Filing your company accounts is a two-part job. You’ve got the statutory accounts for Companies House and the Company Tax Return (the CT600) for HMRC. It all boils down to preparing your financial records properly and hitting those strict legal deadlines. Getting this right from the get-go is absolutely essential for staying compliant.

Understanding Your Filing Obligations

As a director of a limited company here in the UK, the law says you're personally responsible for making sure the company's accounts are accurate and filed on time. This isn't just a friendly suggestion; it's a fundamental part of your duties. If you drop the ball here, you’re looking at hefty penalties and a serious dent in your company's reputation.

The whole process is split between two different government bodies, and each one has its own rules and deadlines. This is a common tripwire for new directors, so let’s break down exactly what goes where.

The Two Pillars of Company Filing

Here’s how your annual filing duties are split:

- Companies House: This is where you file your statutory accounts. Think of this as the public record of your company's financial performance and position over the last year. It’s all about transparency.

- HMRC (His Majesty's Revenue and Customs): This is where you send your Company Tax Return, which is officially called the CT600. HMRC uses this to figure out how much Corporation Tax your company needs to pay.

Even though you’ll use the same set of financial records to prepare both, they are two completely separate submissions with different deadlines. Simply put, Companies House cares about corporate governance, while HMRC is all about collecting tax.

The buck stops with you. As a director, you are legally on the hook for the accuracy and timely filing of both your accounts and your tax return. Pleading ignorance of the rules won’t get you out of trouble.

Navigating Key Deadlines

Missing your filing deadlines is a costly mistake. For a private limited company, the penalties for filing late with Companies House kick in immediately. You're looking at £150 if you're just one day late, and that fee can jump to £1,500 if you're more than six months behind. Public companies face even bigger fines.

Here’s a quick rundown of the deadlines you absolutely cannot miss.

UK Company Accounts Filing Deadlines

This table provides a quick reference for the statutory filing deadlines for a private limited company.

| Filing Requirement | Deadline to File |

|---|---|

| Statutory Accounts to Companies House | 9 months after your company’s financial year ends. |

| Company Tax Return (CT600) to HMRC | 12 months after your accounting period for Corporation Tax ends. |

| Corporation Tax Payment to HMRC | Usually 9 months and 1 day after your accounting period ends. |

Remember, the deadline to pay your Corporation Tax is typically earlier than the deadline to file your tax return. This catches a lot of people out.

It’s also really important to know that the timeline for your very first set of accounts can be different from subsequent years. For a wider view on all the legal duties that go beyond just financial reporting, this ultimate small business compliance checklist is a great resource. Getting these dates locked into your calendar is the first, and most important, step to keeping your company on the right side of the law.

Preparing Your Essential Financial Records

Before you can even think about logging into a government portal, the real work starts with getting your financial records in order. Trying to file accounts without solid preparation is a recipe for disaster. It all hinges on having accurate, organised financial data ready to go.

This means you need a clear paper trail for every single transaction your business has made during its financial year. Without this groundwork, the filing process becomes a nightmare, and you run the real risk of submitting inaccurate information, which can lead to serious compliance headaches down the road.

Your Core Financial Checklist

As a starting point, you’ll need a complete set of records covering the entire accounting period. This isn't just good practice—it's a legal requirement. You must hold on to these records for at least six years from the end of the last company financial year they relate to.

Here’s a practical list of the absolute must-haves:

- All Company Bank Statements: This covers every current account, savings account, and credit card linked to the business.

- Sales Invoices and Income Records: A full log of all money coming into the company, from sales to any interest earned.

- Expense Receipts and Purchase Invoices: Every receipt for things your company has bought, whether it’s stock, office supplies, or software subscriptions.

- Payroll Data: Detailed records of all employee payments, including salaries, PAYE, and National Insurance.

- Asset Register: A list of valuable items the company owns (like computers or machinery), complete with purchase dates and costs.

If your business deals with physical products, solid record-keeping is even more critical. Getting your stock figures right is essential for accurate accounts. This guide on UK Inventory Management for Small Businesses has some great advice for keeping your stock records in check.

Understanding Your Statutory Accounts

Once you’ve gathered all your records, you’ll use them to put together your statutory accounts. These are the formal documents that summarise your company's financial performance and position. They must include two key statements.

First, there's the Balance Sheet. This is a snapshot of your company’s financial health on the last day of its accounting period. It lays out what the company owns (assets) and what it owes (liabilities) and has to be signed off by a director.

Second is the Profit and Loss (P&L) Account. This document shows your company’s sales and running costs over the financial year, ultimately revealing whether you made a profit or a loss.

Your accounts must present a 'true and fair view' of the business's finances. This isn't just a turn of phrase; it's a legal standard that directors are responsible for upholding.

Filing Options for Small Businesses

Thankfully, the system recognises that a small consultancy doesn't have the same reporting burden as a huge corporation. Depending on the size of your company, you might be able to use simplified filing options that can save you a ton of time and effort.

If your company qualifies as a 'micro-entity' or 'small company', you can file what are known as abridged or 'filleted' accounts. This is a huge advantage, as it means you submit far less detailed information to the public record at Companies House. It’s a great way to protect your commercial privacy while still ticking all the legal boxes. You’ll need to check the latest turnover, balance sheet, and employee thresholds on the GOV.UK website to see if you qualify.

Navigating the Companies House Filing Process

Once you've got all your financial records in order, it’s time to actually submit your accounts. This is where all that careful preparation really pays off.

These days, the most common and sensible way to file is through the Companies House online service. It’s a digital portal designed to make a potentially tricky process as painless as possible.

You could still file paper accounts, but I wouldn't recommend it. It's slower, far easier to make a mistake on, and frankly, it's on its way out. The digital route is much safer – you get an instant confirmation that they’ve received your submission, which is great for peace of mind, and it dramatically cuts the risk of rejection over a simple error.

Getting Ready to File Online

Before you can get started, you'll need two crucial bits of information handy:

- Your company registration number (CRN): This is the unique eight-digit number assigned to your company.

- Your Companies House authentication code: Think of this as your company’s digital signature. It's a six-character alphanumeric code that was posted to your registered office address when you first set up the company.

If you can't find your authentication code, don't worry, it happens. You can easily request a new one from the Companies House website. Just be aware they'll post it to your company's registered office, and it can take up to five working days to arrive. It’s a good idea to check you have it well before your deadline to avoid any last-minute panic.

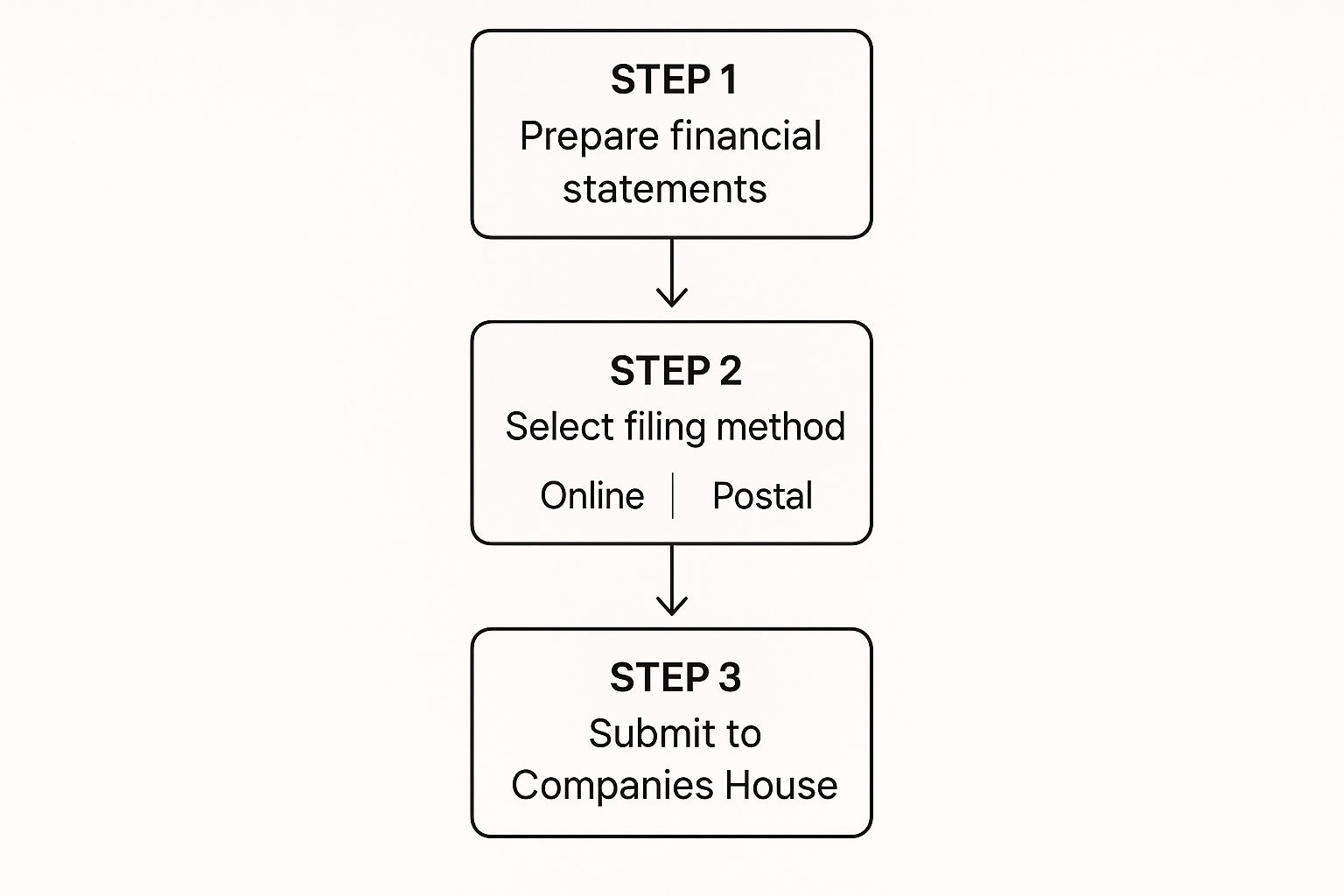

This image gives a great overview of the whole submission workflow, from preparation to filing.

As you can see, choosing how you're going to file is one of the key decisions you'll make right after you've pulled your financial documents together.

A Real-World Example: Filing for a Micro-Entity

Let's imagine a common scenario. Say we have a small e-commerce business called "Crafty Creations Ltd," and they're filing their first set of micro-entity accounts.

The director logs into the Companies House web filing service with the company's authentication code. The system first asks for the accounting period dates. Since Crafty Creations is a brand new business, the director just needs to enter the period from the date of incorporation up to their accounting reference date.

From there, the portal brings up a simplified balance sheet template, with all the necessary fields for a micro-entity already laid out. It’s pretty intuitive.

The director then carefully plugs in the figures for assets (like cash in the bank and any stock they hold) and liabilities (perhaps a small start-up loan). One of the best features of the online service is that it automatically calculates the totals and flags if the balance sheet doesn't balance – a fantastic safeguard against common mistakes.

After a final review of the numbers, the director confirms everything is correct and hits 'Submit'. A confirmation email pops into their inbox just moments later. Job done.

The online service is genuinely user-friendly, especially for simpler filings like those for micro-entities. The system really holds your hand through each section, making it much harder to accidentally miss out on crucial information.

The process for a small or large company is naturally a bit more involved and demands more detailed data entry. However, the basic steps are the same: log in securely, complete the required forms, and submit. Following the clear pathway laid out by the digital system turns what can feel like a daunting legal chore into a perfectly manageable task.

Right, so you’ve filed your statutory accounts with Companies House. That’s a big job ticked off the list, but you’re not quite finished yet. Now it's time to deal with HMRC and your Company Tax Return, otherwise known as the CT600.

These two tasks are two sides of the same coin. The numbers you've so carefully prepared for your statutory accounts are the foundation for working out how much Corporation Tax you owe.

Think of it this way: your statutory accounts tell the complete financial story of your year. The CT600 takes that story and translates it for the taxman. Your profit and loss statement, for instance, is the starting point for calculating your taxable profit.

But—and this is a crucial point—the final profit figure in your accounts is almost never the same as your taxable profit. This is where things get a bit more technical.

From Accounting Profit to Taxable Profit

The journey from your accounts to your final tax return is all about making adjustments. HMRC has its own rulebook for what counts as a legitimate business expense, and it doesn't always match up with standard accounting. Getting this right is one of the biggest opportunities to run your business tax-efficiently and avoid costly errors.

You'll need to go through your expenses and "add back" anything that's considered a "disallowable expense." These are costs you’ve correctly included in your accounts, but HMRC won’t let you deduct them when calculating your taxable profit.

A few classic examples pop up all the time:

- Client Entertainment: That business lunch where you sealed the deal? It's a valid company expense, but you can't deduct it for tax purposes.

- Personal Expenses: Any spending that isn't "wholly and exclusively" for the business has to be added back.

- Depreciation: Your accounts will show depreciation to reflect the falling value of your assets. HMRC ignores this and instead uses its own system: capital allowances.

Capital allowances are HMRC's way of letting you get tax relief on your major assets, like computers or machinery. It’s a completely different calculation from depreciation, and understanding how it works is key to making sure you don't hand over more tax than you need to.

Deadlines A Common Point of Confusion

Here’s one of the biggest tripwires I see new directors fall over: mixing up the deadline for paying the tax with the deadline for filing the return. They are two different dates, and HMRC is notoriously strict about them. Get it wrong, and you're looking at automatic penalties.

Your deadline to pay your Corporation Tax is almost always earlier than your deadline to file the return. For most companies, the payment is due nine months and one day after your accounting period ends.

You actually have a full 12 months from the end of your accounting period to submit the CT600 return itself. This system gives you a bit of breathing room to get the final figures perfect, but HMRC wants its payment much sooner. If you miss that payment deadline, they'll start charging interest straight away, even if you file the return on time.

It's also essential to remember that you can't just pop your return in the post anymore. All submissions to HMRC must be done digitally. You’ll need to use HMRC-recognised software that can prepare and send your CT600 and accounts in a special digital format called iXBRL. This digital-first approach is mandatory and helps cut down on errors for everyone involved.

Preparing for Software-Only Digital Filing

The way we all file our annual accounts is about to change, and it’s probably the biggest shake-up we’ve seen in years. Say goodbye to logging into the old web portal or, for the truly traditional, sending in paper forms. A major shift to mandatory software-only filing is just around the corner, and every company director needs to get ready for it.

This whole move is being driven by the Economic Crime and Corporate Transparency Act. The big idea is to make the information on the public register more trustworthy, secure, and transparent. It's a serious effort to clamp down on economic crime by making sure all the data submitted is traceable and up to scratch.

And just to be clear, this isn't optional. From 1 April 2027, every single company will be legally required to file its accounts using commercial software that links directly to Companies House. That means the current web-based and paper filing options will be gone for good, even for dormant companies. You can get the full rundown on the upcoming changes to UK company law on GOV.UK.

Why the Change is Happening

I know what you might be thinking – just another bit of admin to deal with. But honestly, this move has some real upsides that will help legitimate businesses in the long run.

The key benefits really boil down to this:

- Improved Accuracy: The right software runs instant checks as you go, which dramatically cuts down on the simple mistakes that so often lead to rejections.

- Enhanced Security: Sending your sensitive financial data directly from verified software is a world away from the older, less secure methods.

- Better Data Quality: When everyone submits data in a standardised way, the public register becomes far more useful and reliable for lenders, investors, and potential partners.

It’s all part of a bigger push to modernise the system, bringing the UK in line with how things are done elsewhere and boosting the integrity of our corporate records.

How to Get Your Business Ready

Putting this off until the last minute would be a mistake. The smart move is to get ahead of the game now and start using compatible software well before the 2027 deadline hits. If you're already using a cloud accounting package, you’re probably in a really good spot.

When you’re looking at different tools, make sure it’s Making Tax Digital (MTD) compliant. That’s a pretty solid sign that the provider is already on board with government digital-first thinking and will be ready for this next step.

By adopting the right software early, you're doing more than just ticking a compliance box. You're actually future-proofing your entire financial admin. Think of it as a chance to make your processes much more efficient for the long haul.

For instance, platforms like Xero or QuickBooks are built for exactly this kind of digital submission. They connect your day-to-day bookkeeping directly to your year-end filing duties, transforming what used to be a frantic annual chore into a much smoother, joined-up process. Start looking at your options now to find a solution that works for your business and makes the transition feel effortless.

Answering Your Top Questions About Filing Company Accounts

When you're running a business, getting the accounts right is crucial, but it's completely normal to have a few questions pop up. Let's walk through some of the most common queries we hear from directors to help you feel more confident about the process.

What Happens if I Miss the Filing Deadline?

This is probably the number one concern, and for good reason. The consequences for missing your deadline with Companies House are both automatic and unforgiving.

As soon as the deadline passes, you’re hit with a late filing penalty. For a private limited company, this starts at £150 and can climb all the way to £1,500 if you’re more than six months late. It’s not just about the money, either—a late filing puts a black mark on your company's public record, which can hurt your credit score and business reputation.

Should I File Myself or Hire an Accountant?

This is a classic dilemma for many directors. You are absolutely allowed to prepare and file your own company accounts, and plenty of small business owners manage it perfectly well, especially with the help of modern accounting software. If your business finances are relatively simple, going the DIY route can definitely save you some money.

On the other hand, if things are a bit more complicated or you're feeling out of your depth, bringing in an accountant is a wise move. It's about more than just getting the paperwork done; a good accountant saves you time, prevents expensive mistakes, and can offer tax-planning advice that could save you far more than their fee.

Ultimately, it's a judgement call based on your budget, how complex your business is, and your own confidence levels. For many, an accountant's fee is a small price to pay for the assurance that everything is correct and fully compliant.

What Do the Different Company Sizes Mean?

You’ll often hear terms like 'micro-entity' or 'small company', and it's important to know where you fit, as it determines what you need to file.

Here’s a quick breakdown:

- Dormant Company: This applies if your company had no 'significant' financial transactions in the accounting period. Filing is very straightforward.

- Micro-entity: You fall into this category if you meet at least two of these criteria: turnover of £632,000 or less, a balance sheet total of £316,000 or less, or 10 employees or fewer. You can file the simplest type of accounts.

- Small Company: Your business is 'small' if it meets two of these: turnover of £10.2 million or less, a balance sheet total of £5.1 million or less, or 50 employees or fewer. Your filing requirements are reduced compared to larger companies.

The business landscape is always changing. In the year to March 2024, for instance, company dissolutions increased by 9.6%, while the total register grew to almost 4.87 million businesses. If you're interested in the data, you can read more about these UK business environment fluctuations on GOV.UK.

Feeling overwhelmed by filing deadlines and financial compliance? The team at Stewart Accounting Services provides expert help with year-end accounts, tax returns, and bookkeeping. We'll give you back your time, save you money, and offer complete peace of mind. Contact us today for a free consultation.