At its core, reverse charge VAT is a simple flip of responsibility. Normally, the person selling you something charges you VAT and then pays that money to HMRC. With the reverse charge, that responsibility shifts from the supplier to you, the customer.

You calculate and pay the VAT directly to HMRC on behalf of your supplier. In your VAT return, you effectively act as both the seller and the buyer.

How Reverse Charge VAT Works

Think of it like a game of 'pass the parcel' with a tax payment. Usually, the seller hands you a parcel and collects the tax money for HMRC. The reverse charge changes the rules. The seller hands you the parcel without the tax, and it becomes your job to sort out the VAT directly with the tax man.

So, why does this system exist? It was brought in for a couple of key reasons: to make VAT accounting easier for cross-border transactions and to tackle VAT fraud in certain high-risk industries. It changes who pays the VAT, but it doesn't change the amount of VAT that’s due.

Who Handles What: A Comparison

Let's break down the difference between the standard process and the reverse charge mechanism. Getting this straight is the first step to keeping your business compliant.

| Responsibility | Standard VAT Rules | Reverse Charge VAT Rules |

|---|---|---|

| Supplier's Invoice | Includes VAT amount (e.g., 20%). | Excludes VAT but must clearly state that the reverse charge applies. |

| Who Pays VAT to HMRC | The supplier collects VAT from the customer and pays it to HMRC. | The customer calculates the VAT and pays it directly to HMRC. |

| VAT Return Entry | Supplier declares output VAT. Customer reclaims input VAT. | Customer declares both output and input VAT on the same return. |

This dual entry by the customer is the crucial part of the process. You declare the VAT as if you made the sale (output VAT) and then claim it back as if you made the purchase (input VAT).

For most VAT-registered businesses that can fully reclaim their VAT, these two entries simply cancel each other out. The net effect on your VAT bill is zero. It's a crucial concept, and you can dive deeper into the basics in our guide to output and input VAT.

When Does Reverse Charge VAT Apply?

The rules aren't random; they only apply in very specific situations that many UK businesses will run into sooner or later. This isn't something you can opt into—it's mandatory if your transaction fits the criteria.

The two most common scenarios for UK businesses are:

- Receiving services from overseas suppliers: This comes up all the time with digital services. Think software subscriptions from the US, advertising spend with a company in Ireland, or consultancy from a firm in the EU.

- Domestic transactions in specific industries: The big one here is the construction industry. The reverse charge for certain building services was introduced specifically to combat fraud.

The key takeaway is simple: Reverse charge VAT doesn't alter the final amount of tax owed to HMRC. It only changes the administrative responsibility, shifting the reporting duty from the seller to the buyer to increase transparency and reduce fraud.

When and Why Does Reverse Charge VAT Apply?

Knowing exactly when the reverse charge mechanism kicks in is non-negotiable for staying compliant. It’s not something you can opt into or out of; if a transaction fits the criteria laid out by HMRC, you’re legally required to use it. The rules are designed for very specific situations, mainly targeting services bought from overseas and certain domestic sectors where VAT fraud has been a persistent problem.

For most UK businesses, this boils down to two key scenarios. The first, and most common, involves buying services from suppliers located outside the UK. The second is the domestic reverse charge, which has had a huge impact on the UK construction industry since its introduction. Let's break down both to see when the rules apply to you.

Cross-Border Services From Overseas Suppliers

This is the trigger most small and medium-sized businesses will encounter. If your UK-based, VAT-registered company buys services from a supplier in another country, the responsibility for handling the VAT typically falls on you. It’s a clever way to ensure that UK VAT is paid on services that are effectively ‘used’ in the UK, even when the seller is miles away.

You've probably come across this more often than you think. Common examples include:

- Digital Marketing: Hiring a social media agency based in the EU or an SEO specialist from the US.

- Software Subscriptions: Paying for tools like Adobe (often billed from Ireland) or cloud storage from a US provider.

- Professional Advice: Engaging consultants, architects, or lawyers from overseas for their expertise.

In these situations, the overseas supplier shouldn't charge you their local VAT. Their invoice should arrive without VAT added, often with a note saying something like "subject to reverse charge". It's then up to you to calculate the UK VAT at the correct rate (usually 20%) and report it on your VAT return.

The whole point is to create a level playing field. The reverse charge stops overseas suppliers from having an automatic price advantage over UK suppliers, as UK VAT gets accounted for no matter where the seller is based.

The Domestic Reverse Charge for Construction

While the cross-border rule is quite broad, the domestic reverse charge is razor-focused. It was brought in to tackle a specific type of VAT fraud that was rampant in the UK construction industry. The long supply chains in this sector were being exploited by "missing traders" – subcontractors who would charge VAT, collect the cash, and then disappear before paying it over to HMRC.

The domestic reverse charge flips this on its head by moving the VAT responsibility up the chain to the main contractor, making that kind of fraud almost impossible. From 1 March 2021, HMRC made this mandatory for most building and construction services, affecting thousands of businesses. You can read more about the broader VAT regulations in the United Kingdom to see how this fits in.

This rule applies to specific services that fall under the Construction Industry Scheme (CIS), such as:

- Building, altering, repairing, or demolishing buildings.

- Site clearance and groundworks.

- Internal work like painting and decorating.

- Installing heating, lighting, or water systems.

But here’s the crucial part: there are big exceptions. The reverse charge does not apply if you’re supplying the service to an ‘end user’ or an ‘intermediary supplier’ linked to one. An end user is simply the final customer—the person or business that will use the construction service themselves, not sell it on. A classic example is a retailer hiring a builder to refurbish their shop; they are the end user.

This is why communication is key. Before you send an invoice, you absolutely must confirm your customer's status. If they’re an end user, you charge VAT the normal way. If they're not, the reverse charge VAT must be applied. Getting this distinction right is the biggest hurdle for most construction firms.

To make things clearer, here is a quick reference table to help you spot when the reverse charge might apply.

Reverse Charge Triggers At-a-Glance

| Scenario | Is Reverse Charge VAT Applicable? | Who Accounts for the VAT? | Example |

|---|---|---|---|

| UK business buys software subscription from an Irish company | Yes | The UK business | A marketing agency in Manchester pays for a project management tool billed from Dublin. |

| UK contractor invoices a UK developer (not the end user) | Yes (Domestic Reverse Charge) | The UK developer (the customer) | A scaffolding firm invoices a main contractor for work on a new housing development. |

| UK plumbing firm invoices a homeowner for a new bathroom | No | The UK plumbing firm (the supplier) | The homeowner is the 'end user', so normal VAT rules apply. |

| UK business buys consultancy from a US firm | Yes | The UK business | A London-based fintech company hires a New York consultant for market research. |

This table covers the most frequent scenarios, but remember to always check the specific details of your transaction if you're ever in doubt.

Seeing Reverse Charge in the Real World

Theory is one thing, but the best way to really get your head around reverse charge VAT is to see how it works day-to-day. Once you walk through the steps, the whole process starts to make a lot more sense.

Let's break down two very common situations UK businesses run into: buying digital services from an overseas company and a typical job within the construction industry.

Example 1: Buying Digital Services from Abroad

Picture this: your UK marketing agency, "Bright Spark Ltd," signs up for a project management tool from a company based in Ireland. The subscription is £100 a month. Because this is a business-to-business (B2B) service supplied from the EU to the UK, the reverse charge kicks in.

The invoice that lands in your inbox from the Irish software firm will look a bit different from your usual UK supplier invoices.

- Net Amount: £100.00

- VAT Charged: £0.00

- Total Payable: £100.00

- Invoice Note: "Reverse charge: Customer to account for VAT to HMRC."

Bright Spark Ltd pays the £100, but that’s not the end of the story. Now, you have to do the VAT accounting on your side.

How to Calculate and Record the VAT

First, you need to work out the UK VAT that would have been due if you'd bought the software from a UK company. At the standard rate of 20%, that's £20 (£100 x 0.20).

On your VAT return, you'll make two entries that mirror each other:

- You declare £20 of output VAT in Box 1, almost as if you sold the service to yourself.

- You then reclaim that same £20 as input VAT in Box 4, just like any other business purchase.

The result? The two entries cancel each other out, so the net effect on what you owe HMRC is zero. This clever little loop ensures VAT is paid in the UK where the service is being used, without forcing the Irish supplier to go through the hassle of registering for UK VAT.

Example 2: A Domestic Construction Job

Now, let's switch over to the UK construction sector, where the domestic reverse charge is part of daily life for many.

Imagine a main contractor, "BuildRight Contractors," hires a VAT-registered subcontractor, "Sparks Electrical," to handle the wiring for a new office development. The job is worth £10,000.

Because BuildRight Contractors isn't the final customer (they'll be selling the completed building to their client), the domestic reverse charge rules apply to this transaction.

Sparks Electrical sends their invoice to BuildRight, but here's the crucial part: they do not add VAT to it.

- Net Amount: £10,000.00

- VAT Charged: £0.00

- Total Payable: £10,000.00

- Invoice Note: "Reverse charge: VAT Act 1994 Section 55A applies. Customer to pay the VAT to HMRC."

BuildRight pays the £10,000, and just like our first example, the responsibility for handling the VAT now sits with them.

The whole point of the domestic reverse charge is to tackle "missing trader" fraud. By shifting the VAT accounting from the subcontractor to the main contractor, it stops a scenario where a subbie could charge VAT, pocket the cash, and then disappear before paying it over to HMRC.

The Contractor's VAT Return

BuildRight Contractors has to calculate the VAT on the £10,000 service, which comes to £2,000 (£10,000 x 20%). They then report it on their VAT return like this:

- Box 1 (Output VAT): The £2,000 is added to the total VAT due on their sales.

- Box 4 (Input VAT): They reclaim the same £2,000 as input VAT on their purchases.

- Box 7 (Net Purchases): The £10,000 net value of the service is included here.

And what about Sparks Electrical? Their side is simpler. They just record the net sale of £10,000 in Box 6 of their VAT return and don't put anything in Box 1 for this transaction. As you can see, while the name sounds complicated, the actual accounting is just a logical, step-by-step procedure.

Getting Your Invoicing and VAT Returns Right

Knowing what the reverse charge is one thing, but getting the paperwork right is what really matters. This is where theory meets practice, and it’s crucial for keeping your accounts tidy and staying on the right side of HMRC.

Getting this wrong can lead to some serious headaches, like paying the wrong amount of VAT or facing awkward questions from the tax man. The whole process really boils down to two things: wording your invoices correctly and putting the right numbers in the right boxes on your VAT return. Let's break down exactly how to do that.

How to Word Your Invoices

When you’re the one issuing an invoice that falls under the reverse charge, you have to be crystal clear that the VAT responsibility is now on your customer’s shoulders. Vague notes just won’t cut it; HMRC has specific requirements.

If you're the supplier, here’s what your invoice needs to show:

- No VAT charged: The VAT amount on your invoice should be £0. You're only invoicing for the net cost of your services or goods. Don't add the 20% VAT like you normally would.

- A specific note: This is the most important part. You must add a clear statement to the invoice. HMRC gives a couple of options, and something like this works perfectly:

- "Reverse charge: customer to pay the VAT to HMRC."

- "Reverse charge: VAT Act 1994 Section 55A applies."

This little line is a non-negotiable legal instruction. It tells your customer, "Over to you – you need to handle the VAT on this one." If you want a refresher on general invoicing rules, our guide on what should be on a VAT invoice is a great place to start. And if you're ever unsure, it’s worth understanding the nuances between a receipt and an invoice to avoid common mix-ups.

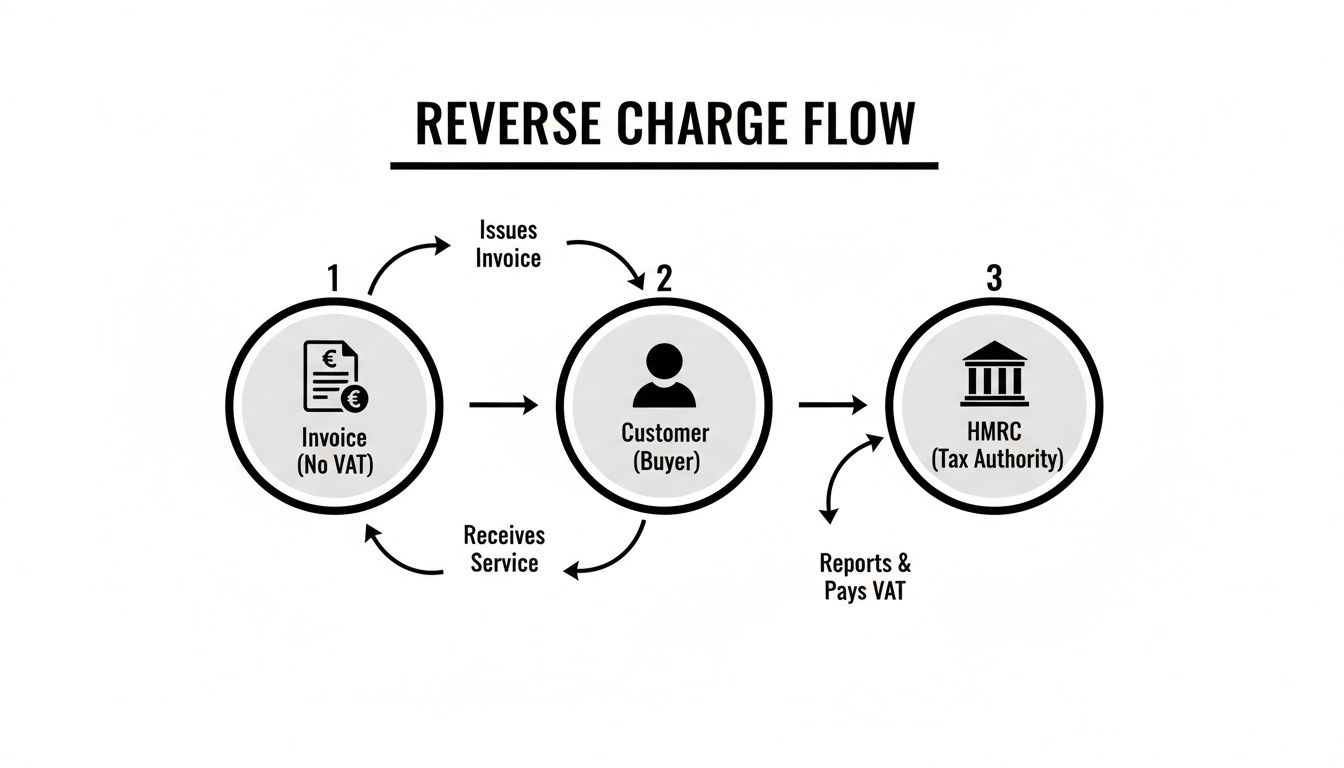

This diagram helps visualise how the responsibility shifts from the supplier to the customer and then to HMRC.

As you can see, the supplier steps back from collecting VAT, and the customer steps in to account for it directly on their own tax return.

Filling Out Your VAT Return

Now, let's look at the other side of the coin: you’re the customer who has received a reverse charge invoice. Recording it on your VAT return can feel a bit strange at first, almost like you're acting as both your own customer and supplier.

Here’s the box-by-box guide for you, the customer, filling out your UK VAT return:

- Box 1 (Output VAT): You need to calculate the VAT on the service you've received and add it here. This is the VAT you would have paid the supplier.

- Box 4 (Input VAT): Enter the exact same amount of VAT here. This is you reclaiming the VAT on the purchase.

- Box 6 (Total Sales): Nothing goes in here for this transaction. That’s the supplier’s job.

- Box 7 (Total Purchases): Pop the net value of the goods or services (the amount on the invoice) in this box.

For the vast majority of businesses, the figures in Box 1 and Box 4 will be identical. This creates a net-neutral effect on your VAT bill for this specific transaction. The output VAT you declare is instantly cancelled out by the input VAT you reclaim, so no actual cash has to be paid over to HMRC.

Making Cross-Border Trade Simpler

The reverse charge isn't just about clamping down on fraud; it’s also a brilliant tool for simplifying international trade. If you're a UK business with your sights set on European markets, getting your head around this is more than just a box-ticking exercise—it’s a real strategic advantage. It strips away a lot of the admin that can make expanding abroad feel like a nightmare.

Think about it. Let's say your UK consultancy lands a project with a client in France. Without the reverse charge, you could be looking at having to register for French VAT, wrestle with a foreign tax system, and file returns in another language. It's often complicated, expensive, and a huge time-sink, especially for smaller businesses.

The reverse charge neatly sidesteps all of that. By making your French business customer responsible for handling the VAT on their end, you can provide your services without ever needing to register for VAT in France. This simple shift makes trading across borders far more straightforward and a lot less costly.

A Joined-Up Approach to EU Trade

This isn't just a happy accident; it's a deliberate system put in place by countries across the EU, including big players like France and Italy. The whole point is to modernise VAT and create a smoother, more unified trading environment for everyone.

By making it easier for companies to trade without getting bogged down in multiple VAT registrations, the EU is building a more competitive and integrated single market. For a UK business, this is great news. The principles you learn for dealing with one EU country will often apply to others, making it much easier to scale your expansion plans.

And the system is still evolving. The use of the domestic reverse charge, both in the UK and across the EU, is a key part of the strategy for managing cross-border VAT. A significant wave of changes is coming, with mandatory implementation starting from 1 January 2025 as part of a wider EU VAT modernisation push. These updates are designed to seriously cut down the admin burden of EU trade and improve VAT compliance overall. You can read more about these upcoming EU VAT changes on Tax Adviser Magazine.

What's Changed for UK Businesses After Brexit?

Things have obviously shifted since Brexit, but the core ideas are still incredibly relevant. The UK is no longer inside the EU VAT area, but the reverse charge still applies to many services you buy from the EU. At the same time, many UK businesses now export goods to the EU, which brings its own set of customs and VAT rules into play.

For ambitious UK business owners, understanding these rules changes everything. It turns Europe from a tangled mess of tax laws into an open, accessible market. VAT stops being a barrier and becomes just another manageable part of your growth plan.

Getting to grips with how VAT works on international sales is non-negotiable. For a deeper dive into this, take a look at our article on VAT on goods you export, which clarifies the post-Brexit trading landscape. This knowledge will help you price your services competitively and operate smoothly across the European market.

Common Mistakes to Avoid and A Compliance Checklist

Reverse charge VAT can feel like a minefield. It’s one of those areas where a simple misunderstanding can quickly snowball into a compliance headache or, worse, a sudden cash flow problem. Having been in the trenches with businesses navigating this, we've seen the same few tripwires catch people out time and time again. The key is to spot them before they become an issue.

One of the classic blunders we see is a supplier charging VAT out of sheer habit, even when the reverse charge applies. It's an easy mistake to make, but it creates a real mess that needs unpicking. On the flip side, we often see the customer receive a reverse charge invoice, pay the net amount, and then completely forget to handle the VAT on their own return. They miss that crucial two-step accounting entry, leaving a hole in their records.

The construction industry has its own unique trap: confusion over who qualifies as an ‘end user’. A subcontractor might assume their client is an intermediary and apply the reverse charge, only to find out they were the final customer all along. A quick chat to clarify status before the invoice goes out can save a world of pain.

Common Pitfalls at a Glance

To keep things straight, here’s a quick rundown of the errors that pop up most often:

- Supplier Error: Slapping VAT on an invoice for a service that absolutely falls under the reverse charge rules.

- Customer Oversight: Forgetting to declare the output VAT and reclaim the input VAT on their VAT return. This breaks the entire accounting chain.

- Incorrect Invoicing: Missing that all-important phrase on the invoice, like "Reverse charge: customer to pay the VAT to HMRC."

- Construction Confusion: Getting a customer's 'end user' or 'intermediary supplier' status wrong, which leads to completely incorrect VAT treatment.

Staying compliant with reverse charge VAT isn't about memorising every line of the tax code. It's about building a solid, repeatable process. A simple checklist can shift you from constantly putting out fires to confidently managing your VAT obligations.

Your Essential Compliance Checklist

Run through this checklist every time you handle a reverse charge transaction. Think of it as your pre-flight check to ensure everything is handled correctly and you avoid those costly mistakes.

- Verify the Service: First things first, is this service actually on HMRC’s list for the domestic reverse charge (like construction), or is it a B2B cross-border service? If not, normal VAT rules apply.

- Check VAT Registration: Always make sure both you and your customer or supplier are VAT registered. The reverse charge doesn't apply if one party isn't.

- Confirm Customer Status (Construction): If you're in construction, get written confirmation of your customer's 'end user' or 'intermediary' status. Don't just assume—get it in writing before invoicing.

- Ensure Correct Invoice Wording: Take a moment to read your invoice. Does it clearly state that the reverse charge applies and that the customer is responsible for the VAT?

- Review VAT Return Entries: Before hitting ‘submit’ on your VAT return, do a final check. For the customer, are the figures correctly entered in Boxes 1, 4, and 7? For the supplier, is the net sale recorded in Box 6?

Your Reverse Charge VAT Questions Answered

It's natural to have questions when you're getting to grips with the reverse charge rules. Let's tackle some of the most common ones we hear from business owners.

What Happens if I Forget to Apply the Reverse Charge?

Forgetting to apply the reverse charge is an easy mistake to make, but it's one you need to fix quickly.

If you’re the supplier and you've wrongly charged VAT on an invoice, you can't just ignore it. You'll need to issue a credit note to cancel the incorrect invoice, then raise a new one that correctly states the reverse charge applies. Crucially, you're still on the hook for paying the VAT you mistakenly charged over to HMRC.

If you’re the customer and you've forgotten to account for it on your VAT return, you should correct the error as soon as you spot it. This usually means adjusting your next VAT return to include the output and input tax you missed. Acting promptly is the best way to avoid any potential trouble with HMRC.

Does the Reverse Charge Affect My Eligibility for the Flat Rate Scheme?

Yes, absolutely – and the impact is significant. If you provide services that fall under the domestic reverse charge, you must exclude that income from your Flat Rate Scheme turnover. Those sales have to be accounted for using standard VAT rules, not your flat rate percentage.

On the flip side, when you buy services subject to the reverse charge, you still need to account for them on your VAT return, but they won't affect your turnover calculation for the scheme. This added complexity often means the Flat Rate Scheme is no longer a good fit for businesses in sectors like construction.

How Does Reverse Charge Impact Cash Flow?

The effect on your cash flow really depends on whether you're the supplier or the customer.

For the supplier, the change can be a real headache, especially for subcontractors in the construction industry. You no longer receive the VAT payment from your customer, which many businesses rely on as part of their working capital until their own VAT bill is due.

For the customer, the impact is usually neutral, or even a slight positive. You aren't paying VAT out to your supplier and then waiting for months to reclaim it. The whole thing becomes an accounting exercise on your VAT return, which can free up cash in the short term.

Navigating the complexities of VAT is what we do best. If you're struggling with the reverse charge or any other part of your business finances, get in touch with our expert team at Stewart Accounting Services today for clear, practical support.