For most UK limited company directors, the secret to maximising your take-home pay isn't about one big salary. Instead, it's about a clever, tax-efficient blend of a low salary and high dividends. This strategy is all about making the tax system work for you, not against you.

It’s a common misconception for new directors to think they can just transfer money from the business account whenever they need it. But your company is a distinct legal entity, and its money isn't yours until it's paid out properly. Getting this wrong can land you in hot water with HMRC.

The Smart Way to Pay Yourself From Your Limited Company

The most effective and widely used approach involves splitting your income into two streams:

- A Director's Salary: Think of this as a small, regular wage you pay yourself through the company's PAYE scheme.

- Shareholder Dividends: These are payments made from the company's post-tax profits, rewarding you as a business owner.

This isn't some obscure loophole; it’s a standard, legitimate strategy that savvy business owners have been using for years. It allows you to wear both your 'employee' and 'owner' hats, and get the financial benefits of each.

Why This Combination Is So Powerful

The real magic happens when this salary-dividend mix meets the UK tax system. It all comes down to navigating National Insurance Contributions (NICs) and your personal tax-free allowance in the smartest way possible.

By setting your salary at just the right level, you can build up qualifying years for your State Pension without actually paying any income tax or National Insurance on it. It’s a win-win.

Then come the dividends. Crucially, dividends are not subject to National Insurance. That's an immediate, hefty saving compared to taking all your income as a salary, where you'd be paying NICs on every pound above the threshold.

Need proof? Tax specialists consistently show this is the best approach. One analysis found a director taking a salary of £12,570 and the rest in dividends could boost their net income by over £2,000 a year compared to just taking dividends. You can dive deeper into these tax-efficient salary calculations on 1st Formations' blog.

The core idea is simple: pay yourself a salary up to a key tax threshold. This salary becomes a business expense, lowering your Corporation Tax bill. You then take the rest of the profits as dividends, which are taxed at a much friendlier rate.

Once you grasp this principle, you're no longer just taking money out of the business; you're strategically managing your income. This guide will show you exactly how to set it all up, step by step.

Before we get into the nitty-gritty of setting salaries and declaring dividends, let's quickly compare the two side-by-side. This table gives you a clear snapshot of how each payment method works and why combining them is so effective.

Director's Pay At a Glance: Salary vs Dividends

| Feature | Salary | Dividends |

|---|---|---|

| Tax Treatment | Treated as employment income, subject to Income Tax and National Insurance. | Treated as investment income, subject to Dividend Tax rates. |

| National Insurance | Employee's and Employer's NICs are payable above certain thresholds. | No National Insurance is due from the director or the company. |

| Corporation Tax | It's an allowable business expense, reducing the company's Corporation Tax bill. | Paid out after the company has paid Corporation Tax on its profits. |

| Timing of Payment | Can be paid anytime, typically monthly, regardless of company profit. | Can only be paid if the company has sufficient post-tax profits available. |

| State Pension | A qualifying salary builds up entitlement to the State Pension. | Dividends do not count towards your State Pension qualifying years. |

As you can see, each has its own distinct advantages. The salary gives you pension credits and reduces company profit for tax purposes, while the dividends offer the huge benefit of zero National Insurance. By combining them, you get the best of both worlds.

Finding the Optimal Director's Salary for Your Business

Alright, let's zero in on the salary part of your pay. Nailing your director's salary isn't about just pulling as much as you can out of the business; it's a strategic move to find a tax-efficient 'sweet spot'. This magic number is dictated by a couple of key government thresholds: your Personal Allowance and the National Insurance (NI) limits.

Getting your head around these thresholds is the key to paying yourself smartly as a limited company director. If you get this right, you can draw a wage without losing a penny to income tax or personal NI, all while making sure you're still building up your State Pension entitlement for the future.

From the company's point of view, this salary is more than just money in your pocket. It’s a legitimate business expense, which means it reduces your company's taxable profit. That directly lowers your Corporation Tax bill at the year's end. It's a classic win-win.

The Magic Number for Your Salary

So, what is this optimal salary? While the exact figures get tweaked by the government in most tax years, the underlying strategy stays the same. The goal is to pay yourself up to a specific threshold that gives you the maximum benefit for the minimum tax hit.

For the 2025/26 tax year, the ideal salary for most solo limited company directors is £12,570 per year. This figure is so important because it lines up perfectly with the standard Personal Allowance – the amount you can earn before you have to start paying income tax.

By setting your salary at exactly this level, you tick a few very important boxes all at once:

- No Income Tax: Your entire salary is covered by your tax-free Personal Allowance, meaning you pay 0% income tax on it.

- No Employee NI: The point at which you start paying employee National Insurance also happens to be £12,570, so you won't pay any contributions yourself.

- Qualifying for State Pension: Crucially, this salary is above what's called the Lower Earnings Limit for National Insurance. This means that even though you aren't physically paying NI contributions, the year still counts as a 'qualifying year' towards your State Pension.

This clever alignment lets you take £12,570 out of your company completely tax-free on a personal level, while still banking those valuable pension credits.

What About the Company's Contribution?

Now, a salary of £12,570 is fantastic for you personally, but we also have to look at it from the company's perspective. There's another piece to this puzzle: employer's National Insurance. The threshold where a company has to start paying employer's NI is actually much lower than the employee one.

This is where you have a decision to make. For the 2025/26 tax year, paying a salary of £12,570 means the company will have to pay a small amount of employer's NI.

So why do it? For most directors, paying this small NI bill is a worthwhile trade-off. The entire £12,570 salary is deducted from the company's profits before Corporation Tax is worked out. The tax saving you make on Corporation Tax almost always outweighs the small cost of the employer's NI, making it the most efficient route overall. This is especially true if your company is turning a decent profit and paying the main rate of Corporation Tax.

A Quick Scenario

Picture this: your company has £60,000 in pre-tax profit. By paying yourself that £12,570 salary, you instantly reduce the taxable profit to £47,430. Just like that, you've cut your Corporation Tax bill before you've even touched your dividends.

Why Not Just Pay a Lower Salary?

You might be thinking, "Why not just pay a salary below the employer's NI threshold and avoid that cost altogether?" It’s a fair question. You could pay yourself a smaller salary (say, around £9,100) and the company wouldn't have any NI to pay.

The catch is that you need to earn above the Lower Earnings Limit (which is even lower, around £6,725) to make qualifying contributions for your State Pension. For this reason, most accountants will tell you that paying a salary right up to the Personal Allowance is the better long-term strategy. It strikes the perfect balance between personal tax efficiency, company tax savings, and your future state benefits.

Most detailed analyses, like this breakdown of how the optimum salary is calculated on IT Contracting, confirm that for the 2025/26 tax year, the £12,570 salary level minimises the total tax paid by both you and your company.

Once you've got this optimal salary set up and running through your company's payroll, you've built a solid, tax-efficient foundation. The next step is to look at using dividends to draw any further income you need from the company's remaining profits.

Using Dividends to Boost Your Take-Home Pay

Now that your director's salary is sorted, let's talk about the second, and usually much larger, slice of your income: dividends. For most of us running a limited company, dividends are the main event – it’s how we really get paid for the company’s success.

It’s crucial to understand that a dividend isn't just another word for salary. Your salary is what you get for being a director, for doing the day-to-day work. A dividend, on the other hand, is a distribution of company profits to you as a shareholder. This distinction isn't just semantics; it comes with a non-negotiable golden rule.

The Golden Rule of Dividends

Here it is: you can only declare and pay a dividend if your company has enough retained profits to cover it. This is after you’ve accounted for all your business costs and liabilities, including your upcoming Corporation Tax bill.

Getting this wrong is a serious misstep. Taking money out as a dividend when the company isn’t actually profitable is what HMRC calls an ‘illegal’ or ‘ultra vires’ dividend. If they find out, you'll be facing penalties and will almost certainly have to pay the money back.

Think of it this way. Your salary is a business expense, just like your phone bill or software subscriptions. Dividends are the reward, the spoils of victory, paid out only after the business has won its financial battles for the year.

How to Declare Dividends the Right Way

You can't just move money from the business account to your personal one and call it a dividend. To keep everything compliant and create a clear paper trail for HMRC, there’s a formal process you need to follow. This protects you and proves the payment is a legitimate distribution of profit.

Here’s what you need to do:

- Hold a directors' meeting. Yes, even if you’re the only director and shareholder, you need to formally minute the decision to declare a dividend. The minutes should clearly state the total dividend amount and the date it was declared.

- Create a dividend voucher for each shareholder. This is a simple but essential document that acts as a formal record of the payment.

For a dividend voucher to be valid, it has to include:

- Your company's name

- The date of the payment

- The name of the shareholder

- The number of shares they hold

- The total dividend amount they are being paid

Keeping these records is absolutely non-negotiable. They are your proof that you’ve followed the correct procedure for paying yourself as a limited company director.

Understanding Dividend Tax

One of the biggest perks of taking dividends is that they are not subject to National Insurance contributions. This alone can save you a significant amount compared to taking a larger salary. But they aren't entirely tax-free. You do pay personal tax on them, just at special dividend tax rates.

The system is designed to be quite generous, especially at the lower end. For the 2025/26 tax year, every person has a tax-free Dividend Allowance of £500. This means the first £500 of dividends you receive in the tax year doesn’t cost you a penny in personal tax.

Key Takeaway: The £500 Dividend Allowance is completely separate from your Personal Allowance. This means you can earn your £12,570 salary tax-free and also receive £500 in dividends tax-free in the same year.

Once you’ve used up that allowance, any further dividends are taxed based on which income tax band you fall into. The rates for the 2025/26 tax year are:

- Basic Rate Taxpayers: 8.75%

- Higher Rate Taxpayers: 33.75%

- Additional Rate Taxpayers: 39.35%

Your total income from all sources (including your salary) determines your tax band. You’ll declare your dividend income on your annual Self-Assessment tax return and settle up with HMRC then.

A Practical Example of Your Take-Home Pay

Let's pull all this together and see how it works in a real-world scenario.

Imagine you're the sole director and shareholder of a company that's made a profit of £60,000 before paying your salary.

- Pay Your Salary: First, you pay yourself that tax-efficient salary of £12,570.

- Calculate Corporation Tax: This salary is a business expense, so the company's taxable profit is now £60,000 – £12,570 = £47,430. Assuming your profits fall under the small profits rate of 19%, the company’s Corporation Tax bill will be £9,011.70 (£47,430 x 19%).

- Find the Available Profit for Dividends: After tax, the remaining profit is £47,430 – £9,011.70 = £38,418.30. This is the maximum amount you can legally take as a dividend.

- Work Out Your Personal Tax:

- Your £12,570 salary is covered by your Personal Allowance, so you pay £0 income tax and NI on it.

- You draw the full £38,418.30 as a dividend.

- The first £500 is tax-free thanks to your Dividend Allowance.

- The remaining £37,918.30 is taxed at the basic rate of 8.75%, which comes to £3,317.85.

So, what's your final take-home pay? It’s your salary plus the dividend after you've paid the personal tax:

£12,570 (salary) + £35,100.45 (net dividend) = £47,670.45

This salary-plus-dividend strategy is hands-down the most efficient way to pay yourself from a profitable UK limited company, making sure as much of your hard-earned money stays in your pocket.

Claiming Business Expenses to Lower Your Tax Bill

So, we've covered your salary and dividends, but there's a third crucial piece of the financial puzzle for any limited company director: business expenses. This isn't about paying yourself in the traditional sense. Instead, it’s about your company paying you back for money you’ve personally spent on legitimate business costs.

Getting this right is a game-changer. Every valid expense you claim directly reduces your company's declared profit. And a lower profit means a smaller Corporation Tax bill. It’s one of the simplest and most effective ways to make your entire operation more tax-efficient.

The Wholly and Exclusively Rule

Before you start tallying up receipts, you need to get your head around HMRC's golden rule: the 'wholly and exclusively' test. This is the bedrock of expense claims. It means an expense is only allowable if it was incurred purely for business purposes.

If an item has a dual purpose—partly for business, partly for personal use—it generally falls foul of the rule. For example, a new laptop you buy and use only for work? That’s a clear business expense. Your weekly supermarket shop, however, isn't, even if you grab a sandwich to eat at your desk. Understanding this distinction is absolutely key to staying on the right side of HMRC.

My Two Cents: Don't be shy about claiming what you're entitled to. The secret isn't in bending the rules, but in keeping flawless records. Seriously, get an app like Xero or QuickBooks. Snap a photo of every receipt the second you get it. This one habit can transform a year-end accounting headache into a simple, ongoing process.

What Can You Actually Claim?

The list of potential expenses is probably much longer than you think. As long as a cost passes that 'wholly and exclusively' test, there's a good chance you can claim it. Let's run through some of the most common ones I see with clients.

Here’s a quick look at some frequently claimed expenses to give you an idea of what’s possible.

| Expense Category | Examples and Key Considerations |

|---|---|

| Office Costs | Stationery, business postage, printer ink, and other day-to-day office supplies. |

| Travel & Subsistence | Train tickets, fuel (for business mileage in your own car), parking, and hotel stays for business trips. |

| Software & Subscriptions | Tools essential for your work, like Adobe Creative Suite, accounting software, or project management platforms. |

| Professional Fees | Your accountant's or solicitor's fees, plus memberships to professional bodies if they're required for your role. |

| Training & Development | The cost of courses or training that directly enhances the skills you need to run your business. |

| Marketing & Advertising | Website hosting, online ads, business cards, and other promotional costs. |

This is just a starting point. The government provides a very detailed A-to-Z list of expenses and benefits, which is an excellent resource to bookmark.

This official list on GOV.UK gives you clear, direct guidance from HMRC, helping you make the right call on what you can and can't claim.

What About Working From Home?

With so many directors now running their businesses from a home office, this is a big one. HMRC gives you two main ways to handle this.

The first is the easy route: a simplified flat rate. For the 2025/26 tax year, you can claim a flat £6 per week (£26 per month). It’s dead simple and doesn't require you to wade through your utility bills.

The second method involves a bit more legwork but can often result in a much larger claim. You can calculate a fair proportion of your actual household running costs. This means figuring out what percentage of your home you use for business (and for how long), then applying that to your gas, electricity, and even council tax bills. You'll need solid records to justify your calculations, but the payoff can be well worth it.

Ultimately, diligently claiming every single legitimate business expense is a non-negotiable part of paying yourself properly as a director. It ensures you’re not leaving money on the table and are running your company in the most tax-savvy way possible.

Your Guide to the Payment Process

Knowing the theory is one thing, but actually moving money from your company's bank account to your personal one is where it gets real. Let's walk through the practical steps to get this right, so you can build a solid, repeatable process that keeps you on the right side of HMRC and gives you complete financial clarity.

The very first thing you need to do before paying anyone a salary—including yourself—is to register your company as an employer with HMRC. This gets you set up with a PAYE (Pay As You Earn) scheme, which is the system the UK uses to handle Income Tax and National Insurance on employment income.

Once you're registered, you have a legal duty to report your salary payments to HMRC every single time you run payroll. This is done through a Real Time Information (RTI) submission, which typically happens on or before your payday each month. It’s a quick report that details your pay and any deductions, keeping HMRC in the loop.

Setting Up Your Salary Payments

Let's be honest, nobody wants to be doing tax and National Insurance calculations by hand. This is why most directors use payroll software. It automates all the tricky maths and generates the RTI file you need to send to HMRC. Getting into a smooth monthly routine is key here, as missing submissions can lead to penalties.

Your actual salary payment is just a simple bank transfer from your business account to your personal one. The crucial part is making sure the amount you transfer is the exact net pay figure shown on your payslip, after your payroll software has worked out any tax or NI deductions.

Seasoned UK directors have always tweaked their salaries to work with the ever-changing tax rules. For example, back in the 2022/23 tax year, a popular salary was £9,100, but by 2025/26, shifts in NIC thresholds and the Employment Allowance made £12,570 the go-to figure. This constant back-and-forth really shows why you need to stay on top of things. The government is always adjusting the tax landscape, which is why a hybrid salary-and-dividend strategy remains the most reliable approach for most small businesses.

The Mechanics of Issuing Dividends

Paying dividends involves a bit more paperwork, but it's just as important to get it right. Remember, dividends are a slice of your company's post-tax profits. You absolutely must have the figures to prove your company is in profit before you can even think about declaring one.

You need to create a proper paper trail for every dividend payment. This isn't just for your own records; it's a legal requirement that proves to HMRC that the payment is a legitimate dividend and not just you taking cash out of the company. Using good accounting software can make keeping these records accurate and straightforward.

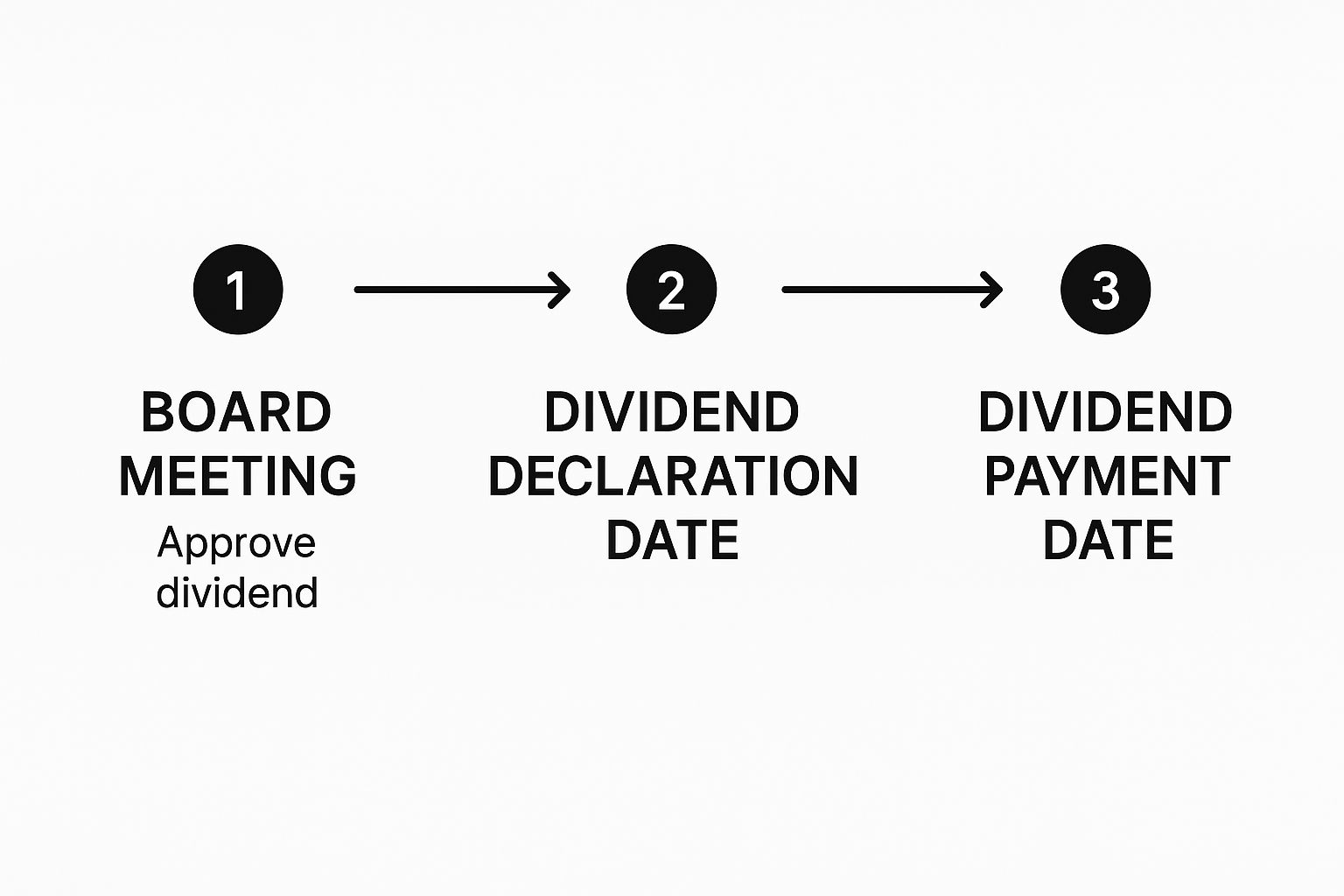

The image below breaks down the simple three-stage process for declaring and paying a dividend.

As you can see, it's a series of dated events that all need to be properly documented.

Here’s what you need to do:

- Hold a directors' meeting to officially declare the dividend. You have to record this decision in your company's meeting minutes.

- Create a dividend voucher for each shareholder. Think of this as a receipt. It must include key details like the date, company name, shareholder's name, and the dividend amount.

- Transfer the money. Once the paperwork is sorted, you can make the payment from the business account to the shareholders' personal bank accounts.

A Critical Reminder

I can't stress this enough: never mix your business and personal finances. Your limited company is a separate legal entity and must have its own bank account. Paying for your weekly shop from the business account or covering a business expense from your own pocket (without formally reclaiming it) will create an absolute mess for your accountant and can lead to serious tax headaches.

Timing Your Payments Strategically

When it comes to both salary and dividends, consistency is your friend. Most directors find a regular payment schedule helps with personal budgeting and keeps the bookkeeping nice and clean.

- Salary: This is nearly always paid monthly. It creates a predictable personal income and fits perfectly with standard payroll practices.

- Dividends: You can technically pay these whenever you like, as long as the company has enough profit. In practice, many directors take them quarterly or even annually, usually after looking at their management accounts to confirm the business can afford it.

By setting yourself up with a regular monthly salary and topping it up with periodic dividends, you create a payment system that is both structured and compliant. This methodical approach is the foundation of paying yourself correctly, turning complex tax rules into a clear, actionable routine you can rely on.

Common Questions About Director Pay

https://www.youtube.com/embed/2DK14i2fqKc

Even with the best strategy on paper, you're bound to have questions when it comes to the practicalities of paying yourself. Let's run through some of the most common queries I hear from directors. Getting these details right from the start will save you a world of headaches down the line.

Can I Just Take Money From the Business Account Whenever I Want?

Tempting as it may be, this is a hard no. It’s probably the single biggest mistake new directors make, and treating the company's bank account like your own personal piggy bank is a sure-fire way to get into hot water with HMRC.

Remember, your company is its own legal entity. Every single pound that leaves the business account must be properly accounted for. It can only be one of three things:

- A salary, run through a proper PAYE payroll scheme.

- A dividend, which must be formally declared from post-tax profits, complete with board minutes and a voucher.

- A reimbursement for a legitimate business expense you covered with your own money.

If you just pull cash out without categorising it, you create a Director's Loan. These come with their own complex tax rules and can lead to penalties if not repaid to the company within a strict timeframe. It's a mess you'll want to avoid.

What Happens if My Company Doesn't Make a Profit?

This is a crucial one, as it fundamentally changes your options. If your business hasn't made a profit after paying all its bills and taxes, then you cannot legally declare and pay any dividends.

It’s as simple as that. Dividends are a share of profits, so no profits means nothing to share. Paying one anyway is considered an 'illegal dividend,' and you'll be required to pay it back. You can, however, still pay yourself a salary through PAYE, as long as the company has the cash flow to support it.

Do I Need an Accountant to Manage Director Pay?

Technically, no. You could try to manage your own payroll, dividend paperwork, and tax filings. But I would strongly advise against it.

Tax legislation, National Insurance thresholds, and dividend allowances are constantly changing. A good accountant isn't just a number-cruncher; they're your guide to navigating this complex system and keeping you compliant.

An experienced accountant does more than just keep you out of trouble; they provide strategic advice. They'll help you fine-tune your payment mix as your business grows, ensuring you're always using the most tax-efficient structure. The money you save in tax and avoided penalties often far outweighs their fee.

How Do I Pay the Tax on My Dividends?

This often catches people out. Unlike your salary, where tax is neatly deducted at source through PAYE, dividend tax is entirely your personal responsibility. The company pays the dividend to you gross, without taking any tax off.

It's up to you to declare all of your dividend income on your annual Self-Assessment tax return. You’ll tell HMRC the total you received, and they will calculate the tax you owe based on your overall income and the dividend tax bands for that year. The key here is to be disciplined and set money aside as you receive dividends to cover that future tax bill.

Sorting out director pay can feel complicated, but you don't have to figure it all out on your own. At Stewart Accounting Services, we specialise in helping limited company directors build smart, tax-efficient payment strategies that grow with their business. Contact us today for a consultation and get the confidence that comes from knowing your finances are in expert hands.