Optimising your working capital isn't just about tweaking numbers on a balance sheet; it's about improving the efficiency of your day-to-day operations to free up cash. It all comes down to how well you manage the flow of money in and out of the business—how quickly you get paid, how long stock sits on the shelf, and when you pay your own bills.

The key is to use a few core metrics (DSO, DIO, and DPO) to find out precisely where your cash is getting stuck.

Understanding Your Working Capital Health

Before you can start making improvements, you need a clear picture of where you stand right now. Whether you're running an engineering firm in Falkirk or a retail shop in Stirling, the first step is always an honest assessment of your financial position. This isn't about getting lost in complex spreadsheets; it's about understanding the real-world rhythm of cash as it moves through your company.

This initial diagnostic really just focuses on three fundamental metrics that make up your working capital cycle. Think of them as the vital signs for your business's financial health.

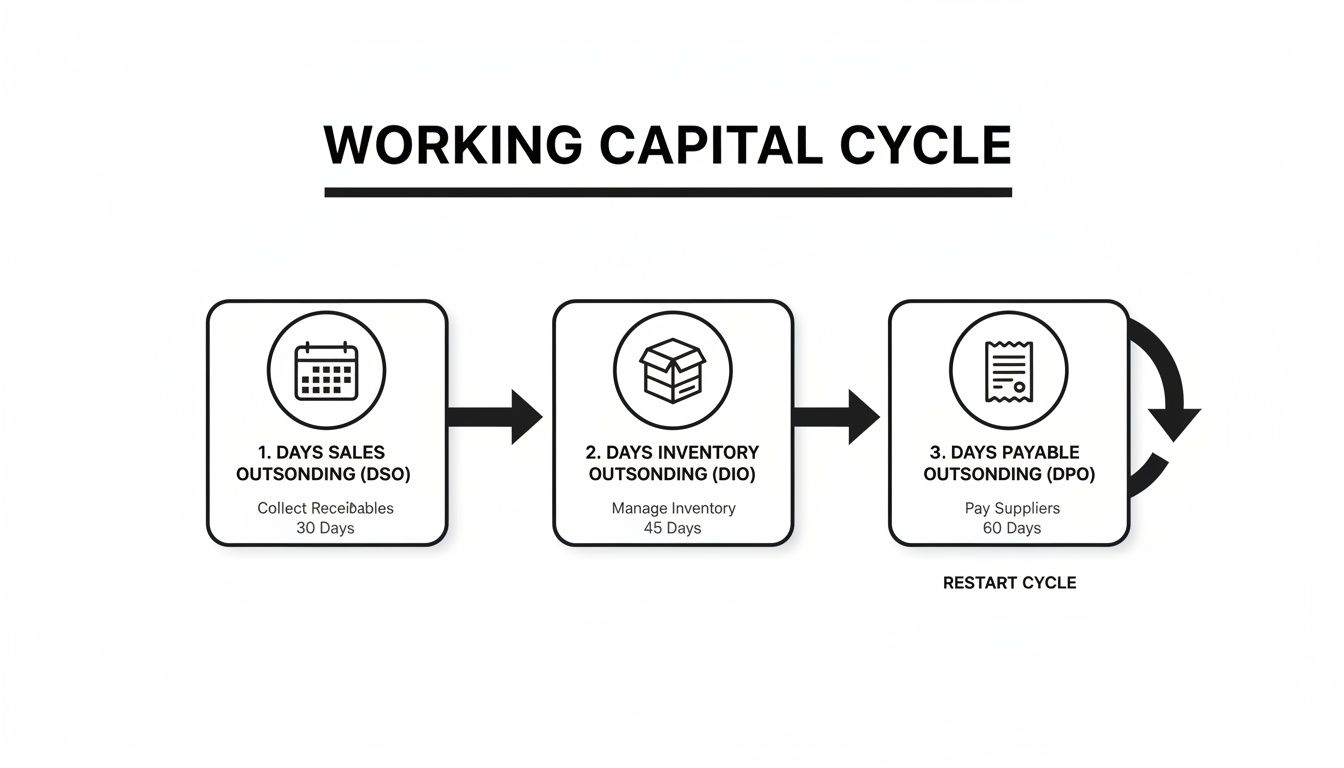

The Three Pillars of Working Capital Analysis

These metrics tell the story of how long your cash is tied up at each stage of your operations. Getting a handle on them is the first practical step towards unlocking that cash. For a lot of our clients, this becomes much clearer after implementing robust business intelligence dashboards that give them a real-time view.

Below is a quick breakdown of what these metrics mean.

Key Working Capital Metrics Explained

This table breaks down the three core components of the working capital cycle, what they measure, and why they are so critical for your business's financial health.

| Metric | What It Measures | Why It Matters |

|---|---|---|

| Days Sales Outstanding (DSO) | The average number of days it takes for customers to pay you after a sale. | A high DSO means your cash is tied up in accounts receivable. Lowering it gets cash into your bank account faster. |

| Days Inventory Outstanding (DIO) | How long your stock sits on the shelf before it's sold. | High DIO means capital is locked up in unsold goods, risking obsolescence and increasing storage costs. |

| Days Payables Outstanding (DPO) | The average number of days you take to pay your own suppliers. | A higher DPO can be a good source of short-term cash, but stretching it too far can seriously damage supplier relationships. |

Getting to grips with these three pillars gives you the insight you need to make targeted changes.

The diagram below shows how these three components work together in a cycle.

As you can see, your cash is committed the moment you pay for materials or stock, and it only comes back when your customer finally pays you. The goal is to shorten that time as much as possible.

Calculating Your Cash Conversion Cycle

These three metrics are the building blocks for your Cash Conversion Cycle (CCC), which is the ultimate measure of how efficiently you're managing working capital.

The Formula:

Cash Conversion Cycle (CCC) = DIO + DSO – DPO

The answer gives you the number of days your company's own cash is trapped funding its operations. The lower the number, the better. It points to a more efficient, cash-generative business. Of course, calculating this is much simpler once you know how to read financial statements and pull the right numbers.

This isn't just an abstract financial concept; it's a major issue for UK businesses. Recent analysis shows that net working capital days have shot up by almost 48% since 2015—the biggest jump in Europe. Smaller firms have been hit particularly hard, seeing their working capital days worsen by 13.5% because they often don't have the clout to negotiate longer payment terms with their own suppliers.

Let's put this into context. Imagine a manufacturing SME based in Alloa has a CCC of 90 days. That means for an entire quarter of the year, their own cash is funding the business before they see a penny back from their sales. By digging into the numbers, they can pinpoint the root cause—be it slow-paying customers (high DSO), too much stock (high DIO), or paying suppliers too fast (low DPO)—and start taking targeted action.

Quick Wins to Immediately Improve Cash Flow

You don't always need a six-month strategic overhaul to get your working capital in shape. In my experience, some of the most dramatic improvements come from small, immediate tweaks to your everyday processes. By focusing on these low-hanging fruit, you can get cash back into the business in weeks, not months.

These quick wins really boil down to two simple goals: getting paid faster and being smarter about how you pay others. For most SMEs I've worked with, the chasm between sending an invoice and seeing the cash land in the bank is the single biggest drain on their resources. Closing that gap is your fastest route to a healthier financial footing.

Refine Your Invoicing and Collections Process

Let's be blunt: the most effective way to speed up your cash flow is to get tough on your accounts receivable process. Delays here hit your bank balance directly. A disorganised approach to invoicing and chasing payments is a surprisingly common—but thankfully, easily fixed—problem.

I recently worked with a digital agency in Glasgow that was really feeling the pinch. Their Days Sales Outstanding (DSO) was over 60 days, which is a long time to wait for your money. The culprit? An inconsistent invoicing schedule. Invoices were often sent out weeks after key project milestones were hit.

We put a simple rule in place: invoice immediately after the work is completed. We also set up automated reminders for upcoming due dates. The result? Within two months, they cut their average DSO down to 38 days. This one change freed up a huge amount of cash that was previously stuck on their sales ledger.

Here are a few practical things you can do right now:

- Offer an early payment discount. It might sound small, but offering 2% off for payment within 10 days (often written as "2/10 net 30") gives your clients a solid reason to pay you before anyone else.

- Make it ridiculously easy to pay you. Get rid of any friction. Your invoice should have clear bank transfer details and, ideally, a link to pay online by card. Don't make them hunt for the information.

- Automate your reminders. Use your accounting software to send polite nudges before, on, and just after the due date. This takes the manual work out of it and ensures nothing gets missed.

A proactive, organised collections process isn’t about being aggressive. It's about clear communication and making it simple for clients to pay you on time. This is the bedrock of good working capital management.

Strategically Manage Supplier Payments

Just as speeding up incoming cash is vital, so is managing your outgoing payments. Now, this doesn't mean you should start paying everyone late and ruining your reputation. It’s about aligning your payment runs with your own cash flow cycle and using the terms you've been given.

Talk to your key suppliers. If a supplier gives you 30-day terms, paying their invoice the day it arrives doesn't do your cash flow any favours. Using the full credit period is simply smart cash management.

I saw a great example of this with a retail shop in Edinburgh. They talked to their main wholesaler and managed to extend their payment terms from 30 to 45 days during their peak Christmas season. This meant they could sell most of the stock before the bill was even due, which completely changed their cash position during their most critical trading period. A simple conversation created vital breathing room.

Optimise Your Inventory Levels

If your business holds stock, your warehouse is probably your biggest cash trap. Every single box on those shelves represents money you can't use elsewhere. Implementing effective strategies for managing excess inventory is a huge quick win for unlocking capital.

A great place to start is with a straightforward stock analysis. Find your slow-moving or obsolete items—anything that hasn't sold in the last 6-12 months.

Running a clearance sale or creating a special bundle deal for these products can quickly turn that dead stock back into cold, hard cash. You're not just improving your cash flow; you're also cutting the costs of storing products that aren't making you any money.

Using Systems and Technology to Work Smarter, Not Harder

Relying on manual spreadsheets and a jumble of disconnected processes is one of the fastest ways to trap cash in your business. Think about it: the hours spent manually chasing invoices, keying in supplier bills, and trying to get an accurate stock count isn't just inefficient—it directly slows down how quickly you can turn your operations back into cash.

To really get a grip on working capital today, you have to embrace technology that can handle the repetitive grunt work and give you a clear, real-time picture of your finances.

For many of the SMEs we work with across Central Scotland, this journey starts with a simple but powerful shift: moving from old desktop software to a cloud-based accounting platform. This single change lays the foundation for a connected system that actually works for you, not against you.

Building Your Financial ‘Tech Stack’

The term 'tech stack' might sound like something you'd hear in a Silicon Valley boardroom, but it's just a fancy way of describing the set of tools you use to manage your finances. At the heart of it is your accounting software, with other specialist apps plugging in to smooth out specific, time-consuming jobs.

The real goal here is to get information flowing seamlessly from one place to another. This means no more mind-numbing manual data entry, fewer costly errors, and an up-to-the-minute view of where your working capital stands. This is where platforms like Xero really come into their own, acting as the central hub for all your financial data.

A dashboard like Xero’s gives you that at-a-glance view of the numbers that matter.

Having this kind of real-time visibility is the first, crucial step towards making smarter decisions about your cash.

Let's break down how you can build a simple stack to tackle the three main areas of your cash cycle.

Automating Your Accounts Receivable

Chasing late payments is a massive time-suck for any business owner. It’s frustrating and takes you away from what you should be doing. This is where dedicated accounts receivable (AR) tools can be a game-changer.

- Tools like Chaser hook directly into your accounting software (like Xero or QuickBooks) and put your entire invoice reminder process on autopilot.

- You can set up polite, customised email templates that are sent out automatically based on a schedule you decide on—say, a gentle nudge a week before the due date, one on the day, and another a week after.

- It ensures every invoice is followed up consistently without you lifting a finger, which can have a massive impact on reducing your Days Sales Outstanding (DSO).

Streamlining Your Accounts Payable

Are you still dealing with piles of paper bills, manual data entry, and complicated approval chains? Managing supplier invoices can easily descend into chaos. This is an area where accounts payable (AP) automation tools can transform your efficiency.

By digitising the AP process, businesses can cut invoice processing costs by over 80%. But it’s not just about saving a bit of money; it’s about finally gaining proper control and visibility over your cash outflows.

Tools such as Dext (which you might remember as Receipt Bank) are brilliant for this. You just snap a photo of a receipt or forward an email invoice, and the software reads all the key details—supplier name, date, amount, VAT—and puts it straight into your accounting system. All you need to do is approve it.

This completely gets rid of manual data entry, cuts the risk of human error, and gives you a real-time list of what you owe. You can then schedule payments to take full advantage of your credit terms, directly improving your Days Payables Outstanding (DPO). Our guide to accounting process automation dives deeper into how these systems can work for your business.

Gaining Control Over Your Stock

For any business holding stock, inventory management is a huge piece of the working capital puzzle. Cloud-based inventory systems give you the power to fine-tune your stock levels with incredible precision.

- Platforms like Unleashed or Katana link up with both your accounting software and your sales channels (like Shopify, for example).

- They provide a live view of stock levels across all your locations, automate purchase orders when you're running low, and even offer powerful sales forecasting.

- This data-driven approach helps you stop tying up cash in products that aren't selling (overstocking) and avoid missing out on sales because you've run out (under-stocking), directly improving your Days Inventory Outstanding (DIO).

Putting It Into Practice: A Perthshire Construction Company

We worked with a construction firm in Perthshire that was really struggling with its cash cycle. Their DSO was sitting at around 75 days because their project managers were flat out on-site and simply didn't have time to consistently chase invoices. On top of that, supplier invoices were getting lost in vans or buried under paperwork, meaning they were missing out on early payment discounts and straining relationships.

By getting them set up on Xero with Chaser and Dext, we completely turned things around. Chaser put the invoice reminders on autopilot, and within three months, their average DSO had dropped to 42 days. Dext digitised all their supplier bills, giving the finance team a clear, real-time view of what was owed and when, allowing them to pay suppliers more strategically. This simple tech stack freed up thousands of pounds in working capital, which they were able to reinvest straight back into new equipment.

Strategic Inventory and Supplier Management

If your business holds stock – whether you're a retailer, wholesaler, or manufacturer – then your inventory is almost certainly the biggest cash trap you have. Every single item sitting on a shelf or in a warehouse is capital that could be used for growth, paying down debt, or just giving you a bit more breathing room.

Finding that sweet spot is what this is all about. Too much inventory ties up cash and racks up costs for storage, insurance, and the risk of it all becoming obsolete. But hold too little, and you're looking at stockouts, lost sales, and unhappy customers. The goal is to hold the right amount of the right stock to meet demand without locking up cash you don't need to.

Prioritising Your Inventory Investment

Let's be honest, not all stock is created equal. So why would you manage it all in the same way? A really effective first step is to run an ABC analysis. It sounds technical, but it’s a surprisingly straightforward way to segment your inventory based on its value.

- 'A' Items: These are your stars. The small group of high-value products that bring in the lion's share of your revenue—typically 70-80%. They need constant attention, frequent reordering, and the best forecasting you can manage. You simply can't afford to run out of these.

- 'B' Items: Your solid performers. These mid-range products are important, but they only make up about 15-25% of your revenue. You can manage them with slightly less obsessive controls than your 'A' items.

- 'C' Items: This is the long tail—the largest group of individual items that contribute the least to your revenue, maybe just 5%. For these slow-movers, you can simplify things. Order in larger batches less often and keep minimal safety stock.

By splitting your inventory this way, you can focus your time, energy, and cash where it makes the biggest difference.

Fine-Tuning Your Stock Levels

Once you know what to focus on, you can start getting the actual numbers right. This means setting realistic safety stock levels and getting much better at predicting what your customers are going to buy.

Safety stock is your buffer. It’s the backup plan for a sudden spike in demand or a supplier letting you down. The danger is being too cautious, which leads to massive overstocking. You need to base your safety stock on real sales data and supplier lead times, not just a gut feeling.

This is where demand forecasting tools come in. Many modern inventory management systems, like those that integrate with Xero, have this functionality built-in. It helps you shift from being reactive to proactive. Instead of just reordering what you sold last month, you can start to anticipate sales patterns, preventing both cash-sapping overstocking and reputation-damaging stockouts.

To get a better handle on the best inventory management technique for your specific business, it helps to compare the most common approaches.

Inventory Management Techniques Comparison

Choosing the right strategy depends entirely on what you sell and how you sell it. A business dealing with perishable goods has very different needs to one selling high-value, non-perishable items. This table breaks down the main options.

| Technique | Best For | Key Benefit |

|---|---|---|

| Just-In-Time (JIT) | Businesses with reliable suppliers and predictable demand (e.g., manufacturing, fast food). | Minimises holding costs and waste by ordering stock only as it's needed. |

| ABC Analysis | Companies with a wide range of products with varying values (e.g., retail, wholesale). | Focuses management effort on the most valuable items, optimising resource allocation. |

| First-In, First-Out (FIFO) | Businesses selling perishable goods or items with a limited shelf life (e.g., food, cosmetics). | Ensures older stock is sold first, reducing the risk of spoilage or obsolescence. |

| Dropshipping | E-commerce businesses that want to avoid holding any physical inventory. | Eliminates inventory holding costs and risk entirely; you only buy what you've already sold. |

| Economic Order Quantity (EOQ) | Companies with stable demand and predictable ordering and holding costs. | Calculates the ideal order quantity to minimise the total cost of inventory. |

By reviewing these, you can see how a manufacturer in Lanarkshire might lean towards JIT, while a speciality food retailer in Glasgow would be lost without a strict FIFO system. The key is to pick the model—or combination of models—that fits your reality.

Building Collaborative Supplier Relationships

Think of your suppliers as partners, not just vendors. Building genuine, transparent relationships can unlock incredible financial flexibility that goes far beyond just pushing for longer payment terms (which often just damages goodwill anyway).

I’m reminded of a Dundee-based food producer we work with. With perishable goods, their inventory management has to be razor-sharp. They started sharing their sales forecasts with their key packaging supplier, which allowed them to negotiate staggered deliveries. Instead of one huge, cash-draining order each quarter, they now get smaller, frequent drops that match their production runs.

That one change freed up a significant amount of cash that was previously tied up in cardboard boxes and plastic wrap, slashed their warehousing costs, and directly improved their working capital.

Here are a few practical strategies you can explore with your suppliers:

- Negotiate Better Terms: Look beyond the "net 60" deadline. Could you get a discount for paying early? Are there rebates available for hitting certain volumes?

- Explore Consignment Stock: This is a game-changer. Your supplier retains ownership of the stock while it sits in your warehouse. You only pay for it when you actually sell or use it. This can wipe huge amounts of inventory value off your balance sheet.

- Communicate Openly: Share your sales forecasts and production plans. The more visibility a supplier has, the better they can plan. That efficiency often translates into more flexibility and better terms for you.

Ultimately, getting a grip on your inventory and suppliers is a continuous cycle of refinement. By prioritising your stock, fine-tuning your levels, and working with your partners, you can turn your biggest cash drain into a major asset for a healthy, resilient business.

Using Financing to Bridge Working Capital Gaps

Even with the most efficient processes in the world, there will be times when cash flow gets tight. It happens. A large, unexpected order lands in your lap, a seasonal sales surge catches you off guard, or a major client pays later than promised. These moments can create temporary working capital gaps.

This isn't a sign of failure—it's just a normal part of running a business.

The key is to bridge these shortfalls intelligently. We're talking about using short-term financing that solves the immediate problem without saddling your business with unnecessary long-term debt. It’s about finding the right tool for the right job, giving you the flexibility to seize opportunities and navigate those inevitable bumps in the road.

Understanding Your Short-Term Financing Options

For most SMEs, there are three main avenues to explore when you need a temporary cash injection. Each one is designed for a different scenario, so getting to grips with the practical differences is crucial before you commit.

Let’s break them down:

- Business Overdrafts: An overdraft is the classic safety net. Linked directly to your business current account, it allows you to spend more than you have, up to a pre-agreed limit. It's best used for covering very short-term, unexpected expenses—a sudden bill, for instance.

- Revolving Credit Facilities: Think of this as a more formal, flexible version of an overdraft. You're given a total credit limit and can draw down, repay, and redraw funds as and when you need them. It's ideal for managing the natural ebbs and flows of your cash position throughout the year.

- Invoice Financing: This is a game-changer for many businesses. It lets you unlock the cash tied up in your unpaid customer invoices. A lender advances you a large chunk (often 80-90%) of an invoice's value almost immediately, giving you instant access to money you've already earned but are still waiting for.

Which one is right for you? It depends entirely on why you need the cash. An overdraft might cover a surprise repair bill, but invoice financing is purpose-built for businesses stuck waiting on large client payments.

Matching the Solution to the Situation

To make the right choice, you need absolute clarity on the problem you’re solving. An overdraft is wonderfully simple, but the interest rates can sting if you lean on it for too long. A revolving credit facility offers more structure and often better rates, making it a better fit for ongoing cash flow management.

Invoice financing, however, is uniquely powerful because it grows with your business. The more you sell, the more cash you can access. This makes it a superb tool for funding growth, taking on bigger contracts, or smoothing out the lumpy cash flow so common in project-based industries here in Scotland.

Using short-term finance strategically isn't about getting into debt; it's about maintaining operational momentum. It ensures you never have to turn down a great opportunity simply because you're waiting for last month's invoices to be paid.

This proactive approach to optimising working capital is vital. Poor cash management contributes to the UK's massive £2 trillion capital gap, locking money in operations instead of being put to work in productive assets. Releasing this trapped cash through smarter financing can fund investments in machinery and technology, helping to close this national productivity shortfall. A recent report dives deeper into these economic findings if you're interested.

Real-World Example: A Stirling Events Company

Picture a thriving events company based in Stirling. They often have huge upfront costs for a major conference—venue deposits, catering, staffing—but their corporate client might not settle the final invoice until 30 or even 60 days after the event is over. That creates a significant, and potentially stressful, cash flow gap.

By using invoice financing, the company can submit its large final invoice to a finance provider and receive 85% of its value within 24 hours. This immediate cash injection allows them to pay all their suppliers on time and start planning the next big project without delay.

For them, it’s not debt; it’s a strategic tool that turns a 60-day wait into a one-day wait. It completely smooths out their revenue cycle and gives them the confidence to grow. Navigating these options can be complex, and understanding the accountant’s role in business financing and loan applications is a great next step.

Got Questions? We've Got Answers

When we sit down with business owners in Glasgow, Stirling, or anywhere across Central Scotland to talk about working capital, the same questions pop up time and again. It's completely normal. Moving from the big picture to the nitty-gritty of your business's finances always brings up practical queries.

Here are the straightforward answers to the questions we hear most often.

What Does a "Good" Working Capital Ratio Actually Look Like?

Everyone wants a magic number, but the truth is, it depends. As a general rule of thumb, a current ratio (that's your current assets divided by your current liabilities) between 1.5 and 2.0 is a healthy spot for most businesses. It shows you've got enough in the tank to cover your short-term bills comfortably.

But context is king. A construction firm with long project timelines will have a totally different "good" ratio than a local cafe with rapid turnover. What's crucial is tracking your own ratio month-on-month and seeing how you stack up against others in your industry.

A ratio that's too high isn't something to brag about. It can be a red flag that you've got cash gathering dust in slow-moving stock instead of working for you. A ratio under 1.0, on the other hand, is a warning sign that cash flow problems could be just around the corner.

How Can I Chase Payments Without Annoying My Customers?

Getting your Days Sales Outstanding (DSO) down isn't about becoming a heavy-handed debt collector. It’s all about making it incredibly easy for people to pay you on time. It's a game of process, not pressure.

Here are a few things that work wonders without being confrontational:

- Invoice instantly. The minute the job is done, send a clear, accurate invoice. Don't let it sit on your desk for a week.

- Make it easy to pay. Add a payment link right on the invoice so they can pay by card in two clicks. The less hassle, the faster you get paid.

- Automate gentle reminders. Let your accounting software do the polite nudging for you. A friendly email before the due date and another just after is a simple, non-awkward way to stay top of mind.

- Offer a little thank you. A small early payment discount, even just 1-2%, can be surprisingly effective at bumping your invoice to the top of their payment pile.

Is a Higher DPO Always a Good Thing?

Not at all. While stretching out how long you take to pay suppliers (your Days Payable Outstanding, or DPO) can give you a short-term cash boost, it’s a risky game to play. Push it too far, and you can seriously damage relationships that are vital to your business.

Remember, your best suppliers are your partners. Squeezing them on payment terms can backfire badly, leading to:

- Losing out on valuable early payment discounts they might offer.

- Damaging your reputation in the local business community.

- Finding yourself at the back of the queue when stock is tight.

The goal should be to optimise your DPO, not just blindly maximise it. Pay on time, within the agreed terms, and keep the lines of communication open.

How Do Service Businesses Improve Working Capital?

If you run a service-based business—say, a marketing agency or an IT consultancy—you don't have cash tied up in physical stock. For you, the entire working capital game is about one thing: the gap between getting paid for your expertise and paying your own running costs.

Your focus should be squarely on a few key tactics:

- Bill as you go. For any project that lasts more than a month, invoice at key milestones. Don’t wait until the very end. This helps the project pay for itself along the way.

- Get a deposit upfront. This is standard practice in so many sectors, so don't be shy. Asking for a portion of the fee before work begins is a massive boost to your cash position.

- Manage your time like a hawk. In a service business, unbilled hours are the same as unsold products on a shelf. Tight project management ensures work gets done, signed off, and invoiced without delay, which directly shrinks your cash cycle.

At Stewart Accounting Services, we help businesses across Central Scotland put this theory into practice every day. If you’re ready to get a real grip on your cash flow and build a stronger, more resilient business, get in touch with our team today.