Before you can even think about pulling together your final accounts, you need to get the groundwork right. The whole process hinges on having a solid, organised foundation, which comes from consistent and accurate bookkeeping.

Think of it as the bedrock for your entire financial reporting structure. If there are any cracks here, they’ll absolutely show up in your final statements, guaranteed.

Building a Solid Foundation for Financial Reporting

Reliable bookkeeping isn’t just about ticking a compliance box. It’s the day-in, day-out discipline of recording every single financial transaction your business makes. Get this right, and everything that follows becomes so much smoother.

Let’s take a small UK e-commerce business as an example. Good bookkeeping for them means meticulously tracking:

- Every single sale, whether it’s through their website or a marketplace like Etsy.

- The cost of the goods they’ve sold (their COGS) for each dispatched order.

- All the operational expenses—from the monthly Shopify fee to the Facebook ad spend.

- The VAT they’ve collected on sales and paid out on their business purchases.

When all this data is captured correctly throughout the year, you’re in a great position for the next stage.

Preparing the Trial Balance

The trial balance is the first major milestone on the road to producing your financial statements. It’s essentially an internal report, a big list of every single account in your general ledger and its final balance at the end of your accounting period.

Its main job? To prove that your debits and credits match up. This is the heart of double-entry bookkeeping, where every transaction has two sides. For instance, when that e-commerce business makes a £100 sale on credit:

- Its Accounts Receivable (an asset) goes up by £100 (a debit).

- Its Sales Revenue (income) also goes up by £100 (a credit).

A perfectly balanced trial balance, where the total of the debit column equals the total of the credit column, is your green light. It gives you confidence that your bookkeeping is mathematically sound. It won’t tell you if you’ve put an expense in the wrong category, but it confirms the fundamental accounting equation is holding up.

What Your Trial Balance Tells You

If your trial balance doesn’t balance, that’s an immediate red flag. Stop everything. It’s a clear signal that there’s an error hiding somewhere in your books, and you have to find it before you can move on. The usual suspects are simple transposition errors (writing £54 instead of £45) or accidentally posting a debit as a credit.

On the other hand, a balanced trial balance provides the clean, verified data you need to start building the reports. Each account on that list has a destination. Your revenue and expense accounts will feed directly into the Profit and Loss Account, while your assets, liabilities, and equity accounts are the building blocks for your Balance Sheet.

These accounts are all organised according to a structured list. If you want to get a better handle on how to create one for your own business, have a look at our detailed guide on what is a chart of accounts here: https://stewartaccounting.co.uk/what-is-a-chart-of-accounts/. This organised list is the starting point for creating a true and fair picture of your company’s financial health.

Before diving deeper into the process, let’s quickly summarise the three core statements you’ll be creating.

The Three Core Financial Statements

This table offers a quick overview of the primary financial statements and the essential insights each provides for a UK business.

| Statement Type | What It Reveals | Key Questions It Answers |

|---|---|---|

| Profit & Loss Account | The company’s financial performance over a specific period (e.g., a year or quarter). | “Did we make a profit?” “How much revenue did we generate?” “What were our biggest expenses?” |

| Balance Sheet | A snapshot of the company’s financial position at a single point in time. | “What does the company own and owe?” “How much equity do the shareholders have?” |

| Cash Flow Statement | How cash has moved in and out of the business from operating, investing, and financing activities. | “Where did our cash come from?” “Where did our cash go?” “Is the business generating enough cash to survive?” |

Each of these statements tells a different part of your business’s story. Together, they give you—and stakeholders like investors or HMRC—a complete and transparent view.

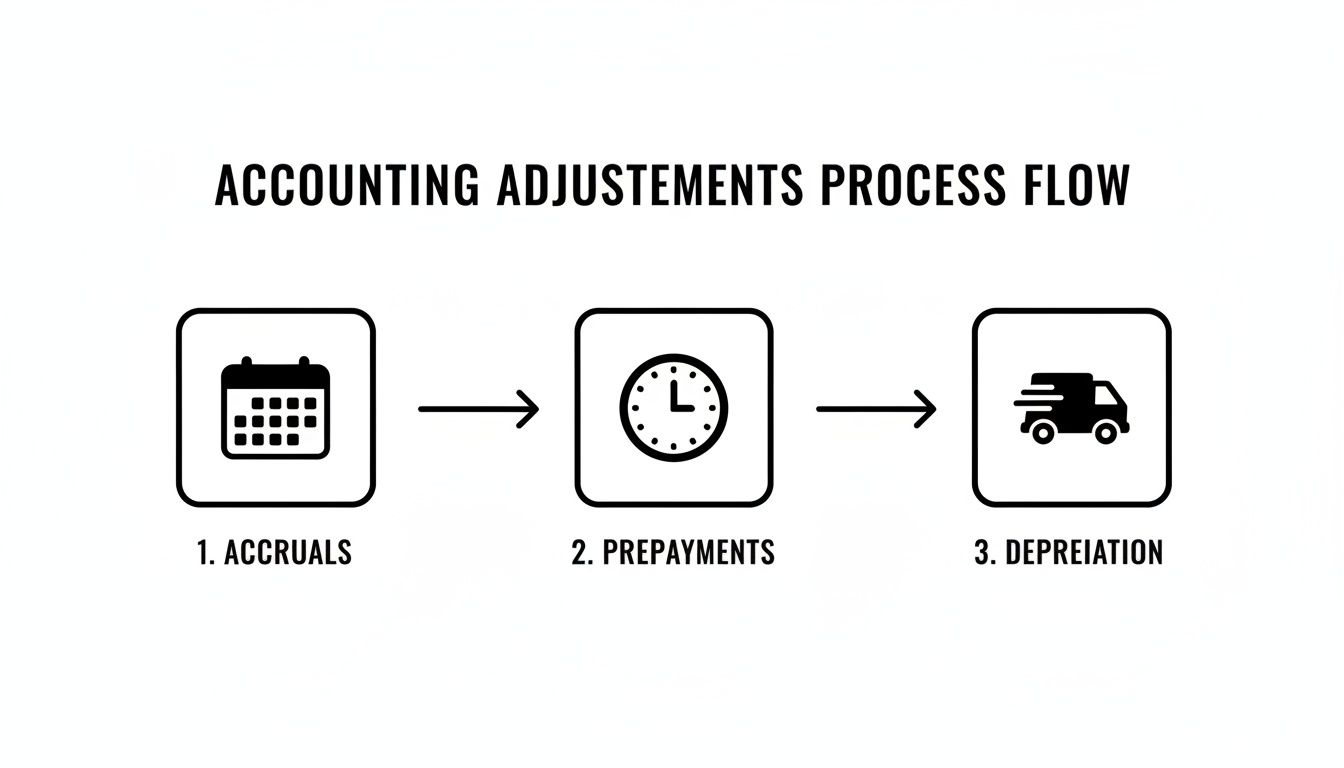

Getting the Adjustments Right for a True Financial Picture

Your initial trial balance might be perfectly balanced, but it rarely tells the whole story. Think of it as a raw draft. It’s a simple record of cash in and cash out, which doesn’t quite capture the economic reality of when you actually earned revenue or incurred expenses.

This is where year-end adjustments are so important. They’re the essential tweaks that transform those raw numbers into a “true and fair” view of your business’s performance. Getting these right is the difference between a basic cash summary and a professional set of accounts that meet UK standards.

Matching Timing with Accruals and Prepayments

The most common adjustments you’ll make deal with timing. Cash doesn’t always change hands at the same time a service is delivered, and this is where accruals and prepayments come into play.

- Accrued Revenue: This is income you’ve earned but haven’t yet been paid for by your year-end. Say your consultancy finishes a big project worth £5,000 in the last week of December, but you don’t send the invoice until January. Without an adjustment, that £5,000 would wrongly show up in the next financial year. You need a journal entry to recognise it in December, where it belongs.

- Prepayments: This is the other side of the coin. It’s when you pay for something upfront but haven’t used the full benefit yet. The classic example is your annual business insurance. If you pay £1,200 in January for a full year of cover, you can’t just expense the whole lot at once. That would artificially squash your January profits. Instead, you recognise £100 of the cost each month.

Getting your head around these concepts is fundamental to accurate reporting. If you need a refresher, you can learn more about what accrual accounting is and why it’s so critical for your business.

Don’t think of these as optional tweaks. They are a core requirement under UK accounting standards. The whole point is to make sure your Profit and Loss account accurately reflects the profitability of the specific period you’re reporting on.

Modern accounting software like Xero makes tracking these items much less of a headache. The dashboard gives you a live overview, which helps you spot where adjustments might be needed.

Having this kind of real-time data makes managing month-end or year-end adjustments far more systematic.

Accounting for Wear and Tear with Depreciation

Your long-term assets—vehicles, machinery, computers—all lose value over time. We call this loss in value depreciation, and it’s a non-cash expense that absolutely must be recorded. If you skip it, you’re overstating your profits and the value of your assets on the balance sheet.

This isn’t just a formality for small businesses. Even government bodies track it meticulously. For the year ending 31 March 2024, the UK Statistics Authority reported buildings valued at £12,449,000 and computers at £7,831,000. They then recorded depreciation charges of £5,729,000 on the buildings and £207,000 on the computer equipment. It shows just how seriously this is taken at every level.

You generally have two ways to calculate this:

- The Straight-Line Method: This is the simplest way. You just spread the asset’s cost evenly over its useful life. For example, if your company buys a van for £25,000 and you expect to use it for five years before selling it for £5,000, your annual depreciation is straightforward: (£25,000 – £5,000) / 5 = £4,000 a year.

- The Reducing Balance Method: This approach applies a fixed percentage to the asset’s carrying value each year. This means you have higher depreciation charges in the early years and lower ones later on. It’s often a more realistic reflection for assets that lose value quickly, like tech hardware.

Whichever method you pick, the key is to be consistent. You’ll also need to disclose your policy in the notes to the financial statements, so anyone reading them can understand exactly how you’ve valued your assets. By diligently applying these adjustments, you move beyond simple bookkeeping and create financial statements that truly represent your business.

Assembling Your Key Financial Statements

With your trial balance tweaked and polished, it’s time for the main event: putting together the core financial statements. This is where all your careful record-keeping and adjustments finally come together to tell the financial story of your business. It’s a satisfying process, and it’s sequential—the numbers from one statement feed directly into the next.

To make this real, let’s follow the journey of a small UK-based online retail business. Using one consistent example will make it much clearer how the numbers connect and flow between the statements.

Crafting the Profit and Loss Account

First up is the Profit and Loss (P&L) account, which you might also know as the Income Statement. Its job is simple: to show how your company performed financially over a specific period. It answers the one question every business owner wants to know: “Did we actually make a profit?”

You’ll be pulling all the revenue and expense account balances straight from your adjusted trial balance. The logic flows naturally from top to bottom.

Let’s say our online retailer had a total revenue of £150,000 from their website and various marketplaces.

Next, you have to account for the direct costs of making those sales, known as the Cost of Goods Sold (COGS). For our retailer, this is the cost of the products they sold, plus any packaging and shipping. We’ll put this at £60,000.

Subtracting COGS from revenue gives you the Gross Profit. In this case, that’s £150,000 – £60,000, leaving a healthy £90,000. This figure is a great indicator of how efficiently you’re making and selling your products, before factoring in overheads.

Now for the Operating Expenses – all the other costs of keeping the lights on. This bucket includes everything from marketing spend and warehouse rent to software subscriptions, salaries, and that depreciation charge we calculated earlier. Let’s say these add up to £55,000.

Finally, you arrive at the Net Profit. By subtracting operating expenses from the gross profit (£90,000 – £55,000), our retailer’s net profit is £35,000. This is the famous ‘bottom line’, the true profit after every single cost has been accounted for.

Don’t just see this Net Profit figure as the end of the P&L. It’s a vital number you’ll carry directly over to the Balance Sheet. In accounting, everything is connected.

The adjustments we made earlier for things like accruals, prepayments, and depreciation are what make the expense figures on your P&L truly accurate.

As this visual shows, these tweaks are all about matching income and expenses to the right accounting period, giving you a proper measure of your profitability for the year.

Constructing a Balanced Balance Sheet

Next on the list is the Balance Sheet. While the P&L covers a period of time, the Balance Sheet is a snapshot of your company’s financial health on a single day—usually the last day of your financial year. It’s governed by one non-negotiable rule, the fundamental accounting equation:

Assets = Liabilities + Equity

Put simply, what your business owns (assets) must equal what it owes (liabilities) plus what’s left for the owners (equity).

To build it, you’re once again dipping into your adjusted trial balance for the figures:

- Assets: List everything the business owns. This is usually split into Current Assets (cash, money owed by customers, stock) and Fixed Assets (property, equipment, vehicles).

- Liabilities: Here you list all your debts. Similarly, they are broken down into Current Liabilities (money owed to suppliers, short-term loans, VAT) and Long-Term Liabilities (bank loans due in more than a year).

- Equity: This part includes the initial investment (share capital) plus retained earnings. Retained earnings are the accumulated profits from all previous years, topped up with the £35,000 net profit you just calculated on the P&L.

Once you’ve slotted everything in, the two sides must balance to the penny. If they don’t, it’s a red flag. It means there’s a mistake somewhere in your bookkeeping that you need to hunt down and fix before going any further.

Understanding the Statement of Cash Flows

The last of the big three statements is the Statement of Cash Flows. This report is incredibly important because, as many have learned the hard way, profit and cash are two very different things. A company can look profitable on paper but go under if cash runs dry because customers aren’t paying their bills.

This statement tracks the actual movement of cash through three main activities:

- Operating Activities: This shows the cash that came in and went out from your core business operations. You start with net profit and then adjust for non-cash items (like depreciation) and shifts in working capital (like buying more stock or customers taking longer to pay).

- Investing Activities: This section details cash spent on or received from selling long-term assets. Did you buy a new laptop or van? That cash outflow goes here. Did you sell some old machinery? The cash inflow is an investing activity.

- Financing Activities: This covers cash related to how the business is funded. It includes money from a new bank loan, cash used to repay old loans, or dividends paid out to shareholders.

When you add up the cash changes from these three areas and apply them to your opening cash balance, you get your closing cash balance. And here’s the final check: this number must perfectly match the cash figure shown on your Balance Sheet. For help with forecasting, using some sample cash flow projections can be a massive help.

Getting Your Accounts Filed in the UK

Once you’ve put in the hard work to get your financial statements prepared and polished, the final hurdle is getting them filed correctly with the UK authorities. This isn’t just a box-ticking exercise; it’s a legal requirement. Getting it wrong, or missing a deadline, can lead to some painful penalties.

For any UK limited company, you have two masters to serve: Companies House and HM Revenue & Customs (HMRC). While you’re using the same core financial data, what you send to each of them is a bit different. HMRC needs your full, detailed accounts to figure out your Corporation Tax bill. Companies House, on the other hand, is all about public record and transparency, so depending on your company’s size, you can often file a much simpler, stripped-back version of your accounts with them.

Does Size Matter? Yes, It Does.

The level of detail you need to publish in your accounts really boils down to the size of your company. UK regulations are designed to ease the administrative burden on smaller businesses, so understanding which category you fall into is the first step towards getting your filing right.

The good news is that the rules are quite clear. You just need to meet at least two of the three criteria for your size category.

Here’s a look at the current thresholds that determine whether a company is classed as a micro, small, or medium-sized entity.

UK Company Size Thresholds for Financial Reporting

| Criteria | Micro-entity | Small Company | Medium-sized Company |

|---|---|---|---|

| Turnover | Not more than £632,000 | Not more than £10.2 million | Not more than £36 million |

| Balance Sheet Total | Not more than £316,000 | Not more than £5.1 million | Not more than £18 million |

| Average Employees | Not more than 10 | Not more than 50 | Not more than 250 |

As you can see, the requirements scale up significantly. For instance, a micro-entity can get away with filing the bare minimum—often just a balance sheet with a few notes, skipping the Profit & Loss account and director’s report entirely. Small companies have a bit more to disclose but can still file ‘filleted’ or abridged accounts, which is a great way to keep sensitive performance figures off the public register.

The Inevitable Move to Digital-Only Filing

The days of printing out your accounts and popping them in the post are long gone. Both Companies House and HMRC now insist on digital filing. It’s a move that has standardised the whole process, making it far more efficient and, frankly, a lot harder to mess up.

The numbers speak for themselves. As of March 2025, the annual accounts filing rate for UK companies reached a staggering 98.5%, a figure driven almost entirely by how easy digital submission has become. This digital-first world was cemented in early 2025 with new rules requiring complex accounts to be filed through approved software. The sheer scale is mind-boggling, with Companies House processing 13.5 million digital filings in the 2024–2025 period. You can read more about it in the official Companies House annual report.

This isn’t just about ticking a compliance box; it’s about making your life easier. Using cloud accounting software that plugs directly into government gateways transforms what was once a painful, time-consuming task into a few clicks. It massively cuts the risk of typos and late filings.

Modern accounting platforms like Xero or QuickBooks are built for this. They automatically generate compliant accounts based on the right framework (like FRS 105 for micro-entities or FRS 102 for small companies) and often let you file directly from the software itself. It’s a game-changer.

Don’t Miss These Deadlines

Missing a filing deadline is an expensive and completely avoidable mistake. Pop these dates in your calendar right now—they are non-negotiable.

Here’s what you absolutely need to remember:

- Filing with Companies House: Your first set of accounts are due 21 months after the date you incorporated your company. After that, it’s 9 months after your company’s financial year-end, every year.

- Paying Corporation Tax to HMRC: Your payment is due 9 months and one day after your accounting period ends. No excuses.

- Filing your Company Tax Return (CT600) with HMRC: You have 12 months after your accounting period ends to file this. Yes, that’s right—the deadline to file the return is after the deadline to pay the tax.

To get this done, you’ll need your complete financial statements—the P&L, balance sheet, and all the relevant notes. If you’re feeling unsure about the process, our guide on how to submit company accounts breaks it down step-by-step. Getting this final piece of the puzzle right gives you the peace of mind that your business is fully compliant and in good standing.

Your Final Review Checklist to Avoid Common Errors

Before you even think about hitting ‘submit’, it’s time for one last, thorough look-over. This final check is your best defence against those small oversights that can cause big headaches later on, from rejected filings to painful tax recalculations.

Think of it as proofreading your numbers. You’re not just ticking boxes; you’re looking for consistency, accuracy, and anything that just doesn’t feel right. This is about making sure the story your accounts tell is the true one.

Checking for Internal Consistency

The three core financial statements are all linked. A change in one should create a predictable ripple effect across the others. Your first job is to make sure those connections are solid.

A classic check is the bridge between your Profit and Loss account and your Balance Sheet. The net profit figure at the bottom of the P&L needs to perfectly match the increase in retained earnings shown in the equity section of your Balance Sheet. If it doesn’t, something’s amiss.

Likewise, the closing cash balance on your Statement of Cash Flows must equal the cash figure listed under Current Assets on the Balance Sheet. This is a non-negotiable check. It’s the ultimate confirmation that you’ve tracked every penny correctly.

Scrutinising Common Pitfall Areas

From experience, I can tell you that certain accounts are magnets for errors. It’s worth spending a little extra time here, as a mistake in one of these spots can throw everything else off.

Zero in on these key areas:

- Bank Reconciliation: Does the cash balance in your ledger match your final bank statement for the period? Unreconciled differences often hide missed transactions or even bank errors.

- Inventory Valuation: Have you stuck to a consistent method (like FIFO or weighted average cost)? More importantly, have you checked for obsolete stock that needs writing down? Overvaluing inventory gives you a false sense of security by inflating both your assets and your profit.

- Expense Classification: Just scan your expense categories. It’s surprisingly easy to misclassify a big capital purchase as a day-to-day expense, which tanks your profit and understates your assets on the Balance Sheet.

- Accruals and Prepayments: Go back and double-check that every single year-end adjustment has been posted correctly. Missing an accrual for a hefty expense that’s been incurred but not yet invoiced is probably one of the most common errors I see.

The real goal of this final check is to ensure that every figure can be backed up. You should be able to trace any number back to its source—an invoice, a bank transaction, or a calculation schedule. This creates an audit trail that gives you, and any external reviewer, complete confidence in the accounts.

Aligning with UK Reporting Frameworks

Finally, make sure your statements meet the right UK reporting standards for your company’s size. Many small and medium-sized businesses can use simplified reporting frameworks, which is a huge advantage.

In fact, estimates suggest that around 133,000 UK companies could reclassify to less stringent reporting categories, such as a small company moving to micro-entity status. This lets them prepare much simpler financial statements, which can seriously reduce compliance costs. You can find more insights on UK government SME support on publishing.service.gov.uk.

Your review should confirm you’ve applied the right framework—like FRS 105 for micro-entities or FRS 102 for small businesses—and included all the necessary disclosures. This final step ensures all your hard work pays off with a fully compliant, accurate set of accounts.

Common Questions About Preparing Financial Statements

Even with the best guide, a few questions always seem to crop up, especially when you’re getting to grips with financial statements for the first time. Let’s tackle some of the most common ones head-on.

How Often Should I Prepare Financial Statements?

While the legal deadline for Companies House is just once a year, you’re flying blind if you wait that long. Best practice is to get your management accounts in order far more frequently.

Ideally, you should be looking at a Profit & Loss and Balance Sheet every single month. A quarterly review is the absolute minimum. This regular rhythm keeps your finger on the pulse of the business, helping you manage cash flow, spot trends, and make smart decisions with current information. It also transforms the year-end scramble into a straightforward final review.

Can I Prepare My Own Financial Statements?

Absolutely. If you run a small company with relatively simple operations, you can definitely prepare your own accounts. Modern cloud accounting software from providers like Xero or QuickBooks is built to make this as painless as possible, automating much of the heavy lifting.

However, the moment things get more complex—perhaps you’re dealing with different currencies, share options, or complicated loans—it’s time to bring in a professional. A good accountant ensures everything is accurate and compliant with the latest standards (like FRS 102), but their real value goes much deeper.

An accountant doesn’t just prepare the statements; they interpret them. They help you read the story the numbers are telling, spot opportunities you might have missed, and flag risks before they escalate into major problems.

What Is the Difference Between Cash and Accrual Accounting?

The crucial difference between cash and accrual accounting boils down to one word: timing.

- Cash Accounting: This is the simple approach. You only record income and expenses when cash physically moves in or out of your bank account.

- Accrual Accounting: This method records income when it’s earned and expenses when they’re incurred, no matter when the money actually changes hands.

Most UK limited companies must use the accrual method. Why? Because it gives a much truer picture of your company’s financial health over a period, matching the income you’ve generated with the costs you incurred to earn it. That’s the bedrock of solid financial reporting.

Are Notes to the Financial Statements Really Mandatory?

Yes, they are. Under UK accounting standards, the notes aren’t just an appendix; they are a fundamental part of the financial statements. They provide the context that the numbers alone on the P&L and Balance Sheet simply can’t.

Think of them as the director’s commentary. These notes typically explain:

- Accounting policies: The specific rules you’ve followed, like how you calculate depreciation on your assets.

- Figure breakdowns: More granular detail on broad categories, such as a full list of fixed assets or a breakdown of who you owe money to (creditors).

- Important disclosures: Information that isn’t on the balance sheet itself, like potential legal liabilities or transactions with directors.

Even though micro and small companies can file “abridged” accounts with fewer disclosures, some notes are still essential to stay compliant.

Getting your financial statements right—and filed on time—can feel like a lot to handle. At Stewart Accounting Services, we take the entire process off your plate, ensuring your accounts are accurate, compliant, and always on schedule. Find out how we can give you more time, more money, and a clearer mind by visiting our website.