What if your current salary and dividend split is actually costing you £4,200 more in tax than it did just two years ago? If you’re searching for limited company director tax advice, you’re likely part of the 74% of business owners in Stirling who feel they’re working longer hours only to see HMRC take an ever-increasing slice of the pie. You probably feel that the constant shifting of tax bands, especially the growing divergence between Scottish and UK rates, has made managing your pay a source of stress rather than a reward for your hard work.

We’re here to take that burden off your hands. This guide provides the strategy you need to achieve your three freedoms: more time, more money, and a lot less stress. You’ll discover exactly how to structure your 2026 take-home pay to minimise your liability while staying fully compliant with the latest regulations. We’ll preview the most efficient salary-dividend splits and specific planning strategies for Scottish taxpayers to ensure you have a clear, actionable plan for the year ahead.

Key Takeaways

- Learn how to balance your dual role as an employee and shareholder using expert limited company director tax advice to navigate Corporation Tax and National Insurance.

- Discover why the “low salary, high dividend” model remains the most tax-efficient strategy for 2026 and how to adapt to the latest dividend allowance changes.

- Understand the specific impact of Scottish Income Tax bands, such as the Intermediate and Advanced rates, on your overall tax liability and take-home pay.

- Explore high-value corporate deductions, including how pension contributions and electric vehicle Benefit-in-Kind rates can significantly lower your tax bill.

- Identify how moving from basic compliance to proactive annual tax reviews can provide you with more time, more money, and less stress.

Understanding Your Tax Obligations as a Limited Company Director in 2026

Running a limited company in 2026 requires a clear shift in how you view your income and your relationship with the state. You don’t just hold one position; you’re a dual-status individual. You act as an employee of your own business while simultaneously serving as its owner or shareholder. This distinction is the bedrock of any professional limited company director tax advice, as it dictates how you’re taxed and how you extract profit. Since April 2021, the UK government has frozen many tax thresholds, and by 2026, these freezes will have pushed thousands of directors into higher tax brackets through fiscal drag. Staying ahead of these changes is the only way to protect your margins.

At Stewart Accounting Services, we guide our clients in Alloa, Stirling, and Falkirk through these complexities using our “Three Freedoms” approach. Our goal is to provide you with more time, more money, and more mind. By “more mind,” we mean significantly less stress about HMRC deadlines and compliance. We take the heavy lifting off your hands so you can focus on growth. In 2026, managing your obligations involves balancing three primary taxes: Corporation Tax on company profits, and both Income Tax and National Insurance on your personal remuneration. Failing to plan for the interaction between these three can lead to unnecessary leakages in your cash flow.

The Director’s Responsibility to HMRC and Companies House

Your legal duties are split between two distinct government bodies. Companies House requires your Annual Accounts and a Confirmation Statement every year to keep the public register accurate. Meanwhile, HMRC demands your Company Tax Return (CT600) and your personal Self Assessment. You must register for Self Assessment if your dividend income exceeds the £500 tax-free allowance, a threshold that has remained low to capture more tax revenue from small business owners. Many directors attempt “DIY” filing to save costs, but this often leads to expensive mistakes. Statistics suggest that 1 in 4 small businesses face penalties for late or incorrect filings in their first three years. An immediate £100 fine for a late tax return can quickly escalate to over £900 if left unaddressed for six months. We ensure these deadlines are met, removing the risk of “brown envelope anxiety” from your life.

Corporation Tax vs Personal Tax: The Big Picture

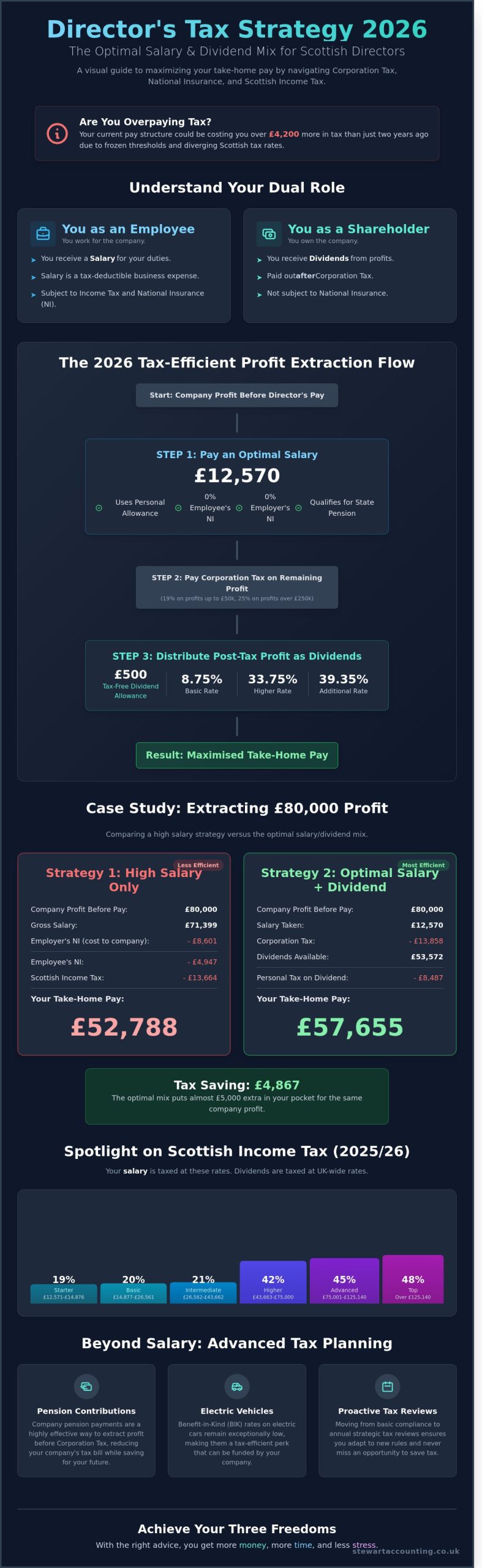

Understanding the “big picture” means separating the company’s money from your own. Your company is a separate legal entity. It pays UK Corporation Tax on its taxable profits before you can touch a penny in dividends. In 2026, the rates remain tiered: a 19% small profits rate for companies with profits under £50,000, and a main rate of 25% for those exceeding £250,000. For businesses sitting between these figures, a marginal relief system applies, effectively creating a sliding scale of taxation.

Profit is calculated by taking your total revenue and subtracting all “wholly and exclusively” business expenses, including your gross director’s salary. Once this tax is paid, the remaining funds can be distributed as dividends. The most effective limited company director tax advice for 2026 focuses on the “tax-efficient envelope,” which is the strategy of taking a low salary up to the National Insurance Primary Threshold of £12,570 and topping up your income with dividends to stay within the basic rate band. This approach minimises your National Insurance contributions while utilising your personal tax-free allowance to its fullest extent.

The Salary vs Dividend Debate: Calculating the Most Tax-Efficient Mix

Most business owners want to keep as much of their hard earned money as possible. The “Low Salary, High Dividend” model remains the most effective strategy for 2025 and 2026. This approach works because dividends don’t attract National Insurance (NI) contributions, which saves both you and your company a significant amount of money. While you pay Corporation Tax on profits first, the combined tax hit is usually lower than taking a high 100% salary. Getting the balance right gives you the “three freedoms” we always talk about: more time, more money, and a lot less stress.

Taking a small salary ensures you qualify for the State Pension and other benefits without triggering heavy tax bills. You then top up your income with dividends. For the 2025/26 and 2026/27 tax years, the dividend allowance sits at £500. This means the first £500 of dividends you receive is tax-free, regardless of your other income. When you’re looking for limited company director tax advice, the goal is always to use your personal tax-free allowances to their full potential before paying a penny more than necessary.

Choosing the Optimal Salary Threshold

Deciding on your salary level is the first step in your tax planning. You have three main routes to consider based on your specific circumstances:

- Option 1: The Lower Earnings Limit (LEL). At £6,396 per year, you don’t pay NI, but the year still counts toward your State Pension. It’s the bare minimum for protection.

- Option 2: The Secondary Threshold (ST). Set at £9,100, this is the limit where your company starts paying 13.8% Employer NI. Many directors stop here to avoid any NI costs entirely.

- Option 3: The Primary Threshold (PT). This usually aligns with the £12,570 Personal Allowance. While the company pays some Employer NI, you maximise your personal tax-free income.

How Dividends Work in 2026

Dividends are different from salaries because they come from “distributable profits.” This is the money left over after your company has paid all expenses and its Corporation Tax bill. For 2026, the tax rates on dividends remain at 8.75% for basic rate payers, 33.75% for higher rate payers, and 39.35% for the additional rate band. You must ensure your company actually has the profit to pay these. If you pay out more than you’ve made, you’re creating “illegal dividends,” which can lead to serious legal and tax complications. Understanding your Director’s Legal Responsibilities is vital here; you are personally responsible for ensuring the company is solvent when dividends are declared.

Let’s look at a practical example. If you want a total take-home target of £50,000, a common limited company director tax advice strategy involves taking a salary of £12,570 and dividends of £37,430. Since your salary uses up your Personal Allowance, you pay £0 income tax on it. Your first £500 of dividends is tax-free. The remaining £36,930 of dividends falls into the basic rate band, taxed at 8.75%. This results in a personal tax bill of roughly £3,231. Compare this to a £50,000 salary, where you would lose over £12,000 to tax and NI, and the benefits are clear. If this feels like a lot to manage, we can take it off your hands and handle the calculations for you.

We recommend reviewing these figures every April. Tax thresholds often change, and even a small adjustment in government policy can shift the “sweet spot” for your salary. Keeping your records accurate throughout the year makes this year-end planning much smoother and ensures you never pay more than you legally owe.

Navigating Scottish Income Tax: Why Location Matters for Director Pay

If your main home is in Scotland, your personal tax liability follows Scottish Government legislation rather than the rules set for the rest of the UK. This creates a distinct financial landscape for business owners. While Corporation Tax remains a UK-wide matter, the income tax you pay on your director’s salary depends entirely on your postcode. This divergence means that generic limited company director tax advice found online often fails to account for the specific hurdles faced by those living in Central Scotland.

The primary challenge for Scottish directors lies in the six-band system. Unlike the three-band system in England, Scotland introduces an “Intermediate” 21% rate and an “Advanced” 45% rate. A director in Stirling earning a £50,000 salary pays roughly £2,000 more in income tax annually than a director in London on the same amount. Because National Insurance (NI) remains a reserved UK-wide matter, we see a complex interaction where NI thresholds don’t align perfectly with Scottish tax bands. This misalignment requires a precise calculation to ensure you aren’t overpaying.

We often find that the traditional salary-to-dividend ratio needs recalibrating for Scottish residents. Since dividend tax rates are reserved and remain the same across the UK, shifting more of your income into dividends is frequently the most efficient route to avoid the higher Scottish income tax brackets. We focus on balancing these elements to help you achieve the “three freedoms”: more time, more money, and less stress.

Scottish Tax Bands for 2026/27

Current projections for the 2026/27 tax year suggest the Scottish Government will maintain its progressive structure. The current bands include:

- Starter Rate (19%): £12,571 to £14,876

- Basic Rate (20%): £14,877 to £26,561

- Intermediate Rate (21%): £26,562 to £43,662

- Higher Rate (42%): £43,663 to £75,000

- Advanced Rate (45%): £75,001 to £125,140

- Top Rate (48%): Over £125,140

The most significant “tax trap” occurs at the £43,663 threshold. Here, the tax rate jumps from 21% to 42%, effectively doubling the tax cost on the next pound earned. For directors, staying just below this threshold through a combination of salary and pension contributions is a common strategy we implement to protect your take-home pay.

Strategic Planning for Central Scotland Businesses

For directors based in Alloa, Stirling, and Falkirk, local expertise is vital. National firms often miss the nuance of how Scottish rates impact your overall wealth. As Fully Qualified Chartered Accountants, we provide limited company director tax advice that considers your total household income and long-term goals. We understand the local economy and the specific pressures facing businesses in Central Scotland.

Our goal is to take the complexity off your hands. By managing the divergence between UK NI and Scottish Income Tax, we ensure your payroll and dividend vouchers are compliant and tax-efficient. Managing these 42% and 45% rates requires proactive planning before the tax year ends, not after. We handle the technical details so you can focus on running your business, providing the peace of mind that comes from knowing your tax position is fully optimised.

Beyond Basic Pay: Strategic Tax Planning and Allowable Expenses

Optimising your tax position requires looking at the bigger picture. When you’re seeking limited company director tax advice, you’ll find that the most successful strategies happen before profit is even declared. Employer pension contributions are a standout tool for this. Because these are usually treated as an allowable business expense, they reduce your Corporation Tax bill by up to 25% while building your private wealth. For the 2024/25 tax year, the annual allowance is £60,000, which offers a massive window to move company cash into your personal future without triggering a personal tax charge.

Swapping a petrol car for an Electric Vehicle (EV) remains a power move for savvy directors. While traditional company cars attract heavy taxes, pure electric models currently sit at a 2% Benefit-in-Kind (BiK) rate for the 2024/25 and 2025/26 tax years. If your company buys a new EV, it can often claim 100% First Year Allowances. This allows you to deduct the full cost of the vehicle from your pre-tax profits in the year of purchase. It’s a practical way to upgrade your transport while drastically lowering your tax liability.

Don’t ignore the small wins that lead to “more mind” and less stress. HMRC allows “trivial benefits” up to £50 per instance. As a director of a close company, you’re capped at £300 per tax year. These cannot be cash or performance-related, but gift cards for a family meal or a hobby are perfectly acceptable. Additionally, income splitting with a spouse or family member who genuinely works in the business can be highly effective. By utilising their £12,570 personal allowance and basic rate bands, you keep more money within your household rather than handing it to the Treasury.

Maximising Allowable Business Expenses

The “wholly and exclusively” rule is the gold standard for HMRC. If a cost is purely for business purposes, it’s likely deductible. Many directors miss out on the £6 per week “use of home” allowance or fail to claim mileage at 45p per mile for the first 10,000 miles. We find that 85% of clients who switch to digital bookkeeping platforms like Xero discover unclaimed expenses they previously overlooked. Keeping your records updated in real-time ensures these small, frequent savings don’t slip through the cracks. We can take it off your hands by managing your bookkeeping and ensuring every penny is accounted for.

Directors’ Loans: Risks and Opportunities

Sometimes you need a short-term cash injection for a personal project. You can take a director’s loan, but you must be disciplined. If you don’t repay the loan within nine months and one day of your company’s year-end, the company faces a “S455” tax charge at 33.75%. While this tax is eventually refundable once the loan is repaid, it creates a significant cash flow burden in the interim. Using a loan for a six-month period can be a tax-free way to manage personal liquidity, provided you have a clear plan to clear the balance before the deadline. Our team in Alloa and Stirling helps directors track these balances to avoid any nasty surprises from HMRC.

Taking the Burden Off Your Hands: Professional Tax Planning for Growth

Every ambitious director needs a roadmap to navigate the UK tax system. An annual tax review isn’t just a box-ticking exercise; it’s a vital strategy for business longevity. Many directors wait until the January Self Assessment deadline to think about their liabilities, but by then, it’s often too late to make meaningful changes. A proactive review allows you to adjust your salary-to-dividend ratio or timing of capital purchases before the tax year ends on 5 April. This shift from reactive “compliance” to forward-looking “advisory” is where the real value lies. We don’t just tell you what you owe; we help you decide how much you keep.

At Stewart Accounting Services, we’ve refined this process to deliver what we call the “Three Freedoms.” First, you get more money. By applying professional limited company director tax advice, we identify efficiencies that can save thousands in Corporation Tax or National Insurance. Second, you gain more time. You didn’t start a business to spend your weekends wrestling with spreadsheets or HMRC portals. We take it off your hands so you can focus on scaling your operations. Finally, you achieve “more mind,” which simply means less stress. When you know your tax affairs are handled by experts, that constant background hum of financial anxiety disappears.

Moving from a state of stress to financial clarity requires a partner who understands the 2026 tax landscape. With Corporation Tax rates sitting at 25% for profits over £250,000 and the tapering of the dividend allowance, the margin for error has shrunk. We provide the technical precision needed to ensure you’re compliant while remaining as tax-efficient as possible. It’s about creating a stable foundation so you can stop worrying about the “what ifs” and start planning for “what’s next.”

The Value of a Chartered Accountant in 2026

There’s a significant difference between a bookkeeper and a Chartered Accountant. While a bookkeeper focuses on recording historical data, a Chartered Accountant interprets that data to find opportunities. In 2026, navigating the complexities of R&D tax credits or the latest capital allowance rules requires a high level of expertise. We spot the tax-saving opportunities that generic software or basic bookkeeping services miss. Our local presence in Alloa, Stirling, and Falkirk means you have access to a team that understands the Scottish business environment and is available for face-to-face support when you need it most.

Contact Us for a Tailored Tax Review

If you’re worried that switching accountants is a complicated ordeal, let us reassure you. It’s actually very simple. We manage the entire “Professional Clearance” process, which involves us contacting your previous accountant to securely transfer your records. You won’t have to deal with any administrative headaches or awkward conversations. We take care of the transition so there’s no interruption to your service. It’s a smooth, professional handover designed to make your life easier from day one.

We invite you to join us for a free consultation to discuss your business goals and how we can help you achieve your Three Freedoms. Whether you’re based in Clackmannanshire or across Central Scotland, our team is ready to provide the clarity you’ve been looking for. Don’t leave your financial future to chance. You can book your 2026 tax planning session today and take the first step toward a more profitable, stress-free business life.

Take Control of Your 2026 Earnings Today

Maximising your take-home pay in the 2026 tax year requires a proactive approach to the salary versus dividend split. By keeping your director’s salary at the £12,570 threshold and strategically timing dividend payments, you’ll protect your personal allowance and reduce your overall tax liability. It’s also vital to account for the specific Scottish Income Tax bands that impact business owners across Central Scotland. Our team of Fully Qualified Chartered Accountants provides the expert limited company director tax advice you need to navigate these complexities without the headache.

With local offices in Alloa, Stirling, and Falkirk, we specialise in delivering the “Three Freedoms”: more time, more money, and much less stress. We’ve helped over 500 local SME owners reclaim their peace of mind by handling the technical details that often lead to overpayment or HMRC penalties. Don’t let the 2026 tax changes catch you off guard. Let us take the tax burden off your hands; contact Stewart Accounting Services today. We’re ready to help you build a more profitable future for your business.

Frequently Asked Questions

Do I have to complete a Self Assessment as a limited company director?

You must complete a Self Assessment tax return if you receive dividends over the £500 allowance or have any other untaxed income. HMRC uses this process to calculate the exact tax you owe on your total personal income, even if your basic salary is handled through PAYE. We can take this task off your hands to ensure your filing is accurate and submitted well before the 31 January deadline.

What is the most tax-efficient salary for a director in the 2026/27 tax year?

The most tax-efficient salary for the 2026/27 tax year is usually £12,570, which matches the current frozen Personal Allowance and National Insurance Primary Threshold. Taking this specific amount allows you to build a qualifying year for your state pension without actually paying employee or employer National Insurance. Our team provides tailored limited company director tax advice to help you balance this salary with dividends for maximum take-home pay.

How much dividend can I take tax-free in 2026?

You can take exactly £500 in dividends tax-free during the 2026/27 tax year. Any dividend income you receive beyond this £500 threshold is taxed at a rate based on your total personal income bracket. Since the allowance was cut from £1,000 to £500 in April 2024, it’s vital to plan your withdrawals carefully to avoid paying more tax than necessary.

Can I pay my spouse a salary from my limited company?

You can pay your spouse a salary if they perform genuine work for the business and the pay reflects a commercial rate for those tasks. This strategy allows your household to utilise two separate £12,570 Personal Allowances, which can save a family up to £2,514 in tax each year. We’ll help you document their role properly to satisfy HMRC’s strict “wholly and exclusively” rules for business expenses.

Is it better to be a sole trader or a limited company in 2026?

A limited company structure is typically more tax-efficient once your annual profits exceed £30,000, though the benefits depend on your specific spending needs. Sole traders face simpler paperwork but don’t have the flexibility to defer dividends or retain profits within the business to manage tax brackets. We help business owners in Alloa and Stirling compare these two options to ensure they’re using the most profitable setup.

What taxes do I pay on dividends as a higher-rate taxpayer?

You pay a tax rate of 33.75% on dividends if your total annual income exceeds the £50,270 higher-rate threshold. This rate applies to every pound of dividend income that falls within the higher-rate band after you’ve used your £500 tax-free allowance. It’s a sharp increase from the 8.75% basic rate, so we often suggest timing your payments to stay within the most efficient tax bands.

What happens if I take more money out of my company than it made in profit?

If you withdraw more money than the company’s available post-tax profit, the excess is recorded as an overdrawn director’s loan. You’ll face a 33.75% S455 tax charge if this loan isn’t repaid within 9 months and 1 day of your company’s accounting year-end. This can lead to significant cash flow stress, but our accountants can help you monitor these balances to avoid such expensive penalties.

How does the Scottish Income Tax rate affect my director salary?

Scottish Income Tax rates apply to your director salary, meaning you’ll pay different percentages than directors in England, such as the 19% starter rate or 42% higher rate. While dividends are taxed at UK-wide rates, your salary is subject to these specific Scottish bands. This makes expert limited company director tax advice essential for our clients in Central Scotland to ensure their total tax burden is minimised effectively.