As a director of a UK limited company, keeping on top of your Companies House filing deadlines isn't just good practice—it's a legal requirement. The two most important dates in your calendar will be for your Annual Accounts and your Confirmation Statement. Getting these right is fundamental to keeping your company in good legal standing.

Your Core Filing Obligations Explained

Think of Companies House as the official public record for every UK business. To ensure your company’s information is accurate and accessible, you need to provide regular updates. This isn't just about ticking boxes; it's about maintaining transparency and proving your company is being run correctly.

Your two main filings serve very different purposes, but they're equally vital. Together, they paint a complete picture of your company’s financial health and its administrative structure for the public, potential investors, and government bodies.

Annual Accounts

This is the financial story of your business over the past year. Your annual accounts need to break down the company's performance, showing everything from income and expenses to its assets and liabilities. Essentially, it's a detailed health check that proves your business is financially sound.

Confirmation Statement

This filing is less about the numbers and more about the facts. It's like an annual census for your company, confirming that the key details Companies House holds are still correct. This covers things like your registered office address, the names of your directors, and who your shareholders are. It’s a snapshot to verify the administrative side of your business hasn't changed without you telling them.

Remember, the legal responsibility for filing these documents on time falls squarely on the company directors. You can (and probably should) get your accountant to handle the actual submission, but if a deadline is missed, the buck stops with you.

To help you keep everything straight, here's a quick summary of the key deadlines you need to know.

Key Filing Deadlines at a Glance

| Filing Type | Standard Deadline | Purpose |

|---|---|---|

| Annual Accounts | 9 months after your financial year-end | To report the company's financial performance and position. |

| Confirmation Statement | At least once every 12 months | To confirm the company's non-financial information is accurate. |

For private limited companies, the deadline for annual accounts is usually 9 months after your company's financial year ends. However, there's a different rule for your very first set of accounts—those must be filed within 21 months of your incorporation date.

Don't take these dates lightly. The penalties for late filing are automatic and can get expensive fast. A delay of less than a month will land you a £150 fine, which jumps all the way to £1,500 if you're over six months late.

To make sure your business ticks all the right boxes beyond just Companies House, it's a good idea to refer to a comprehensive business compliance guide that covers the wider regulatory landscape.

Calculating Your Annual Accounts Deadline

Figuring out your annual accounts deadline isn't as simple as circling a date on the calendar. It’s a date that’s tied directly to your company's own financial year, and this often trips up new business owners. Getting this right is the absolute foundation of staying compliant with Companies House.

The key to it all is your Accounting Reference Date, or ARD. Just think of the ARD as your company's financial birthday. For nearly every new company, Companies House automatically sets this as the last day of the month you were incorporated.

So, if you registered your company on 10 April 2024, your ARD would fall on 30 April every year. Your annual accounts need to cover the financial period leading right up to that date.

Your First Accounts Deadline

This is the one that’s a bit different. The rules for your very first set of accounts are much more generous, giving you some breathing room to get your financial house in order.

Instead of the usual nine-month window, you actually get 21 months from your incorporation date to file your first accounts. Because of this, your first accounting period will naturally be longer than 12 months. Let's stick with our example:

- Incorporation Date: 10 April 2024

- First ARD: 30 April 2025

- First Accounting Period: 10 April 2024 to 30 April 2025 (a little over 12 months)

- Filing Deadline: 10 January 2026 (21 months after the 10 April 2024 incorporation date)

After you've navigated this first, longer period, your company falls into a regular annual pattern. From then on, each accounting period will be a standard 12 months, and you'll have nine months from your ARD to get your accounts filed.

Key Takeaway: Your first filing period is longer than a year, and the deadline is 21 months from incorporation. Every subsequent deadline for a private limited company is nine months after your Accounting Reference Date.

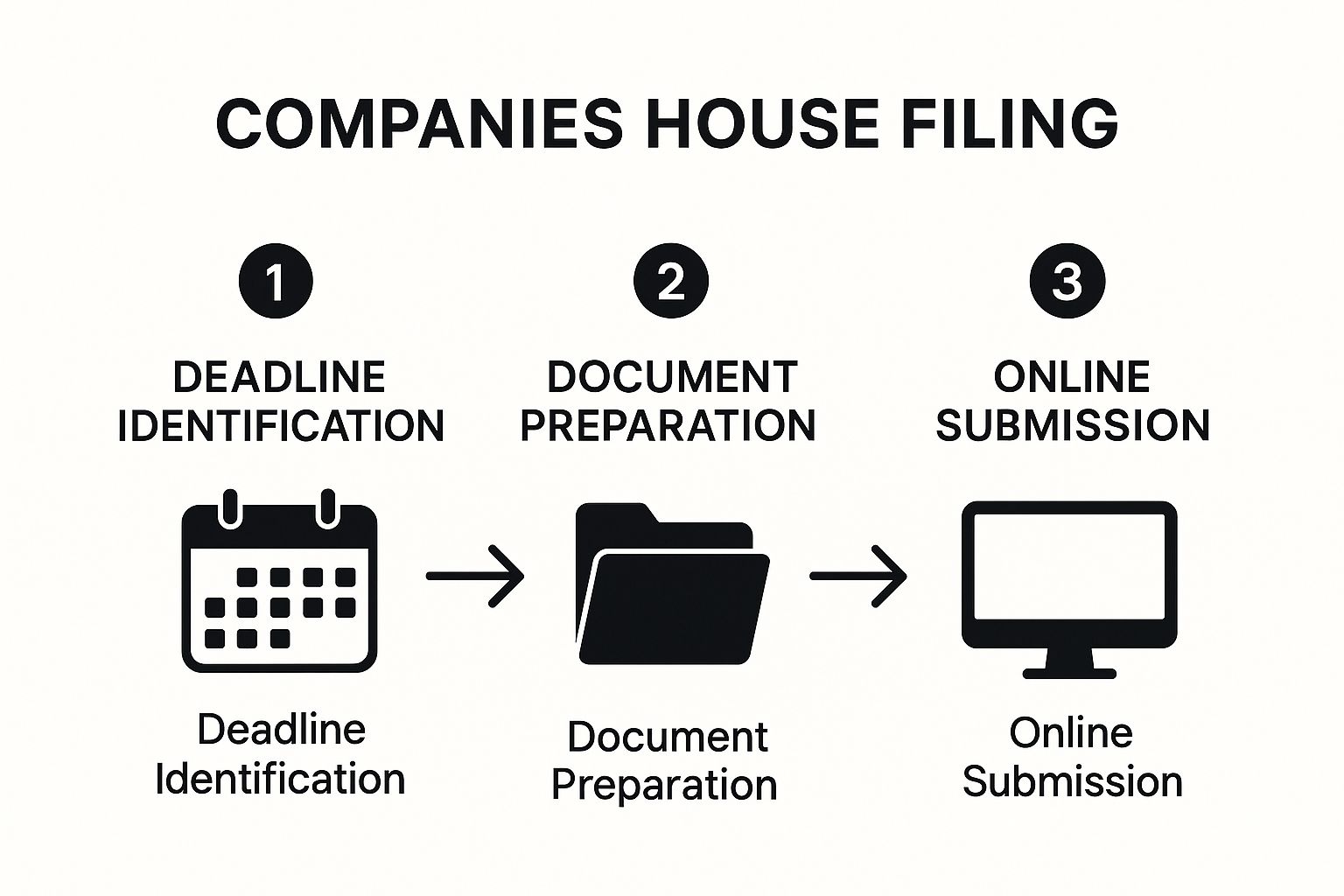

This whole journey, from working out your deadline to finally hitting 'submit', has several steps. The image below gives you a bird's-eye view of the typical workflow.

As you can see, staying on top of your filings starts long before you prepare the documents themselves; it all begins with knowing exactly what your deadlines are.

Changing Your Accounting Period

You aren’t stuck with your initial ARD forever. It's possible to change it by shortening your accounting period (which you can do as often as you like) or lengthening it (which is limited to once every five years).

Be aware, though, that this will directly shift your Companies House filing deadlines.

Shortening your accounting period will pull your deadline forward, while extending it pushes the date further away. This can be a useful strategy to align with a parent company's financial year or just move to a more convenient reporting date, but you have to do it with a clear understanding of how it impacts when you need to file.

Once you know your dates, using effective time management techniques is crucial for getting everything submitted without any last-minute panic. Knowing the deadline is half the battle; planning your time to meet it is the other.

Navigating The Confirmation Statement

While your annual accounts paint the financial picture of your business, the Confirmation Statement is more like its official biography. Think of it as a yearly administrative check-up, making sure all the core details about your company on the public record are spot on. This isn't about profits and losses; it's purely about accuracy.

Filing it confirms that the information available to the public is up-to-date and correct, which is fundamental for transparency and trust. For busy directors, it’s an easy one to overlook, but that can be a costly mistake.

What Does It Confirm?

The Confirmation Statement, which used to be called the Annual Return, is your chance to review and confirm all the key details Companies House holds for your company. If you’ve had any changes during the year that you haven’t yet reported, now’s the time to update them.

You’ll be asked to check and verify a few key things:

- Registered Office Address: Your company's official address for all formal mail.

- Directors and their Details: The names, service addresses, and other recorded info for each director.

- Shareholder Information: A complete list of shareholders and a breakdown of their holdings.

- People with Significant Control (PSCs): Details of anyone who ultimately owns or controls your company.

- Standard Industrial Classification (SIC) Code: The code that identifies your company's main business activity.

Essentially, you’re creating a snapshot in time, confirming that all this information is correct on the day you make the statement.

The Deadline: A Simple Rule

Unlike the accounts deadline, which is linked to your financial year, the Confirmation Statement deadline follows a much simpler rhythm. It’s based on a 12-month review period that usually starts on the anniversary of your company’s incorporation.

Your deadline to file the Confirmation Statement is just 14 days after the end of your review period. It’s a very tight window, so make sure it's firmly marked in your calendar.

Let’s say you incorporated your company on 10th April. Your first review period would end on 9th April the following year, which means your filing deadline would be 23rd April. Simple as that.

This deadline is completely separate from your accounts filing date, and it’s a critical part of your Companies House filing deadlines that you need to track independently. Missing it can lead to penalties, and in more serious cases, the company could be struck off the register entirely. The standard online filing fee is £34, a small price for keeping your company compliant and in good standing.

The Real Cost of Missing Deadlines

Let’s be clear: ignoring your Companies House filing deadlines isn't just a minor administrative slip-up. It's a serious misstep that triggers immediate and escalating consequences. The penalties are automatic, non-negotiable, and honestly, they're just the tip of the iceberg.

The most obvious hit is to your bank account. Companies House enforces a strict penalty system for late accounts, and there’s absolutely no grace period. The second you tick past your deadline, a fine is issued. The longer you wait, the bigger it gets. This isn’t something you can talk your way out of; it’s an automatic penalty baked into UK company law.

Automatic Late Filing Penalties

The fines are designed to be a serious deterrent, and they certainly are. For a private limited company, the penalty structure is set up to increase sharply over time, which means you need to act fast if you’ve missed a date.

Here’s a breakdown of what you can expect if your annual accounts are filed late.

Late Filing Penalty Structure for Private Companies

This table shows the automatic financial penalties issued by Companies House for the late filing of annual accounts.

| How Late the Accounts Are | Penalty Amount |

|---|---|

| Not more than 1 month | £150 |

| More than 1 month but not more than 3 months | £375 |

| More than 3 months but not more than 6 months | £750 |

| More than 6 months | £1,500 |

As you can see, the costs add up quickly.

And here’s the real kicker: these penalties are doubled if your accounts are filed late two years in a row. That initial £150 fine suddenly becomes £300, and the maximum £1,500 penalty balloons to a crippling £3,000.

The financial penalties are just the beginning. The wider consequences of late filing can inflict far more lasting damage on your business's reputation and operational ability.

Of course, these filings are just one piece of the puzzle. A business must manage all its financial responsibilities, which might include things like needing to calculate Capital Gains Tax on asset sales – another crucial task where diligence is key.

The Damage Beyond the Fines

While a surprise bill is never welcome, the non-financial consequences can hurt your business even more in the long run. Missing your Companies House filing deadlines sends a massive red flag to credit agencies, suppliers, and lenders.

-

Damaged Credit Rating: Late filings are a black mark on your public company record. Credit reference agencies see this as a sign of poor financial management, and your business credit score will almost certainly take a nosedive. A poor score makes it much harder and more expensive to get loans, leases, or even good payment terms with suppliers.

-

Risk of Prosecution: As a company director, you are legally responsible for ensuring these documents are filed on time. Persistent failure to do so isn't just bad practice; it's a criminal offence. Directors can be personally prosecuted and fined, putting their own finances and reputation on the line.

-

Company Strike-Off: In the worst-case scenario, the Registrar of Companies might assume the company is no longer trading and start the process of striking it from the register. If your company is struck off, it legally ceases to exist. Its assets—including any cash in the company bank account—become the property of the Crown.

It’s clear that filing on time is about much more than just ticking a compliance box. It’s fundamental to your business’s survival and credibility.

Even with the best intentions, sometimes life just gets in the way of your Companies House filing deadlines. A fire at your office, the sudden loss of critical records, or a key director falling seriously ill – these are the kinds of genuine crises that can derail even the most organised business.

Thankfully, Companies House has a process for these exact situations. You can formally apply for an extension, but it's vital to understand this isn't a get-out-of-jail-free card for poor planning. It’s strictly for exceptional circumstances.

One crucial point to remember: you can only request an extension for your annual accounts, not your Confirmation Statement. The golden rule is to apply before your original filing deadline hits. If you wait until after the date has passed, your request will almost certainly be rejected, and you'll be hit with an automatic late filing penalty.

What Counts as a Valid Reason for an Extension?

Companies House will only consider granting an extension for reasons that are truly unforeseen and outside of your control. Forgetting the date, being too busy, or your accountant going on holiday just won't cut it.

So, what does qualify? Legitimate reasons usually fall into a few categories:

- Sudden Illness: A director responsible for the accounts is unexpectedly incapacitated.

- Unforeseen Events: Something catastrophic like a fire, flood, or a major IT meltdown destroys your company records.

- Bereavement: The death of a director's close family member right before the filing deadline.

When you apply, you need to be specific and explain the situation clearly. A vague request without a compelling reason is destined to be denied.

Precedent During National Crises

We've seen Companies House be flexible during widespread emergencies. The COVID-19 pandemic is a perfect example. The government introduced measures to give businesses breathing room, initially allowing companies to apply for a three-month extension.

This later became an automatic extension for deadlines falling between June 2020 and April 2021. You can read more about these emergency measures to see how government policy can shift filing obligations during a major crisis.

Think of an extension as an emergency parachute, not a standard business strategy. The best plan is always to file well ahead of your deadline, so you never need to pull the cord.

If you find yourself in a genuine crisis and believe you have a valid reason for an extension, you should contact Companies House immediately. You can do this yourself or ask your accountant to handle it. The key is to present a clear, honest case—that's your best shot at getting the extra time you need to get back on your feet.

Common Questions About Filing Deadlines

Once you get your head around the main rules, it’s often the oddball situations that cause the most confusion. What if the company is dormant? What happens if you spot a mistake after filing? Getting these details right is what separates a smooth compliance process from a stressful one.

Let's walk through some of the most frequent questions we hear from directors. This should give you the confidence to handle these tricky scenarios like a pro.

My Company Is Dormant – Do I Still Need to File?

Yes, absolutely. This is probably the biggest tripwire for new directors. A dormant company – one with no ‘significant accounting transactions’ in a financial year – is still on the Companies House register, and that means it still has filing duties.

Even if your company hasn't traded a penny, you must file two things every year:

- Dormant Accounts: These are a stripped-back, simpler version of full accounts, but they are mandatory.

- A Confirmation Statement: Just like an active company, you still need to confirm that the company's details on public record are correct.

The deadlines are the same, and crucially, so are the penalties. Don't fall into the trap of thinking "no activity" means "no paperwork." Companies House will issue the same fines and could eventually strike the company off the register if you ignore these obligations.

How Do I Correct a Mistake in My Filed Accounts?

It’s a heart-sinking moment: you’ve filed your accounts and then you spot a mistake. Don't panic. You can’t just delete the old filing, but there is a formal process for putting it right.

You need to prepare a new, corrected set of accounts. On the balance sheet of this revised version, you must clearly state that they are ‘amended’ accounts, which a director then signs off. This new document gets filed alongside the original, making the correction transparent on the public record. It's always best to act quickly, especially for significant errors, to keep your company's information accurate.

Key Insight: Your legal duty isn't just to file on time, but to ensure the information filed is true and fair. Fixing mistakes shows you're a responsible director and maintains the integrity of your company's public record.

Is My Accountant Responsible for a Missed Deadline?

This is a critical point to understand: no. The legal responsibility for filing documents on time rests entirely with the company directors.

You can, of course, hire an accountant to prepare and submit everything for you—and for most businesses, that's a very sensible thing to do. However, your accountant acts as your agent. If they miss a deadline, the penalty notice from Companies House will be sent to the directors, not them. Your relationship with your accountant is a private matter; in the eyes of the law, the buck stops with you.

Where Can I Check My Company's Deadlines?

The definitive source for your company's deadlines is the official Companies House online service. It's free, completely up-to-date, and the only place you should rely on for this information.

Just pop your company name or number into their search bar. The main page for your company will clearly show the due dates for your next accounts and confirmation statement.

Better yet, sign up for their free email reminder service. This is a brilliant, simple tool that sends you a heads-up as your Companies House filing deadlines get closer. It’s a five-minute job that can save you a lot of money and stress down the line.

Keeping on top of deadlines and ensuring every detail is correct can feel like a full-time job in itself. At Stewart Accounting Services, we take that entire burden away. We manage all your Companies House filings, from annual accounts to confirmation statements, making sure every deadline is hit, every time. You focus on running your business; let us handle the compliance. Find out how we can give you complete peace of mind at https://stewartaccounting.co.uk.