum, your books have to be reconciled every quarter. This is essential for preparing and submitting your VAT returns to HMRC on time.

Leaving everything until the end of the financial year is a recipe for chaos. It guarantees a mountain of stress, a much higher chance of mistakes, and a year's worth of missed opportunities to make tax-savvy decisions. Consistency is everything when it comes to financial clarity.

At Stewart Accounting Services, we know that no two businesses are the same. We offer bookkeeping, payroll, and accounting solutions designed to give you more time, more money, and complete peace of mind. Whether you're a sole trader wrestling with self-assessment or a growing limited company, our team of Chartered Accountants is here to back you. Learn more about our services at stewartaccounting.co.uk and let us handle the numbers, so you can get back to doing what you do best.