Every year, you have a tax-free allowance for the profits you make when selling certain assets. This is officially called the Annual Exempt Amount (AEA), but you can think of it as your personal capital gains tax allowance.

For the 2024/25 tax year, this allowance is set at £3,000 for individuals and personal representatives. For most trusts, it's half that, at £1,500. While it's a critical part of financial planning, this tax-free buffer has been shrinking fast.

What Is The Capital Gains Tax Allowance?

Think of the capital gains tax allowance as your personal tax-free shield. Much like your personal savings allowance protects interest you earn, the AEA shields a portion of the profit—the 'gain'—you make when you sell, gift, or dispose of an asset that's gone up in value.

And this isn't just for City traders. You'll likely encounter capital gains tax in many common situations, including:

- Selling a second home or a buy-to-let property.

- Cashing in shares or investments that aren't held in an ISA or PEP.

- Selling valuable personal items, like artwork or antiques, for more than £6,000.

- Passing on ownership of a family business.

It’s crucial to remember this is a yearly allowance. It resets every tax year on 6th April and works on a strict 'use it or lose it' basis. You can't carry any unused portion forward into the next year.

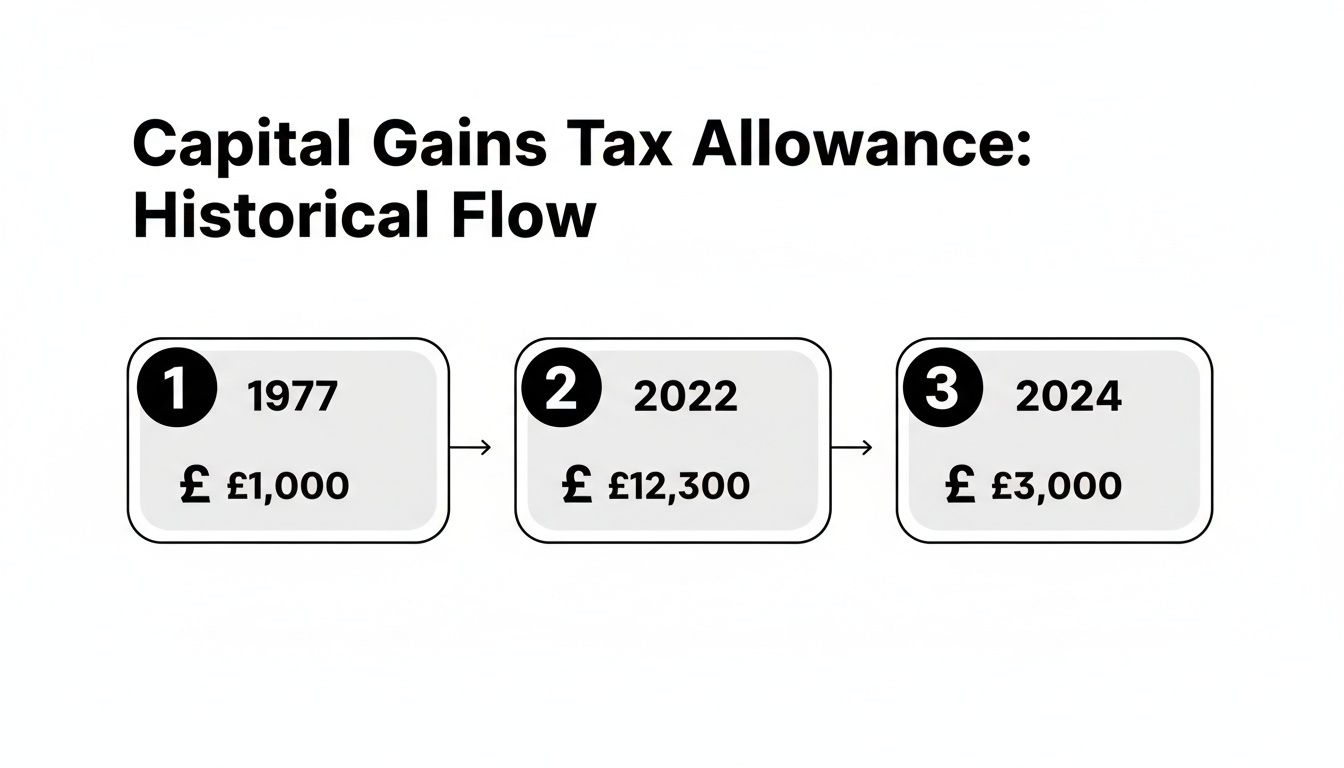

The Shrinking Shield: A Recent History

The value of this tax-free shield has seen some dramatic shifts. It started at a modest £1,000 back in 1977 but climbed steadily over the years, peaking at a generous £12,300 between 2020 and 2023.

However, recent government policy has aggressively cut it back. The 2022 Autumn Statement slashed the allowance to £6,000 for the 2023/24 tax year and then halved it again to just £3,000 from April 2024. This sharp reduction has pulled thousands more people into paying Capital Gains Tax for the first time.

The table below puts these recent changes into stark perspective.

Capital Gains Tax Allowance Thresholds Over Time

| Tax Year(s) | Individual Annual Exempt Amount | Notes |

|---|---|---|

| 2020-2023 | £12,300 | The peak of the allowance, offering significant tax-free gains. |

| 2023/24 | £6,000 | The first major reduction, more than halving the previous allowance. |

| 2024/25 | £3,000 | The current level, a 75% reduction from the 2022/23 peak. |

This dramatic drop means that proactive planning is no longer a luxury—it's essential for anyone with assets. This is especially true for property landlords and business owners in Central Scotland and across the UK.

If you're dealing with property, understanding the specific tax implications of property sales for capital gains is vital to protect your returns. You can also learn more about navigating these rules in our comprehensive guide on what UK investors need to know about Capital Gains Tax.

Calculating Your Potential CGT Liability

Working out your potential Capital Gains Tax (CGT) bill is the essential first step in smart tax planning. It’s more than just a number-crunching exercise; it shows you exactly how different decisions can impact the profit you ultimately take home. The process is logical: figure out your total gain, subtract any costs and your tax-free allowance, and then apply the right tax rate.

We’ll walk you through it. First, you establish the total gain you’ve made. From there, you deduct any allowable costs you incurred when buying, selling, or improving the asset. Finally, you take off your capital gains tax allowance to find the amount that's actually taxable.

Figuring Out Your Taxable Gain

To get started, you just need three key figures: what you sold the asset for, what you originally paid for it, and any related costs. The basic formula is quite simple:

Total Gain = Sale Price – (Purchase Price + Allowable Costs)

Those allowable costs are really important because they directly shrink your gain. They’re not day-to-day running costs, but specific expenses like:

- Solicitors' and estate agents' fees.

- Stamp Duty Land Tax you paid on the purchase.

- The cost of improvement works, like adding an extension (but not routine repairs).

Once you have your total gain, you can deduct your Annual Exempt Amount. For the 2024/25 tax year, this is £3,000. So, the final step is:

Taxable Gain = Total Gain – Capital Gains Tax Allowance

It’s this final figure that HMRC is interested in.

The chart below gives a stark visual of just how much the tax-free allowance has shifted over the years, from its introduction through to its recent peak and the sharp fall we’ve seen lately.

As you can see, the drop from £12,300 to just £3,000 has been dramatic. It means that making use of every allowable cost and relief is more crucial now than ever before.

Applying the Correct CGT Rates

The actual percentage of tax you pay on your taxable gain comes down to two main things: your Income Tax band and the type of asset you’ve sold. HMRC has different rates for basic-rate and higher-rate taxpayers, and it's a common point of confusion.

Here’s how it works: you need to add your total taxable gain to your other income for the year (like your salary or pension). If that combined total keeps you within the basic Income Tax band, you’ll pay the lower CGT rate. If it pushes you into the higher rate band, that portion of your gain is taxed at the higher CGT rate.

The asset type is the other piece of the puzzle. Gains from selling residential property are taxed more heavily than gains from other assets, like shares or business assets.

For the 2024/25 tax year, the rates for residential property are 18% for basic-rate taxpayers and 24% for higher-rate taxpayers. For all other chargeable assets, the rates are a lower 10% and 20%, respectively.

This is a particularly important distinction for our clients who are landlords, as it has a major impact on the tax due when they sell a buy-to-let property. Getting your income calculation right and applying the correct rate is absolutely vital for ensuring you don’t pay a penny more to HMRC than you need to.

Using Key Reliefs to Reduce Your Tax Bill

While the capital gains tax allowance provides a useful starting point, its impact has shrunk after the recent cuts. The real power to slash your tax bill lies in the various reliefs offered by HMRC. Think of these not as simple deductions, but as strategic tools that can postpone, reduce, or sometimes wipe out your CGT liability entirely.

For anyone running a business or investing in property, getting to grips with these reliefs is essential for protecting your hard-earned wealth. They exist to encourage certain economic activities, such as entrepreneurship and reinvestment. Let's look at the most common ones and how they work in practice.

Business Asset Disposal Relief for Entrepreneurs

Formerly known as Entrepreneurs' Relief, Business Asset Disposal Relief (BADR) is a game-changer for business owners. It’s specifically designed to reward the immense effort and risk involved in building and selling a company.

If you meet the criteria, BADR lets you pay CGT at a special rate of just 10% on gains from selling your business. This is a huge saving compared to the standard 20% higher rate that applies to most other assets.

You can claim this relief on up to £1 million of qualifying gains over your lifetime. That translates to a potential tax saving of up to £100,000 compared to paying the higher CGT rate.

To qualify, you typically need to be a sole trader or business partner. If you're selling shares, you must have owned at least 5% of the ordinary shares in a trading company and been an employee or director for at least two years right before the sale.

Private Residence Relief for Your Main Home

For most of us, our home is our biggest asset. Thankfully, when you sell your main home, any profit you make is usually completely free from Capital Gains Tax. This is all down to Private Residence Relief (PRR).

This relief applies automatically as long as the property has been your only or main home for the entire time you've owned it. You simply don't have to pay tax on the gain, which can save you a fortune.

Things can get a bit more complicated, though, if you haven't lived there for the whole period. For instance, you might find only part of your gain is tax-free if you have:

- Rented out part of your home (having a single lodger is usually fine).

- Used a section of the property exclusively for business.

- Lived away from the property for long periods.

In these cases, your relief might be restricted, leaving a portion of the gain taxable. It's worth noting there are special rules for periods of absence, like working abroad, which can still qualify for full relief.

If you've ever rented out your main home, you may also have been eligible for an additional relief. While the rules for Lettings Relief have tightened, it’s worth investigating if it applies to your situation. You can learn more about claiming lettings relief in our detailed guide.

Deferring Tax with Hold-Over and Roll-Over Reliefs

Sometimes the smartest move isn't to eliminate a tax bill, but to kick it down the road. This is precisely what Hold-Over Relief and Roll-Over Relief are for, allowing you to postpone a CGT payment until a later date.

Hold-Over Relief

This is most commonly used when you gift certain business assets, like shares in an unlisted company, to someone else. Rather than you paying CGT on the gain when you make the gift, the gain is "held over."

What this means is the person receiving the asset also inherits your original cost. They only pay CGT on the total gain—the one you made plus any further growth—when they eventually sell it. It's an incredibly useful tool for family succession planning.

Roll-Over Relief

This relief is for businesses that sell a qualifying asset (such as land or a building) and use the money to buy a new one. It lets you "roll over" the gain from the first asset into the replacement.

Instead of facing an immediate tax bill, the gain is subtracted from the cost of the new asset. This lowers its tax-deductible cost, so the deferred tax is only paid when you finally sell the new asset. This is a massive help for growing businesses that need to reinvest every penny without getting stung by tax.

Strategic Planning to Maximise Your Allowance

Knowing the rules is one thing, but putting them into practice is where you can really protect your wealth. The real key is to shift from just understanding the rules to actively planning around them. With the capital gains tax allowance having been cut so sharply, being proactive isn't just a good idea—it's essential for legally minimising what you owe HMRC.

These strategies aren't about finding complex loopholes. They're sensible, forward-thinking actions that give you control over your finances. By planning when and how you sell your assets, tax becomes a manageable part of your financial journey, not a nasty surprise.

Timing Your Asset Disposals

One of the most effective yet simplest tools in your toolbox is timing. The capital gains tax allowance resets every tax year on 6th April, and it’s strictly a "use it or lose it" deal. This simple fact opens up a huge opportunity if you're planning to sell more than one asset.

Let’s say you have a share portfolio and want to sell two different holdings, each likely to produce a gain of about £5,000. If you sell both in the same tax year, your total gain hits £10,000. After using your £3,000 allowance, you'd still have £7,000 left to be taxed.

But what if you timed it differently? By selling the first block in March (just before the 5th April year-end) and the second in April (right at the start of the new tax year), you get to use two separate annual allowances. Suddenly, each £5,000 gain is well within its respective year's allowance, potentially wiping out your CGT bill entirely.

Leveraging Spousal Transfers

Married couples and those in civil partnerships have a fantastic advantage when it comes to CGT planning. You can transfer assets to each other without creating an immediate tax bill. This is known as a 'no gain, no loss' transfer, and it provides a simple way to double your tax-free potential.

Here’s a quick look at how it works:

- Look at the Asset: Imagine one partner holds an asset with a £6,000 gain. Selling it would mean £3,000 of that gain is taxable.

- Make the Transfer: That partner can gift half of the asset to their spouse or civil partner. This transfer is completely tax-neutral.

- Sell Separately: Now, each of you owns half the asset, with a £3,000 gain each. When you both sell, each person's gain is fully covered by their own individual £3,000 allowance.

This straightforward strategy effectively doubles your combined tax-free allowance from £3,000 to £6,000. It's a perfectly legitimate and highly effective way to structure a sale.

As an investor, understanding how different taxes affect your portfolio is crucial. For those with property, navigating real estate taxes for investors can offer valuable insights to complete your financial picture.

Using Losses to Offset Gains

Let's be realistic—not every investment is a winner. While seeing a loss is never ideal, it can be a valuable tool for your tax planning. HMRC allows you to set your capital losses against your capital gains, which can dramatically reduce your final tax bill.

If you have a capital loss in a tax year, you must first use it to reduce any gains made in that same year. For example, if you realised a £10,000 gain on one asset but a £4,000 loss on another, your net gain for the year is cut to £6,000. You’d then apply your £3,000 allowance, leaving only £3,000 of the gain to be taxed.

It's absolutely vital to report any losses to HMRC, which you typically do on your Self Assessment tax return. If your losses for the year outweigh your gains, you can carry the excess loss forward to reduce gains in future years. This is why keeping meticulous records of both your wins and your losses is an indispensable habit for any smart investor.

How to Report and Pay Capital Gains Tax

Figuring out what Capital Gains Tax (CGT) you might owe is only half the battle. The other, equally important part, is reporting it correctly and paying HMRC on time. While the admin side can seem a bit intimidating at first, it's actually quite a logical process once you understand the deadlines and which reporting route applies to you.

The right way to report your gain hinges entirely on what you’ve sold. This is a critical distinction to make, as using the wrong method or missing a deadline can result in penalties. Essentially, the rules split into two main paths: one for UK residential property and another for everything else.

The 60-Day Window for UK Property

If you're a UK landlord or own a second home, this is the one deadline you absolutely cannot afford to miss. When you sell a UK residential property that results in a tax bill, you have a strict 60-day window from the completion date to report the gain and pay an estimate of the tax you owe.

This isn’t part of your regular tax return. It’s a completely separate process that requires you to set up a specific ‘Capital Gains Tax on UK property’ account with HMRC. This rule primarily affects UK residents selling properties that aren't their main home, like a buy-to-let or a holiday cottage.

Reporting Other Gains via Self Assessment

For gains on most other assets – think shares, business disposals, or valuable personal items – the process is much more relaxed. These are declared on your annual Self Assessment tax return. The deadline is the standard 31st January that follows the end of the tax year in which you sold the asset.

So, if you sold some shares and made a gain in July 2024 (which is in the 2024/25 tax year), you wouldn't need to report it until 31st January 2026. This gives you a lot more breathing room compared to the urgent 60-day property deadline. You can find a more detailed walkthrough of the steps in our guide on how to report and pay Capital Gains Tax in our guide.

Getting Your Paperwork in Order

No matter which deadline you’re working towards, good record-keeping is your best friend. It takes the stress out of the process and helps avoid mistakes. Before you even start filling out forms, get all your key information together.

- Acquisition Details: When did you buy or acquire the asset, and exactly how much did it cost you?

- Disposal Details: What was the sale date and the final price you received?

- Allowable Costs: Tally up all the related expenses, such as solicitor fees, stamp duty, or costs for capital improvements.

- Reliefs: Note down any tax reliefs you plan to claim, like Business Asset Disposal Relief.

In the 2022–23 tax year, around 370,000 UK taxpayers reported a staggering £81 billion in taxable gains, a figure amplified by the recent cuts to the capital gains tax allowance. With tax receipts forecast to rise, proper compliance is more important than ever. Discover more insights about UK capital gains tax trends.

These figures show just how many people are in the same boat. Getting your numbers organised from the outset makes the whole experience much smoother. It means you can file with confidence, meet your deadlines, and ensure you pay exactly what you owe without any last-minute panic.

Common CGT Mistakes and How to Avoid Them

Navigating Capital Gains Tax can feel like walking through a minefield. It's surprisingly easy to make a simple oversight that leads to overpaying HMRC or, worse, facing an unexpected inquiry. The good news is that most of these common pitfalls are entirely avoidable with a bit of forward planning.

Spotting these potential errors early is the key to protecting your profits. From forgetting legitimate deductions to misinterpreting complex reliefs, these slip-ups can seriously inflate your final tax bill. Let's walk through the most frequent mistakes we see and, more importantly, how you can steer clear of them.

Forgetting to Deduct All Allowable Costs

This is hands-down one of the most common and costly mistakes we see. When calculating a gain, many people simply subtract the original purchase price from the sale price. They completely forget about a whole host of other legitimate costs that could shrink their taxable gain.

Make sure you're keeping track of these crucial expenses:

- Costs of Buying: Think back to when you acquired the asset. This includes things like Stamp Duty Land Tax and any fees you paid to solicitors or surveyors.

- Costs of Selling: Don't forget to factor in estate agent commissions, advertising costs, and the legal fees from the sale.

- Improvement Costs: Did you make any capital improvements, like building an extension on a property? The cost of those can be deducted (though be careful, this doesn't include general upkeep or routine maintenance).

Missing these costs means you're paying tax on an artificially high gain. This is where diligent record-keeping really pays off.

A simple oversight, like forgetting to deduct £5,000 in solicitor fees and stamp duty, could result in an extra £1,200 in tax for a higher-rate taxpayer selling a property. That's a significant sum left on the table for no reason.

Misunderstanding Relief Rules

Tax reliefs like Private Residence Relief (PRR) are incredibly powerful, but the rules are notoriously strict. A classic error is assuming PRR automatically wipes out the entire gain on a property just because it was once your main home, especially if you rented it out for several years. HMRC has very specific rules for periods of absence, and any part of the property used exclusively for business might not qualify either.

In the same way, many business owners don't realise they need to meet specific criteria to qualify for Business Asset Disposal Relief, potentially missing out on that highly attractive 10% tax rate. It's not enough to just own a business asset; you have to tick all the right boxes.

Failing to Report Capital Losses

Let's face it, not every investment is a winner. While making a loss is never fun, it does have a valuable silver lining for tax purposes. A critical mistake is to simply write off the loss and forget about it, failing to report it to HMRC on your tax return.

By reporting your capital losses, you can use them to offset gains you've made in the same year, which directly cuts your tax bill. And if your losses are bigger than your gains? You can carry the unused amount forward indefinitely to reduce gains in future years. Ignoring losses is like throwing away a perfectly legitimate tool for managing your future capital gains tax allowance and liability.

Your Capital Gains Tax Allowance Questions Answered

We've covered a lot of ground, so let's wrap up by tackling some of the most common questions clients ask us. Think of this as a quick-fire round to clear up any lingering confusion about the capital gains tax allowance and how it works in practice.

We’ll touch on some of the key sticking points, from what happens to your unused allowance to how losses and inherited assets are treated.

Can I Carry Forward My Unused Capital Gains Tax Allowance?

In a word, no. The Capital Gains Tax Annual Exempt Amount is strictly a ‘use it or lose it’ deal for each tax year. You can’t save any leftover allowance from one year and add it to the next.

This is exactly why timing your disposals is such a powerful strategy. If you’re planning to sell multiple assets, spreading those sales across different tax years lets you use a fresh allowance each time, potentially sheltering much more of your profit from the taxman.

What Happens If I Make a Capital Loss Instead of a Gain?

Making a loss is never the goal, but it can provide a silver lining for your tax bill. You should always report any capital losses to HMRC on your Self Assessment tax return. Once reported, you can use these losses to reduce your total capital gains in the same tax year.

For example, imagine you have a £10,000 gain but also a £4,000 loss from another asset. You can offset the loss, bringing your net gain down to £6,000. After applying your £3,000 allowance, you're only taxed on the remaining £3,000.

If your losses are bigger than your gains, you can carry the unused net loss forward indefinitely to offset gains in future years. It's a crucial part of tax planning, so don’t forget to report them.

Does the Allowance Apply to Assets I Inherit?

When you inherit an asset, there’s no Capital Gains Tax to pay at that moment. For tax purposes, the slate is wiped clean, and you are considered to have acquired the asset at its market value on the date of death.

CGT only comes into play when you later decide to sell or gift that asset. Your gain is calculated based on the difference between the sale price and its value when you inherited it. You can then, of course, use your annual capital gains tax allowance against this gain.

At Stewart Accounting Services, we turn complex tax rules into clear, actionable strategies. If you’re a business owner or landlord in Central Scotland looking to plan your asset disposals and protect your wealth, we can help. Contact us today for a consultation to secure more time, more money, and a clearer mind.