So, you’ve decided it’s time to close your limited company. This isn't just about stopping trade; it’s a formal process that needs to be handled correctly to avoid any nasty surprises down the line.

When it comes to shutting things down, you essentially have two main roads you can go down. The path you choose hinges entirely on your company's financial situation—whether it’s solvent (can pay its bills) or insolvent (it can't).

Understanding the Company Closure Process

Closing a limited company is a big deal. It’s the final chapter, whether you're off to a new venture, hanging up your boots for retirement, or the business has just come to its natural end. But it's not as simple as just shutting the doors. There's a proper, formal dance to do with Companies House and HMRC to make sure your exit is clean and final.

Getting this right is absolutely critical. A clean closure protects you and your fellow directors from future legal headaches or financial claims. Get it wrong, and you could be facing penalties or investigations long after you thought you’d moved on. For a bird's-eye view of the entire winding-up process, this guide on how to wind up a company is a great resource.

Why You Can’t Just Walk Away

I've seen business owners tempted to just stop trading and let the company fade away, but trust me, that's a recipe for disaster. A formal closure is your shield. It proves you’ve tied up every legal and financial loose end properly.

In this guide, we'll walk you through the options available to UK business owners, cutting through the jargon. We’ll look at:

- Voluntary Strike-Off: The simplest, most direct route for solvent companies without a lot of baggage.

- Members' Voluntary Liquidation (MVL): A very tax-efficient way to close a solvent company that has significant assets or cash reserves.

- Creditors' Voluntary Liquidation (CVL): The necessary and responsible path for companies that are insolvent.

Of course, sometimes a full closure isn't what you need. If you think you might want to restart the business later, making it dormant could be a better fit. We have a whole other guide explaining how to make a company dormant if that sounds more like your situation.

For now, let's focus on a permanent closure, covering everything from the final accounts to telling everyone who needs to know.

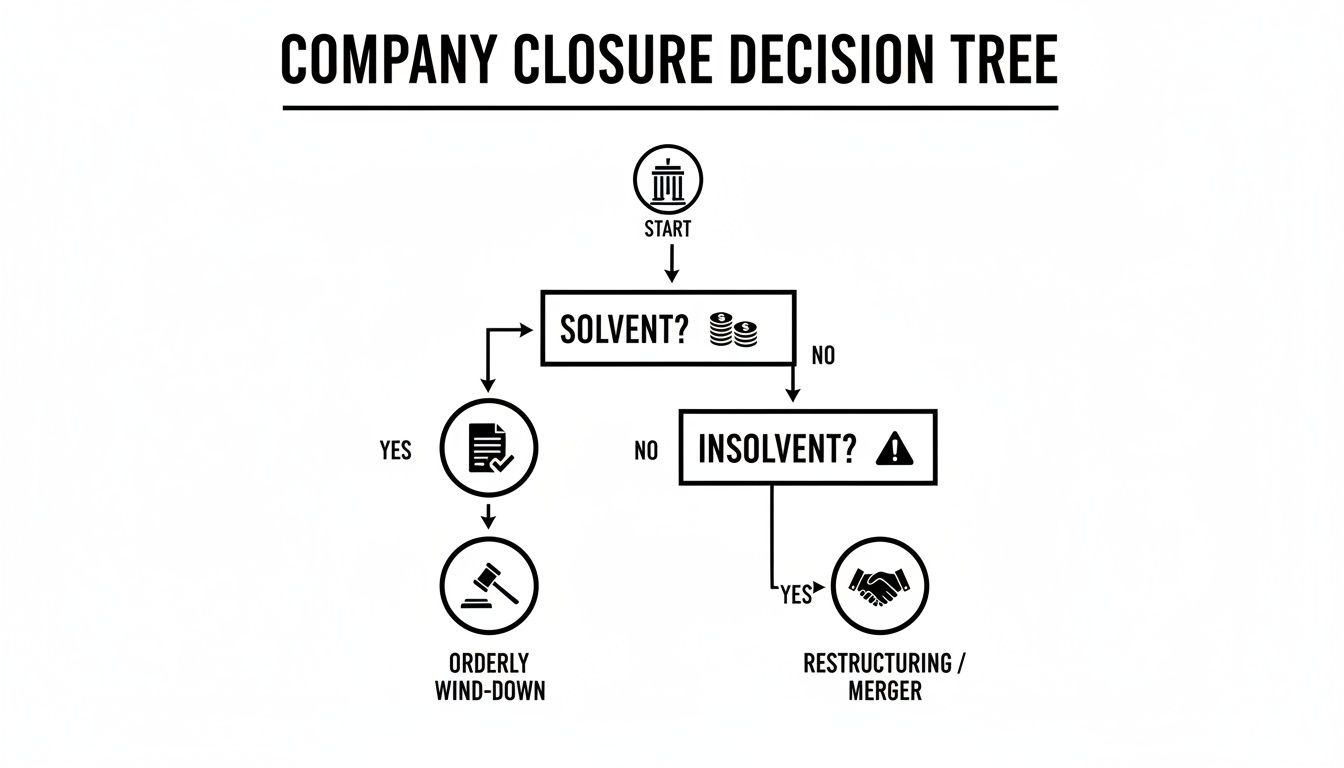

Choosing Your Path: Is Your Company Solvent or Insolvent?

Before you can even think about closing your company, you have to answer one fundamental question: can the business pay its bills? This isn't just a minor detail; it’s the critical fork in the road that determines every single step you take next.

Simply put, a company is solvent if it can comfortably pay all its debts within 12 months of shutting up shop. This includes everything from supplier invoices to tax liabilities. If your balance sheet is in the black, you’re in the driver's seat and have a couple of straightforward, low-stress options.

On the flip side, a company is insolvent if it can’t meet its financial obligations. The moment this happens, your legal duties as a director pivot dramatically. Your primary responsibility is no longer to the shareholders—it's to the creditors you owe money to.

This decision tree gives you a clear visual of how that one question of solvency dictates your entire closure journey.

As you can see, it all starts with solvency. Get this wrong, and you could find yourself in serious trouble.

The Options for a Solvent Company

If your business is financially healthy, closing down is a much cleaner process. You generally have two choices.

1. Voluntary Strike-Off (DS01 Application)

This is by far the most common way to close a small, solvent company. It’s an administrative process, not a formal liquidation, which makes it cheap and relatively simple. You just need to complete a Form DS01 and send it off to Companies House.

This path is perfect for companies that have:

- Already stopped trading and have no assets left.

- Paid off every single creditor, including HMRC.

- Less than £25,000 in assets to distribute among the shareholders.

A Voluntary Strike-Off is about dissolving a clean, debt-free company. It's not a sneaky way to dodge your liabilities. Attempting to dissolve a company to avoid paying creditors is illegal and can bring severe penalties down on you personally as a director.

2. Members’ Voluntary Liquidation (MVL)

An MVL is a more formal affair, handled by a licensed insolvency practitioner. It costs more and takes longer than a strike-off, so why bother? The answer is tax. It can be incredibly tax-efficient if your company has significant assets or retained profits.

When you go through an MVL, the funds distributed to shareholders are treated as capital gains, not income. This opens the door to Business Asset Disposal Relief (previously Entrepreneurs' Relief), which can slash your tax bill to a flat 10%. This is a huge saving compared to the higher rates of dividend tax.

This tax benefit is precisely why an MVL becomes the go-to option once the assets you're distributing top the £25,000 mark. For a deeper dive, you can learn more about the process to voluntarily close a limited company and how the tax side works.

The Route for an Insolvent Company

When your company’s debts are greater than its assets, the situation becomes much more serious. Your options are limited, and the law is very clear: you must act to protect your creditors.

Creditors’ Voluntary Liquidation (CVL)

A CVL is the standard, director-led process for winding up an insolvent business. You and your fellow directors make the difficult decision to put the company into liquidation and appoint an insolvency practitioner to take over.

From that point on, the practitioner’s job is to sell off the company's assets and distribute the proceeds to creditors according to a strict legal hierarchy. By choosing to initiate a CVL, you are demonstrating that you’re a responsible director facing up to a tough situation.

This is far, far better than burying your head in the sand. Ignoring insolvency can lead to accusations of wrongful trading or, even worse, a Compulsory Liquidation. That’s where a frustrated creditor, usually HMRC, petitions the court to force your company to shut down. It's a hostile process where you lose all control, and it almost always triggers an investigation into your conduct as a director.

Comparing Company Closure Options at a Glance

Choosing the right path can feel overwhelming, so we've put together a simple table to help you see the key differences at a glance.

| Method | Company Status | Primary Process | Typical Cost | Key Benefit |

|---|---|---|---|---|

| Voluntary Strike-Off (DS01) | Solvent | Administrative dissolution via Companies House. | Low (£) | Simple, fast, and inexpensive for straightforward closures. |

| Members' Voluntary (MVL) | Solvent | Formal liquidation managed by an Insolvency Practitioner. | Medium (££) | Highly tax-efficient for distributing assets over £25,000. |

| Creditors' Voluntary (CVL) | Insolvent | Formal liquidation to protect creditors' interests. | High (£££) | Fulfills director duties and avoids compulsory court action. |

This table highlights the core trade-offs between cost, complexity, and legal standing. Your company's financial health is the ultimate deciding factor, but understanding these differences is crucial for making an informed decision.

Your Practical Checklist for a Smooth Company Closure

Once you’ve settled on the right way to close your company—be it a strike-off or liquidation—the practical steps begin. A successful closure isn't just about filing a single form. It’s about methodically dismantling the business you built, piece by piece, to make sure nothing is missed.

Think of it as decommissioning a ship. Before you can let it go, you have to shut down every system safely, make sure every crew member is accounted for, and offload all the cargo. If you rush this part, you'll almost certainly run into objections from creditors or HMRC, which can stop the whole process in its tracks.

Winding Down All Trading

First things first: you have to stop trading cleanly. That means no new sales, no more orders, and a clear end date for all commercial operations. You need to draw a firm line in the sand.

To get this right, you’ll want to:

- Fulfil every last customer order. Leaving customers hanging is a surefire way to generate complaints that will only complicate the closure.

- Chase down all unpaid invoices. Any money owed to the company is a company asset. It’s vital to collect everything you can now, because it becomes incredibly difficult later.

- Tell your suppliers and cancel your contracts. Give them formal notice that you won't be placing any more orders and get all your final accounts settled.

Looking After Your Employees

If you have staff, managing their departure properly is both a legal and an ethical duty. UK employment law is very specific about redundancy procedures, and getting it wrong can easily lead to costly employment tribunals.

You are legally required to calculate and pay everything your team is entitled to. This will include their final salary, any holiday pay they've accrued but not used, and statutory redundancy pay for those who qualify. You'll also need to issue a P45 to every single employee and submit your final payroll reports to HMRC—we'll dive deeper into that later.

A common pitfall for directors is forgetting their employer duties amidst the chaos of closing down. Remember, employment law still applies right up to the end. Clear communication and strictly following redundancy rules are non-negotiable for a fair and legal process.

Dealing with Company Assets

Before a company can be struck off, it has to be empty of assets. This means everything the business owns—from office chairs and laptops to leftover stock and property—has to be sold or formally transferred out of the company's name.

The crucial point here is to sell everything at a fair market value. Selling a company van to yourself for £1 will raise red flags. It could be seen as an attempt to devalue assets, which can cause serious headaches later on, particularly if the company is found to have been insolvent. All the money raised from selling assets must go into the company bank account to clear any outstanding debts.

The official guidance on the GOV.UK website is very clear on this. For instance, you can't apply for a strike-off if the company has traded in the last three months, which really drives home how important it is to cease all activities first.

Notifying All Interested Parties

The final preparatory step is to make a list of every single person and organisation that has a stake in your business and tell them you plan to close. This is a vital move to head off any future claims or objections.

Your notification list should cover:

- Banks and Lenders: You’ll need to close the business bank account, but only after every last transaction has fully cleared.

- HMRC: It's essential to inform them you've stopped trading and intend to shut the company down.

- Insurers: Cancel all business insurance policies, like public liability or professional indemnity.

- Utility Providers: Get final meter readings and settle up for your gas, electricity, water, and internet.

- Landlords: If you rent your premises, you must follow the terms of your lease to end the tenancy correctly.

By working through this checklist methodically, you’ll build a solid foundation for the final filings with HMRC and Companies House. It’s the best way to ensure your journey to close your limited company is as straightforward as it can be.

Finalising Your Obligations with HMRC and Companies House

Getting things squared away with HMRC and Companies House is without a doubt the most critical part of closing your company. Any misstep here can bring the whole process to a grinding halt, or worse, leave directors personally liable. Think of it as the final, detailed inspection before you decommission the business for good—every single box has to be ticked.

This is where all your earlier preparation pays off. You’ve already ceased trading, sorted out the assets, and let everyone know what's happening. Now it’s time to settle your official accounts once and for all.

Submitting Your Final Company Accounts

Just because you're closing up shop doesn't mean you can skip the paperwork. You still need to prepare and file a final set of statutory accounts with Companies House. These accounts will run from the end of your last financial year right up to the date your company officially stopped trading.

It’s absolutely crucial that these accounts are clearly marked as 'final'. This simple act signals to both Companies House and HMRC that this is the last report they’ll ever get from you. Forgetting this can trigger automated penalty notices for non-filing down the line, creating a headache you really don't need.

Settling Up with Corporation Tax

Your final accounts go hand-in-hand with your final Company Tax Return (form CT600) for HMRC. This is where you’ll calculate any Corporation Tax owed on profits from your final trading period. Naturally, any outstanding tax must be paid in full before you can move on.

Once that's filed and paid, you need to tell HMRC to formally close down your Corporation Tax record. This isn't automatic; you have to specifically ask them to do it, confirming the company has ceased trading and won't have any future liability.

Deregistering for VAT and PAYE

The other tax schemes need to be shut down properly too. It’s on you to take action for each one.

- VAT Deregistration: You must cancel your VAT registration within 30 days of your final trading date. A final VAT return will then be required, covering the period right up to your cancellation date. One thing to watch out for: you might need to account for VAT on any assets you’re taking for personal use.

- Closing Your PAYE Scheme: As soon as you pay your employees for the last time, you need to tell HMRC you're no longer an employer. This is done by sending one last payroll submission—either a Full Payment Submission (FPS) or an Employer Payment Summary (EPS)—and making sure the 'cessation date' field is completed.

A classic mistake we see is directors assuming one part of HMRC talks to another. They often don't. Closing your Corporation Tax record does nothing to close your PAYE or VAT schemes. You have to tackle each deregistration individually to ensure a clean break.

Managing the Final Payroll Run

Handling that last payroll run correctly is non-negotiable—it's about legal compliance and treating your team with respect. Your final submission to HMRC has to include issuing a P45 to every single employee on their last day. They'll need this vital document for their next job or to claim benefits.

Failing to issue P45s or messing up the final payroll reports will cause serious hassle for your former staff and almost certainly lead to penalties from HMRC.

The Application to Strike Off: Form DS01

For directors going down the voluntary strike-off route, Form DS01 is the key piece of paper. This is your formal application to have the company struck off the Companies House register. Filing it is a huge step, and it means you're confirming that all the pre-closure tasks are complete.

But before you post it, the law requires you to send a copy of the application to all 'notifiable parties' within seven days. This list includes:

- All shareholders (members)

- All directors (even those who didn't sign the form)

- Any creditors, from HMRC to your bank

- Employees and the managers of their pension funds

This gives anyone with a vested interest in the company a formal opportunity to object. It's a common, clean, and cost-effective way for solvent companies to close, a world away from the thousands of insolvencies we've seen in recent years. If you're interested in the broader trends, you can find more data on UK company dissolutions and see how these figures stack up.

The Crown and Your Company Assets

Now for a serious warning that every director needs to hear. You must distribute every last company asset before you submit Form DS01. Any bank accounts, property, or equipment still legally owned by the company when it's dissolved becomes 'bona vacantia'—a Latin term for 'vacant goods'.

In plain English, these assets automatically belong to the Crown. Getting them back is a nightmarishly expensive, slow, and complex legal process. Make absolutely certain the company bank account is empty and closed, and every asset has been sold or transferred before that final application goes in. A simple oversight here is an incredibly costly mistake.

When Insolvency Hits: Understanding Your Liquidation Options

When your company can no longer pay its debts, everything changes. It's a tough spot to be in, and your legal duties as a director pivot dramatically. Your primary responsibility is no longer to the shareholders; it's now to your creditors.

This is the reality of insolvency. Burying your head in the sand is not just a bad idea—it can lead to serious personal consequences.

At this point, a simple company strike-off is off the table. The only responsible path forward is a formal liquidation process. You generally have two choices: one where you stay in control and manage the process, and another where control is ripped away from you by the courts.

Taking Control with a Creditors' Voluntary Liquidation (CVL)

Most directors who realise their company is insolvent and can’t carry on will opt for a Creditors' Voluntary Liquidation, or CVL. It's a formal, structured process where you and the shareholders agree to wind up the company and bring in a licensed insolvency practitioner to handle things.

Think of it as taking decisive, responsible action in a worst-case scenario.

The process usually kicks off with a board meeting to officially cease trading and start the winding-up process. From there, you'll appoint an insolvency practitioner to guide you through the next steps, which include formal meetings with shareholders and creditors to place the company into liquidation.

Once appointed, the insolvency practitioner takes over completely. Their job is to sell off the company's assets—stock, equipment, property—to raise as much cash as possible. This can involve everything from selling intellectual property to finding a buyer for physical goods. A detailed business guide to used office furniture liquidation can be surprisingly helpful in making sure you get the best value. The money raised is then paid out to creditors in a strict, legally defined order.

By choosing a CVL, you're doing the right thing. It's an orderly shutdown that shows you're fulfilling your legal duties as a director, and it significantly reduces the risk of being accused of wrongful trading.

This isn't a niche route; it's the standard. In a recent year in England and Wales, there were 23,938 company insolvencies. A huge 18,525 of those were CVLs, which shows just how common this procedure is.

The Dangers of Compulsory Liquidation

Compulsory liquidation is the polar opposite. It’s a forced closure, usually started by a creditor who has run out of patience. They petition the court to wind up your company so they can get back what they're owed. HMRC is a frequent petitioner in these cases.

This is a far more hostile and stressful route. Directors are stripped of all control.

If the court agrees and issues a winding-up order, an Official Receiver is appointed. They don't just liquidate the assets; they also launch a full-scale investigation into the directors' conduct in the lead-up to the company's collapse.

They'll dig through your records, looking for any signs of misconduct, such as:

- Wrongful trading: Did you keep trading and racking up more debt when you knew the company was going under?

- Preference payments: Did you pay back one specific creditor (like a director's loan) while ignoring others?

- Misfeasance: Were company funds or assets used improperly?

If they find evidence of misconduct, the fallout can be severe. We’re talking about director disqualification for up to 15 years or even being made personally liable for the company's debts.

It's crucial to understand what's at stake. We break this down further in our guide explaining the differences between liquidation and insolvency. A proactive CVL almost always leads to a better, more controlled, and more responsible end to a difficult business chapter.

Common Questions About Closing a Company

Winding up a company isn't something you do every day, so it's natural to have questions. Over the years, we've helped countless directors navigate these final steps, and a few key queries always come up. Getting clear answers from the start can make the whole process feel much more manageable.

How Long Does It Take to Close a Limited Company?

This is probably the most common question we hear, and the honest answer is: it depends entirely on which route you take. There’s no single timeline.

For a straightforward voluntary strike-off (the DS01 form route), you're generally looking at three to six months. This is the quickest option, but that timeline relies on nobody lodging an objection when the proposal is advertised in The Gazette.

A Members' Voluntary Liquidation (MVL) is a more formal affair for solvent companies. Because it involves a licensed insolvency practitioner to handle the assets and distributions properly, it's a longer process. You should plan for it to take anywhere from six to twelve months to be fully wrapped up.

If the company is insolvent, a Creditors' Voluntary Liquidation (CVL) takes the longest, often a year or more. The insolvency practitioner has a complex job to do, selling off assets and settling claims with everyone the company owes money to, which just takes time.

What Happens If I Just Abandon My Company?

I cannot stress this enough: simply walking away from your limited company and hoping it disappears is a terrible idea. It’s a high-risk gamble that can go very wrong.

Yes, eventually Companies House will probably strike the company off for failing to file accounts or a confirmation statement. But this is far from a clean break.

Abandoning a company doesn't erase your responsibilities as a director. It can lead to disqualification, personal fines, and even make you personally liable for company debts, particularly if you've taken assets out of the business improperly.

Creditors, especially HMRC, can easily object to the strike-off, which stops the process dead. This often triggers an investigation into your actions as a director. A formal, by-the-book closure is always the right way to protect yourself.

Can I Close a Company if It Has Debts?

Absolutely, but the path you take depends entirely on whether the company can afford to pay them off.

If your company is solvent (it has more assets than liabilities), the process is simple. You just need to pay off all your creditors first. Once the slate is clean, you can proceed with a voluntary strike-off or an MVL.

However, if the company is insolvent and can't pay its debts, you legally cannot use the strike-off process. Your duties as a director fundamentally shift to prioritising your creditors' interests. In this scenario, the law requires you to place the company into a Creditors' Voluntary Liquidation (CVL). Trying to strike off an insolvent company to dodge its debts is illegal and has serious repercussions.

Navigating the final stages of a limited company requires careful planning and a clear understanding of your obligations. Stewart Accounting Services can provide the expert guidance you need to ensure the process is handled correctly and without stress. Find out how we can help at https://stewartaccounting.co.uk.