A director loan account (DLA) is simply a record of all the money flowing between you and your limited company that isn't salary, a dividend, or an expense repayment. It’s a running tally, showing whether you’ve personally lent money to the business or, more frequently, borrowed money from it. Getting this right is absolutely critical for staying compliant and keeping your finances healthy.

Demystifying the Director Loan Account

Don't think of the DLA as a separate bank account. It’s more like an internal IOU ledger or a "tab" you keep with your company. It meticulously tracks money moving in both directions, creating a clear, official record. Every time you dip into company funds for a personal reason—maybe to cover an unexpected home repair—or you put your own savings in to tide the business over, it gets logged in the DLA.

Keeping this record straight is vital because HMRC scrutinises these transactions very closely. Without a DLA, it's a messy and confusing picture, making it impossible to tell the difference between legitimate business expenses, your salary, dividends, and personal loans. This separation is fundamental; it reinforces the legal fact that your company is a completely separate entity from you.

The Two Sides of a DLA

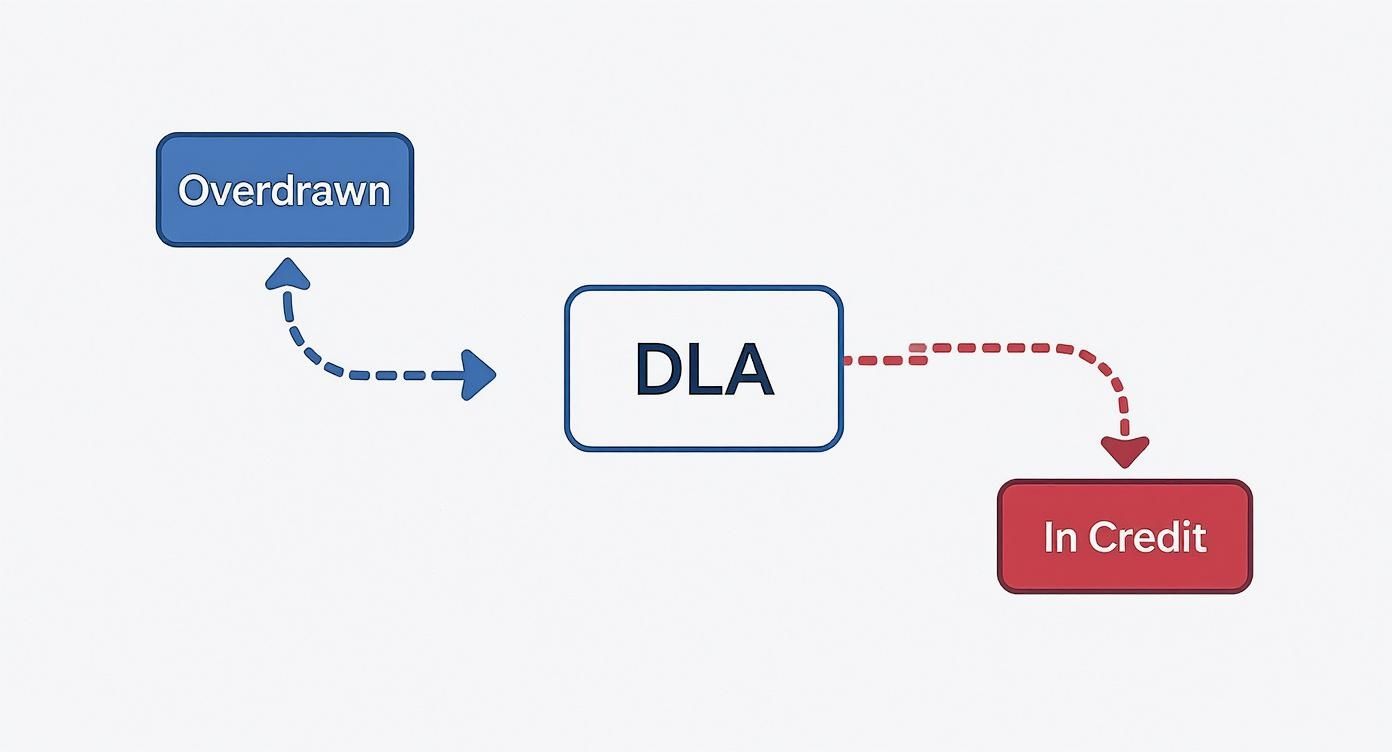

Your director loan account can be in one of two states, and it's essential to understand the difference. The status of the account has major implications for both you and your company.

The infographic below neatly illustrates the two possible states of a DLA.

As you can see, it all comes down to who owes whom. Let's break down what each scenario means in practice.

Here’s a quick summary to help you keep track of the two states of a Director Loan Account.

Director Loan Account At a Glance

| DLA Status | Who Owes Whom? | Common Scenarios | Primary Concern |

|---|---|---|---|

| In Credit | The company owes the director. | Director provides start-up capital; covers a large bill with personal funds. | Ensuring the company can repay the director when needed. |

| Overdrawn | The director owes the company. | Director withdraws funds for personal use; pays for personal items with the company card. | Potential tax charges for both the company and the director. |

This table shows at a glance the fundamental difference and the main thing you need to be aware of in each situation.

Let's dive a little deeper into these two states.

-

DLA in Credit: This is the straightforward one. It means you have lent money to your company, and the business owes you that money back. You are effectively a creditor of your own company. This often happens when a business is just starting out, and directors inject personal cash to get it off the ground. The great thing here is that the company can repay you from this credit balance without any immediate tax headaches.

-

DLA is Overdrawn (or in Debit): This is where things get more complicated. It means you have borrowed money from your company. You now owe the business, and this is where strict tax rules and legal duties kick in. An overdrawn DLA can trigger some hefty tax charges if it isn't managed and repaid properly within specific timeframes set by HMRC.

An overdrawn director loan account is one of the most common compliance traps for small business owners. If you don't understand the rules, you can be hit with unexpected and substantial tax bills for the company, and even personal tax liabilities for yourself.

Keeping this distinction crystal clear is the first step towards good financial management. While a DLA offers some welcome flexibility, letting it become overdrawn requires your full attention to avoid making some very costly mistakes.

Navigating Overdrawn DLA Tax Rules

When your director's loan account goes into the red, it's a bit like borrowing from your company's future. It’s a handy tool for short-term flexibility, but it also brings you face-to-face with some pretty strict tax rules from HMRC. If you’re not careful, ignoring them can land your company with a hefty, and often unexpected, tax bill.

The big one you need to know about is the Section 455 charge. HMRC brought this in to stop directors from using their companies as personal piggy banks, pulling out cash without paying the usual income tax or National Insurance.

The Section 455 Charge Explained

You can think of the Section 455 charge (or S455, as it’s often called) as a hefty deposit your company has to pay HMRC if a director's loan isn't repaid on time. It's a temporary tax, but it can put a serious dent in your cash flow.

The trigger is simple: an outstanding loan that hasn’t been paid back within nine months and one day of your company's financial year-end.

This rule, officially Section 455 of the Corporation Tax Act 2010, was designed to level the playing field. The S455 tax rate is 33.75%. So, if you borrowed £20,000 from the company and didn't repay it within that nine-month window, the business would be hit with an extra tax payment of £6,750 on top of its usual corporation tax.

It's really important to remember this isn't a penalty—it's a refundable charge. Once the loan is fully repaid, the company can claim the S455 tax back from HMRC. The catch is that the refund process isn't instant and can tie up your company’s cash for a long time. For a closer look at the nuts and bolts, it’s worth digging deeper into the specifics of Section 455 tax.

How The Timeline Works

When it comes to managing an overdrawn DLA and avoiding an S455 charge, timing is everything.

Let's walk through a quick example to see it in action.

- Company Year-End: 31st March 2024

- Director's Loan Balance: £15,000 overdrawn

- Repayment Deadline: 1st January 2025 (nine months and one day later)

If the director repays the full £15,000 before 1st January 2025, everything is fine. No S455 tax is due. Simple. But if that date comes and goes with the loan still outstanding, the consequences kick in immediately.

Your company must pay S455 tax of £5,062.50 (£15,000 x 33.75%) to HMRC. This tax is due on the same day as your main Corporation Tax bill, which is also nine months and one day after your year-end.

This shows just how quickly a manageable loan can turn into a major financial headache for the business. This isn't a tax on profits; it's a separate charge levied directly on the loan balance.

Key Points to Remember

To make sure you don't get caught out, keep these key points in mind:

- The Clock is Ticking: That nine-month repayment window is non-negotiable. Being late by even one day triggers the full charge on the outstanding amount.

- It’s the Company's Liability: The director is personally responsible for paying back the loan, but it’s the company that has to cough up the S455 tax to HMRC. This hits the business's cash reserves directly.

- Partial Repayments Help: The tax is calculated on whatever is left unpaid at the deadline. If you repaid £10,000 of the £15,000 loan in our example, the charge would only apply to the remaining £5,000.

Properly managing your director's loan account just means staying aware of your company's year-end and that crucial repayment deadline. A bit of forward planning is all it takes to keep this particular tax problem from ever becoming your problem.

Understanding Benefit-in-Kind Charges

It's not just the company that can get hit with a tax bill. If your director's loan account is overdrawn, you could find yourself with a separate, personal tax liability. This happens when HMRC views the loan as a perk of your job – essentially, an interest-free or cheap loan you wouldn't get on the open market.

This taxable perk is known as a Benefit-in-Kind (BIK).

The trigger for this is a specific number: £10,000. If your loan is overdrawn by more than this amount at any point during the tax year, a BIK charge comes into play. Stay under that threshold, and you're generally in the clear on this front. But the moment you cross it, HMRC considers the 'benefit' part of your income, and you'll have to pay tax on it.

How HMRC Calculates a Benefit-in-Kind

So, what is this "benefit" worth? HMRC looks at it as the interest you should have paid if you’d taken out a normal commercial loan. To make it fair and consistent, they set an official interest rate for exactly these situations.

Right now, that rate for beneficial loans is 2.25% per annum. If your company charges you less than this (or, more commonly, nothing at all), the difference is what you'll be taxed on. You can always check the latest figures by reading the official guidance on beneficial loan arrangement rates from GOV.UK.

Let's run through a quick example to see how this works in the real world.

Example Calculation:

- A director borrows £20,000 from their company. No interest is charged.

- The loan is outstanding for the entire tax year.

- HMRC's official interest rate is 2.25%.

The taxable benefit is calculated like this: £20,000 x 2.25% = £450.

This £450 gets added to the director's total income for the year, meaning they'll pay income tax on it at their usual rate (be it 20%, 40%, or 45%).

This is a crucial point: even if you repay the loan on time and the company completely avoids the S455 charge, you could still face a personal tax bill just for having had the loan in the first place.

Reporting Duties for the Company and Director

When a BIK charge applies, it kicks off a bit of paperwork for both the company and you, the director. It’s not enough to just know the tax is due; it has to be formally declared to HMRC.

Here’s a breakdown of the key responsibilities:

- The P11D Form: The company is required to report the loan benefit to HMRC using a P11D form. This is the standard document for declaring all benefits-in-kind given to directors and employees.

- Class 1A National Insurance: On top of everything else, the company must also pay Class 1A National Insurance Contributions (NICs) on the value of the benefit. This is an extra cost for the business to bear.

- Director's Self-Assessment: You must declare the benefit amount on your personal Self-Assessment tax return. This ensures the income tax is collected correctly.

It's worth noting that a BIK like this is treated very differently from small, everyday perks. To get a better sense of this, you might want to read our article on the difference between taxable benefits and trivial benefits. It helps clarify why a director's loan gets this specific tax treatment.

Getting this reporting wrong can lead to penalties and interest from HMRC for both sides, so it really pays to be organised. Any director's loan over £10,000 needs careful management to keep both your personal and company tax affairs in good order.

Your Legal Duties Under Company Law

It's easy to focus on the tax side of things, but your director's loan account is also governed by a strict set of legal duties under the Companies Act. These rules aren’t just red tape; they exist to protect the company as its own legal entity and ensure directors are always acting in its best interests, not just their own. Mismanaging a DLA isn't merely a financial hiccup—it can be a serious breach of your legal obligations as a director.

One of the biggest legal hurdles kicks in with larger loans. If you borrow more than £10,000 from your company, you almost always need formal approval from the shareholders. Now, if you're the sole director and shareholder, this might feel like you're just giving yourself permission. But don't skip it. Properly documenting this approval with a board minute and a written resolution is a vital piece of corporate housekeeping. It proves the transaction was above board and officially signed off on.

Your Duty to the Company

At its heart, your job as a director is to promote the success of the company for the benefit of all its members. A large, unpaid director's loan can create a direct conflict of interest. When you borrow a significant amount, you’re taking working capital out of the business—money that could have been used to invest in new equipment, fund growth, or simply pay the bills.

This gets particularly sticky if the business hits a rough patch. Should the company face insolvency, that outstanding DLA isn't just a personal IOU. It’s a company asset, and a liquidator will come knocking to get it back for the creditors.

A liquidator’s number one job is to claw back every penny owed to the company to pay its creditors. An overdrawn director's loan is often one of the first things they look for, and they have the full force of the law behind them to pursue you personally for the entire amount.

The Insolvency Risk

Director's loans are incredibly common, especially in smaller businesses where they offer a bit of flexibility with cash flow. But that flexibility comes with a very sharp edge if the company goes under. When a business fails, any money you owe it through your DLA is immediately treated as a debt that must be repaid into the insolvent estate.

Failing to repay is a serious matter. A liquidator can and will take legal action against you, which could lead to a court judgement or even personal bankruptcy. This is why managing your DLA properly is so important; it keeps that crucial line between you and the company clear, avoiding the personal liability risks of piercing the corporate veil.

Ultimately, all these legal duties boil down to one simple principle: the company's money is not your money. To get a better handle on your wider obligations, it's a good idea to refresh your memory on the full scope of your role. You can learn more by reading our guide on understanding the responsibilities of company directors. This helps ensure every financial decision you make—including taking a loan—is fully aligned with your legal duties.

Best Practices for DLA Record Keeping

Clear, meticulous records are your best defence against compliance headaches with your director's loan account. Think of good record-keeping not as a chore, but as essential maintenance. It's what protects both you and your business from costly complications with HMRC.

Taking a systematic approach from the get-go ensures every transaction is transparent and justifiable. This helps maintain that crucial legal wall between your personal finances and the company's.

Set Up a Dedicated DLA Ledger

First things first, create a specific ledger for the DLA within your accounting software. This isn't just a side note or a memo in a spreadsheet; it needs to be a formal account that tracks every single penny moving in or out.

This dedicated ledger becomes the single source of truth for your director's loan account. Every entry needs a date and a clear description explaining the transaction, whether it's a withdrawal you've made or a repayment back into the company.

Getting the categorisation right is absolutely vital. Accidentally logging a loan withdrawal as a business expense, for example, will throw off your company accounts and could lead to some very serious tax reporting errors.

For a deeper dive into managing your books effectively, you might find these practical small business bookkeeping tips quite useful.

Create a Formal Loan Agreement

This might sound like overkill, especially if you're the sole director and shareholder, but a formal written loan agreement is a vital document. It solidifies the arrangement as a legitimate, arm's-length transaction in the eyes of the law and, more importantly, HMRC.

The agreement doesn't need to be dozens of pages long, but it should clearly lay out the key terms of any significant loan.

A solid loan agreement should include:

- The names of the parties (that's you, the director, and your limited company).

- The total amount of the loan that has been approved.

- The agreed interest rate, if any is being charged.

- The repayment schedule and the terms for clearing the debt.

Having a formal agreement in place is a powerful piece of evidence. It demonstrates that the transaction was properly authorised and removes any ambiguity, which is invaluable if your accounts are ever subject to an HMRC enquiry.

Maintain Regular Reconciliations

Finally, don't let the director's loan account become an afterthought you only dust off at year-end. Regular reconciliation is the key to staying on top of your obligations and stopping small issues from spiralling into major problems.

Make it a habit to review your DLA at least once a quarter, or even better, every month. This simple practice helps you to:

- Spot Errors Quickly: You can catch any miscategorised transactions or incorrect entries before they get buried in months of data.

- Monitor Your Balance: Keep a close eye on the outstanding amount, making sure you know if it's creeping up towards that £10,000 Benefit-in-Kind threshold.

- Plan for Repayment: It allows you to proactively manage repayments, so the nine-month S455 tax deadline doesn't sneak up on you.

Consistent oversight turns your DLA from a potential liability into a manageable financial tool. These simple, disciplined practices provide clarity, ensure compliance, and ultimately, give you peace of mind.

Clever Ways to Repay Your Director Loan

https://www.youtube.com/embed/lfSFyrRzzXw

So, you've got an overdrawn director's loan account. The clock is ticking, and HMRC's interest is piqued. The good news is that sorting it out isn't just about wiring money back into the business account—though that's one option. How you choose to repay the loan can make a real difference to both your personal tax bill and the company's finances.

Getting this right is all about picking the smartest, most compliant route for your specific situation. The most common paths involve declaring a dividend, taking a salary or bonus, or simply repaying the cash from your own pocket. Let's look at what each one actually means for you.

H3: Comparing Your Repayment Options

The best way to clear your loan really hinges on the company's financial health and your own tax circumstances. There’s no single "right" answer, just the one that works best for you.

-

Declare a Dividend: This is often the go-to method for a reason. If your company has enough retained profits after tax, it can declare a dividend in your name. Instead of paying that cash out to you, it's credited directly to your loan account, reducing what you owe. The beauty of this is that dividend tax rates are generally kinder than income tax rates.

-

Pay a Salary or Bonus: Another option is for the company to award you a salary or a one-off bonus. That amount is then used to clear your loan balance. It's a perfectly legitimate approach, but it’s usually less tax-efficient. The payment will be hit with both income tax and National Insurance for you, and the company gets to pay employer's NICs on top.

-

Make a Direct Repayment: This is the simplest method by far. You just transfer the money from your personal bank account straight back to the company. It’s a clean transaction that squares things away with no immediate tax headaches, as you're just returning what you borrowed.

To help you weigh these up, here’s a straightforward comparison of the main repayment methods. It highlights what each one means for you and the business when it comes to tax.

Comparing Director Loan Repayment Methods

| Repayment Method | How It Works | Tax Implications for Director | Tax Implications for Company |

|---|---|---|---|

| Dividend | Company profits are declared as a dividend and credited to the DLA. | Dividend tax is payable, but no National Insurance. | Corporation Tax must be paid on profits before the dividend is declared. |

| Salary/Bonus | A bonus is paid and credited to the DLA instead of being paid out. | Subject to Income Tax and employee's National Insurance. | The bonus is a tax-deductible expense but is subject to employer's NI. |

| Cash Repayment | Personal funds are transferred directly to the company. | No personal tax implications on the repayment itself. | No tax implications; the company's cash balance is simply restored. |

Ultimately, choosing between a dividend, a bonus, or a direct repayment comes down to a numbers game. It pays to run the figures with your accountant to see which option leaves everyone in the best financial position.

H3: Dodging the 'Bed and Breakfasting' Trap

Be warned: HMRC has seen every trick in the book. They have specific anti-avoidance rules in place to stop directors from making a loan disappear on paper, only for it to reappear a few days later. The most famous of these is known as 'bed and breakfasting'.

It’s a classic manoeuvre where a director repays their loan just before the nine-month deadline (avoiding the S455 tax charge), only to take out a similar sum right after the new accounting year kicks off.

HMRC views this as a revolving door, not a genuine repayment. If you repay a loan of more than £5,000 and then take out a similar amount within 30 days, they will likely ignore the repayment and hit the company with the S455 tax anyway.

The key takeaway is to make sure any repayment is final and not just a temporary fix. Stick to a clean, well-documented method like a properly declared dividend or a straightforward cash transfer to stay on the right side of the rules.

Director Loan Account FAQs

Once you get your head around the basics of a director's loan account, a lot of specific "what if" questions tend to pop up. Let's tackle some of the most common queries we hear from directors, giving you clear, straightforward answers to help you manage your DLA confidently.

Can I Have a DLA as a Sole Director?

Yes, of course. In fact, it's the norm for most owner-managed businesses where one person is both the director and the shareholder. Just remember, running a one-person company doesn't mean you get a pass on the rules.

Every regulation that applies to an overdrawn director's loan account is still in full effect. That means the potential for a Section 455 tax charge, benefit-in-kind implications for loans over £10,000, and your overarching duty to act in the company's best interests. To keep things clean and legally separate, it’s always smart to draw up a formal loan agreement, even if it feels like you're just making it with yourself.

What if I Can't Repay My Loan on Time?

This is a big one. If you find yourself unable to clear your director's loan within nine months and one day of your company's year-end, the business will have to pay S455 tax on whatever balance is left. The rate is currently a painful 33.75%.

The good news is that this tax is temporary. Once the loan is fully repaid, your company can claim back every penny of the S455 tax from HMRC. The bad news? The reclaim process can be slow, which can put a serious dent in your company's cash flow in the meantime.

Is a Director Loan Better Than a Higher Salary?

It really depends on what you're trying to achieve with your overall tax planning. A director's loan can give you fantastic short-term flexibility, letting you access cash without the immediate hit of National Insurance that comes with a bigger salary. But it's absolutely not a long-term strategy for taking profits out of the business.

Once a loan tips over £10,000, it triggers a personal Benefit-in-Kind tax charge, and the S455 tax is always waiting in the wings if it isn't repaid promptly. For most directors, the sweet spot for tax efficiency is a blend of a modest salary and regular dividends. Think of the director's loan account as a tool for short-term, temporary needs, not your main source of income.

Can the Company Write Off My Director Loan?

While a company can technically forgive or 'write off' a director's loan, it's almost always a very expensive way to deal with it. When a loan is written off, HMRC generally treats that forgiven amount as if it were income for the director.

This means you’ll face both income tax and Class 1 National Insurance contributions on the full amount. On top of that, the company gets hit with an employer's NI bill. In virtually every case, it’s far more tax-efficient for everyone to repay the loan through proper channels, like declaring a dividend or a bonus.

At Stewart Accounting Services, we demystify the complexities of running a limited company, from managing your director loan account to optimising your tax strategy. Let us handle the details so you can focus on growth. Discover how we can bring clarity and control to your finances.