The Construction Industry Scheme (CIS) can seem complicated at first, but it's really just HMRC's way of collecting income tax in advance from subcontractors in the construction trade. It’s not an extra tax. Instead, it’s a system that directly involves both the contractors who pay for work and the subcontractors who carry it out.

What is the CIS Construction Industry Scheme?

Think of the CIS scheme as a tax-withholding system created specifically for the UK construction industry. Its main purpose is to improve tax compliance and prevent tax evasion in a sector known for its heavy reliance on self-employed workers.

So, how does it work in practice? Rather than a subcontractor receiving their full payment and sorting out their tax bill at the end of the year, the contractor they work for is legally obliged to deduct a percentage of that payment right away. This deduction is then paid directly to HMRC on the subcontractor's behalf.

This advance payment acts as a credit against the subcontractor's end-of-year tax and National Insurance bill. Getting a solid grasp of this process is the first, and most important, step to managing your responsibilities properly, whether you're paying people or getting paid.

Who the CIS Scheme Affects

The scheme clearly sets out the duties for two main groups on any construction project: contractors and subcontractors.

It’s crucial to know which category you fall into. A contractor is any business that hires other businesses or self-employed individuals to do construction work. They're the ones who have to check a subcontractor's status with HMRC and make the right deductions.

On the other side, you have the subcontractors – the businesses or individuals who actually perform the construction work. If you're unsure about your status, it's worth taking a moment to understand the official definition of a building sub-contractor.

This system is a unique UK withholding tax, and the deductions are made at source from payments. The rate is typically 20% if the subcontractor is registered with HMRC, but it jumps to a hefty 30% if they aren't. It's not just mainland UK projects, either; the scheme's rules apply to work done across the UK and its territorial waters, covering offshore developments like wind farms.

To get CIS right, it helps to have solid processes in place. A good understanding of what contractor management involves goes a long way. It ensures that beyond just ticking the tax boxes, your projects run smoothly, safely, and efficiently from start to finish.

To make things clearer, here’s a quick breakdown of who does what under the CIS scheme.

CIS Roles and Core Responsibilities

| Role | Key Responsibility |

|---|---|

| Contractor | Verify subcontractor status with HMRC, deduct the correct tax percentage from payments, and pay it directly to HMRC. |

| Subcontractor | Register with HMRC for the correct deduction rate and declare CIS deductions on their annual tax return to offset tax liability. |

Ultimately, both parties have a part to play in ensuring the scheme operates as intended, keeping everything above board with HMRC.

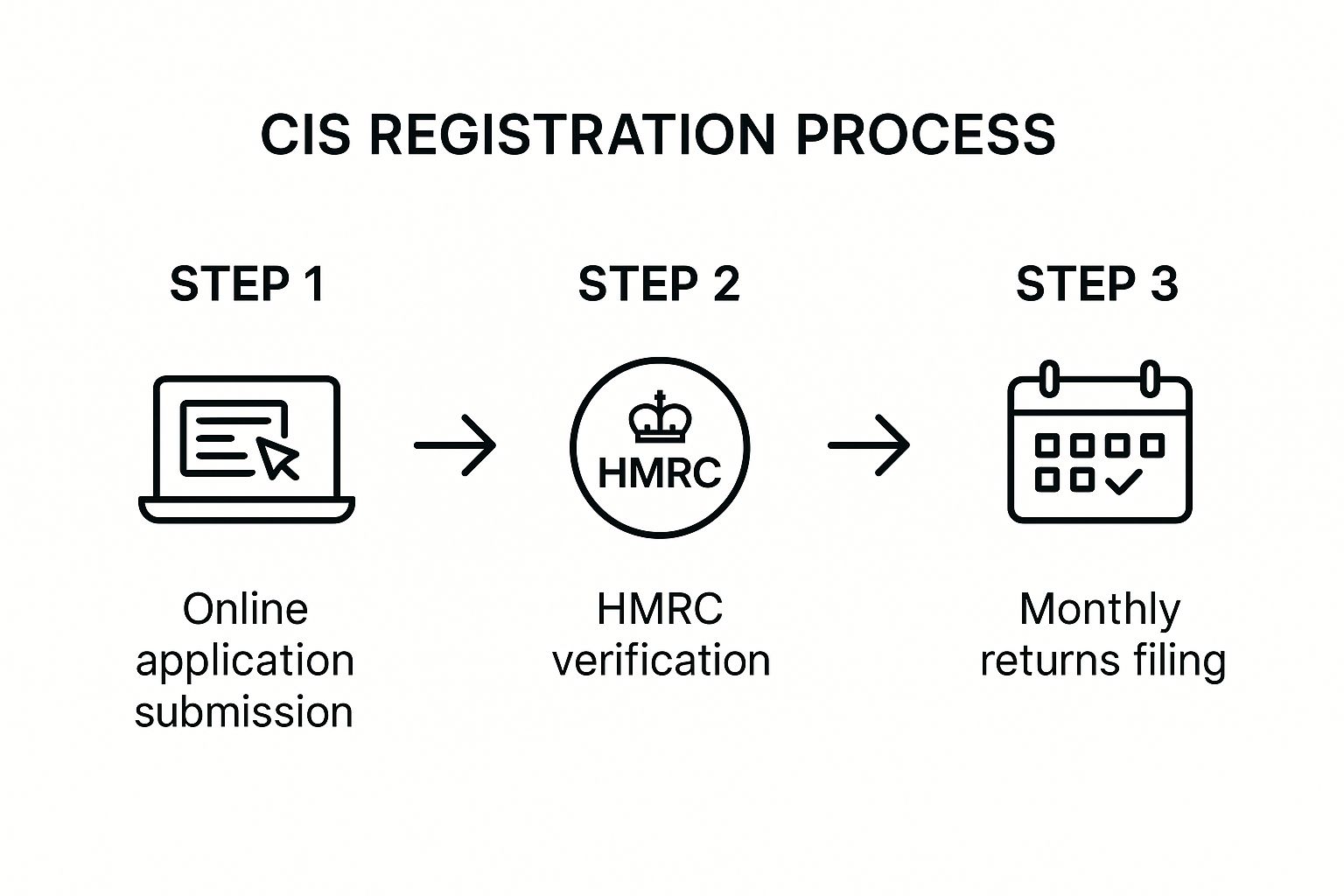

How to Get Registered for CIS

Getting yourself registered for the Construction Industry Scheme (CIS) is one of the first things you need to sort out. It’s a crucial step, whether you’re a contractor who will be paying subcontractors, or a subcontractor who needs to get paid correctly. The process itself isn't too complicated, but you’ll save yourself a lot of hassle by having the right information ready for HMRC from the get-go.

No matter which side of the fence you're on, you'll absolutely need your Unique Taxpayer Reference (UTR). That's the ten-digit number HMRC uses to identify you. You'll also need your National Insurance number and basic details about your business, like its name and how it's set up (sole trader, limited company, etc.).

Getting Started as a Subcontractor

If you're a subcontractor, registering for CIS isn't technically compulsory. However, if you don't, you'll be hit with a hefty 30% deduction from your payments right away. It's a real sting to your cash flow.

By registering, you immediately drop down to the standard 20% deduction rate. This is much more manageable and acts as an advance payment on your annual tax and National Insurance bill.

To get set up for the standard 20% rate, make sure you have these details handy:

- Your Unique Taxpayer Reference (UTR)

- Your National Insurance Number

- Your VAT registration number (if you’re registered for VAT)

The Goal: Achieving Gross Payment Status

For any subcontractor who's been in the game a while, the real prize is getting gross payment status. This is a complete game-changer. It means contractors can pay you in full with 0% deducted.

Think about what that does for your cash flow. You get 100% of your invoice paid straight into your bank, and you sort out your own tax bill at the end of the year.

Securing gross payment status is more than just a financial benefit; it’s a clear signal to HMRC that your business is reliable, compliant, and has a solid trading history. It's a real badge of honour in the industry.

To get there, you need to prove to HMRC that you tick three specific boxes:

- The Business Test: You need to show that you're genuinely running a construction business, and a key part of that is operating primarily through a business bank account.

- The Turnover Test: Your annual turnover from construction work (not including VAT or the cost of materials) must be at least £30,000 if you’re a sole trader. The thresholds are higher for partnerships and companies.

- The Compliance Test: This is a big one. You must have a spotless record with HMRC, meaning all your tax returns and payments have been made on time.

Nailing these criteria shows you can be trusted to handle your own tax affairs without needing deductions taken at source. It puts you firmly in control of your finances.

Making CIS Deductions Work in Practice

Knowing the rules of the Construction Industry Scheme (CIS) is one thing, but applying them correctly day-to-day is what really matters. For contractors, every single payment you make to a subcontractor has to follow a strict process to keep you on the right side of HMRC. It all boils down to verifying your subcontractors, deducting the correct tax, and keeping meticulous records.

Let's walk through a typical scenario. Imagine you're a main contractor and you've just brought a self-employed plasterer onto a job. Before you even think about paying their first invoice, you have one crucial first step: you must verify them with HMRC. This is a quick check, usually done online, that confirms their official CIS status and tells you exactly which tax rate to apply.

You’ll find they fall into one of three categories, and it’s vital you get this right.

CIS Deduction Rate Scenarios

The rate HMRC gives you dictates how you handle the payment. It's not a choice; it's a legal requirement.

| Subcontractor Status | HMRC Deduction Rate | What It Means for Payments |

|---|---|---|

| Has Gross Payment Status | 0% | You pay the subcontractor the full invoice amount with no deductions. |

| Registered for CIS | 20% | You must deduct tax at the standard 20% rate from the labour part of their invoice. |

| Unregistered for CIS | 30% | You must deduct tax at the higher 30% rate from the labour part of their invoice. |

Getting this rate wrong can cause real headaches down the line, so always verify first.

Getting the Calculation Right

Once you have the rate, the maths is pretty simple. The most important thing to remember is that CIS deductions only apply to the labour element of an invoice, not the cost of materials.

Let's go back to our plasterer. Their invoice comes in for £1,000. On it, they’ve clearly broken down that £700 is for their labour and £300 is for the materials they bought for the job. HMRC has confirmed they are registered for CIS at the standard 20% rate.

Your calculation is based only on that £700 labour figure.

Calculation Example: £700 (Labour) x 20% = £140 (CIS Deduction)

You would pay the plasterer £860 (the £1,000 total invoice minus the £140 you've deducted). That £140 is held by you to be paid over to HMRC in your next monthly CIS return.

This flow, from verification to calculation and reporting, is the core of your monthly CIS duties.

As the infographic shows, these steps are cyclical and central to staying compliant.

Don't Forget the Paperwork

Your last job in this process is to give each subcontractor a payment and deduction statement. This is essentially their payslip. It must clearly show the gross payment, the cost of any materials, and the final amount of tax deducted.

This isn't an optional step—it's a legal requirement and provides the subcontractor with the proof they need for their own tax affairs. Diligent record-keeping is a cornerstone of good financial practice, something we cover in more detail in our guide on accounting for contractors.

A quick note: you can only exclude the cost of materials from the CIS calculation if the subcontractor bought them directly. Also, be aware of the 'deemed contractor' rules. If your business spends over £3 million on construction within any rolling 12-month period, you fall under CIS and must continuously monitor that spend. HMRC has been tightening the rules here, which you can read about in the government's guidance on tackling CIS abuse.

Reporting Your CIS Deductions to HMRC

Once you've calculated and made the deductions from your subcontractors' pay, the final piece of the puzzle is to report everything and pay the tax over to HMRC. This is a non-negotiable part of the cis construction industry scheme and is handled through a mandatory monthly return.

Every single month, you need to file a return that covers all payments you've made to your subcontractors. Remember, the tax month runs from the 6th of one month to the 5th of the next. Your deadline to get that return filed is the 19th of every month.

So, for example, any payments you make between 6th May and 5th June must be reported on a return that's due by 19th June. It’s a tight turnaround, so it pays to be organised.

What to Include in Your Monthly Return

Getting the details right on your return is absolutely crucial. HMRC needs a clear breakdown for each and every subcontractor you've paid in the period.

You'll need to report:

- Their name and Unique Taxpayer Reference (UTR).

- The gross amount you paid them before any deductions.

- The total cost of any materials they included on their invoices, as this part isn't subject to the CIS deduction.

- The final figure for the tax you actually deducted from their labour costs.

This information basically proves you've followed the rules. The CIS deductions you've held back are then paid to HMRC along with your regular PAYE and National Insurance payments, usually by the 22nd of the month if you're paying electronically.

I always tell clients to think of the monthly return as the final, official record. It connects all your earlier checks, calculations, and payments, demonstrating your compliance and making sure your subcontractors get the proper credit for the tax they’ve paid upfront.

The Consequences of Late Filing

Don't be late. Seriously. HMRC's penalty system for late CIS returns is automatic, and it's incredibly strict. Missing the deadline, even by a single day, will land you an instant £100 fine.

And the penalties don't stop there; they escalate pretty quickly. If your return is two months late, that fine jumps to £200. After six months, you're looking at £300 or 5% of the CIS deductions on the return, whichever is higher.

If it drags on for a year or more, the penalties can climb as high as £3,000. The easiest way to avoid these completely unnecessary costs is simply to have a solid system in place to file on time, every time.

Common CIS Mistakes and How to Avoid Them

Getting to grips with the CIS construction industry scheme isn't rocket science, but small administrative mistakes can quickly turn into expensive penalties from HMRC. Knowing what to watch out for is the best way to keep your business compliant and save yourself a lot of headaches down the line.

One of the easiest traps to fall into is failing to verify a new subcontractor before their first payment goes out. It's a simple step, but forgetting it means you could apply the wrong deduction rate, instantly putting you on the wrong side of the rules. The solution? Make it a non-negotiable part of your process: verify every single subcontractor with HMRC before you pay them a penny.

Another common slip-up happens with the maths. Contractors often mistakenly calculate the CIS deduction on the full invoice amount, including VAT. Remember, the deduction only applies to the labour component of the bill, not the cost of materials or any VAT that's been added on.

Misclassifying Workers and Other Pitfalls

Perhaps the most critical error is misclassifying someone who is, for all intents and purposes, an employee as a self-employed subcontractor. This is a massive red flag for HMRC and can lead to hefty backdated tax and National Insurance bills. A good rule of thumb is if you set their hours, give them the tools for the job, and control their day-to-day work, they're probably an employee.

A few other frequent blunders to keep on your radar include:

- Late Monthly Returns: Submitting your return even a day after the 19th of the month means an instant £100 penalty. There’s no grace period.

- Poor Record-Keeping: Not keeping or providing accurate payment and deduction statements creates a messy paper trail that can cause issues for both you and your subcontractors come tax time.

The construction industry is a cornerstone of the UK economy, making up around 6% of GDP and providing jobs for over 2.4 million people. Because it's so significant, HMRC keeps a close watch on it. This scrutiny, combined with the administrative weight of CIS, adds real pressure to businesses. For a deeper dive, check out these UK construction trends at Munichre.com.

The good news is that these mistakes are entirely preventable with the right systems in place. For more expert advice, have a read of our article on how accountants help contractors avoid UK tax traps.

Your CIS Questions Answered

Even once you get the hang of the CIS construction industry scheme, specific questions always seem to crop up. Let's run through some of the most common queries I hear, breaking them down into simple, practical answers to help you stay on the right side of HMRC.

What Construction Work Does CIS Cover?

The scope of CIS is surprisingly wide, covering most work you’d associate with a building site and then some. It isn’t just about the major structural stuff like bricklaying; the rules also pull in the jobs that get a project started and finished.

Typically, any of the following activities will fall under CIS:

- Site preparation, including demolition and putting up scaffolding.

- The actual building work, alterations, repairs, and even decorating.

- Installing systems for heating, lighting, and power.

It’s worth noting, though, that some jobs are specifically excluded. Professional services from architects and surveyors don't fall under the scheme. Neither do certain finishing trades, like carpet fitting. It’s always best to check if you’re unsure.

How Do I Reclaim Tax Deducted Under CIS?

The best way to think of CIS deductions is as an advance payment towards your tax and National Insurance bill. How you get that money back depends entirely on how your business is set up.

If you’re a sole trader, it’s a case of detailing all your CIS deductions on your annual Self Assessment tax return. HMRC will then offset this total against what you owe. If the deductions are more than your bill, you’ll get a refund. Simple as that.

For a limited company, it works a bit differently. You’ll offset the CIS deductions you've had taken from your income against the PAYE and National Insurance you owe to HMRC for your own employees and subcontractors.

The crucial thing to remember is that this isn't lost money. It’s a credit against your tax liabilities, which is why keeping every single payment and deduction statement is absolutely non-negotiable. Good records ensure you reclaim every penny.

What Are the Penalties for a Late CIS Return?

This is one area where HMRC doesn't mess about. The penalty system for late monthly returns is automated and unforgiving. Miss the filing deadline by just a single day, and you’ll be hit with an instant £100 fine.

It gets expensive very quickly from there. A return that’s two months late will land you another £100 penalty, and the fines keep climbing. For persistent late filing, penalties can reach as high as £3,000. You can appeal a penalty, but you'll need a very good reason—like a sudden, serious illness—for HMRC to even consider it.

At Stewart Accounting Services, we handle the complexities of CIS so you don't have to. From managing monthly returns to making sure deductions are spot on and helping you reclaim what you're owed, we give you back your time and your peace of mind. See how we can support your business at https://stewartaccounting.co.uk.