When you sell a rental property for more than you originally paid for it, that profit is subject to Capital Gains Tax (CGT). This isn't like the income tax you pay on your monthly rent; CGT is a tax on the gain you make when you "dispose" of an asset. For any landlord, getting to grips with this tax is vital when it comes time to sell, transfer, or even gift your buy-to-let property.

What Is Capital Gains Tax for Landlords?

Think of it like this: you buy a vintage watch for £5,000 and, after a few years, sell it for £15,000. You wouldn't be taxed on the full £15,000 sale price. The tax man is only interested in the £10,000 profit you made.

Capital Gains Tax for landlords works on the exact same principle. It's a tax applied purely to the profit—the "capital gain"—you make when you get rid of a second home or investment property.

This makes it completely different from the income tax you declare on rental profits each year. While income tax deals with the regular cash flow your property generates, CGT is a one-off tax that only comes into play when you part ways with the asset itself.

When Is Capital Gains Tax Triggered?

It’s crucial to understand what HMRC considers a 'disposal', because it’s not just about a straightforward sale. Several common scenarios can trigger a CGT liability for landlords:

- Selling the property: This is the most obvious one. You sell for more than you (and your associated costs) paid.

- Gifting the property: Handing over the property to someone else (unless it's your spouse or civil partner) is treated as a disposal at its full market value at that time.

- Transferring ownership: Moving the property into a trust or a limited company, for instance, can also trigger CGT.

- Receiving compensation: If you get an insurance payout for the property's damage or destruction, this can count as a disposal.

The UK's Capital Gains Tax system was actually introduced back in 1965. It was brought in to tax the huge profits people were making from rising property values after World War II. Before that, these gains were completely tax-free, but its arrival made CGT a major consideration for property investors ever since.

In short, any time the ownership of your rental property changes hands, you need to stop and figure out if a capital gain has been made. For a deeper dive into the fundamentals, check out our guide on what UK investors need to know about Capital Gains Tax.

How to Calculate Your Property Capital Gain

https://www.youtube.com/embed/M21Z6_K_sbI

Figuring out the Capital Gains Tax (CGT) you owe on a rental property can feel daunting, but the actual maths is surprisingly straightforward. At its heart, it’s just your final sale price minus all your initial and improvement costs. This simple subtraction ensures you're only paying tax on the real profit you've pocketed.

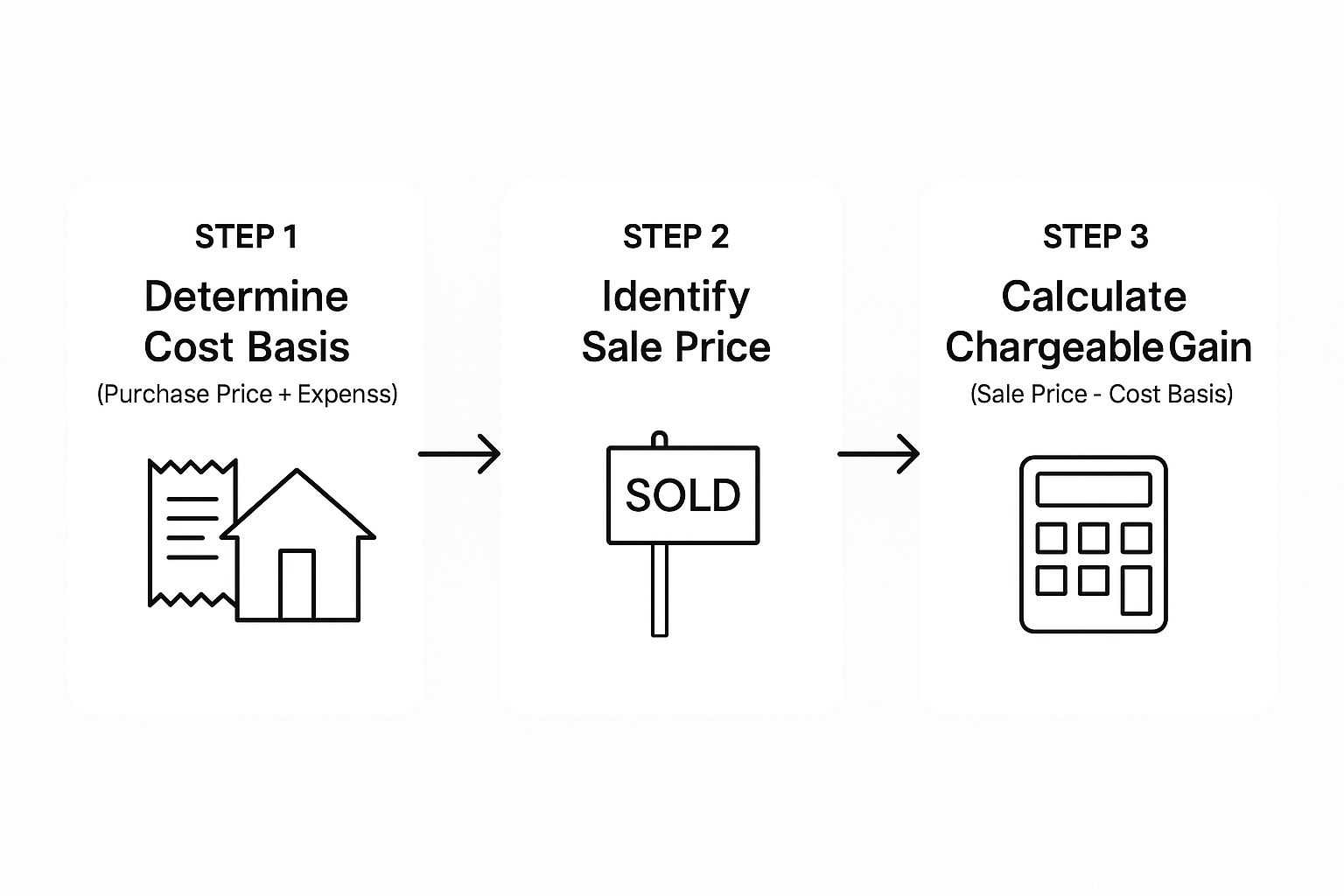

The first, and most critical, step is to work out your property's 'cost basis'. This isn't just the price you paid for the house; it's a bigger number that includes the purchase price plus a range of other legitimate buying costs.

Think of it like building a wall. Each allowable expense you add is another brick, making your cost basis higher and, in turn, shrinking your taxable gain. It's all about meticulous record-keeping.

Establishing Your Total Cost Basis

Getting your cost basis right is the bedrock of the whole calculation. You need to gather every receipt and invoice for any allowable expense you've incurred over the years.

These costs typically include:

- Stamp Duty Land Tax (SDLT): The hefty tax bill you paid right at the start.

- Legal and Professional Fees: Don't forget what you paid your solicitor and surveyor to get the deal done.

- Major Capital Improvements: This is a big one. It covers any significant work that genuinely added value to the property, like an extension, a loft conversion, or a complete kitchen refit. Day-to-day repairs or a lick of paint, however, don't make the cut.

The golden rule is simple: the higher you can legitimately build your cost basis, the smaller your taxable gain will be. Every pound you can prove you spent is a pound HMRC can't tax.

The infographic below neatly summarises the three core steps to finding your gain.

As you can see, it's a simple process of taking the sale price and subtracting everything you've spent to arrive at the final profit figure.

Calculating the Chargeable Gain

Once you've tallied up your total cost basis, the next bit is easy. You just subtract that total from the property's final sale price. The number you're left with is your 'chargeable gain'.

Sale Price – Total Cost Basis = Chargeable Gain

This gain is the profit that's subject to tax. And for long-term landlords, these gains can be huge. Thanks to decades of house price growth, a landlord who bought an average property back in 1990 and sold it in 2022 could be looking at an average capital gain of around £240,634. You can dig deeper into the data on landlord property value increases to see just how much values have climbed.

Let's put this into practice with a quick example.

The following table breaks down a typical scenario to show you how these numbers come together.

Example CGT Calculation for a Landlord

| Calculation Step | Description | Example Amount |

|---|---|---|

| Purchase Price | The original amount paid for the buy-to-let property. | £150,000 |

| Buying Costs | Includes Stamp Duty and solicitor/surveyor fees. | £5,000 |

| Capital Improvements | Money spent on a major kitchen and bathroom renovation. | £20,000 |

| Total Cost Basis | Adding the purchase price, buying costs, and improvements together. | £175,000 |

| Final Sale Price | The price the property was sold for years later. | £250,000 |

| Chargeable Gain | The sale price minus the total cost basis. | £75,000 |

In this case, the landlord's chargeable gain—the amount that CGT is calculated on—is £75,000. The next step, of course, is to apply any tax-free allowances and reliefs you're entitled to, which will bring down the final tax bill.

Understanding CGT Rates and Allowances

So, you've worked out your chargeable gain. The next logical question is: how much of that profit actually goes to the taxman? The answer isn't a simple one-size-fits-all percentage.

The amount of CGT you pay on a property sale is directly tied to your income for that year. HMRC looks at your total earnings to see which income tax bracket you fall into, and that determines the CGT rate you'll face.

The Current CGT Rates for Landlords

When it comes to residential property, the tax rates are higher than for other assets like shares. As a landlord, these are the numbers you really need to know.

For the 2024/25 tax year, the capital gains tax rates on residential property are:

- 18% if your gain, when added to your income, still keeps you within the basic-rate tax band.

- 24% for any part of the gain that pushes you into the higher or additional-rate tax bands.

Think of it this way: your property profit gets stacked on top of your other income (like your salary). Any part of that profit that falls into the basic-rate slice of your total income gets the lower 18% rate. Anything that tips over into the higher-rate slice gets hit with the 24% rate.

The Annual Exempt Amount: Your Tax-Free Buffer

Before you even start worrying about those rates, there's a bit of good news. Every individual gets a tax-free allowance for capital gains, known as the Annual Exempt Amount (AEA).

For the 2024/25 tax year, the AEA is £3,000.

This means the first £3,000 of your profit is completely tax-free. You only start calculating tax on the gain above this amount. It’s your first and most important tool for reducing the final bill.

This allowance is a "use it or lose it" benefit. It cannot be carried forward to future tax years, making the timing of a property sale an important strategic decision.

The impact of this tax on landlords is significant. In the tax year ending 2025, an estimated 163,000 taxpayers are expected to report residential property sales, generating a whopping £2.2 billion in CGT for the government. You can dig into the latest government CGT statistics to see the full picture.

Let's go back to our landlord, David, who had a chargeable gain of £75,000. He first subtracts his £3,000 AEA, which brings his taxable gain down to £72,000.

Now, we look at his income. If David is a basic-rate taxpayer and has £10,000 of his basic-rate band left for the year, the calculation looks like this:

- The first £10,000 of his gain is taxed at 18% = £1,800.

- The remaining £62,000 (£72,000 – £10,000) is taxed at the higher rate of 24% = £14,880.

His total CGT bill would be £16,680.

But what if David was already a higher-rate taxpayer before even factoring in the property sale? In that case, the entire £72,000 gain would be taxed at 24%, resulting in a much higher bill of £17,280.

Using Tax Reliefs to Reduce Your CGT Bill

While the Annual Exempt Amount gives you a decent starting buffer, the real game-changer for slashing your capital gains tax bill is using specific tax reliefs. These aren't sneaky loopholes; they are legitimate allowances from HMRC designed for certain situations – like when your rental property used to be your home.

For any landlord, getting your head around these reliefs is non-negotiable. It’s the key to making sure you pay the tax you owe, and not a penny more.

The most powerful relief by far is Private Residence Relief (PRR). It’s the reason you don’t pay a bean in CGT when you sell your main family home. But here's the crucial part for landlords: PRR can also make a huge dent in the tax on a rental property, but only if you lived in it as your main home at some point before you started letting it out.

Claiming Private Residence Relief

The logic behind PRR is straightforward. You get tax relief for the chunk of time the property was officially your main home. Simple enough. But HMRC also gives you a bonus: the final nine months you own the property are also covered by the relief, even if you weren't living there. This is a handy grace period to help you sell your old home after you've already moved on.

Let's walk through an example. Say you bought a flat and lived there for five years. Then, you moved into a new house and decided to rent out the flat for the next ten years before finally selling it.

Here’s how the relief calculation would look:

- Total ownership period: 15 years (or 180 months).

- Time you lived there as your main home: 5 years (60 months).

- The final period that automatically qualifies: 9 months.

So, a total of 69 months (60 + 9) out of the 180 months you owned the property are exempt from CGT. That means you can claim relief on 38.3% of your total gain (69 ÷ 180). This single calculation could easily save you thousands of pounds.

To dig deeper into the rules, have a look at our guide on when Private Residence Relief applies.

Key Takeaway: If your rental property was ever your main home, you're almost certainly entitled to some Private Residence Relief. Keeping meticulous records of when you lived there is vital for making an accurate claim.

Understanding Lettings Relief

Now, you might have heard of another relief called Lettings Relief. In the past, this was an incredibly valuable tool for landlords who had lived in their rental property. It provided an extra layer of tax reduction on top of PRR.

However, the goalposts moved dramatically in April 2020. The rules were tightened, and now Lettings Relief is much harder to qualify for.

Today, it's only really available to landlords who shared the property with their tenant – in other words, if you had a lodger while you were also living there. For the vast majority of landlords who move out completely before finding tenants, this relief is sadly off the table.

This change makes it more important than ever to accurately calculate and claim every single month of PRR you’re entitled to. It’s now the primary way for landlords to manage their final capital gains tax liability effectively.

Reporting and Paying Your CGT to HMRC

So, you’ve worked out your gain and figured out which reliefs apply. Now what? The clock is officially ticking, and when it comes to Capital Gains Tax for landlords, HMRC doesn't hang about.

Forget waiting for your annual Self Assessment tax return. For property sales, the rules are much tighter.

You have a strict 60-day window from the date your property sale completes to report the gain and pay the tax you owe. Miss this deadline, and you’ll be hit with penalties and interest almost immediately. It’s a date for your diary you absolutely cannot miss.

This quick turnaround means you need to get your ducks in a row as soon as the sale is agreed upon, not when the money hits your bank account.

How to Report Your Gain

HMRC has a dedicated online system for this, called the 'Capital Gains Tax on UK property' service. This is completely separate from your usual tax return process.

Before you even log in, get all your paperwork together. You’ll need:

- The property address and postcode.

- The date you originally got the property.

- The dates you exchanged contracts and completed the sale.

- The price you paid for the property and the price you sold it for.

- A detailed list of your allowable costs – think stamp duty, estate agent fees, and the cost of that new extension.

- Details of any reliefs you’re claiming.

A bit of hard-won advice: don't think of the 60-day window as your target. Treat it as the final, non-negotiable deadline. Plan to get everything submitted well before the cut-off to sidestep any last-minute stress or technical glitches.

Once you’ve submitted the report online, HMRC will give you a payment reference number. You’ll need this to pay your estimated CGT bill, which is also due within that same 60-day period.

The whole process can feel a little complicated, so it's worth understanding the steps for filing and paying CGT after property sales ahead of time. Getting the admin right means you can move on without any nagging tax worries.

Practical Ways to Legally Reduce Your CGT Bill

The savviest landlords don't just think about Capital Gains Tax when a "For Sale" sign goes up. Getting ahead of it is the secret. Smart, proactive planning can turn a potential tax headache into a manageable part of your investment journey.

There are several perfectly legal ways to significantly shrink the final cheque you write to HMRC. It all starts with a simple change in perspective: stop seeing tax planning as a chore and start seeing it as a powerful tool for boosting your overall returns. Often, it just comes down to smart timing and thinking carefully about who owns what.

Time Your Sale to Your Advantage

One of the most straightforward yet powerful tactics is simply choosing when to sell. Every individual gets a tax-free allowance for capital gains each year, known as the Annual Exempt Amount (AEA). For the 2024/25 tax year, this allowance is £3,000.

Think of this allowance as a "use it or lose it" voucher from the taxman. It resets every tax year. By timing your sale to fall in a year where you haven't made any other gains, you ensure that the first £3,000 of your profit is completely tax-free.

If you happen to be selling more than one asset, staggering the sales across different tax years lets you claim this allowance multiple times. It’s a simple way to shield more of your hard-earned gains from tax.

Make Use of Your Spouse's Allowances

Another brilliant strategy involves your spouse or civil partner. The good news is that you can transfer assets between you without triggering any Capital Gains Tax. This unlocks a couple of fantastic planning opportunities.

First, you can transfer a share of the property to your partner before you sell. This means you can both use your individual Annual Exempt Amounts on the profit from that single sale. Just like that, your tax-free allowance on the property doubles from £3,000 to £6,000.

What's more, if your partner pays tax at the basic rate and you're a higher-rate taxpayer, this move is even more effective. By transferring a portion of the gain to them, their share will be taxed at the much lower 18% rate, rather than your 24%.

Good Records Are Your Best Friend

Never, ever underestimate the power of a well-organised folder of receipts. Every penny you’ve spent on genuine capital improvements – we’re talking a loft conversion, a new extension, or a significant structural upgrade – adds to your property's cost base.

Each one of those receipts is a tool that directly chips away at your final taxable gain. Keep a detailed record of every allowable cost, from the solicitor’s fees and stamp duty when you first bought the place to the invoices for that brand-new kitchen. These documented expenses are your number one defence against overpaying your capital gains tax.

Landlord CGT: Your Questions Answered

When you're dealing with Capital Gains Tax, a few specific questions tend to pop up time and time again. Let's tackle some of the most common ones we hear from landlords.

Can I Knock My Mortgage Interest Off the Gain?

That’s a definite no, I’m afraid. While you can claim a portion of your mortgage interest as a credit against your rental income each year, you can't deduct it from your capital gain.

Think of it this way: HMRC sees mortgage interest as a day-to-day running cost of your rental business (a revenue expense), not part of the cost of buying or selling the property itself.

What if I Sell the Property for a Loss?

Selling for less than you paid is never the goal, but if it happens, you’ll have a capital loss. You can’t use this loss to reduce your income tax bill, but it’s not useless.

First, you must use it to offset any other capital gains you might have in the same tax year. If you still have losses left over after that, you can carry them forward to reduce gains in future years. There's no time limit on carrying them forward, which is a useful silver lining.

Do I Pay CGT if I Inherit a Property?

No, you don't pay Capital Gains Tax just for inheriting a property. When you inherit, the property's value for tax purposes is reset to whatever it was worth on the date the previous owner passed away.

This means you only have to worry about CGT on the growth in value from that date forward, if and when you decide to sell.

A Quick Word of Warning: Just because there's no CGT at the point of inheritance doesn't mean it's tax-free. The property's value will form part of the deceased's estate, which could trigger an Inheritance Tax bill.

Understanding this difference is key to both good estate planning and managing your own future tax situation as a landlord.

Getting to grips with capital gains tax for landlords can feel overwhelming, but you don't have to do it alone. The team at Stewart Accounting Services is here to help you navigate your obligations, make sure you're claiming every relief you're entitled to, and avoid overpaying. Reach out today for clear, personalised advice at https://stewartaccounting.co.uk.