Getting your head around how to pay yourself from a limited company might seem complex at first, but it really boils down to getting the right mix of salary and dividends. For most UK directors, the go-to, tax-smart strategy is to take a small salary and top it up with larger dividend payments. This method is popular for a good reason: it cleverly uses tax-free allowances and keeps National Insurance Contributions as low as possible.

Finding Your Ideal Pay Mix: Salary vs. Dividends

When you're running your own limited company, you're not just the boss—you're an employee and a shareholder too. This means you can't simply move cash from your business account to your personal one on a whim. Every penny you take out needs to be accounted for, usually as a salary, a dividend, or a legitimate expense reimbursement.

The two main ways to pay yourself are through a director's salary and shareholder dividends, and understanding the difference is crucial.

A salary is what you get for the work you do as a director. Your company pays this to you just like any other employee, and the great thing is that it's a business expense. This means it comes out before your company's Corporation Tax is worked out, effectively lowering your profit and your tax bill. Simple.

Dividends, on the other hand, are a share of the company's profits paid out to shareholders. The key difference is that they can only be paid from post-tax profits—that is, after the company has already paid Corporation Tax. Your company must have enough profit left over to cover any dividends you want to issue.

This fundamental distinction is precisely why mixing the two is almost always the best approach.

The Hybrid Approach: Getting the Best of Both Worlds

So, what does this look like in practice? Most sole directors find the sweet spot by paying themselves a small, tax-efficient salary and taking the rest of their income as dividends.

This hybrid model works so well because it plays to the strengths of each payment type. By setting your salary at just the right level, you can make sure you're still building up your qualifying years for the State Pension without actually paying much (or any) tax or National Insurance. It’s a win-win.

For the 2025/26 tax year, the magic number for a director's salary is often £12,570 per year (assuming you have no other sources of income). This figure sits perfectly at the threshold where you start paying tax (your Personal Allowance) and also aligns with the National Insurance primary threshold, making it incredibly efficient.

Anything you need above that amount can then be drawn down as dividends. Dividends come with their own £500 tax-free allowance and are taxed at much friendlier rates than salary income. If you're looking for a deeper dive into this, you can discover more insights about the optimal director's salary on pattersonhallaccountants.co.uk.

By blending a low salary with dividends, you can significantly increase your take-home pay compared to taking a straight salary of the same gross amount. This is the cornerstone of tax-efficient remuneration for limited company directors.

Let's quickly break down the core differences.

At a Glance: Salary vs. Dividends

This table gives a quick snapshot of the key characteristics of each payment method.

| Feature | Director's Salary | Director's Dividends |

|---|---|---|

| Tax Treatment (Company) | A business expense; reduces Corporation Tax. | Paid out of post-tax profits. |

| Tax Treatment (Personal) | Taxed via PAYE (Income Tax & National Insurance). | Taxed via Self Assessment; no National Insurance. |

| Tax-Free Allowance | Personal Allowance (£12,570). | Dividend Allowance (£500). |

| National Insurance | Both employee's and employer's NI apply above thresholds. | No NI contributions are due. |

| State Pension | Qualifies you for State Pension credits if above LEL. | Does not count towards State Pension. |

| Requirement | Must be registered as an employer with HMRC. | Company must have sufficient post-tax profits. |

As you can see, they both have their own pros and cons, which is why using them together is the smartest way to structure your pay.

Nailing the Perfect Director's Salary for Maximum Tax-Efficiency

When it comes to paying yourself, your director's salary is the foundation of a smart tax strategy. The goal isn’t to draw a huge salary; it’s about finding the 'sweet spot'. Think of it as the most efficient way to get your foot on the earnings ladder, minimising your tax and National Insurance (NI) burden while staying compliant with HMRC.

The secret lies in understanding the thresholds HMRC sets each year. These numbers aren't arbitrary—they're the triggers for when you start paying tax and NI. By cleverly aligning your salary with these figures, you can unlock some serious savings.

The Thresholds That Really Matter

For directors, there are two key numbers to watch: the Personal Allowance and the NI Primary Threshold. The Personal Allowance is what you can earn before paying a penny of Income Tax. The NI Primary Threshold is the point where you start paying employee's National Insurance.

Your aim is to set a salary that’s high enough to be recognised by the system but low enough to sidestep any hefty deductions. It's a bit of a balancing act, but it's where the magic really happens.

From my experience, the go-to strategy for most sole directors is to pay a salary that uses up the Personal Allowance without triggering any significant NI payments. This clever move ensures you're building qualifying years for your State Pension while keeping costs to an absolute minimum for both you and your company.

This low-salary, high-dividend approach is the cornerstone of tax-efficient remuneration. It effectively turns your salary into a tool for efficiency, leaving dividends to do the heavy lifting for your main income.

Finding Your Optimal Salary Figure

So, what's the magic number? For most directors, the optimal salary lines up perfectly with the NI thresholds. For the 2025/26 tax year, one of the most effective strategies is to set a salary right at the Personal Allowance, which also happens to be the NI Primary Threshold.

This means a sole director with no other income can set an annual salary of £12,570. That works out to a neat £1,047 per month. At this level, you pay zero Income Tax and zero employee's NI, but you still get the all-important NI credits towards your State Pension. For a more detailed look at how these figures are worked out, IT Contracting offers a great breakdown of the optimal salary for directors.

Why This £12,570 Figure is So Effective

Paying yourself exactly £12,570 is a popular strategy because it ticks all the right boxes:

- Zero Income Tax: Your entire salary is neatly covered by your tax-free Personal Allowance.

- No Employee's NI: The salary is set precisely at the NI Primary Threshold, meaning you don't pay any employee contributions.

- Qualifies for State Pension: It's above the Lower Earnings Limit (£6,396 for 2025/26), so you still earn a qualifying year towards your future State Pension.

- Reduces Your Corporation Tax Bill: Don't forget, your salary is a legitimate business expense. This reduces your company's taxable profit and, consequently, its Corporation Tax liability.

The only slight cost is a very small amount of employer's NI for the company to pay, as the salary just tips over the Secondary Threshold. However, this minor cost is almost always wiped out by the much larger Corporation Tax saving the salary creates. It's a highly beneficial trade-off that sets the perfect foundation for drawing the rest of your income through tax-efficient dividends.

Using Dividends to Maximise Your Earnings

Once you've sorted out your small, tax-efficient salary, dividends are where the real magic happens. This is your primary tool for drawing the rest of your income from the company. Think of the salary as covering your National Insurance contributions, and the dividends as the flexible, much more tax-friendly way to take home the bulk of the profits.

But it’s not a free-for-all. You can't just transfer money from the business account whenever you feel like it. There are strict rules to follow to keep everything above board with HMRC, and the biggest one is this: dividends can only be paid out of post-tax profits. In simple terms, your company has to have made enough profit after it has paid its Corporation Tax bill to cover the dividend you want to pay.

If you try to pay a dividend when the company doesn't have the profits to back it up, you’ve just paid an 'illegal dividend'. Trust me, that’s a headache you really want to avoid.

Getting the Dividend Paperwork Right

To pay a dividend legally, you need to create a paper trail. This involves holding a formal directors' meeting to declare the dividend and, crucially, keeping minutes of that meeting. Yes, even if you're the only director and the "meeting" is just you at your desk, this step is a non-negotiable legal requirement.

For every single dividend payment, you also need to issue a dividend voucher. It's a straightforward document, but an essential one. It needs to show:

- The date

- Your company's name

- The name(s) of the shareholder(s) getting paid

- The amount of the dividend

This paperwork proves the payment was a legitimate distribution of profit and not just you dipping into the company's cash.

Forgetting this paperwork is probably the most common slip-up I see from new company directors. Get into the habit of creating minutes and a voucher for every dividend payment. It creates a clean, clear record that will satisfy HMRC if they ever come knocking.

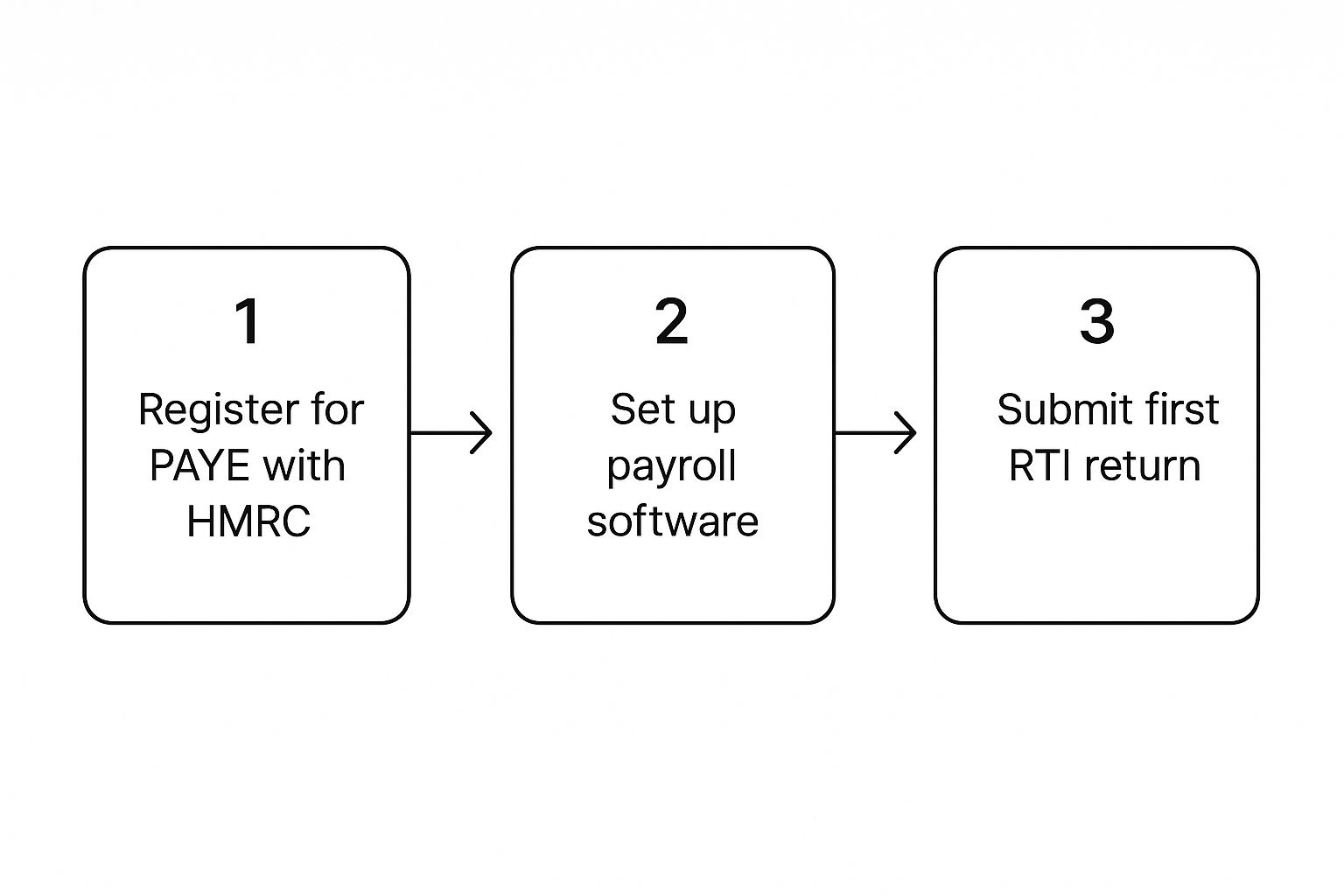

This whole process works hand-in-hand with your PAYE setup, which you need for your salary payments.

This flowchart gives you a simple overview of the basic steps involved in getting your company set up to pay a director’s salary through PAYE.

Understanding the Tax on Your Dividends

Here’s the big win with dividends: they are not subject to National Insurance. That’s a huge saving right there. They do have their own rates of tax, but these are much kinder than the standard income tax rates you pay on a salary.

For the 2025/26 tax year, everyone has a tax-free Dividend Allowance of £500. Any dividend income you take above this £500 will be taxed according to which income tax band you fall into.

Here are the dividend tax rates:

- 8.75% for basic-rate taxpayers

- 33.75% for higher-rate taxpayers

- 39.35% for additional-rate taxpayers

To figure out your tax band, you simply add your dividend income to your other income (like your director's salary). Let’s say you take a salary of £12,570 and dividends of £40,000. Your total income is £52,570. The basic rate band goes up to £50,270, so most of your dividends will be taxed at the lower 8.75% rate (after your allowance). This is the core of smart tax planning for a company director – balancing your salary and dividends to keep your personal tax bill as low as possible.

How National Insurance and Corporation Tax Shape Your Pay

When figuring out how to pay yourself from a limited company, you can't just look at your personal tax bill. You have to consider the taxes your business pays, too. The two big ones are National Insurance Contributions (NICs) and Corporation Tax, and they're completely interlinked.

Here’s the fundamental difference: your director's salary is a business expense. That means it gets deducted from your company's income before you calculate your profit, which in turn lowers your Corporation Tax bill. Dividends are different—they can only be paid out of profits after Corporation Tax has been taken care of.

This is the very heart of tax-efficient planning. A bigger salary means a bigger business expense, which reduces your Corporation Tax. But, push it too high, and you’ll start getting hit with both employee's and employer's National Insurance.

The Hidden Cost: Employer National Insurance

It’s easy to forget that it's not just your personal NI that gets deducted. Your company also has to pay employer’s NICs on top of your salary. This is an extra cost to the business, and it’s what makes large director salaries a pretty inefficient way to take money out of the company.

With recent tweaks to NI thresholds, this has become an even bigger deal, as the real cost of running a payroll has gone up for many small businesses. It's well worth reading the details on these director salary changes to see exactly how it might affect your own numbers.

The goal is to strike the right balance. You're looking for a salary that's high enough to count as a useful business expense but low enough to keep you clear of triggering hefty employer's National Insurance bills, which can wipe out any tax savings you've made.

This is why a particular government scheme often comes up in conversation.

What About the Employment Allowance?

You might have come across the Employment Allowance, a government scheme that can cut a company's employer NI bill. It sounds like a perfect solution, but there’s a major catch for most small business owners.

Unfortunately, the allowance isn't available for 'single-director' companies where that director is the only person on the payroll. This rule effectively excludes most freelancers, contractors, and consultants who run their own limited company, so you can't use it to cancel out your employer NICs.

While you're working out your personal pay, it's also a good time to remember the wider picture of general tax compliance considerations for businesses. Keeping everything above board is just good practice for the long haul.

Let's put this into a quick, practical example to see how it works.

Example Scenario

- Company Profit (before salary): £60,000

- Director's Salary: £12,570

- Remaining Profit: £47,430 (This is the figure now subject to Corporation Tax)

Just by paying that salary, the company’s taxable profit drops significantly. The small amount of employer's NI you might pay on that salary is almost always a drop in the ocean compared to the Corporation Tax you save. It’s a simple but incredibly effective strategy.

Other Smart Ways to Take Money from Your Company

While the salary and dividend combination is the bread and butter for most company directors, it’s certainly not the whole picture. There are a few other highly effective—and perfectly legitimate—ways to draw value from your business, each with its own benefits.

Thinking beyond the monthly payroll can open up some really significant tax savings. These aren’t loopholes; they're smart financial planning tools that every limited company director should be aware of. Let's look at how to build a more well-rounded approach to your remuneration.

Make Company Pension Contributions

This is a big one. Having your company pay directly into your personal pension is probably the most tax-efficient method available for extracting profit. Why? Because these payments are almost always treated as an allowable business expense.

This creates a brilliant double win. First, the contribution reduces your company's profit, which in turn lowers its Corporation Tax bill. Second, the money lands in your pension pot and grows tax-free, securing your future without creating a personal tax liability for you right now.

Unlike personal pension contributions that are limited by your salary, company contributions have a much more generous annual allowance—currently £60,000.

Paying into your pension from the business is arguably the single most tax-efficient way to move money from your company to yourself. It simultaneously lowers your company's tax bill and builds your long-term wealth, a combination that's hard to beat.

Directors can also look into setting up workplace pension schemes to further bolster their retirement savings in a tax-savvy way.

Use a Director's Loan Account

A director's loan is exactly what it sounds like: you borrow money from your company. It’s not a salary, dividend, or expense payment. It can offer some handy short-term flexibility, but you have to be incredibly careful with the rules.

The crucial deadline is that you must repay any loan to your company within 9 months and 1 day of your company's year-end. If you miss this, HMRC will hit the company with a hefty tax charge (known as a Section 455 charge) of 33.75% on whatever amount is still outstanding. While this tax is eventually refundable once the loan is paid back, it can cause a serious cash flow headache in the meantime.

My advice? Use this for genuine short-term needs only, not as a way to take a regular income.

Claim All Legitimate Business Expenses

Finally, don't forget the basics. The simplest way to take money out of your company tax-free is by reimbursing yourself for every single legitimate business expense you incur personally. If you've paid for something solely for the purpose of your business, you can claim that money back.

This can cover a surprisingly wide range of things:

- Travel and accommodation for business meetings or site visits.

- Software subscriptions, stationery, and other essential office supplies.

- Use of your home as an office, which can be claimed either as a flat rate or by calculating a proportion of your actual household bills.

Get into the habit of tracking these expenses diligently. It’s a simple but effective way to make sure you’re not paying for business costs out of your own taxed income. Every pound you reclaim is a pound you don't have to pay tax on.

Frequently Asked Questions About Director Pay

https://www.youtube.com/embed/9a6TzImev2c

Figuring out the best way to pay yourself as a director can feel like walking a tightrope. You’re trying to balance taking home as much as you can with keeping everything above board for HMRC. It’s a common challenge, so let's break down some of the questions I hear all the time from directors.

Getting your pay structure right from the start saves a lot of headaches down the line. One of the first things people wonder is whether they can just skip a salary entirely and live off dividends. It sounds simple, but it's usually not the smartest move.

Can I Pay Myself Only in Dividends?

While you can pay yourself exclusively through dividends, it’s rarely the best strategy. The main reason comes down to National Insurance.

Taking only dividends means you're not making any National Insurance contributions (NICs). That might seem like a clever tax-saving trick, but it has a massive sting in the tail: your State Pension. To get the full State Pension in retirement, you need to have 35 "qualifying years" of NICs under your belt.

By paying yourself a small salary above the Lower Earnings Limit (which is £6,396 for the 2025/26 tax year), you automatically earn a qualifying year towards your pension, often without actually paying any NI. It’s a crucial box to tick for your future, and one you'll miss out on if you rely solely on dividends.

How Often Should I Pay Dividends?

This is where you get some real flexibility. Unlike a rigid monthly salary, there's no set rule for how often you can take a dividend. You could do it monthly, quarterly, or just once a year—it all depends on your personal cash flow needs and, just as importantly, your company's performance.

Many directors I work with opt for a monthly dividend to give themselves a steady, predictable income, much like a regular paycheque. Others prefer to take larger lump sums when the business has had a great quarter.

The key thing to remember is that you absolutely must follow the proper procedure for every single payment. That means holding a board meeting (even if it's just you), documenting the decision in the minutes, and issuing a dividend voucher.

Skipping this paperwork is a surprisingly common mistake, but it's a red flag for HMRC and can cause serious compliance issues. It's not just bureaucratic fluff; it's the legal proof that the payment is a legitimate distribution of profit.

What If My Company Has No Profits?

This is a big one, and getting it wrong can land you in hot water. Dividends can only be paid out of post-tax profits. If your company hasn't made a profit, you simply can't declare a dividend.

If you take money from the business when there are no retained profits to cover it, that payment is classed as an ‘illegal dividend’.

HMRC takes this very seriously. They will reclassify the payment, usually as a director's loan, which you then have to repay to the company. If you don't repay it quickly, both you and your business could face hefty tax penalties.

The takeaway here is simple: always check your management accounts before you even think about declaring a dividend. Make sure the retained profits are there to cover it. If you're ever unsure, it’s far better to be cautious and speak with your accountant first.

At Stewart Accounting Services, we guide business owners across Central Scotland and the UK through these decisions every day. If you need a hand setting up a tax-efficient pay structure or just want peace of mind that you're staying compliant, get in touch with our team of Chartered Accountants.