So, you’re ready to take the plunge into self-employment. It’s an exciting step, but one of the first bits of admin you can't ignore is letting HMRC know what you're up to. Officially, this is called registering as a sole trader, and it's how you get set up to handle your own taxes through Self Assessment.

The process itself is pretty straightforward, but the deadlines are what catch people out. You need to register online within three months of starting your business, and crucially, before the 5th of October in your business's second tax year.

Your First Steps to Becoming a Sole Trader

Deciding to be your own boss means joining a huge and vital part of the UK economy. In the third quarter of 2025, there were around 4.39 million of us, making up about 13.5% of the entire workforce. The importance of being officially on the books was thrown into sharp relief during the pandemic; the government's Self-Employment Income Support Scheme (SEISS) saw 2.7 million claims in its first round alone, a lifeline only available to those who were properly registered.

The big question is, when do you actually need to register? The rule is simple: if you earn more than £1,000 from your self-employed activities in a single tax year (which runs from 6th April to 5th April), you must tell HMRC. And remember, that’s based on your gross income—the total amount you've billed—not your profit.

Nailing Down Your Start Date

Your "start date" is a key piece of information, but it's not always the day you got your first payment. Think of it as the day your business activities officially began. This could be when you bought your first bit of essential kit, paid for your business website to go live, or started actively marketing your services.

For instance, imagine a freelance photographer buys a new camera and lenses on 15th August specifically for their new business venture. That becomes their official start date, even if their first paid photoshoot isn't until September. Getting this date right is crucial because it locks in the start of your first tax year.

A Crucial Point: You are legally operating as a sole trader from the moment you begin your business activities. The registration process is simply you notifying HMRC of this fact. It’s an essential step that underpins everything from paying the right tax and National Insurance to being able to apply for a mortgage.

Getting Your Details in Order

Before you dive into the online registration form, do yourself a favour and get all your information ready. A little prep here saves a lot of hassle later.

You'll need a few bits and pieces to hand:

- Personal Info: Your full name, date of birth, current address, and of course, your National Insurance number.

- Business Info: The date you started trading (as we just discussed), the name you'll be trading under (which can be your own name or a specific business name), and a clear description of what your business actually does.

Having these details ready makes the whole process quick and painless. If you want a heads-up on what happens next, take a look at our article on what to be aware of if you are self-employed.

Key Deadlines and Thresholds for New Sole Traders

To help you stay on the right side of HMRC, it's worth keeping a few key dates and figures in mind. This table breaks down the essentials you'll need to remember as you get started.

| Requirement | Deadline / Threshold | What This Means For You |

|---|---|---|

| Register for Self Assessment | 5th October after the end of the tax year in which you started trading. | If you started your business in the 2024/25 tax year, you must register by 5th October 2025. Don't miss this! |

| Trading Allowance | £1,000 gross income per tax year. | If your total earnings from self-employment are below this, you don't need to register or file a tax return. |

| Online Tax Return Filing | 31st January following the end of the tax year. | For the 2024/25 tax year, your tax return is due online by 31st January 2026. |

| Tax Payment Deadline | 31st January following the end of the tax year. | Your tax bill for the 2024/25 tax year must also be paid by 31st January 2026. |

Getting these dates in your diary from day one is one of the best habits you can form as a new business owner. It prevents last-minute panic and ensures you avoid any potential penalties.

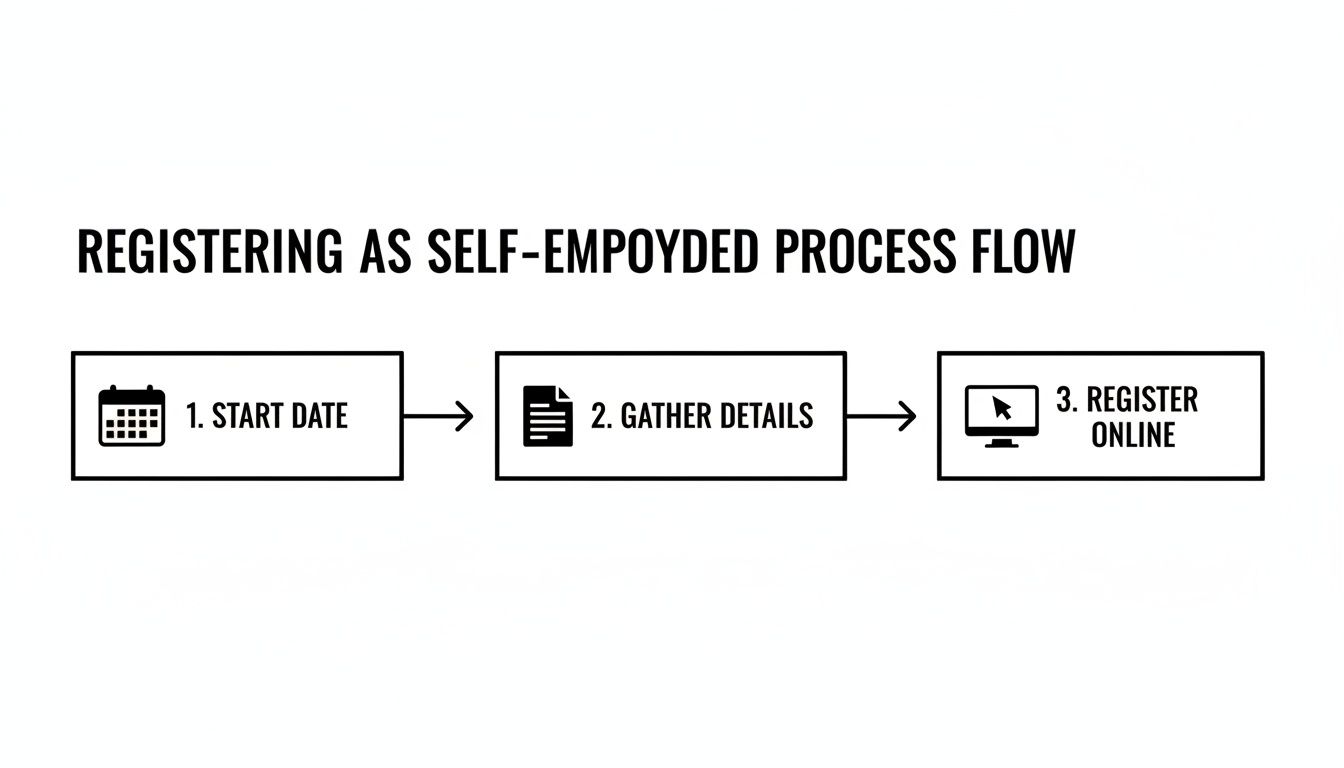

How to Register as Self-Employed with HMRC

So, you’ve pinpointed your start date and have all your details handy. Now for the main event: telling HMRC you’re officially in business. It can sound a bit daunting, but honestly, it's a straightforward online process. Think of it less like a bureaucratic headache and more like putting your new venture on the map.

This little flow chart breaks it down into the three core actions you'll need to take.

As you can see, it’s a pretty logical path. The single biggest takeaway I can give you from years of experience is that getting your documents ready beforehand makes the actual online bit a breeze.

Kicking Off the Online Form

First things first, you'll need a Government Gateway user ID. If you've never filed a tax return online before, you’ll need to create one. This is your secure key to the HMRC kingdom—you'll use it for everything from filing returns to checking your National Insurance record, so keep those login details somewhere very safe.

Once you’re in, the form will ask for all the information you’ve just gathered: your name, address, National Insurance number, and that all-important start date. It’s essentially a data-entry task, but double-check everything for typos. A simple mistake here can cause unnecessary delays down the line.

What’s in a Name? Choosing Your Business Name

As a sole trader, you can either use your own name (like ‘John Smith, Plumber’) or come up with a separate trading name (e.g., ‘Pro-Plumb Solutions’). While you have a lot of freedom, there are a few ground rules to be aware of.

Your name can't:

- Include terms like ‘Limited’, ‘Ltd’, ‘LLP’, or ‘PLC’. These are reserved for specific legal business structures that you, as a sole trader, are not.

- Contain offensive or sensitive words.

- Be identical to an existing trade mark. It's always worth a quick search to avoid any legal issues later.

A practical tip from me: before you settle on a name, check if the website domain and social media handles are free. Snagging them early on helps you build a consistent brand right from the start.

Describing What You Actually Do

The form asks for a description of your business. You don't need to write a novel, but "consultant" or "freelancer" is just too vague. You need to be specific enough for HMRC to understand your line of work.

For instance, instead of “IT services,” try “Providing IT support and network installation for small businesses.” Instead of “creative work,” go for something like “Freelance graphic design and branding services.” This helps HMRC categorise your business correctly.

A Quick Tip from Experience: Your business description isn't set in stone. Many businesses evolve. You might start out as a copywriter and later branch into social media management. You can always update your details with HMRC. The important thing is that the description is accurate when you register.

Don't Sweat the Turnover Estimate

HMRC will ask for an estimate of your annual turnover. This throws a lot of people, but please don't panic about it. This isn't a binding contract; it’s a ballpark figure they use for their own statistics.

If you’re just starting out, a good faith guess based on your initial contracts or projections is absolutely fine. It doesn't directly impact the tax you'll pay right now—that will be based on your actual income, which you’ll report on your tax return. For more on that, you can check out our guide on who must send in a tax return.

The Final Click and Getting Your UTR

Once you’ve filled everything in and given it a final once-over, hit submit. And that’s it – your part is done.

In about 10 to 21 working days, a letter from HMRC will land on your doormat. Inside, you’ll find your Unique Taxpayer Reference (UTR). This 10-digit number is incredibly important; it’s how HMRC identifies you in the Self Assessment system.

You’ll need your UTR number for just about everything tax-related:

- Filing your annual tax return.

- Speaking to HMRC about your business.

- Giving an accountant, like us at Stewart Accounting Services, permission to handle your tax affairs.

When that letter arrives, you are officially registered as self-employed. Find a safe place for it, because you'll need that UTR every single year. Now, the focus shifts from getting registered to getting organised, which is the foundation of any successful business.

Getting to Grips with Tax and National Insurance

So, you’ve officially registered as a sole trader. That’s a huge first step, but it’s really the start line, not the finish. Now, your focus needs to shift to the money side of things—specifically, getting your head around the tax and National Insurance (NI) that comes with being your own boss.

It might feel a bit daunting at first, but getting this right from day one will save you a world of headaches down the line. As a self-employed person, you're responsible for paying Income Tax on your profits and making your own National Insurance contributions. For a sole trader, this involves two different types of NI.

The Two Classes of National Insurance

When you're an employee, NI contributions are just a line on your payslip, handled by your employer. When you're working for yourself, the responsibility falls to you, and it's all handled through your annual Self Assessment tax return.

There are two "classes" of National Insurance you need to be aware of.

Class 2 National Insurance is a flat-rate weekly amount. Its main purpose is to build up your qualifying years for the State Pension. For the 2024/25 tax year, if your profits are over £12,570, you’ll automatically build a qualifying year without actually paying anything. If your profits dip below £6,725, you have the option to make voluntary contributions to make sure you don't miss out on that pension entitlement.

Class 4 National Insurance, on the other hand, is directly tied to how well your business is doing. It’s calculated as a percentage of your annual profits. The more profit you make, the more Class 4 NI you'll pay. Simple as that.

Here’s the main difference in a nutshell:

- Class 4 is paid on profits above a certain threshold.

- Unlike Class 2, it doesn't count towards your State Pension but is still mandatory.

- It's all calculated and paid at the same time as your Income Tax bill via your Self Assessment.

Think of Class 2 as your ticket to a State Pension, and Class 4 as a tax on your success. Getting the distinction is key. For a more detailed breakdown, have a look at our guide to paying Class 4 NICs.

Decoding Payments on Account

One of the biggest financial shocks for new sole traders is something called ‘payments on account’. This is where HMRC asks you to make advance payments towards your next year's tax bill.

Essentially, HMRC looks at your tax bill for the year and assumes you'll earn a similar amount next year. If your total bill is over £1,000, they’ll typically ask you to pay half of it in advance by 31st January and the other half by 31st July.

Here’s a real-world example: Let's say a freelance photographer makes a £25,000 profit in their first year. Their tax and NI bill comes to £3,000. When they file their tax return by the 31st January deadline, they have to pay that £3,000 plus the first payment on account for the next year, which is another £1,500 (50% of the bill). The second £1,500 is then due on 31st July.

You can see how that could catch you off guard if you haven't put money aside. If you know your income is going to be lower in the coming year, you can apply to HMRC to have your payments on account reduced.

Planning for Growth and VAT

As your business thrives, another major milestone you need to watch for is the VAT (Value Added Tax) threshold. It’s a legal requirement to register for VAT once your turnover hits a certain level within any rolling 12-month period.

Right now, that VAT registration threshold is £90,000. Once your turnover crosses that line, you must:

- Register for VAT with HMRC.

- Start charging VAT on your services or products.

- File regular VAT returns.

While it does mean more admin, being VAT registered isn't all bad. It allows you to reclaim the VAT you spend on business-related purchases, which can be a real advantage. More than anything, it's a clear signal that your business is on the right track and growing successfully.

Juggling all these financial duties can feel like a lot, especially when you’re trying to run your business. But you don't have to figure it all out on your own. At Stewart Accounting Services, we help sole traders across the UK handle their tax and NI with confidence. If you need a hand with your Self Assessment or just want to get your finances in order, get in touch with our expert team today.

Setting Up Your Business for Financial Success

Registering with HMRC is a huge step, but let's be honest, a UTR number alone doesn't build a business. What really sets you up for the long haul are the financial habits you put in place right from the beginning. Get your record-keeping sorted now, and you'll save yourself a world of pain come tax season.

Think of it like this: you wouldn't drive a car without a fuel gauge. In the same way, you can't run a business effectively without knowing exactly what's coming in and what's going out. This isn't about becoming an accounting wizard overnight. It’s about finding a simple, reliable system that you can stick with.

Choosing Your Record-Keeping Method

There's no single 'best' way to keep your books. The right system is simply the one you'll actually use. The goal is straightforward: track every penny of your business income and every single expense.

You've really got two main options here:

- Simple Spreadsheets: Honestly, for a lot of new sole traders, a well-organised spreadsheet does the job perfectly. You can set up different tabs for your income, your expenses, and maybe even your business mileage. It’s a cheap and cheerful solution that puts you in full control.

- Cloud Accounting Software: This is where tools like Xero or QuickBooks come in. They’re built for small businesses and can link straight to your bank account, which is a massive time-saver. While they come with a monthly fee, the hours they save you, especially when preparing your tax return, can be well worth it.

The tool you choose is less important than the habit you build. Just block out 30 minutes in your calendar each week to get your records up to date. This simple routine stops the paperwork from piling up and becoming a monster task you dread.

Why a Separate Business Bank Account Is a Non-Negotiable

If I could give one piece of advice to every new sole trader, it would be this: open a separate bank account for your business. It's not technically a legal requirement, but trust me, mixing your business and personal finances is a recipe for disaster.

A dedicated business account gives you a clean, clear view of your cash flow. It makes spotting allowable expenses incredibly easy because every transaction in that account is business-related. When it's time to do your Self Assessment, you (or your accountant) won't have to waste hours trawling through your weekly Tesco shop and Costa trips to find legitimate business costs.

What Records Does HMRC Expect You to Keep?

HMRC isn't just being difficult; they need you to keep detailed records to verify your income and expenses. Keeping good records is also your best tool for reducing your tax bill, as it provides the evidence you need to claim every allowable expense you're entitled to.

You absolutely must keep records of:

- All sales and income: This means copies of every invoice you issue.

- All business expenses: Keep every receipt, from a train ticket for a client meeting to your monthly software subscriptions.

- VAT records: If you're VAT registered, this is a whole other level of meticulous bookkeeping.

- Records of personal money: Make a note of any cash you put into the business or take out for yourself.

And the golden rule? You must hold onto these records for at least 5 years after the 31st January submission deadline for that tax year. Don't get caught out.

Understanding Allowable Business Expenses

Allowable expenses are simply the costs you incur "wholly and exclusively" for running your business. By claiming them, you reduce your taxable profit, which means you pay less in Tax and National Insurance. It’s a win-win.

A few common examples include:

- Office Costs: Things like stationery, phone bills, or a portion of your home's utility bills if you work from home.

- Travel Costs: Fuel for your car, parking fees, and train fares for business journeys.

- Marketing and Advertising: The cost of your website, business cards, or any social media ads you run.

- Professional Development: Any training courses that help you improve the skills you need for your business.

Beyond just tracking expenses, good time tracking and invoicing strategies for freelancers are vital for managing your cash flow. Great records make this a breeze. If getting all this set up feels a bit daunting, the team at Stewart Accounting Services can help you build a solid system from day one.

When Things Get a Little More Complicated

Getting registered for Self Assessment is the first major hurdle, and for many sole traders, it's the only one for a while. But as your business grows, or if you work in a specific industry, you'll find other HMRC registrations pop up on your radar.

Think of these as tripwires. Crossing certain business milestones triggers new responsibilities, and ignoring them can lead to some painful penalties from HMRC. Let's be honest, getting these things wrong is a common mistake, but a little bit of foresight goes a long way.

Working in Construction? You Need to Know About CIS

If your work is in the construction industry, you can't afford to ignore the Construction Industry Scheme (CIS). It’s a specific set of tax rules designed for how contractors pay subcontractors. This doesn't affect anyone outside of construction, but for a self-employed plumber, sparky, or builder, it's absolutely essential.

Simply put, CIS requires contractors to deduct a portion of a subcontractor's payment and send it straight to HMRC. This acts as an advance payment towards your final tax and National Insurance bill. If you're the subcontractor, you have to be registered. If you're not, the contractor is legally required to deduct tax at a much higher rate of 30%, which can be a massive hit to your cash flow.

Here's how it plays out: Say you're a freelance electrician brought in by a main building firm to handle the wiring on a new estate. The firm is your 'contractor', and you're the 'subcontractor'. They'll ask for your UTR to check your status with HMRC. If you’re registered for CIS, they'll deduct the standard 20%. If you’re not, that deduction shoots up to 30%.

Taking on Your First Employee: Registering for PAYE

As a sole trader, you are the business. But that all changes the moment you hire your first member of staff. This is the trigger for registering as an employer and setting up PAYE (Pay As You Earn).

PAYE is HMRC’s system for collecting Income Tax and National Insurance directly from employees' salaries. Once you're registered, you are responsible for running payroll, calculating the right deductions, and paying them over to HMRC on time. It's a big step up in your administrative workload.

Keeping an Eye on the VAT Threshold

Growth is a great problem to have, but it brings new duties. The big one for most sole traders is the VAT registration threshold. Once your VAT-taxable turnover hits £90,000 within any rolling 12-month period (as of 2025), you are legally required to register for VAT. This isn't just for huge companies; a successful consultant or a booming online shop can hit this level faster than you might think.

As of March 2025, there were 2.73 million businesses in the UK registered for VAT and/or PAYE. While the number of sole proprietors has dipped slightly to 380,520, they are still a core part of the UK economy. It's a reminder that many small businesses reach these thresholds. And remember, the penalties for getting things wrong, like missing a Self Assessment deadline, start at £100 plus interest. It pays to be prepared. You can find more data on UK business activity on ONS.gov.uk.

Juggling these extra registrations can feel like a lot to handle on top of your day-to-day work. Below is a quick table to help you spot which of these might apply to you.

When Do You Need to Register for More Than Self Assessment?

This table provides a clear comparison of the triggers for VAT, CIS, and PAYE registration to help you identify your specific obligations.

| Registration Type | Who Needs to Register? | Key Trigger |

|---|---|---|

| VAT (Value Added Tax) | Any business (sole trader, partnership, limited company). | Your VAT-taxable turnover exceeds £90,000 in a rolling 12-month period. |

| CIS (Construction Industry Scheme) | Subcontractors working in the construction industry. | You start doing construction work for a contractor. Registration ensures tax is deducted at the correct rate. |

| PAYE (Pay As You Earn) | Any business that hires one or more employees. | The moment you hire your first employee (before their first payday). |

Navigating these rules adds another layer of complexity to running your own business. At Stewart Accounting Services, we guide sole traders through these exact situations every single day. If you think you might be approaching a threshold for CIS, PAYE, or VAT, don't guess. Contact our expert team for clear, straightforward advice and get it right the first time.

Your Top Questions Answered

Starting out on your own always throws up a few questions. It's completely normal. Getting these sorted early on can give you the confidence that you're getting things right from day one and not storing up problems for later. Let's run through some of the most common queries we hear from new sole traders.

Can I Be Self-Employed and Employed at the Same Time?

Yes, you certainly can. In fact, it’s a very popular way to start a business, keeping the security of a salary while you build your own thing on the side.

The key trigger for HMRC is when your income from your side-hustle or freelance work tops the £1,000 trading allowance within a single tax year. As soon as you cross that line, you need to register as self-employed.

When you complete your Self Assessment tax return, you’ll declare everything – your salary from your job (which is already taxed via PAYE) and the profits from your self-employed work. HMRC’s system then tots it all up to see if you owe any extra tax. This is exactly why keeping your business finances separate from your personal ones is so important; it makes this whole process much, much simpler.

What If I've Missed the Registration Deadline?

Ah, the 5th of October deadline. This one catches a lot of people out because it feels a bit counterintuitive. You have to tell HMRC you need to send them a tax return by the 5th of October after the tax year in which you started your business.

Let’s use an example. Say you kick off your new venture in February 2025. That date falls within the 2024/25 tax year (which ends on 5th April 2025). This means you have until 5th October 2025 to register with HMRC.

If that date has already passed, don't panic, but do act quickly. Missing it can attract a 'failure to notify' penalty from HMRC, but these are often less severe than the penalties for filing your return late or paying your tax late. The most important thing is to get registered as soon as you realise and make sure you still hit the main 31st January deadline for filing and paying.

Do I Really Need to Register if I'm Only Earning a Little Bit?

This is where the £1,000 trading allowance comes in. It was designed to stop people with tiny bits of extra income from having to go through the whole Self Assessment process.

If your total income from all your self-employed activities is £1,000 or less in a tax year, you don't need to register or declare it. Simple as that.

A Crucial Distinction: Remember, this £1,000 threshold is for your turnover (the total amount of money you've billed), not your profit. If you invoice a client for £1,200 but had £300 in costs, your income is still over the limit, and you must register.

How Do I Pick a Business Name as a Sole Trader?

As a sole trader, you've got a couple of options. You can just use your own name (like 'Jane Doe, Graphic Designer') or come up with a trading name that's a bit more memorable (like 'Bright Spark Designs').

There are just a few ground rules to be aware of:

- No misleading endings: You can't use 'Limited', 'Ltd', 'LLP', or 'PLC' in your name. Those are reserved for specific company structures.

- Keep it clean and official: The name can't be offensive, and you can't imply a connection to the government or a local authority unless you genuinely have one.

- Do a quick check: It's a good idea to search for your chosen name online to make sure it's not already a registered trade mark. A bit of research now can save you a legal headache down the line.

A good practical tip? Before you get attached to a name, check if the website domain and social media handles are available. And remember, even if you use a trading name, your invoices and official letters must also include your own name.

Getting these details right sets you up for a smooth start. If you're still feeling a bit lost or just want the peace of mind that comes with getting it done properly, the team at Stewart Accounting Services is here to help. Get in touch with us for some friendly, expert advice on your new venture.