If you want to increase your profit margins, you need to make more money from every pound you sell. It’s that simple. You can achieve this by raising prices, cutting costs, or just getting more efficient. At its heart, it all comes down to the relationship between three key numbers: your revenue, your direct costs, and your overheads. Get a handle on these, and you're well on your way to a much healthier bottom line.

Where Are You Now? Establishing Your Profit Baseline

Before you can even think about improving your profit margins, you have to know what they are right now. Trying to boost profitability without a clear baseline is like setting off on a road trip with no map – you’ll be moving, but you won't have a clue if you're going in the right direction.

For any SME owner, the first step is to get comfortable with the numbers and what they’re telling you about the health of your business. This is about more than just a quick glance at your bank balance. It’s about calculating three specific profit margins, each of which tells a different part of your financial story. Moving from guesswork to a data-backed strategy is how you truly improve profit margins with business leverage and build a foundation for real, sustainable growth.

The Three Core Profit Margins You Need to Know

Think of your profit margins as diagnostic tools. Each one shines a light on a different part of your business, helping you pinpoint exactly where you can make improvements.

Before we dive in, here’s a quick reference table breaking down the three key margins.

Understanding Your Key Profit Margins

| Margin Type | How to Calculate It | What It Reveals |

|---|---|---|

| Gross Profit Margin | (Revenue – Cost of Goods Sold) / Revenue | The profitability of your core products or services themselves, before any overheads. |

| Operating Profit Margin | (Operating Income / Revenue) | Your company's earning power from its day-to-day business operations, after overheads. |

| Net Profit Margin | (Net Income / Revenue) | The final figure showing what’s left after all expenses, including interest and taxes. |

Knowing these figures is crucial. They help you answer important questions. Is the problem with your production costs? Are your operational expenses too high? Or is something else eating into your final profit? If you need a more detailed breakdown of your financial statements, our guide on how to read a profit and loss statement is a great place to start.

Using Technology to Get an Accurate Baseline

Thankfully, the days of wrestling with clunky spreadsheets and manual calculations are over. Modern cloud accounting software gives you an accurate, real-time baseline without the headache.

Platforms like Xero are designed for this. They automatically categorise your transactions and generate financial reports on the fly, giving you an up-to-the-minute view of your business’s financial health. This kind of instant insight is vital for making smart, timely decisions.

With this data at your fingertips, you can spot trends as they emerge. Imagine seeing a sudden drop in your gross profit margin. This could be an early warning sign that your supplier costs are creeping up, giving you a chance to renegotiate terms or find a new vendor now, not three months down the line when the problem is much bigger. This proactive approach is the secret to protecting your margins.

Optimising Your Pricing and Product Mix

Once you’ve got a firm grip on your baseline numbers, it’s time to look at where your money is actually coming from: your revenue streams. I see it all the time—so many small and medium-sized businesses leave cash on the table by underpricing what they sell or pouring energy into the wrong products.

If you’re serious about boosting your profit margins, you have to move beyond a simple cost-plus calculation.

This isn’t about plucking numbers out of thin air. It’s about making small, deliberate shifts backed by data that add up to a big impact. A smart analysis of your pricing and product mix can unlock hidden profitability without scaring away your customers.

Moving Beyond Cost-Plus Pricing

The go-to pricing method for many is cost-plus. You figure out your costs, slap on a standard markup, and you’re done. Simple, yes, but it completely misses the bigger picture: the actual value you deliver.

Smarter pricing strategies are all about what your customers are willing to pay, not what it costs you to make something. This change in thinking is absolutely fundamental.

Value-Based Pricing: Here, you set your price based on the value your product or service provides. If your software saves a client £10,000 a year in admin time, pricing it at £2,000 suddenly feels like an incredible deal for them, even if your internal cost is only £200.

Tiered Offerings: Instead of one price for everyone, why not create different packages? Think Bronze, Silver, and Gold. This lets customers choose the level of service they need and can afford, often nudging them towards a more premium option.

To really nail these methods, you need to get inside your customers' heads and understand the problems you're solving for them. We explore this in more detail in our guide on valuing and pricing goods and services.

Analyse Your Product and Service Profitability

Here’s a hard truth: not all revenue is good revenue. Some of your products and services are almost certainly working much harder for you than others. Digging into your sales data to find your star performers is one of the most powerful moves you can make.

Start by calculating the gross profit margin for each individual product line. You might be shocked at what you uncover.

Take a local café that sells artisan sandwiches and custom-made cakes. A quick look at the numbers shows their sandwiches have a juicy 70% margin. The custom cakes, which take ages to make, only bring in a 20% margin. That single piece of information changes everything.

Armed with this insight, the café owner can now make some sharp decisions:

- Shift Marketing Focus: Push the high-margin sandwiches on social media, in-store promotions, and on the menu board.

- Adjust Pricing: Raise the price of the custom cakes to better reflect the skill and time required, instantly improving their margin.

- Create Bundles: Introduce a "lunch deal" that pairs a high-margin sandwich with a lower-margin drink, driving up the average spend and overall profit.

This isn’t about axing less profitable items, especially if they’re what gets people through the door. It’s about being deliberate with your time and resources, focusing them where they’ll make the biggest difference to your bottom line.

The Impact of Strategic Pricing on UK SMEs

This focus on smarter revenue generation is precisely what separates the good businesses from the great ones. Strategic pricing and revenue growth strategies have propelled top UK SMEs to outperform their peers, with mean non-financial profit margins rising from 13.0% in 1997 to 14.2% in 2023, despite median drops. This shows how limited company owners can scale by leveraging expertise. In fact, two-fifths of SMEs reported revenue increases in the prior year. For the many sole traders and small businesses handling HMRC filings, payroll, and VAT, optimising pricing is a key route to achieving healthy margins of 10-15%. Discover more insights about average profit margins in the UK on mypos.com.

Making these small, calculated tweaks to your pricing and product mix is one of the most direct ways to increase your profit margins. It costs next to nothing to implement but can give your profitability an immediate and lasting boost.

Controlling Costs Without Compromising Quality

Once you've looked at your revenue, the other side of the profitability coin is getting your costs under control. For a lot of business owners I speak to, this feels like the most direct and tangible way to make a difference. Every single pound you save on expenses goes straight to your bottom line, boosting your net profit without you having to make a single extra sale.

Now, this isn’t about just slashing budgets across the board. That’s a fast track to unhappy staff and a lower-quality product. The real skill is in being deliberate and surgical—performing a proper audit of where your money is going and making intelligent, sustainable reductions. It’s about trimming the fat, not the muscle.

This process has never been more critical. Across the UK, small business profit margins have been squeezed, falling from an average of 10.7% in Q1 2023 to just 8.8% by Q2 2024. This drop highlights the immense pressure of rising costs, which a staggering 47% of SMEs now name as their number one challenge. For those of us running limited companies, getting smart with cloud accounting and other efficiencies is key. You can dig into more of the latest UK small business statistics on money.co.uk.

Conduct a Ruthless Overheads Review

Your indirect costs, or overheads, are often fertile ground for finding quick savings. These are the expenses that keep the lights on but aren't directly tied to producing your goods or services—and they have a sneaky habit of piling up if you’re not watching them closely.

The best place to start? Export a full list of all recurring payments from your accounting software. Go through it, line by line, and ask one simple question for each expense: "Is this absolutely essential for us to operate?" You’ll probably be surprised by what you find.

- Software Subscriptions: Are you paying for multiple tools that basically do the same job? Still have licences active for team members who left months ago?

- Professional Services: Take a look at your contracts for things like marketing, IT support, or even the office cleaning. Are the terms still competitive, or could you get a better deal elsewhere?

- Utilities and Rent: These are tougher to change, of course, but it never hurts to check if you can renegotiate terms or switch to more cost-effective utility providers.

I worked with a small creative agency in Stirling who did exactly this. They found they were paying for three different project management tools, two separate cloud storage services, and a handful of niche design software licences that hadn't been touched in over a year. By simply cancelling the overlaps and unused accounts, they cut their annual software bill by over £5,000. That’s pure net profit.

Renegotiate with Your Suppliers

Your direct costs, especially your Cost of Goods Sold (COGS), are another huge opportunity to improve your margins. Your relationships with suppliers shouldn't be set in stone; think of them as dynamic partnerships that need a regular health check.

Don't be afraid to pick up the phone and start a conversation. You might be surprised—many suppliers are willing to negotiate, particularly if you're a loyal, long-term customer.

Here’s how I’d suggest you approach it:

- Do your homework first. Before you even make the call, get fresh quotes from at least two other potential suppliers. Knowing the current market rate gives you real leverage.

- Remind them of your value. Don’t be shy. Point out your loyalty, your consistent order volume, and the fact you always pay on time.

- Think beyond the price tag. If they can't budge on the unit price, what else can they offer? Maybe better payment terms (like 60 days instead of 30), a new bulk discount tier, or free delivery? These all help your cash flow and reduce other related costs.

Even a small discount here can have a massive impact. Let’s say your COGS represents 40% of your revenue. A simple 5% reduction in your supplier costs will instantly increase your gross profit margin by 2%. It’s one of the most powerful levers you can pull.

Using Technology and Automation to Work Smarter

Once you've got a handle on your pricing and costs, the next big lever for boosting your profit margin is operational efficiency. For any SME, time is quite literally money. Every hour your team spends manually keying in data, chasing up an invoice, or correcting a simple mistake is an hour they’re not spending on the things that actually drive the business forward.

The answer isn’t to work longer hours; it's to work smarter. By bringing the right technology and automation into your business, you can cut down on repetitive tasks, reduce the risk of costly human errors, and give your people the space to focus on high-value work. This isn't about replacing your team; it's about empowering them.

Building Your Modern Accounting App Stack

The starting point for any truly efficient business these days is a solid cloud accounting system. For most UK SMEs we work with, Xero acts as the central hub for their finances. But the real magic happens when you start connecting other specialist apps to it, creating what’s known as an ‘app stack’.

This is all about getting different parts of your business talking to each other, letting data flow automatically between systems. Forget about manually typing information from your CRM into your accounting software – the apps can do that for you.

Just take a look at the sheer number of applications designed to plug straight into a platform like Xero. It's a huge ecosystem.

This marketplace shows there’s a tool for almost everything, from HR and payroll to stock control and detailed reporting. By choosing a few key apps that solve your biggest headaches, you can build a powerful, custom system that makes a massive difference to your day-to-day efficiency. Navigating all these options can be daunting, but we can help you find and implement the right accounting process automation for your specific needs.

To give you a clearer idea, here’s a look at how different apps can plug into your core accounting system to streamline various business functions.

Building Your SME Efficiency App Stack

A look at key business functions and the popular cloud-based apps that can automate them, centred around Xero for seamless integration.

| Business Function | Example Xero-Integrated App | How It Boosts Efficiency |

|---|---|---|

| Bills & Expenses | Dext Prepare | Eliminates manual data entry. Staff just snap a photo of a receipt, and the data is extracted and sent straight to Xero, ready to be reconciled. |

| Sales & CRM | HubSpot | Creates a seamless link between your sales team and finance. Invoices can be generated automatically in Xero when a deal is closed in HubSpot. |

| Payments | GoCardless | Automates collecting recurring payments via Direct Debit. It marks invoices as paid in Xero, saving huge amounts of time on payment admin. |

| Reporting & Forecasting | Fathom | Pulls your Xero data into beautiful, insightful management reports and cash flow forecasts, giving you a much clearer view of business performance. |

| Payroll & HR | BrightPay | Manages your payroll calculations and compliance, then posts all the wage journals directly into Xero, saving you from complex manual calculations. |

This isn't about adding complexity; it's about connecting the dots. Each integration removes a manual step, which not only saves time but also reduces the chance of errors creeping in.

Key Integrations for an Immediate Impact

You don't need a dozen different apps to feel the benefit. In my experience, focusing on one or two high-impact areas first is the best way to get started.

Here are a couple of the most popular and effective integrations we see:

Receipt Capture: A tool like Dext (which used to be called Receipt Bank) is a game-changer. You or your team can just snap a photo of a receipt on a phone. The app uses technology to read the supplier, date, amount, and VAT, then sends it all straight into Xero. This one simple change can claw back countless hours of mind-numbing data entry.

Payment Processing: Connecting a payment provider like Stripe or GoCardless to your Xero invoices makes it ridiculously easy for your clients to pay you. It also automates the reconciliation, matching payments to invoices for you. This doesn’t just cut down on admin; it directly speeds up your cash flow.

Ultimately, the goal here is to create a 'single source of truth' for your finances. When all your systems are communicating, your data is always accurate and up-to-date. That means you can trust the numbers you're seeing and make much better business decisions.

The Strategic Value of Outsourcing

Automation is fantastic, but sometimes the most efficient and profitable move is to hand a whole function over to an expert. Outsourcing things like payroll, bookkeeping, or VAT returns is a strategic decision that can have a direct, positive impact on your bottom line.

Think about it: instead of hiring a full-time bookkeeper, you get access to a specialist team for a fraction of the cost. This also lifts the burden of keeping up with ever-changing regulations like PAYE or Making Tax Digital, letting you focus your energy on what you do best – running and growing your business. For those looking to take things a step further, exploring advanced AI automation solutions can unlock even greater efficiencies across your operations.

Your 90-Day Profitability Action Plan

All the strategies we've discussed are great in theory, but ideas don't pay the bills. Real progress only happens when you put them into practice with consistent, focused action.

This 90-day plan is designed to turn all that theory into tangible results. It breaks down the journey to healthier profit margins into manageable, week-by-week steps. Think of it less as a rigid set of rules and more as a launchpad to build momentum, create good financial habits, and make meaningful changes that actually stick.

The goal is simple: move from just looking at the numbers to actively improving them, and see a real difference in your bottom line within a single business quarter.

Month 1: Foundations and Quick Wins (Days 1-30)

The first month is all about getting your bearings and grabbing the low-hanging fruit. Before you can measure success, you need to know exactly where you’re starting from. Nailing a few quick wins early on will also give you the momentum needed to tackle the bigger challenges ahead.

Weeks 1-2: Establish Your Baseline. Your first job is to get the data. Jump into your accounting software and calculate your gross, operating, and net profit margins for the last quarter. This isn't just a box-ticking exercise; this is the benchmark against which you'll measure every bit of progress.

Weeks 3-4: Conduct a Cost Audit. This is where you’ll find your first easy savings. Export a full list of all your recurring overheads – software, subscriptions, utilities, the lot – and scrutinise every single line. At the same time, list your top five suppliers by annual spend and start getting quotes from alternatives. This prepares you for some serious renegotiations.

Your goal for this first month is simple: clarity and control. By the end of Day 30, you should know your exact margins and have identified at least three non-essential costs you can cut immediately.

Month 2: Strategic Optimisation (Days 31-60)

With a clear baseline established and a few cost savings already in the bank, Month 2 is about making smarter, more strategic shifts in how you generate revenue. It’s time to focus on working smarter, not just harder, by optimising what you sell and how you price it.

This is where the more difficult, but often more rewarding, work really begins.

Weeks 5-6: Analyse Your Product and Service Mix. Run a proper profitability analysis on each of your key offerings. You need to identify your ‘hero’ products (high margin, high volume) and your ‘villain’ products (low margin, high effort). You can't make smart decisions without knowing which parts of your business are actually pulling their weight.

Weeks 7-8: Implement Pricing Adjustments. Armed with that profitability data, it’s time to act. For your most valuable offerings, consider a small, value-justified price increase of 3-5%. For your least profitable items, you have a choice: raise prices significantly, bundle them with a hero product, or make the tough call to phase them out entirely.

The objective for Month 2 is to reshape your revenue streams for maximum profitability. You should aim to have a new pricing structure in place and a clear marketing plan that pushes your most profitable services.

Month 3: Automation and Monitoring (Days 61-90)

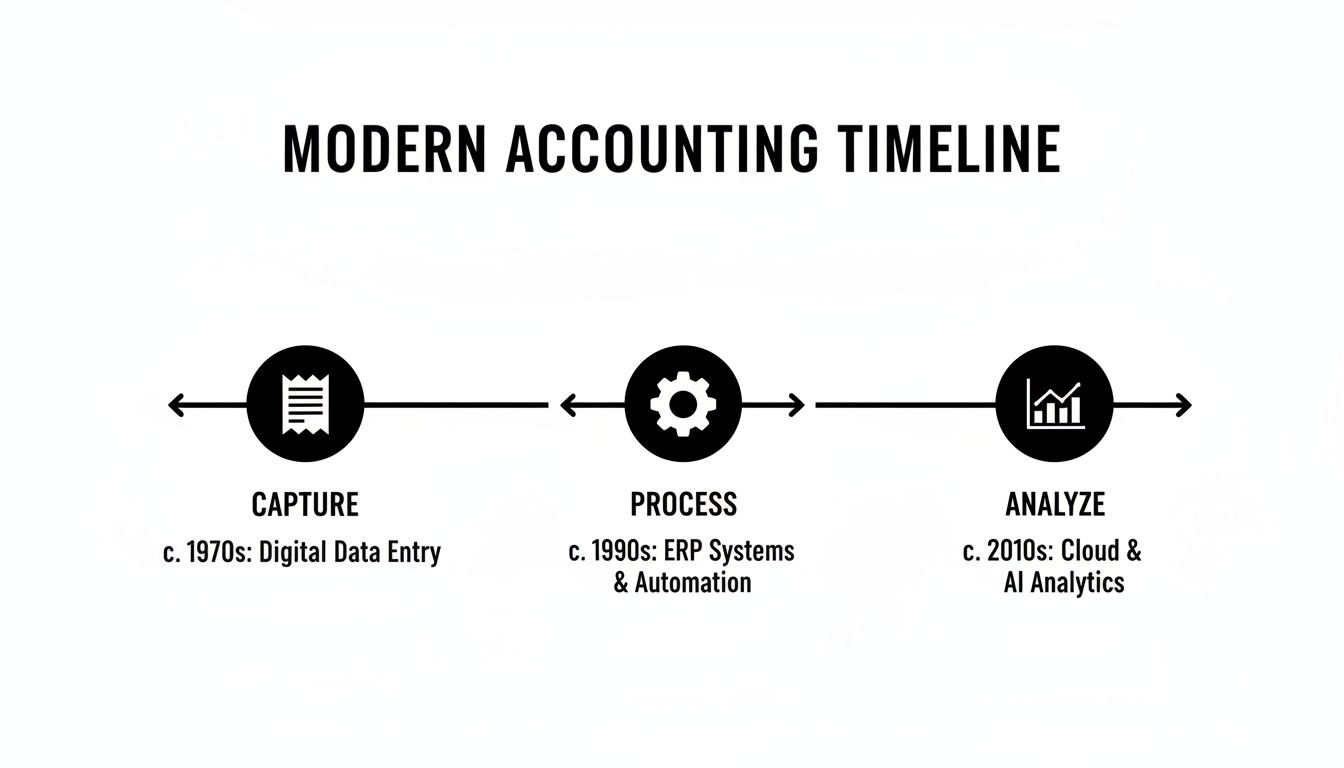

The final month is all about embedding efficiency into your day-to-day operations and building a system for ongoing monitoring. This is what ensures the gains you've made aren't just a one-off boost, but the start of a continuous cycle of improvement.

This stage moves you from actively 'doing' the work to building systems that work for you. Modern accounting is a simple progression: you capture data, process it efficiently, and then analyse it for insights.

This diagram shows it perfectly – analysis is the final, crucial step. Technology should handle the heavy lifting of capturing and processing data, freeing you up for strategic thinking.

Weeks 9-10: Put Technology to Work. Identify your single biggest administrative bottleneck. Is it chasing overdue invoices? Manually typing up expense receipts? Choose just one process to automate this month. Bringing in a tool like Dext for receipt capture or GoCardless for direct debit payments can save you hours every single week.

Weeks 11-12: Set Up Your KPIs and Review. You can't improve what you don't measure. Establish 3-5 key performance indicators (KPIs) that you will track every single month. These must include your three core profit margins, but you could also add metrics like Average Billable Rate or Customer Acquisition Cost. Most importantly, schedule a recurring monthly meeting—even if it's just with yourself—to review these numbers and track your progress.

By the end of this plan, you will have shifted from being reactive to proactive. You’ll have a leaner cost base, a more profitable mix of products and services, and the systems in place to keep your business financially healthy for the long term.

Got Questions About Profit Margins? We've Got Answers

Once you start digging into your profit margins, a lot of questions tend to crop up. You've done the hard work of calculating your baseline, looking for cost savings, and rethinking your pricing. So, let's tackle some of the common things that trip business owners up.

Getting your head around these points is key to making smart decisions and keeping your business on the right track financially. Think of this as your quick-fire guide to clearing up the confusion.

What’s a "Good" Profit Margin for a Small UK Business?

This is the million-dollar question, and the honest answer is: it really depends on your industry. A software business might enjoy healthy net margins of 30% or more, whereas a local café or retail shop could be doing brilliantly on 5-10%.

Rather than fixating on a single magic number, it's far more helpful to focus on two things:

- Your Industry's Benchmark: Get a feel for the average profit margins in your specific sector here in the UK. This gives you a realistic goalpost to aim for.

- Your Own Progress: The best measure of success is your own trajectory. If you made 8% net profit last year and you’ve managed to push that to 10% this year, that’s a massive win.

As a general rule of thumb for many service-based SMEs, a net profit margin of 10% is considered healthy, 20% is fantastic, and anything below 5% is a red flag. It probably means you need to take an urgent look at your pricing, your cost of sales, or both.

How Do I Put My Prices Up Without Losing Customers?

The fear of upsetting loyal customers is completely valid, but increasing your prices is often vital for growth. The trick is all in how you handle it. Just slapping an extra 5% on your next invoice out of the blue is a sure-fire way to get people’s backs up.

You have to shift the focus from price to value.

A price increase becomes so much easier for a customer to swallow when they feel they’re getting more in return. It’s not about the price tag; it’s about the whole experience and the results you deliver.

Try thinking about it like this:

- Add More Value First: Before you even mention a price change, can you introduce a small, low-cost perk? Maybe it's a monthly summary report, a quick check-in call, or access to a new resource. It sweetens the deal.

- Be Transparent: Explain why things are changing. Honesty goes a long way. Mentioning that your own supplier costs have risen, or that you're investing in better tech to serve them, feels justified, not greedy.

- Phase It In: A sudden 15% hike is a shock to anyone's budget. It’s often much smarter to introduce a 5% increase every six months. It’s less of a jolt and gives your clients time to adjust.

Which Costs Should I Tackle First?

When you need to boost your bottom line, cutting costs is the fastest way to make an impact. The secret is to start with the expenses that won’t hurt the quality of your work or your team's morale.

Always go for the low-hanging fruit first—the non-essential overheads.

- Audit Your Subscriptions: Comb through your bank statements and look at every recurring payment for software and services. I guarantee you’ll find tools you forgot you were paying for or licences for staff who left months ago.

- Renegotiate with Suppliers: Don't just accept your current rates as final. It costs you nothing to get a few quotes from competitors, and you can use that as leverage to negotiate better terms with your existing partners.

- Scrutinise Office Overheads: Take a look at everything. Stationery, printing, utilities, cleaning services—all those little things. Small savings across lots of different areas can add up to a serious amount over a year.

The aim here is to trim the fat, not the muscle. By zeroing in on these areas, you can make a real difference to your net profit without compromising the stuff your customers actually pay you for.

Ready to stop guessing and start growing? The expert team at Stewart Accounting Services can help you analyse your numbers, identify opportunities, and build a clear strategy to boost your profitability. Find out how we can help your business thrive.