If you're a director of a UK limited company, you've probably heard the term 'Directors Loan Account' or 'DLA'. It’s one of those bits of accounting jargon that can sound more complicated than it really is.

A directors loan account isn't a separate bank account you can log into. Instead, think of it as a running tally within your company's books. It simply tracks the money that moves between you, the director, and your company—specifically, any money that isn't part of your salary, a dividend payment, or a direct reimbursement for a business expense.

Getting this right is crucial for keeping your finances clean and staying on the right side of HMRC.

Understanding Your Directors Loan Account

At its heart, your Directors Loan Account (DLA) is a straightforward IOU ledger. It keeps a record of any personal money you lend to the business and any company money you borrow for personal reasons.

Every single limited company in the UK has a DLA for each of its directors, even if the balance is zero. Keeping this record accurate isn't just good housekeeping; it’s a legal necessity under the Companies Act 2006. More importantly, HMRC pays very close attention to DLAs to make sure directors aren’t pulling money out of their companies without paying the right amount of tax.

The status of your DLA can be in one of two states: in credit or overdrawn.

When Your DLA Is in Credit

This is the simple one. Your DLA is in credit when your company owes you money. It's a common scenario, especially in the early days of a business when you might be using personal funds to get things off the ground.

Here are a few ways your DLA might end up in credit:

- Start-up cash: You put your own money into the business to buy equipment or cover initial running costs.

- Paying for things personally: You use your own credit card to pay for a business subscription or a train ticket to a client meeting, and the company hasn't paid you back yet.

- A cash injection: You transfer some personal savings into the business account to help with cash flow during a quiet month.

When your DLA is in credit, you're free to draw that money back out of the company completely tax-free. It's not income; it's simply your company repaying a loan.

When Your DLA Is Overdrawn

Now for the other side of the coin. Your DLA is overdrawn when you owe the company money. This is where things can get tricky, and if you’re not careful, it can lead to some hefty tax bills. An overdrawn DLA is essentially a loan from your company to you.

An overdrawn directors loan account can be a flexible tool for directors, but it comes with strict HMRC rules. Failing to understand and manage an overdrawn balance is one of the most common—and costly—mistakes a director can make.

An overdrawn balance can happen for a few reasons:

- You take cash out of the business for something personal.

- The company pays a personal bill for you directly, like your home council tax or a family holiday.

- You accidentally declare and take a dividend that's larger than the company's available post-tax profits.

Understanding the difference between these two states is the first, most important step. An overdrawn DLA, in particular, has specific tax rules that we’ll dive into next, including the infamous Section 455 charge.

Directors Loan Account Status At a Glance

To quickly see the difference, this table breaks down the two states of a DLA.

| Status | Who Owes Whom? | Immediate Implication | Common Transactions |

|---|---|---|---|

| In Credit | The company owes the director | The director can withdraw funds tax-free up to the amount owed | Director lending money to the company; paying for business expenses with personal funds. |

| Overdrawn | The director owes the company | Potential tax liabilities for both the director (Benefit-in-Kind) and the company (s455 charge) if not repaid promptly | Director taking cash for personal use; company paying a director's personal bill. |

Essentially, keeping your DLA in credit is straightforward. Letting it become overdrawn requires careful management to avoid falling foul of HMRC's rules.

Navigating the Tax Risks of an Overdrawn Directors Loan

Taking a short-term loan from your own company can be incredibly convenient, but letting that loan go unpaid can create a massive financial headache. HMRC has very clear, and very strict, rules designed to stop directors from using their company as a personal, tax-free piggy bank.

The main weapon in their arsenal is the Section 455 (s455) tax charge.

This isn't just a slap on the wrist. It’s a hefty tax, deliberately designed to be painful enough to make you think twice about leaving a director's loan outstanding for too long. If your loan is still unpaid more than nine months after your company's year-end, the business gets hit with a special corporation tax on the full amount.

The Nine-Month Rule and the S455 Charge

The critical deadline you need to burn into your memory is nine months and one day after your company's accounting year ends. If your DLA is still overdrawn by that date, your company is on the hook for the s455 tax.

The Section 455 Corporation Tax Charge is a hefty 33.75% of whatever the outstanding loan balance is.

To put that into real-world numbers, let's say you borrow £20,000 from your company. Your year-end is 31 March. If you haven't paid that back by the following 1 January (which is nine months and a day later), your company will face an immediate tax bill of £6,750. That’s £20,000 multiplied by 33.75%. An unexpected bill of that size can seriously dent a small business's cash flow.

Now, it's important to know this is technically a temporary tax. Once the director finally repays the loan in full, the company can claim back the s455 tax it paid. The problem is, the reclaim process isn't instant. It can take a while, and in the meantime, that cash is out of your business account. This is exactly why getting ahead of the issue is so vital.

"The s455 regime has become increasingly complex over the years as HMRC introduce new legislation and anti-avoidance provisions… it is more important than ever to ensure that loans and repayments are properly documented and professional advice is sought at the earliest possible stage."

Avoiding the Bed and Breakfasting Trap

HMRC is wise to the obvious loopholes. They quickly cottoned on to directors trying to sidestep the charge with a tactic known as "bed and breakfasting". This is where a director repays the loan just before the nine-month deadline, only to take the exact same amount of money back out again a few days later.

To stop this, they brought in some powerful anti-avoidance rules. Here’s how they work in a nutshell:

-

The 30-Day Rule: If you repay a loan of over £5,000 but then borrow a similar amount back within 30 days, HMRC will simply ignore the repayment. The original loan is treated as if it was never cleared, and the s455 tax applies.

-

The Arrangements Rule: Even if you wait longer than 30 days, if HMRC can show there was a pre-existing plan or 'arrangement' to re-borrow the funds, they can still apply the charge.

These rules ensure that repayments have to be genuine and permanent to count. For a more detailed breakdown of how this works, have a look at our guide on what is Section 455 tax. The only sure-fire way to avoid this costly penalty is to plan your repayments carefully and genuinely clear the debt.

Watch Out for Interest and Benefit in Kind Rules

That hefty s455 charge isn't the only tax headache an overdrawn director's loan can cause. If you're not careful, it can create a personal tax problem for you, too. This is where HMRC’s Benefit in Kind (BIK) rules kick in, treating an interest-free or cheap loan from your company as a taxable perk of your job.

HMRC sees it like this: if you’ve borrowed more than £10,000 from your company at any point in the tax year and you're not paying a commercial rate of interest, you're getting a valuable benefit. It’s not cash, but it’s still taxable.

To sidestep this tax charge, you need to pay interest back to your company on the loan. The crucial part is that the interest rate you pay must be at least what HMRC calls the ‘official rate of interest’.

HMRC's Official Rate of Interest

This isn't a number you can just pluck out of thin air. It’s a specific rate set by HMRC, and it can change, so you need to stay on top of it.

In fact, a recent change has made this more important than ever. The Official Rate of Interest has hit its highest point in over a decade, jumping from 2.25% to 3.75% from 6 April. This is a big increase, reflecting what’s been happening in the wider economy. If your loan is over £10,000, you have to use this rate to calculate the interest, or you’ll face a BIK charge.

Calculating the interest can get a bit tricky, as it’s usually worked out on the average loan balance over the course of the year. But as long as you pay interest at or above this official rate, the whole BIK problem goes away completely.

The key is not just to calculate the interest, but to physically pay it to the company. Simply making a bookkeeping entry to 'roll up' the interest isn't enough to satisfy HMRC's requirements.

The Consequences of Getting It Wrong

If you miss this or get the interest calculation wrong, it triggers a double whammy of tax consequences – one for you personally, and one for your company.

-

For you, the Director: The value of the benefit – essentially, the interest you should have paid – gets reported on a P11D form. This figure is then added to your total income for the year, and you’ll pay income tax on it at your usual rate (20%, 40%, or 45%).

-

For the Company: The business isn't off the hook either. It has to pay Class 1A National Insurance on the full value of that benefit. The current rate for this is 13.8%.

So, you end up with a personal tax bill and your company gets hit with a National Insurance bill. It’s a classic tax trap. Getting to grips with these rules is just as vital as understanding other taxable company benefits. When you manage your DLA properly, it’s a brilliant, flexible tool; when you don’t, it becomes an expensive mistake.

How to Correctly Record and Manage Your DLA

Good bookkeeping is your best defence against any director's loan account headaches. When you keep clear, accurate records, you always know where you stand with your DLA balance. This real-time view helps you sidestep nasty tax surprises and make smarter financial decisions throughout the year. Thankfully, modern accounting software makes this whole process much easier than it used to be.

The first step is to get the DLA set up properly in your company's books. It needs to be created as a liability account within your chart of accounts. To get the numbers right, you'll need a basic grasp of double-entry bookkeeping principles, as every transaction will always impact at least two different accounts.

Setting Up and Tracking Your DLA

Once your DLA is set up, every single financial movement between you and your company must be carefully recorded. I'm not just talking about big cash withdrawals; it's the small, everyday transactions that often catch people out. They can add up surprisingly quickly and push your account into an overdrawn state if you're not paying attention.

Here are the key transactions you absolutely must record:

- Cash Repayments: When you put your own money back into the company to pay down what you owe, this needs to be logged directly against your DLA balance.

- Personal Expenses Paid by the Company: Did the business card pay for a personal subscription or a non-work-related meal? That transaction increases the amount you owe the company and has to be posted to your DLA.

- Dividends or Salary: If you decide to use a declared dividend or your net salary to reduce your loan, make sure there’s a clear paper trail. This includes proper board minutes for any dividend declaration.

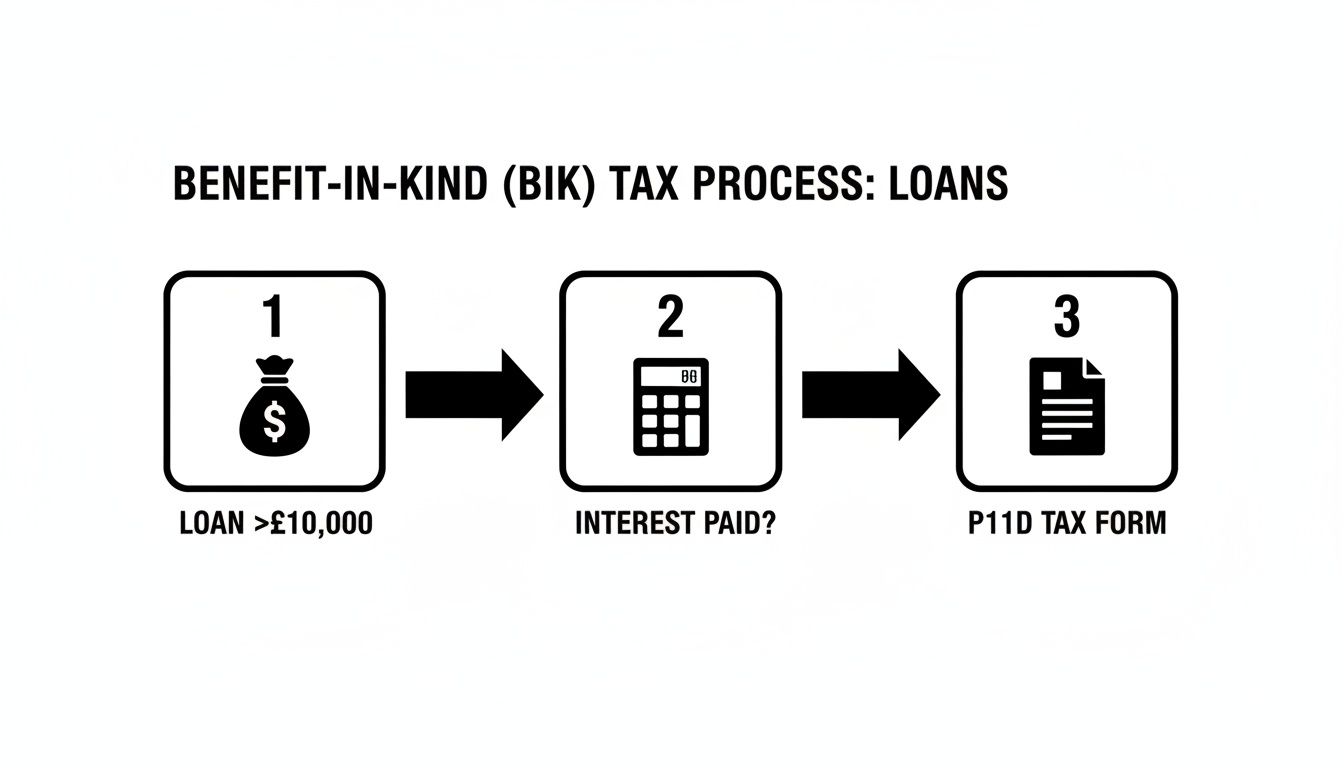

This flowchart shows how HMRC looks at loans over £10,000 that might be treated as a Benefit-in-Kind.

The key takeaway is that failing to pay the right amount of interest on a large loan is what triggers the need to file a P11D.

Using Accounting Software

Cloud accounting platforms like Xero or QuickBooks are brilliant for keeping your DLA in check. You can set up rules to automatically categorise regular payments and see your live DLA balance on a dashboard anytime you log in. That kind of financial clarity is invaluable.

Think about reconciling your DLA every month. It’s a simple habit that allows you to be proactive, stopping a small, manageable overdrawn balance from snowballing into a major tax problem at your year-end.

Consistent and accurate bookkeeping is what turns the DLA from a potential risk into a transparent and genuinely useful financial tool for any company director.

Smart Strategies for Repaying an Overdrawn Loan

Realising your director's loan account is overdrawn can certainly feel a bit stressful, but don’t panic. The important thing is to act decisively to get that balance back to zero. Thankfully, you have a few solid, legitimate options for repaying the debt and avoiding that nasty s455 tax charge.

Each repayment route has different tax consequences for both you and your company, so the best choice really comes down to your unique financial circumstances. The cleanest and most direct method is simply to repay the loan using your own personal funds. This is a straightforward transaction that directly cuts down what you owe the business.

But what if you don't have the personal cash on hand? Not a problem. You can use company profits or your own earnings to settle the debt, but this requires a bit more careful planning to make sure everything is done by the book.

Methods for Clearing Your DLA Balance

When it comes to using company money to clear an overdrawn loan, there are three main ways to go about it. Getting your head around how each one works is key to making the right call.

-

Declare a Dividend: If your company is sitting on enough post-tax profits (often called retained earnings), you can declare a dividend. Instead of the cash hitting your personal bank account, it gets credited straight to your DLA, which reduces or completely clears the overdrawn balance. For most director-shareholders, this is usually the most tax-efficient way forward.

-

Vote a Salary or Bonus: Another option is to pay yourself a salary or bonus through the company's payroll. Once PAYE tax and National Insurance have been deducted, the net pay is used to reduce your loan. This works perfectly well, but it’s generally less tax-friendly than a dividend because of the National Insurance contributions that both you and the company have to pay.

-

A Combination Approach: Sometimes, one method alone won't quite cut it. You might, for example, use a dividend to clear the lion's share of the loan and then top it up with a smaller cash repayment from your own funds to cover the rest.

Crucially, every single repayment decision must be formally documented, especially when it involves a dividend or bonus. You need proper board minutes to create a clear paper trail for HMRC, proving the transaction was legitimate and officially approved by the company.

This paperwork isn't just a box-ticking exercise; it's your primary defence if HMRC ever queries the repayment. Without it, they could potentially disregard the transaction, triggering the very tax penalties you were trying to sidestep. Your accountant can give you the correct templates for these vital records.

Common Pitfalls and Recent HMRC Rule Changes

Running a director's loan account isn't something you can set and forget. It needs careful attention because a few common slip-ups can snowball into some pretty serious tax headaches. On top of that, the rules aren't static; HMRC is always tightening things up, so staying on top of their latest focus is key to keeping your company safe.

One of the easiest traps to fall into is informal borrowing. A director might take out small sums here and there, thinking nothing of it, and then get a shock at the year-end when it all adds up to a hefty overdrawn balance. Without tracking these amounts as they happen, finding the cash to repay the loan before that critical nine-month deadline can become a real scramble.

Another classic mistake is getting caught by the ‘bed and breakfasting’ rules. This is where you repay a large loan just before the deadline only to take the same amount back out again shortly after. HMRC sees right through this and will treat it as if the loan was never repaid, landing your company with that painful s455 charge.

HMRC’s Tighter Grip on Repayments

HMRC has been cracking down on loopholes to make sure the rules are followed to the letter. A big one they've recently closed relates to when a loan is considered repaid. It used to be that some companies would claim relief on their tax return for a loan they intended to repay, even if the cash hadn't actually moved by the filing date.

That's no longer an option. HMRC has made it crystal clear: you can't claim relief for a loan you plan to repay. The only thing that counts is a genuine repayment made within the nine-month window after your company's year-end. This is the only way to reduce or cancel out a Section 455 tax charge. You can read up on the official guidance on the ICAEW website to see the specifics.

This change really hammers home a simple but vital point: when it comes to a DLA, what matters is the action, not the intention. HMRC only cares about when the money was actually and permanently repaid.

This shift means there’s no wiggle room. It puts the pressure squarely on directors to manage their DLAs with discipline throughout the year. A last-minute rush just won't cut it anymore—proactive, regular management is the only way to stay out of trouble.

Your Directors Loan Account Questions Answered

We get asked a lot of questions about the practical side of directors' loans. Let's tackle some of the most common real-world scenarios you might be wondering about.

Can I Use a Directors Loan for a House Deposit?

Technically, yes, but this is a move you need to make with your eyes wide open to the tax implications. Using company funds for a personal house deposit instantly puts your DLA into an overdrawn state.

If that loan tips over £10,000, it triggers Benefit in Kind (BIK) rules, meaning you'll need to pay interest to the company at HMRC's official rate to avoid a personal tax charge. More critically, if the loan isn't fully paid back within nine months and one day of your company's year-end, the business gets hit with a hefty s455 corporation tax bill.

Bottom line? Never do this without a solid repayment plan and a chat with your accountant first.

What Is the Difference Between a Directors Loan and a Dividend?

This is a fundamental distinction every director needs to grasp. Think of it this way: a directors loan is money you borrow from your company, and it absolutely has to be repaid. A dividend, on the other hand, is a share of the company's profits paid out to shareholders. It’s your money to keep.

The tax treatment is completely different, too. Dividends are taxed as part of your personal income. A loan isn't, but as we've seen, an overdrawn loan comes with its own set of complex tax headaches (s455 and BIK charges). Deciding which is better depends entirely on your company's cash position, its profitability, and your own personal tax circumstances.

What Happens to an Overdrawn DLA in Liquidation?

This is a serious situation. If your company goes into liquidation, any outstanding overdrawn director's loan is considered an asset of the company. The appointed liquidator has a legal duty to chase down all company assets to pay off creditors.

This means the loan doesn't just disappear. You become personally liable to repay the entire outstanding balance to the liquidator, who can and will take legal action against you to get the money back.

Navigating the rules around a directors loan account can feel like a minefield, but you don't have to walk it alone. The team at Stewart Accounting Services has the expertise to guide you, helping you stay compliant and make smart decisions for your business.

Reach out to us today for professional support and get the peace of mind you need.