Let's be honest, the thought of doing your Self Assessment can bring on a cold sweat. But it really doesn't need to be that annual nightmare. The secret isn't being a tax whiz; it's about breaking the whole thing down into smaller, more manageable steps. This guide will be your roadmap to getting it done and, more importantly, getting it done right.

Your Guide to a Stress-Free Tax Return

While submitting your tax return is a legal duty for millions of people across the UK, many of us put it off, dreading the complexity. The good news? A bit of structure transforms this chore into a straightforward financial health check. We'll walk you through everything, from digging out the right documents to hitting that final "submit" button, so you feel in control the whole way.

The real work starts long before the January deadline is breathing down your neck. It’s about knowing your responsibilities, getting your financial records in order, and understanding exactly what information HMRC is looking for. This groundwork is what separates a last-minute panic from a smooth, stress-free filing.

Key Self Assessment Deadlines You Cannot Miss

One of the biggest anxieties is the fear of missing a critical date. Get it wrong, and you're looking at automatic penalties. The simplest way to avoid fines is to get these dates in your calendar right now. A little planning is your best defence.

The tax year itself runs from 6th April to 5th April, but the Self Assessment calendar is dotted with several other important milestones you need to be aware of, not just the final filing date.

To help you stay on top of things, here’s a quick summary of the most important dates in the Self Assessment calendar.

Key Self Assessment Deadlines You Cannot Miss

| Deadline | Task | Notes for Filing Online |

|---|---|---|

| 5th October | Register for Self Assessment | An absolute must if you're filing for the first time or need to re-register. |

| 31st October | Paper tax return deadline | This is for postal submissions only, which are much less common these days. |

| 30th December | Pay tax through your tax code | An option if you're also an employee and meet specific criteria. |

| 31st January | Online tax return deadline | The final day to submit your online return for the previous tax year. |

| 31st January | Pay the tax you owe | Crucially, your payment must have cleared in HMRC's account by this date. |

Getting these dates locked in your diary is the first step to a hassle-free tax season.

Why Preparation is Paramount

Knowing how to complete self assessment is less about being a tax expert and more about being organised. A little bit of prep work can turn what feels like a monumental task into a simple box-ticking exercise. Once you have all your figures to hand, HMRC’s online forms suddenly seem much less intimidating.

Think of it this way: a well-organised system for your finances doesn't just make your tax return easier. It gives you a crystal-clear view of your business's financial health all year round. It's a proactive habit that pays off long after tax season is over.

By taking the time to understand what’s needed and gathering your information early, you give yourself the breathing room to file accurately and without pressure. For more practical advice on building good habits, check out our tips for stress-free self-assessment tax filing.

Next, we'll dive into exactly what documents you need to start pulling together.

Getting Your Paperwork in Order: A Pre-Filing Checklist

Let's be honest, the secret to a stress-free Self Assessment isn't some magic formula—it's preparation. Getting everything organised before you even think about logging into the HMRC website transforms the entire process from a major headache into a straightforward task. Think of it as laying out all your ingredients before you start cooking; it just makes everything that follows so much easier.

First things first, you'll need your essential identifiers. You can't even get started without them. Make sure you have your Unique Taxpayer Reference (UTR) number and your National Insurance number handy. Your UTR is the 10-digit code HMRC gave you when you registered, and it's the key that unlocks your entire tax account.

Pulling Together Your Income Records

With your personal details ready, the next job is to create a complete picture of everything you earned during the tax year, which runs from 6th April to 5th April. It's not just about your main business turnover; HMRC wants to know about every single income stream.

Start gathering the following documents and figures:

- Self-Employment Income: Pull together all your sales invoices for the year. If you're VAT registered, you'll need the totals before VAT was added.

- Employment Income: If you also had a PAYE job, you'll need your P60. This is the summary your employer gives you after the tax year ends. If you left a job during the year, you'll need the P45 they gave you.

- Rental Income: For any landlords out there, this means a full log of all the rent you received from your properties.

- Dividends and Savings Interest: Dig out the statements from any company shares you hold and the interest summaries from your bank or building society accounts. Every little bit counts and needs to be declared.

- Other Income: Don't forget the odds and ends. This could be anything from a few freelance "side hustle" gigs to commissions or even certain taxable state benefits.

Getting your income figures spot on is the bedrock of a solid tax return. Missing something is one of the quickest ways to trigger an enquiry from HMRC, so it really does pay to be meticulous here.

Tracking Down Your Allowable Expenses

Telling HMRC what you've earned is only one side of the coin. The other crucial part is claiming for all your allowable expenses. These are the costs you paid out purely for business purposes, and they directly reduce your profit, which in turn lowers the amount of tax you have to pay.

For a typical sole trader, this could include a whole host of things:

- Office Costs: Stationery, phone bills, postage, and software subscriptions.

- Travel Costs: Fuel for business trips, train tickets, or a portion of your vehicle insurance.

- Stock and Materials: The cost of any raw materials or goods you bought to sell.

- Marketing and Professional Fees: Advertising costs or the fees you paid to your accountant or a solicitor for business advice.

Trying to keep all this organised can be tough. To make life easier, especially when it comes to keeping track of endless receipts, you might want to look at dedicated receipt management tools. These apps can help you digitise and categorise your spending on the go, making sure you never misplace a claimable expense again.

The Power of Going Digital

That old shoebox overflowing with crumpled receipts? It's a classic recipe for stress and missed claims. Switching to a digital record-keeping system is a game-changer. It not only makes filing your Self Assessment a breeze but also gives you a much clearer view of your business's financial health all year round.

Using accounting software or even just a well-organised spreadsheet means you can log income and expenses as they happen. When tax time rolls around, the hard work is already done. You just need to run a report for the tax year, and your figures are ready. For a detailed list of exactly what you need to look for, our comprehensive Self Assessment checklist breaks it all down for you. This forward-thinking approach will save you hours of panicked searching later on and ensures you have a robust, compliant record of your finances.

Navigating the Online Self Assessment Form Section by Section

With your financial records all lined up, it’s time to get stuck into the online form. The HMRC portal does a decent job of guiding you through, but knowing what’s coming up in each section will make the whole process much quicker and less stressful. Think of it as a logical journey that builds a complete picture of your finances for the tax year.

Getting Started: Tailor Your Return

The first few pages are straightforward. You’ll be asked to confirm your personal details are correct—name, address, and, most importantly, your Unique Taxpayer Reference (UTR).

Next comes a crucial step: "tailor your return." This is where you tell HMRC which sections you actually need to fill in. You’ll tick boxes based on your circumstances, like being self-employed, earning rental income, or making a capital gain.

Getting this right from the start is a huge time-saver. It stops you from having to click through pages that have nothing to do with you. If you’re a freelance graphic designer in Scotland, for example, you won’t need to see the sections for company directors or foreign income.

Declaring Your Self-Employment Income

For any sole trader, this is the main event. It's where you'll enter your total turnover—that’s the grand total of all your sales invoices for the tax year. You’ll also need to add any other business income, maybe from selling an old work laptop or another business asset.

Then comes the most important part: declaring your allowable expenses. This is your chance to shrink your taxable profit, so don't rush it. You'll enter the total amounts for different spending categories, such as:

- Office, property, and equipment: Think stationery, rent for your workspace, and software subscriptions.

- Travel costs: This covers fuel for business trips, train tickets, and vehicle insurance.

- Costs of goods: Anything you bought to resell or use directly in your business.

- Legal and professional costs: Crucially, this includes fees paid to your accountant.

This is where meticulous record-keeping throughout the year really pays off. Getting your expenses right is fundamental to making sure you don't hand over a penny more in tax than you need to.

Reporting Property and Other Income Sources

If you’re a landlord, the property section is where you’ll lay out the finances of your rental business. You’ll need to put in the total rental income you received from all your properties. Just like with self-employment, you then get to deduct your allowable expenses. This could be anything from letting agent fees and landlord insurance to maintenance costs and a portion of your mortgage interest.

Other income streams get their own dedicated sections. If you've earned interest from savings or received dividends from shares, you'll need those statements you gathered earlier. It’s usually a simple case of transferring the figures from your documents into the right boxes on the form.

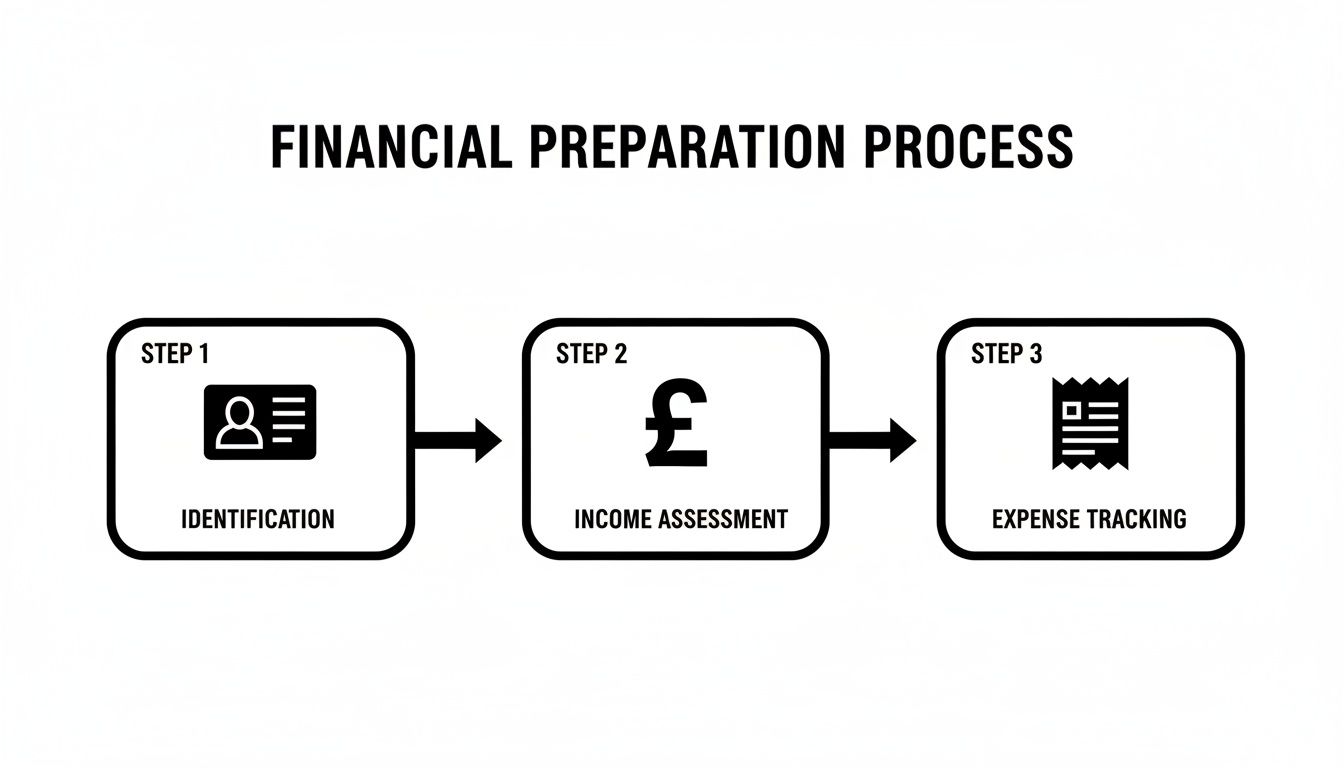

The whole process boils down to a few core steps: confirm who you are, summarise what you’ve earned, and then tally up what you’ve spent.

This visual just reinforces that a successful, pain-free filing is built on these three pillars, which mirror the main sections of the online form perfectly.

And more people are choosing the digital route. Take a sole trader in Central Scotland juggling freelance work and a couple of rental properties. HMRC data shows that 339,490 people paid their tax through the HMRC app between April and January—a 65% increase on the previous year. It’s clear that filing online is becoming the go-to method for a reason. You can read more about HMRC's findings on app-based payments.

Handling Capital Gains and the Final Calculation

The Capital Gains section can feel like the trickiest part of the return. You’ll need to fill this in if you’ve sold a significant asset—like a second property, shares, or even valuable antiques—and made a profit over the annual tax-free allowance. You’ll be asked for the details: what you sold, when you bought it, when you sold it, how much you got for it, and what it originally cost you.

It's absolutely crucial to report Capital Gains accurately. HMRC gets data from all sorts of places, so they can easily spot if something doesn't add up. If you're even slightly unsure about what counts or how to work out the gain, this is one area where getting professional advice can save you from a very costly mistake down the line.

Once every bit of income and every gain has been entered, the system works its magic. It will automatically calculate your total tax and National Insurance bill based on the figures you’ve provided.

Before you submit, you get a full summary to review. This is your last chance to check everything over. Take your time, read through each figure, and make sure it all looks correct before you hit that final button. With digital tax on the horizon, getting comfortable with this process is essential, and it’s worth understanding what’s required from April 2026 for MTD for Income Tax.

Common Filing Mistakes and How to Avoid Penalties

Getting your tax return filed on time is one thing, but getting it right is another challenge entirely. It’s far easier to make a mistake than you might think, and with HMRC’s systems getting smarter every year, even small errors can lead to a lot of unwanted stress and penalties.

The best way to sidestep these issues is to understand where people commonly go wrong. Year after year, we see the same simple mistakes trip people up, turning what should be a straightforward task into a costly headache.

The Most Frequent Filing Errors

Some mistakes crop up more often than others. Simple typos are one thing, but fundamental errors in how you report your income or expenses can have much bigger consequences. Being aware of these common pitfalls is your first line of defence.

- Forgetting a source of income: This is surprisingly common. Maybe you did a small freelance job on the side, sold some shares, or earned a bit of interest from a savings account. Every single stream of income, no matter how minor it seems, has to be on that form.

- Miscategorising expenses: Claiming for a business lunch when it was really a personal meal, or trying to claim the full cost of your phone bill when you also use it for personal calls. Remember the golden rule: expenses must be "wholly and exclusively" for business purposes.

- Simple calculation errors: Even with online calculators, mistakes can creep in. Transposing a number or putting a decimal point in the wrong place can completely change your tax liability. It pays to double-check every single figure before you submit.

Don’t assume a small slip-up will go unnoticed. HMRC's tech is watching closer than ever, and accurate Self Assessment is non-negotiable. Their compliance efforts brought in £48 billion in a recent tax year—a 15% jump—fuelled by advanced data-matching. They now cross-reference your return with everything from bank interest and PAYE data to crypto exchanges and letting agent reports.

Any inconsistency can flag you for an audit. With 52% of individuals recently reporting poor experiences with HMRC, often stemming from filing errors, getting it right the first time is crucial. You can read more about HMRC's compliance strategies to see just how seriously they take this.

Understanding the Penalty System

HMRC's penalty regime isn't just about punishment; it's designed to encourage everyone to file on time and accurately. The penalties can be steep, so it’s vital to understand what you’re up against if things go wrong.

The system doesn’t just penalise late filers—it also comes down hard on carelessness. Penalties for inaccuracies are calculated as a percentage of the extra tax you owe, and the amount depends on why you made the error. If HMRC believes you took reasonable care but still made an honest mistake, you might not be penalised. But if the error is deemed careless, you could be looking at a penalty of up to 30% of the tax due.

The message from HMRC is clear: getting it wrong can be expensive. Penalties for deliberate errors can soar to 70% or even 100% of the unpaid tax, so pleading ignorance is not a viable strategy.

If you spot an error after you've already filed, don't panic. The best thing you can do is amend your return as soon as you realise. You can usually do this online within 12 months of the original filing deadline. Acting quickly and proactively shows HMRC you're trying to be compliant, which can make a huge difference in reducing or even eliminating potential penalties.

Tips for an Error-Free Return

Avoiding these common issues really comes down to good habits and careful checking. Knowing how to complete self assessment accurately is a skill that saves you both money and sleepless nights.

- Start Early: Rushing at the last minute is a recipe for disaster. Give yourself plenty of time to gather all your documents and review your figures without the pressure of the 31st January deadline breathing down your neck.

- Keep Meticulous Records: Don't wait until January to sort through a year's worth of crumpled receipts. Use accounting software or even just a simple spreadsheet to log your income and expenses as they happen. It makes the final tally so much more reliable.

- Review, Review, Review: Before you hit that final "submit" button, print out the calculation and summary. Go through it line by line, comparing it with your original records to make sure everything matches up. It often helps to step away for a bit and come back with fresh eyes.

- When in Doubt, Ask: If you’re unsure about whether you can claim a certain expense or how to declare a particular type of income, don't just guess. The GOV.UK website has a lot of guidance, but for anything complex, getting professional advice is always the safest bet. Think of it as an investment in your peace of mind.

When to Partner with a Professional Accountant

While HMRC’s online system is perfectly usable, there often comes a point where doing your own tax return stops being the most sensible option. Knowing how to complete self assessment is one skill; knowing when it’s time to call in an expert is another entirely.

This isn’t about throwing in the towel. Far from it. Handing your tax affairs over to a professional is a smart business move that can save you a surprising amount of time, money, and stress down the line.

The tipping point is different for everyone. For some, it’s when their finances get more complicated than a single income stream. For others, it’s the simple realisation that the hours spent battling with tax rules could be better invested in growing their business. Spotting these signs early can save you from making expensive mistakes.

Your Financial World is Expanding

As your business or personal finances grow, your tax return inevitably gets more complicated. The clearest sign you might need an accountant is when your income starts coming from several different places.

What starts as a straightforward sole trader return can quickly become a tangled mess. Ask yourself if any of these sound familiar:

- Multiple Income Sources: Are you juggling freelance work with a part-time PAYE job? Maybe you’ve started renting out a property? An accountant ensures every income stream is declared properly and you’re not missing out on any allowances.

- Company Director Responsibilities: Running a limited company means your personal and business taxes are closely linked. You’ll be dealing with a director’s salary, dividends, and maybe even director’s loans, all of which have their own specific rules.

- Navigating Capital Gains Tax: If you’ve sold a major asset this tax year—like a second property, shares, or cryptocurrency—the Capital Gains Tax calculations can be a minefield. An expert can make sure you get it right and avoid a nasty surprise from HMRC.

Time is Your Most Valuable Asset

For many entrepreneurs and busy professionals, it’s not the complexity that’s the issue—it’s the clock. The hours you spend digging out paperwork, poring over the tax return, and second-guessing every entry are hours you’re not spending on what you do best.

Think about what your time is really worth. If a few hours spent on your business generates more income than an accountant’s fee, the decision practically makes itself.

An accountant does so much more than just fill in boxes. They offer strategic tax planning, spot expenses you might never have thought of, and can act as your representative with HMRC. It's a direct investment in your own efficiency and peace of mind.

Ultimately, this is about offloading the administrative headache of tax. When you bring a professional on board, you’re not just paying for their expertise; you’re buying back your own time and mental space.

Seeking Proactive Financial Strategy

A great accountant doesn't just look backwards at the tax year that’s gone. They partner with you to look ahead, helping you structure your finances to be as tax-efficient as possible for the years to come.

This could mean advising on the best way to draw an income from your limited company or planning the tax implications of a major asset purchase. They can help you see the financial consequences of big decisions before you make them, turning your tax return from a chore into a powerful planning tool.

Before an accountant can work on your behalf, you'll need to formally grant them authority to deal with HMRC for you. This is a standard procedure, conceptually similar to how professionals in other countries get authorised, for which you might see something like an IRS Form 2848 Instructions Guide. It's the official step that lets your accountant handle all the submissions and communications, ensuring everything is managed correctly from the start.

Your Self Assessment Questions Answered

Even with a detailed guide in front of you, it’s completely normal for a few nagging questions to pop up while you’re getting your tax return sorted. Here, I’ll tackle some of the most common queries we get from clients, giving you some straight answers to get you over those final hurdles.

What Happens If I Miss the Self Assessment Deadline?

Let's be blunt: missing the 31st January online filing deadline is a mistake you want to avoid. HMRC hits you with an immediate £100 penalty the very next day. This applies even if you don't owe any tax, or if you’ve already paid what you think you owe.

And it doesn't stop there. The penalties are designed to escalate the longer the delay continues.

After three months, you’re looking at daily penalties of £10 for up to 90 days, which can quickly rack up another £900. If it gets even later, the charges climb higher:

- Six months late: You'll get another penalty of £300 or 5% of the tax due (whichever is greater).

- 12 months late: A further penalty of £300 or 5% of the tax due is added.

It's also crucial to remember that there are separate penalties for paying your tax bill late. If you know you're going to struggle to meet the deadline, the best thing you can do is get in touch with HMRC or speak to an accountant right away.

Can I Claim Expenses for Working from Home?

Absolutely. If you're self-employed, you can definitely claim for the costs of running your business from home. HMRC gives you two ways to do this, so you can pick the one that fits your circumstances.

The first is using HMRC's simplified expenses. This is just a flat monthly rate based on how many hours you work from home. It's a no-fuss calculation that saves you from digging through piles of household bills.

The other route is to calculate the actual business portion of your household running costs. This is more involved, as you need to work out what percentage of your home you use for business and for how long. You can then claim that proportion of costs like:

- Heating and electricity

- Council Tax

- Mortgage interest or rent

- Internet and phone line use

If you go down this second, more detailed route, meticulous record-keeping isn't just a good idea—it's essential.

Choosing the right method can be tricky. Simplified expenses are quick, but you might be leaving money on the table. Calculating actual costs can lead to a bigger claim but takes a lot more effort. An accountant can run the numbers for you to figure out which approach will actually save you more money.

Do I Need to Register If I Only Have a Little Extra Income?

Whether you need to register for Self Assessment often boils down to where the extra income came from and how much it was. For money earned from self-employment or renting out a property, HMRC created allowances to make life simpler for those with small amounts of income.

The key figure to remember is £1,000. If your gross income from either of these sources is more than £1,000 in a tax year, you must register. This is known as the trading allowance for self-employment or the property allowance for rental income.

If your income is under that £1,000 threshold, you don't need to declare it or file a tax return for it. Be careful, though, as different rules can apply to other types of income, or if you're in a position like a company director. When in doubt, always check the latest guidance on the GOV.UK website or get some professional advice.

How Do I Pay My Self Assessment Tax Bill?

HMRC has made it pretty easy to pay your tax bill, offering a few different options. By far the most popular and quickest methods involve online banking.

You can make a direct bank transfer via Faster Payments, BACS, or CHAPS straight into HMRC’s account. Another common choice is to pay online through your Government Gateway account using a debit card or a corporate credit card. You can even set up a Direct Debit to have the funds taken automatically on a date you choose.

Recently, paying through the official HMRC app has become a really popular and simple option for many. Just remember, you can no longer pay at the Post Office, and HMRC won't accept personal credit cards. Whatever method you choose, always leave a few business days for the payment to clear to make sure you don't get hit with any late payment penalties.

Getting through a Self Assessment can feel like a real slog, but you don't have to face it alone. The team at Stewart Accounting Services is here to offer expert, friendly advice, ensuring your tax return is spot-on and you're not paying a penny more than you need to. Get in touch with us today to see how we can give you more time, more money, and a clearer mind.