Think of your rental property like any other business. It generates income, but it also has running costs. The good news is that HMRC allows you to deduct many of these day-to-day costs from your rental income, which in turn lowers your overall tax bill.

These deductible costs are officially known as allowable expenses.

What Counts as an Allowable Expense?

At the heart of every claim is a simple rule from HMRC: the cost must be incurred "wholly and exclusively" for the purpose of renting out the property.

This is the key test for everything you want to claim. It’s what makes your landlord insurance a clear-cut deduction, but stops you from claiming for the new sofa you bought for your own living room. Getting your head around this concept isn't just about ticking boxes for the tax man; it's fundamental to running a profitable portfolio. The more legitimate expenses you track, the less tax you pay. It's that simple. To get a full picture of your obligations, it's also worth understanding How Is Rental Income Taxed? and where these expenses fit in.

The Repair vs. Improvement Test

So, how do you distinguish a deductible running cost from a non-deductible upgrade? The easiest way is to think about repairs versus improvements.

Let's use an analogy. Imagine your rental property is a car you use as a taxi.

Paying for petrol, getting the annual MOT, and replacing a worn-out tyre are all essential running costs. They keep the car on the road and earning you money. These are your allowable expenses.

But what if you decided to replace the standard engine with a high-performance one to make the car faster and more valuable? That’s not a running cost; it's a major upgrade.

This type of upgrade is what HMRC calls a capital expense. You can't deduct its cost from your rental income each year. However, you can use it to help reduce your Capital Gains Tax bill if and when you decide to sell the property.

Here's the distinction in a nutshell:

- Allowable Expenses (Revenue): These are the everyday costs of keeping the property in a lettable state. Think letting agent fees, safety certificates, and fixing a leaky tap.

- Capital Expenses (Improvements): These are costs that add something new or significantly upgrade the property, boosting its value. Building an extension or knocking through walls to create an open-plan kitchen are classic examples.

The question you always need to ask is: "Am I restoring something to its original condition, or am I creating something better?" Your answer is the key to getting your tax return right.

Distinguishing Between Repairs and Improvements

This is where things can get a bit tricky, and it's one of the most common areas where landlords slip up. Getting the distinction between a 'repair' and an 'improvement' right is absolutely vital. Why? Because a repair is an allowable expense you can deduct from your rental income right away, while an improvement is a capital expense that you generally can't.

Think of it like this: a repair is all about getting the property back to its original state. It’s maintenance. It’s fixing something that’s broken or worn out. An improvement, on the other hand, makes the property substantially better than it was before, adding real value or significantly extending its life.

For instance, if a storm blows a few tiles off the roof and you pay someone to replace them, that’s a clear-cut repair. You're just keeping the roof doing its job. But if you decide to rip off the entire old roof and replace it with a brand-new, top-of-the-line slate system, that’s a major improvement. The first is a running cost; the second is a long-term investment in the asset itself.

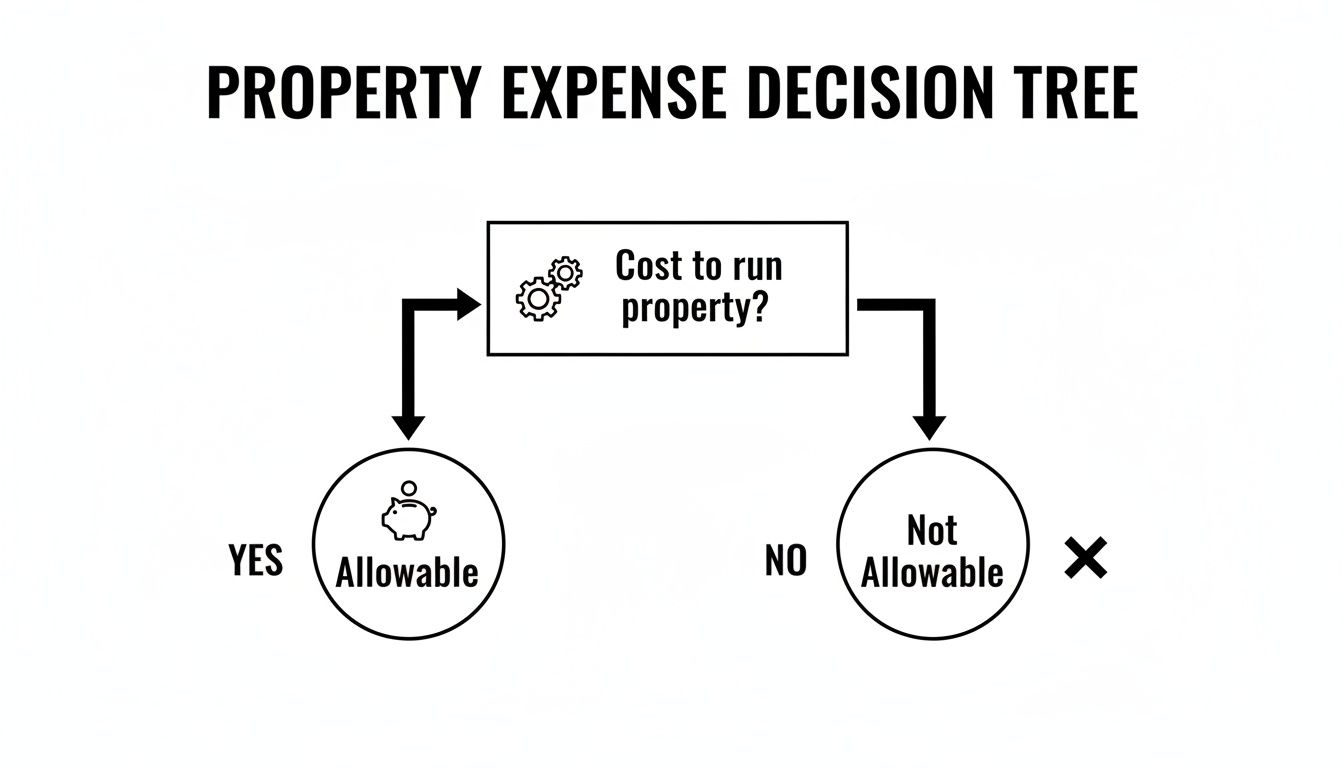

This little decision tree gets to the heart of the matter.

It boils down to a simple question: is this a cost of running the property day-to-day? If so, it’s probably allowable.

Navigating the Grey Areas

Of course, it's not always black and white. Many jobs fall into a frustrating grey area that can confuse even seasoned landlords. The trick is to look closely at what work was actually done.

Take replacing windows, a classic example. Let's say you swap out old, draughty single-glazed wooden frames for modern uPVC double-glazing. Years ago, HMRC might have viewed this purely as an improvement. These days, the guidance is much more practical. As double-glazing is now the industry standard, this is often seen as a repair – you're simply replacing an old part of the building with its modern equivalent.

The real test isn't about using new materials; it's whether you've created something fundamentally better than what was there before. Replacing a tired 1980s kitchen with a standard, modern equivalent from Howdens is likely a repair. Gutting the room and installing a high-spec designer kitchen with a different layout is an improvement.

Real-World Scenarios Explained

Let's walk through a few common situations to make this crystal clear. Seeing how these principles apply in practice will help you categorise your own spending with confidence.

The Leaky Tap: You call a plumber to sort out a dripping tap in the bathroom. They pop in a new washer, and the job’s done. This is a repair, plain and simple. It’s a minor fix to restore the tap to working order, and the cost is 100% deductible.

The Boiler Breakdown: Your ancient boiler finally gives up the ghost. You get a Gas Safe engineer to install a new, energy-efficient combi boiler in its place. This is almost always considered a repair. You aren't adding a new heating system where there wasn't one; you're just replacing a crucial component with its modern-day equivalent.

The Kitchen Overhaul: You decide the kitchen is holding the property back. You rip everything out—units, worktops, appliances—and install a brand-new, much higher quality kitchen, changing the layout to create a breakfast bar. This is a capital improvement. You've gone way beyond restoration and have significantly boosted the property's value. These costs are not allowable against your rental income.

Repair vs Improvement: A Quick-Reference Guide

To help you decide on the fly, here’s a table breaking down some common landlord jobs.

| Expense Scenario | Category | Tax Treatment |

|---|---|---|

| Repainting a room between tenancies | Repair | Fully deductible as an allowable expense. |

| Fixing a fence panel blown down in a storm | Repair | Fully deductible as an allowable expense. |

| Building a new extension or conservatory | Improvement | Not deductible; this is a capital expense. |

| Replacing a worn-out carpet with a similar new one | Repair | Fully deductible as an allowable expense. |

| Upgrading from standard lino to premium solid oak flooring | Improvement | Not deductible; this is a capital expense. |

| Rewiring the property to meet modern safety standards | Repair | Fully deductible as an allowable expense. |

By taking a moment to assess each cost against this "repair vs improvement" test, you can make sure your tax return is spot-on and that you're claiming every penny you're entitled to. It's a habit well worth getting into.

Your Checklist of Common Allowable Expenses

Alright, you’ve grasped the crucial difference between a repair and an improvement. Now, let's get down to the practical side of things. Knowing the theory is great, but what really matters is having a solid list of rental property allowable expenses so you don’t leave any money on the table.

Think of this section as your go-to checklist. If you get into the habit of tracking these costs as they happen, you'll find it makes a massive difference to your final tax bill. It’s all about keeping more of your rental income where it belongs – in your pocket.

And this isn't just small change. In the 2023-24 tax year, UK landlords claimed a staggering £29.2 billion in allowable expenses. The average landlord alone claimed £11,500 on their return. This just goes to show that diligent expense tracking isn't a minor tweak; it's a core part of running a profitable property business.

So, let's dive into the common categories you should be logging.

Professional and Financial Costs

These are the fees you pay to other professionals to help you run your rental business. The good news is they are almost always fully deductible, making them some of the easiest wins on your tax return.

Letting Agent Fees: Whether you pay an agent to find a tenant or for full-time management, those fees are an allowable expense. This covers everything from their management commission (typically 10-15% of the rent) to renewal fees and inventory checks.

Accountancy Fees: Paying an accountant to handle your rental accounts and file your Self Assessment tax return? That cost is 100% deductible.

Legal Fees: You can claim for legal help related to your rental business, like drafting a tenancy agreement or, if necessary, eviction costs. Just remember, you can't claim for the legal fees you paid when you first bought the property – HMRC views those as capital costs.

Insurance Premiums: Landlord insurance is a non-negotiable running cost. You can deduct the premiums for your buildings, contents, and public liability policies.

Property Running and Maintenance Costs

This bucket covers all the day-to-day costs of keeping the property in good shape and ready for your tenants. For most landlords, this is where a huge chunk of allowable expenses comes from.

The real secret here is consistency. A lot of these costs, like ground rent or utilities during void periods, are recurring. Setting up a simple system to track them means nothing gets missed.

The list is long, but here are some of the most common things you'll be claiming for:

General Repairs: This is everything from fixing that dripping tap and mending a faulty boiler to a fresh coat of paint between tenancies. As we’ve covered, it’s all about maintaining the property, not upgrading it.

Safety Certificates: The costs for mandatory checks are fully deductible. We're talking about the annual Gas Safety Certificate (CP12) and the Electrical Installation Condition Report (EICR).

Utility Bills: You can claim for council tax, water, gas, and electricity during any 'void periods' when the property is empty between tenants.

Service Charges and Ground Rent: If you own a leasehold property, the ground rent and any service charges you pay are allowable expenses.

Don't forget that it’s often the smaller, easily forgotten costs that add up. Finding these hidden gems can make a surprising difference, which is why we put together a guide on the 10 tax deductions UK landlords often miss.

Office and Travel Expenses

Running a rental property is a business, and HMRC gets that it comes with admin and travel costs. The golden rule is that the expense must be "wholly and exclusively" for your property business.

For instance, if you drive to your rental to carry out an inspection or meet a tradesperson, you can claim for the journey. You’ve got two ways to do this:

- Claim Mileage: The simplest way is to use HMRC's approved mileage rates. Right now, that’s 45p per mile for the first 10,000 business miles you do in a tax year.

- Claim Actual Costs: Alternatively, you can add up all your vehicle's running costs (fuel, insurance, MOT, repairs) and claim the portion that relates to your business use.

On top of travel, you can also claim for those essential admin costs:

- Stationery and Postage: Printer paper, ink, envelopes, and stamps you use for the business.

- Phone Calls: The business-use percentage of your mobile or landline bill.

- Subscriptions: Fees for joining a landlord association or subscribing to a relevant trade magazine.

By carefully logging every one of these expenses, you turn them from simple outgoings into powerful tools for cutting your tax bill. All that’s left is to keep organised records, and you’ll be set to justify every claim and maximise your return.

How Mortgage Interest Relief Works Today

The way landlords handle mortgage interest is probably one of the biggest tax shifts we’ve seen in a generation. If you were a landlord before 2017, you'll remember the old system. It was beautifully simple: you treated your mortgage interest as a standard business cost, deducting the full amount from your rental income before the taxman even got a look in.

But then came Section 24 of the Finance Act. Dubbed the "tenant tax" by many in the industry, it completely rewrote the rules. These changes were rolled out gradually between 2017 and 2020, and now, they’re the law of the land for every individual landlord in the UK.

So, what changed? Instead of directly deducting your mortgage interest from your income, you now get a tax credit. It sounds like a minor tweak in wording, but the financial sting, particularly for higher-rate taxpayers, can be immense.

The Shift From Deduction to Tax Credit

Under the new system, you have to calculate your rental profit before taking off any mortgage interest. This larger profit figure is what you declare on your tax return. Only after calculating your initial tax bill does HMRC give you a tax credit, which is fixed at 20% of your annual mortgage interest.

This is a critical change because it artificially inflates your declared income. For some landlords, this has been enough to push them into a higher tax bracket, which not only hikes up their tax bill but can also mess with their eligibility for things like Child Benefit.

Here's the bottom line: every individual landlord now gets the same 20% tax relief on their mortgage interest. It doesn't matter if you're a basic, higher, or additional rate taxpayer. This is precisely why those in the higher-rate brackets have felt the squeeze the most.

Let's walk through an example to see how this plays out in the real world.

A Worked Example: Old System vs. New

Meet Sarah, a landlord who is a higher-rate taxpayer (40%). She brings in £15,000 a year in rent and pays £5,000 in mortgage interest. For the sake of clarity, we'll ignore any other expenses.

Under the Old Rules:

- Rental Income: £15,000

- Allowable Expense (Mortgage Interest): -£5,000

- Taxable Profit: £10,000

- Tax Due at 40%: £4,000

Nice and straightforward. The interest was deducted from the top, bringing down her taxable profit.

Under the Current Rules (Section 24):

- Rental Income: £15,000

- Taxable Profit (no interest deducted): £15,000

- Initial Tax Due at 40%: £6,000

- Tax Credit (20% of £5,000 interest): -£1,000

- Final Tax Due: £5,000

Look at that difference. Sarah's tax bill has shot up by £1,000—a 25% jump—without her making a single extra penny in profit. For basic-rate taxpayers, the change is a wash because their 20% tax rate lines up perfectly with the 20% credit.

If you want to dig deeper into these mechanics, our detailed guide on the mortgage interest deduction for rental property breaks it all down.

The Limited Company Advantage

Unsurprisingly, this upheaval has prompted many landlords to rethink how they structure their portfolios. The crucial detail here is that Section 24 rules do not apply to rental properties held inside a limited company.

For a company, finance costs like mortgage interest are still treated as a fully deductible business expense. This means the company can subtract the entire interest cost from its rental income before calculating its Corporation Tax bill. Keeping an eye on the bigger picture through resources about mortgage rate cuts for landlords can also help you make smarter financial decisions in this climate.

This strategic loophole is a major reason why incorporating a property business has become such a popular move, especially for higher-rate taxpayers looking for a legitimate way to manage their tax bill more effectively.

Choosing Your Ownership Structure Wisely

The changes to mortgage interest relief, known as Section 24, have completely shaken up the tax game for landlords. This has brought one crucial question to the forefront: should you operate as an individual (a sole trader), or should you hold your properties inside a limited company? This decision goes far deeper than just finance costs; it has huge knock-on effects for your tax bill, how you get your hands on your profits, and your day-to-day paperwork.

Getting this right from the start means aligning your business structure with your personal goals. Are you playing the long game, focused on building a large portfolio for future growth? Or do you need to draw a regular income from your properties right now? Your answer will point you down one path or the other.

Individual Landlord: The Traditional Route

Operating as an individual is the most straightforward way to get started. Your rental profits are simply added on top of your other earnings (like a salary from your day job) and taxed at your personal Income Tax rate. Depending on your total income, that’ll be 20%, 40%, or even 45%.

Taking money out is simple – you just withdraw the profits. The big drawback, however, is that this is where you feel the full force of Section 24. Your mortgage interest relief is slashed to a basic 20% tax credit, even if you’re a higher-rate taxpayer. If you own property with someone else, it’s also vital you understand the rules on sharing income from jointly held property to stay compliant.

Limited Company: The Strategic Alternative

Setting up a limited company means you’re creating a completely separate legal entity that owns the properties. The company pays Corporation Tax on its profits, which is often lower than the higher rates of Income Tax. And here’s the clincher: finance costs are fully deductible as a business expense before tax is calculated, neatly sidestepping the Section 24 restrictions.

But there's a trade-off. While the tax treatment of finance costs is a huge plus, getting money out of the company is more complicated. You can’t just dip into the bank account; you have to formally pay yourself a salary (which involves PAYE) or declare dividends, both of which have their own specific tax rules and allowances.

This structure is a firm favourite for landlords who are focused on reinvesting their profits to expand their portfolio, as it’s often more tax-efficient to leave money in the company to fund the next purchase.

Property Ownership Structure At a Glance

So, how do the two structures really stack up against each other? This table puts the key differences side-by-side to help you see which might be a better fit for you.

| Feature | Individual Landlord (Sole Trader) | Limited Company |

|---|---|---|

| Tax on Profits | Income Tax at personal rates (20%, 40%, 45%). | Corporation Tax on profits (currently 19%–25%). |

| Mortgage Interest | Relief restricted to a 20% tax credit (Section 24). | Fully deductible as a business expense before tax. |

| Accessing Profits | Simple withdrawal of post-tax profits. | Must be formally extracted via salary or dividends. |

| Admin & Costs | Simpler, just a Self Assessment tax return. | More complex: annual accounts & confirmation statements. |

| Liability | Personal assets are at risk. | Limited liability protects personal assets. |

Ultimately, there's no single 'right' answer that works for everyone. If you’re a basic-rate taxpayer with one or two properties, sticking to the sole trader route is often simpler and just as effective. But if you’re a higher-rate taxpayer with ambitious plans to grow your portfolio, the tax efficiencies offered by a limited company become incredibly hard to ignore, even with the extra admin involved.

Making Your Expense Claims Bulletproof

Spotting your rental property allowable expenses is only half the job. If you can’t prove you actually spent the money, you can’t claim for it. That's why having a watertight record-keeping system isn't just a "nice-to-have" – it's the very foundation of running a tax-efficient and stress-free property business.

Think of every receipt, invoice, and bank statement as a piece of evidence. Without it, your expense claim is just a number on a form, and one that HMRC can easily challenge. The old shoebox full of crumpled receipts might have been a running joke in the past, but it simply won't cut it anymore.

The Digital Advantage in Record Keeping

These days, savvy landlords are moving their financial records to the cloud, and for very good reasons. Using cloud accounting software like Xero or QuickBooks is no longer just for big businesses; it’s fast becoming a necessity for landlords too. These platforms don't just store your receipts – they can categorise your spending as it happens, giving you a real-time picture of your profitability.

Going digital isn't just about convenience, either. It’s about getting ready for the future of tax.

Making Tax Digital (MTD) for Income Tax is just around the corner, set to kick in from April 2026 for landlords with income over £50,000. This will require you to keep digital records and send quarterly updates to HMRC. Getting on board with the right software now puts you miles ahead of the curve.

Organising your finances digitally brings some brilliant benefits:

- Instant Access: Need to find that plumber's invoice from six months ago? You can pull it up in seconds, from anywhere.

- Fewer Errors: Automation drastically cuts the risk of typos and manual data entry mistakes that can cost you money.

- Simpler Tax Returns: Most good software can generate the exact reports your accountant needs, saving them time and you money on their fees.

How to Claim Your Expenses on a Tax Return

Once you've got all your records neatly organised, the final step is declaring everything correctly on your Self Assessment tax return. For most individual landlords, this means filling out the SA105 ‘UK Property’ pages, which is a supplement to your main tax return.

It sounds more daunting than it is. You'll be asked for your total rental income, and then you'll list the totals for your allowable expenses, broken down into a few categories. Here’s a quick rundown of the process:

- Gather Your Totals: At the end of the tax year, add up all your rental income and your expenses, separated by category (e.g., repairs, professional fees, etc.).

- Complete the SA105 Form: You’ll enter your total expenses into the relevant boxes, like 'Property repairs and maintenance' or 'Legal, management and other professional fees'.

- Calculate Your Profit: The form guides you through subtracting your total expenses from your total income. This gives you your net profit (or loss).

- Transfer to Your Main Return: This final profit figure is what you carry over to your main SA100 tax return. It's then used to work out your overall tax bill for the year.

While the process itself is logical, it's the meticulous record-keeping throughout the year that makes it painless. It turns tax time from a frantic scramble through piles of paper into a straightforward administrative task, ensuring you claim every single penny you're entitled to – and can prove it.

Landlord FAQs: Your Rental Expense Questions Answered

When you get down to the nitty-gritty of managing a rental property, you’ll inevitably run into some specific questions about expenses. You can know the rules inside-out, but certain real-world situations always seem to fall into a grey area. Let’s clear up some of the most common queries we get from landlords.

Think of this as tying up the loose ends. Getting these details right not only keeps you compliant with HMRC but also makes sure you’re taking full advantage of every deduction you're entitled to.

Can I Claim for Expenses When My Property is Empty?

Yes, you absolutely can. Just because the property is empty doesn't mean your business has stopped. You can, and should, claim for the day-to-day running costs you incur during these 'void periods', as long as the property is still being advertised and is available to let.

These are simply the ongoing costs of keeping the property ready for your next tenant. Common examples include:

- Council tax

- Standing charges for utilities like gas and electricity

- Landlord insurance premiums

- Ground rent or service charges on a leasehold flat

Basically, if it's a cost you'd have to pay anyway (apart from things like letting agent fees, which are obviously tied to having a tenant), it's almost certainly still a valid business expense.

What Is This "Replacement of Domestic Items Relief"?

This is a crucial one for anyone letting a furnished or part-furnished property. It’s the tax relief you get for replacing things like sofas, beds, fridges, or even curtains and carpets. The key thing to remember is that you can only claim for the replacement, not the initial cost of furnishing the property from scratch.

The rule is based on a like-for-like replacement.

For instance, imagine your tenant’s £400 fridge gives up the ghost. You replace it with a similar model that costs £450. You can claim relief on the £400 – the cost of an equivalent replacement. That extra £50 is seen as an 'improvement' by HMRC, so you can't claim it.

Can I Claim for My Travel to and from the Property?

You can, but there’s a big condition attached: the trip must have been made 'wholly and exclusively' for the purpose of your property business. Driving over to meet a plumber, conduct a six-month inspection, or show a prospective tenant around are all perfect examples.

You can claim for fuel using HMRC's approved mileage rates (currently 45p per mile for the first 10,000 miles) or claim the actual cost of a train or bus ticket. What you can't do is mix business with pleasure. If you’re driving to see family and just happen to pop by the rental on the way, that journey doesn't count.

Do I Really Need to Hire an Accountant for Just One Rental?

Legally, no. Practically, it’s one of the smartest investments a landlord can make. The rules around property tax, from allowable expenses and mortgage interest relief to Capital Gains Tax, are notoriously complicated and constantly changing.

A good, specialist accountant does more than just fill in a form. They'll make sure you’re 100% compliant, find every legitimate deduction to improve your net profit, and offer advice to help you structure your portfolio tax-efficiently for the future. More often than not, they save you far more money than their fee costs, not to mention the time and stress.

Managing rental property finances can be complex, but you don't have to do it alone. The team at Stewart Accounting Services provides expert guidance to landlords across Central Scotland and the UK, ensuring you claim every allowable expense and run your portfolio as profitably as possible. Learn how we can help you today.