Filing your company's tax return boils down to a few key activities: pulling together your financial records, working out your Corporation Tax, filling in the CT600 form, and getting it all over to HMRC before the deadline hits. The real task is converting your annual accounts into a format HMRC understands, making sure you've claimed every relief you're entitled to and are paying the right amount of tax.

Your Practical Roadmap to Filing Company Taxes

Tackling company taxes for the first time can feel a bit daunting, but having a clear roadmap makes all the difference. Knowing how to file your company tax return isn't really about memorising complex tax law; it’s about understanding the core stages of the process. Get that right, and you'll stay compliant and sidestep any nasty penalties from HMRC or Companies House.

The whole thing is a cycle that starts way before you even think about filling in a form. It begins with solid record-keeping throughout your financial year and finishes with a successful submission and payment. Breaking it down into smaller, manageable chunks takes the stress out of it and turns it into just another part of running your business.

The Two Key Submissions You Can't Ignore

At its core, filing your company's return means making two separate submissions. They're related, but they have their own purposes and, crucially, their own deadlines.

You absolutely must file:

- Annual Accounts with Companies House. Think of these as a public snapshot of your company's financial health and performance over the year.

- A Company Tax Return (CT600) with HMRC. This is the document where you detail your taxable profits and calculate your final Corporation Tax bill.

These two go hand-in-hand. The figures you prepare for your annual accounts are the foundation for your tax return calculations. If you're running a different business structure, like an LLC, you might find this step-by-step guide to filing LLC taxes useful for comparison.

A classic trip-up is mixing up the deadline for filing your accounts with the one for paying your tax. Your Corporation Tax payment is usually due nine months and one day after your accounting period ends. The deadline to actually file the tax return, however, is 12 months after. Don't get caught out.

Understanding the Journey Ahead

To make the process less overwhelming, it helps to see it as a journey with distinct stages. Each stage has a clear goal and builds on the one before it, leading to a smooth and accurate submission. Approaching it this way avoids that last-minute panic and cuts down on the risk of mistakes that could attract HMRC's attention.

Let's break down the journey into its key stages. This high-level overview gives you a clear picture of what needs to be done and when.

Key Stages of Your Company Tax Return Journey

| Stage | Key Action | Primary Goal |

|---|---|---|

| Preparation | Gather all financial records and statements for the accounting period. | To create a complete and accurate financial picture of the business. |

| Calculation | Adjust accounting profit to calculate taxable profit and Corporation Tax. | To determine the exact amount of tax owed after applying all reliefs. |

| Submission | Complete the CT600 form and file it with accounts to HMRC. | To officially report your company's tax liability to the authorities. |

| Payment & Closure | Pay the calculated Corporation Tax by the due date. | To meet your financial obligation and close the tax year successfully. |

Thinking about the process in these four stages helps organise your efforts and ensures nothing gets missed along the way.

Getting Your Financial Records Ready for Tax Season

A stress-free tax filing experience doesn’t start when you log into the HMRC portal. It starts months, or even a year, beforehand. The real secret is having organised, accurate, and complete financial records at your fingertips.

Before you even glance at a CT600 form, you need all your financial information gathered and reconciled. This isn't just about ticking boxes; it’s about creating a clear and robust financial picture of your business's performance over the year.

This groundwork is what makes the difference between a frantic scramble and a structured, manageable task. It allows you to confidently claim every allowable expense and tax relief, which can have a big impact on your final Corporation Tax bill. Think of it as mise en place for your accounts – get everything prepped, and the final assembly is simple.

Your Essential Document Checklist

To get your company tax return right, you need a core set of documents that tell the financial story of your business's year. Start by gathering everything here; having it all ready will save you a world of pain later on.

First up, your main financial statements. These are non-negotiable.

- Profit and Loss (P&L) Statement: This shows whether you made a profit or loss by summarising all your revenues, costs, and expenses during your accounting period.

- Balance Sheet: This is a snapshot of your company’s financial health on the last day of the accounting period, detailing what you own (assets) and what you owe (liabilities), along with shareholder equity.

These two documents give HMRC the headline figures, but they'll need the detail that sits behind them.

Digging into the Details: Income and Expenses

Your P&L gives the grand totals, but you need the detailed, categorised records for every transaction that makes up those numbers. Every single penny of income needs to be accounted for, from individual sales invoices right down to the interest earned on a business savings account.

On the flip side, you need a fully itemised breakdown of all your business expenses. This is where meticulous, year-round record-keeping really pays for itself. For instance, a single "Marketing" line on your P&L might be made up of hundreds of different costs, from software subscriptions and freelance fees to advertising campaigns.

The better your records, the easier it is to spot every last tax-deductible expense. It’s easy to forget about a small software subscription or a one-off training course, but they all add up. Good bookkeeping is genuinely your best tool for reducing your tax liability.

Beyond the Day-to-Day Transactions

The story of your financial year isn't just about sales and running costs. You have to document other significant events accurately because they come with their own specific tax implications.

Make sure you have all the records for these activities:

- Asset Purchases and Sales: Bought a new company van or sold off some old office computers? You'll need the invoices and receipts to calculate capital allowances correctly.

- Director's Loans: Any money loaned to a director (or from a director to the company) has to be tracked precisely. There are specific tax rules here, like the s455 charge, that you don’t want to get wrong.

- Dividends Paid: You need a clear record of all dividend payments made to shareholders, along with the board minutes that authorised them.

- VAT Records: While VAT is its own separate tax, your quarterly returns are a fantastic way to cross-reference and verify your income and expense figures.

This is where modern accounting software becomes invaluable. It doesn't just organise your day-to-day transactions; it also makes tracking things like assets and loans much more straightforward. For any business trying to become more efficient, using the right technology is a game-changer. For example, looking into automating invoice processing with RPA can dramatically cut down on manual errors, ensuring your records are always up-to-date and ready for tax season.

How to Calculate Your Corporation Tax

Once you’ve got your financial records tidied up, it’s time to get down to the numbers. This is where you’ll translate your company's accounting profit into the figure HMRC actually cares about for your Corporation Tax bill. It's rarely a straightforward case of applying a tax rate to your bottom line; there are some crucial adjustments you need to make first.

The whole point of this exercise is to arrive at your taxable profit. This number can often look quite different from the profit you see in your annual accounts because you have to add back certain expenses that aren't tax-deductible and subtract any allowances or reliefs you're eligible for.

From Accounting Profit to Taxable Profit

First things first, you need to adjust your accounting profit. HMRC has very specific rules about what qualifies as an allowable business expense for tax purposes. Some costs that are perfectly normal in your day-to-day business accounts have to be added back to your profit before you can calculate the tax.

Some of the most common non-allowable expenses include:

- Client entertainment: That lunch you took a client to? It's a valid business cost, but you can’t deduct it for Corporation Tax.

- Depreciation: While you track the declining value of your assets in your own books, HMRC has its own system for this called capital allowances.

- Personal expenses: Any money spent that wasn't "wholly and exclusively" for business must be stripped out.

Getting these adjustments right is fundamental. It can be the difference between paying the right amount of tax and either overpaying or, worse, facing an uncomfortable enquiry from HMRC.

Claiming Capital Allowances

Instead of the depreciation you record in your accounts, you'll claim capital allowances on major assets you’ve bought for the business. Think machinery, computer equipment, or company vehicles. This system lets you deduct a percentage of the asset's value from your profits each year, which in turn lowers your tax bill.

For example, say you invested in a new server for £5,000. You wouldn't just write off the full amount in one go. Instead, you'd claim capital allowances on it over several years at HMRC's set rates. The good news is that for many purchases of plant and machinery, you might be able to claim the entire cost in the first year using the Annual Investment Allowance (AIA).

A quick tip from experience: Getting to grips with capital allowances is a game-changer, especially for businesses that need to invest in equipment. It’s a direct tax reward for your investment and can make a huge difference to your cash flow right after you've made a big purchase.

Unlocking Tax Reliefs and Credits

Beyond capital allowances, there are several other valuable reliefs that can seriously reduce your taxable profit. Many businesses I've worked with, particularly in the tech and manufacturing sectors, are eligible for Research and Development (R&D) tax credits. This is an incredibly generous government scheme that lets you deduct an extra chunk of your R&D costs from your profits.

Don't stop there, though. Other reliefs to look into are:

- Patent Box: This offers a much lower Corporation Tax rate on profits your company earns from its patented inventions.

- Creative industry reliefs: A lifeline for companies in sectors like film, TV production, and video games.

- Trading losses: If you've had a tough year and made a loss, you can often carry it back to a previously profitable year to claim a tax refund, or carry it forward to reduce future tax bills.

It's always worth spending the time to explore these reliefs. You could be leaving money on the table otherwise.

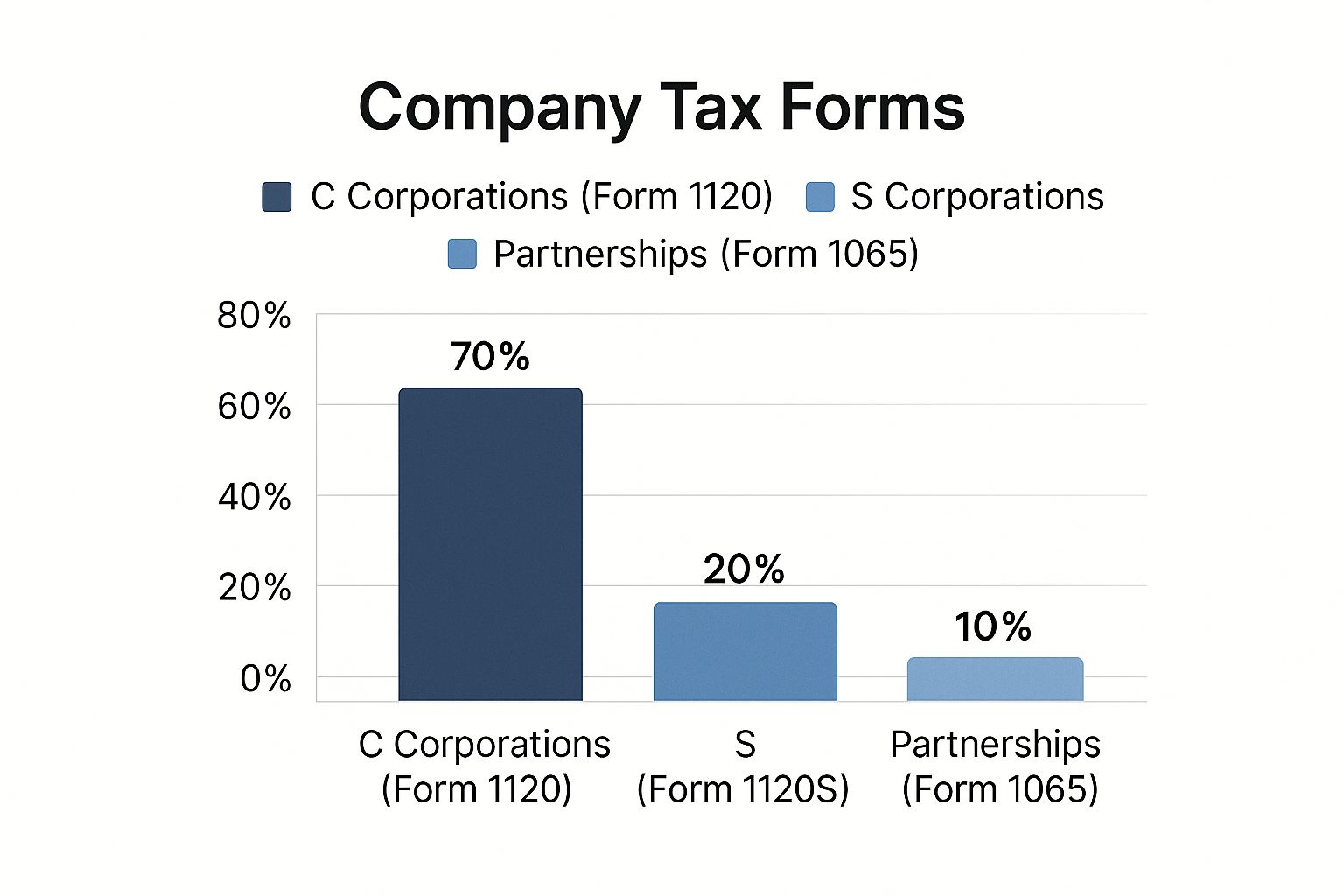

The image below gives a useful snapshot of the different tax forms used by UK companies, showing just how common the standard filings are.

As you can see, the vast majority of companies use a standard form, which really drives home the importance of mastering these core calculation principles.

Applying the Correct Corporation Tax Rate

After all those adjustments, you’ll have your final taxable profit. The last piece of the puzzle is to apply the right Corporation Tax rate. The UK doesn't have a single flat rate; it's a tiered system where the rate you pay is linked to how much profit you’ve made.

This structure is designed to give smaller businesses a bit of a break while ensuring larger, more profitable companies contribute more. Here's a breakdown of the current rates.

UK Corporation Tax Rates and Profit Thresholds

| Annual Profit Level | Applicable Corporation Tax Rate | Key Consideration |

|---|---|---|

| Up to £50,000 | 19% (Small Profits Rate) | This rate applies to companies with lower profits, offering a significant tax saving. |

| Over £250,000 | 25% (Main Rate) | This is the headline rate for the UK’s most profitable companies. |

| Between £50,001 and £250,000 | Tapered Rate | The effective tax rate gradually increases from 19% to 25% due to Marginal Relief. |

This tiered system is why calculating your taxable profit precisely is so critical—a small error could easily push you into a higher effective tax bracket. You can dive deeper into how these tax brackets work by exploring insights on UK corporate taxes from PwC.com.

Once this final calculation is done, you'll have the Corporation Tax figure that you need to report on your CT600 form.

Completing and Submitting the CT600 Form

You’ve done the heavy lifting and calculated your Corporation Tax. Now it’s time to get that information to HMRC using the CT600 form. This is the official document that translates your company's financial year into a formal tax declaration.

Think of the CT600 as the summary sheet for your tax return. It doesn’t contain every last detail; instead, it pulls the key numbers from your full accounts and tax computations into a standardised format that HMRC can process efficiently. Getting this right is obviously critical.

Let's walk through what you need to know to get this form completed accurately and submitted without any hitches.

Navigating the Key Sections of the CT600

At first glance, the CT600 can look intimidating with its 100+ boxes. The good news? You’ll probably only need to fill in a small fraction of them. For most small businesses, the focus is straightforward: declaring your turnover, profits, and the final tax figure you've already worked out.

However, certain circumstances demand a bit more detail, and that's where supplementary pages come in. You’ll need to pay close attention if your company has dealt with any of the following:

- Loans to participators (CT600A): This is a big one. If a director or shareholder has borrowed from the company and the loan isn't repaid within nine months of your year-end, you have to complete this form.

- Controlled Foreign Companies (CT600B): This is less common for small businesses, applying only if you have stakes in companies based in low-tax countries.

- Group and consortium relief (CT600C): If your company is part of a larger group, this section allows you to move losses around to offset profits in another group company, which can be a huge tax-saver.

These areas are where mistakes often happen. Forgetting to declare a director's loan, for instance, can trigger a nasty tax charge under section 455. It’s well worth double-checking if any of these apply to you.

Choosing Your Filing Method

When you’re ready to send everything off, you have a couple of options. Remember, you’re not just sending the CT600 form on its own; it has to be submitted as a single package with your annual accounts and your tax computations.

1. HMRC’s Free Online Service

HMRC does offer a free tool for filing directly. For a very simple business with no complex transactions, it can work. However, it's quite basic. It doesn’t support all the supplementary pages and can be clunky if you're trying to claim certain tax reliefs.

2. Commercial Accounting Software

This is the route most businesses and almost all accountants take. Using dedicated software from providers like Xero, QuickBooks, or other tax platforms is far more reliable. This software is built to handle the nuances of Corporation Tax, guiding you through the process and often linking directly to your bookkeeping records to pull the numbers automatically.

Using dedicated software massively cuts down the risk of manual error. It populates the CT600 from your accounts and ensures the entire submission is formatted correctly for HMRC's systems, saving you a world of time and potential stress.

The iXBRL Format: A Non-Negotiable Requirement

This is a technical detail that trips up a lot of first-time filers. You cannot simply upload a PDF of your accounts to HMRC. Your annual accounts and tax computations must be in a specific digital format called iXBRL (Inline eXtensible Business Reporting Language).

So, what is it? Think of iXBRL as a "smart" document. It looks like a normal set of accounts, but behind the scenes, every important number is digitally "tagged."

For example, the figure for 'Turnover' in your accounts will have a unique iXBRL tag attached to it. This tells HMRC's computers "this number is turnover," allowing them to analyse data automatically without a human having to read it.

Thankfully, you don't need to become an iXBRL expert. This is another major reason why commercial software is the standard. Any approved accounting or tax software will handle this conversion for you, generating your files in the correct format as part of the submission process. If you insist on using HMRC’s free service, you'll have to find another way to convert your accounts to iXBRL first, which just adds an extra, unnecessary step.

Meeting Deadlines and Avoiding Costly Penalties

When it comes to your company's tax obligations, timing is just as crucial as accuracy. One of the easiest—and most frustrating—ways to rack up unnecessary costs is by missing a key date. The secret to avoiding this trap is simple: understand that filing your return and paying your tax are two separate jobs with two different deadlines.

A surprisingly common mistake is thinking the deadline to file your Company Tax Return is the same day you have to pay your Corporation Tax bill. It’s a costly assumption. This mix-up can lead to instant, escalating penalties, even if every figure on your return is perfect. Getting these two dates straight is the first real step towards a penalty-free tax year.

This isn't a niche problem; it affects a huge number of businesses. As of early 2024, there are around 5.5 million private sector businesses in the UK, and 99.9% of them are SMEs. That’s millions of company directors juggling these critical dates every single year. This sheer volume is exactly why HMRC is pushing for simpler digital processes—to help business owners stay compliant and sidestep these common pitfalls. You can dig into more UK business statistics at Money.co.uk.

Identifying Your Key Deadlines

Your company’s tax calendar is entirely dictated by its accounting period—the financial year your annual accounts cover. Everything hinges on this.

- Deadline to Pay Corporation Tax: This one comes first. You must pay your Corporation Tax bill nine months and one day after your accounting period ends.

- Deadline to File Your Company Tax Return: You get a bit more breathing room here. The filing deadline is a full 12 months after the end of your accounting period.

Let's make that real. Say your company's accounting period ends on 31 March. Your tax payment is due by 1 January the following year. But you still have until 31 March of that same year to actually file your CT600 return.

The Real Cost of Missing a Deadline

HMRC's penalty system is automatic and doesn't make exceptions. The fines are designed to get steeper the longer your return is overdue, making procrastination a very expensive habit.

Here’s a quick breakdown of how the late filing penalties stack up:

- 1 day late: You’re hit with an immediate £100 penalty.

- 3 months late: Another £100 is added, bringing the total to £200.

- 6 months late: HMRC will estimate your tax bill and add a 10% penalty on top of their figure.

- 12 months late: Another 10% penalty is applied to any tax that remains unpaid.

It's crucial to realise these penalties are cumulative. If you're late for a second year in a row, those initial £100 fines jump to £500 each. The system is deliberately built to discourage repeat offenders, so getting into a good rhythm from day one is essential.

Proactive Steps to Stay on Track

Staying ahead of tax deadlines isn't about complex software; it's about simple, practical organisation. Don't just rely on your memory.

Pop your payment and filing deadlines into your calendar right now, and set multiple reminders well in advance. Better yet, plan your workflow by working backwards from the payment deadline, not the filing one. Since you have to pay first, aim to have your tax calculation finalised at least a month before that date. This builds in a vital buffer to sort out the payment and deal with any last-minute surprises without descending into panic.

And if you ever think you're going to have trouble, talking to HMRC proactively is always a better move than waiting for a penalty notice to land on your doormat.

Common Questions About Filing Company Taxes

Even with the clearest instructions, filing your company tax return for the first time—or the tenth time—can throw up some tricky questions. Business in the real world isn't always a straight line, so knowing how to handle specific scenarios is key to filing with confidence and staying on the right side of HMRC.

Let's dig into some of the most frequent queries I hear from business owners. Here are some direct, practical answers to help you navigate these common sticking points.

What if I Make a Mistake on My Return?

That heart-stopping moment when you spot an error after hitting 'submit' is something many business owners experience. Don't panic. It's usually straightforward to fix.

If you find a mistake on your Company Tax Return, you can simply amend it. You generally have a window of 12 months from the original filing deadline to make any changes. You can do this by submitting an amended return online through your accounting software or HMRC’s portal. This new submission just replaces the old one, making sure your records are completely accurate.

It's always, always better to voluntarily correct a mistake than to wait for HMRC to find it. Being proactive shows you're diligent and can help you avoid much harsher penalties that might come your way if an error is uncovered during an inspection.

The scale of company tax filings really highlights why accuracy is so vital. For the 2024/25 tax year, corporation tax receipts were projected to hit around £91.6 billion—a massive jump of over 14% from the previous year. This shows just how crucial these submissions are to the government's finances and why HMRC is so focused on compliance. You can explore more insights on UK tax receipts on Statista.com.

Do I Still File if My Company Made a Loss?

Yes, absolutely. This one is non-negotiable. You are legally required to file a Company Tax Return every year, no matter if you made a profit or a loss.

In fact, filing a return when you've made a loss is actually a smart move for your business. By officially declaring a trading loss, you unlock a couple of valuable options:

- Carry it back: You can offset the loss against profits from the previous year, which can trigger a tax refund.

- Carry it forward: You can use the loss to reduce your taxable profit in future years, effectively lowering your tax bill when you get back in the black.

Think of it as banking a future tax saving. If you ignore this filing duty, you not only risk late filing penalties but you also miss out on tax relief that could be a huge help down the line.

Can I File the Return Myself?

Technically, yes, you can. HMRC provides the tools and guidance for directors who want to handle their own tax affairs. The real question, though, is should you?

Filing a company tax return is more than just plugging numbers into a form. You need a solid understanding of things like:

- Allowable expenses: Knowing exactly what you can and can't claim against your profit is an art in itself.

- Capital allowances: You need to correctly calculate the tax relief on assets your company has bought, from laptops to machinery.

- Complex tax reliefs: Are you missing out on things like R&D tax credits that could save your company thousands?

- iXBRL formatting: Your accounts must be submitted in a specific digital format, which can be a technical hurdle.

For a very simple, non-trading company, a DIY approach might be feasible. For most active businesses, however, the risk of making a costly error or missing out on significant tax savings is incredibly high. The fee for a good accountant is often a fraction of the tax you could save or the penalties you could avoid.

What if I Can't Afford to Pay My Tax Bill?

If you can see that you won't be able to pay your Corporation Tax bill by the deadline, the absolute worst thing you can do is bury your head in the sand. HMRC can be surprisingly reasonable and supportive of businesses facing genuine financial difficulty, but only if you communicate with them early.

Get in touch with HMRC and ask for a ‘Time to Pay’ arrangement. This is a formal agreement that lets you pay your tax bill in instalments over a period you both agree on.

To set one up, you'll need to explain why you can't pay in full, what you’ve done to try and get the funds together, and what you can realistically afford to pay each month. Being prepared, honest, and proactive makes a positive outcome far more likely.

At Stewart Accounting Services, we take the stress and uncertainty out of your tax obligations. Our team of Chartered Accountants specialises in helping SMEs across Central Scotland and the UK with their company accounts and tax returns. We ensure you're fully compliant while spotting every opportunity to improve your bottom line. We handle the complexities so you can focus on running your business with peace of mind. Let us help you achieve more time, more money, and a clearer mind by visiting us at https://stewartaccounting.co.uk.