Deciding to set up as a sole trader is often the simplest and quickest way to get your business off the ground in the UK. It's a popular choice, and for good reason. It means you're the exclusive owner, keeping all the profits after tax, but it also means you're personally on the hook for any debts.

Is Becoming a Sole Trader the Right Path for You?

Choosing your business structure is one of the very first, and most important, decisions you'll make. It’s a choice that will shape everything from how you pay tax to the level of financial risk you’re exposed to personally. While the simplicity of being a sole trader is a massive draw, it’s vital to understand what you’re signing up for before you jump in.

The main appeal for many new business owners is the straightforward, low-cost setup. You don't have to deal with the formal registration process at Companies House, and your ongoing admin is much lighter compared to running a limited company. You're the boss, plain and simple. You make all the decisions, and there's no board of directors to answer to.

Understanding Unlimited Liability

But that complete control comes with a very important catch: unlimited liability. This is the single most critical point to get your head around.

As a sole trader, the law makes no distinction between you and your business. From a legal standpoint, you are the business.

This means if your business runs into financial trouble or faces a lawsuit, your personal assets—your house, your car, your savings—could be used to pay off those debts. For someone like a freelance writer with minimal startup costs, the risk might feel quite low. But if you're a builder taking on big contracts and hiring expensive equipment, the potential for things to go wrong is much higher.

Sole Trader or Limited Company?

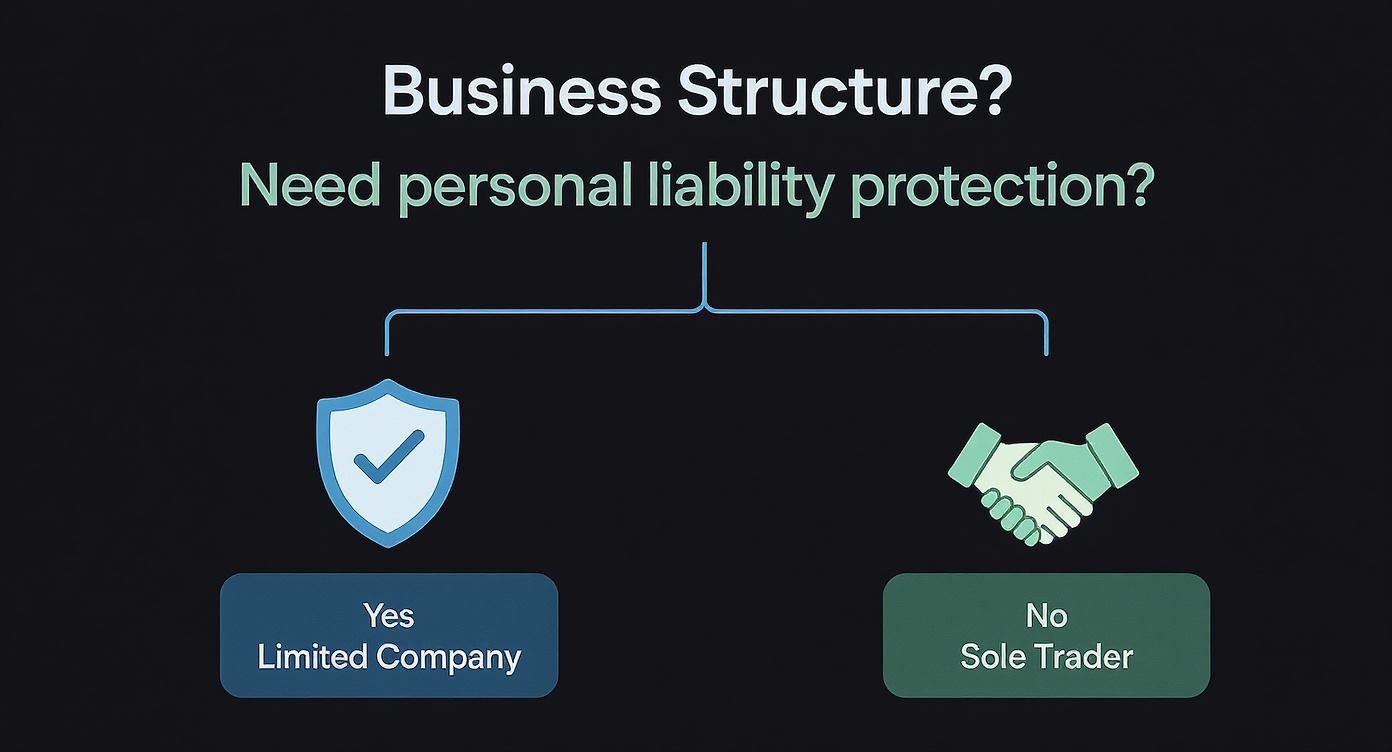

The main alternative is to set up a limited company. This creates a completely separate legal entity, which shields your personal finances through 'limited liability'. The company is responsible for its own debts, not you personally (though there are exceptions, like if you've signed a personal guarantee for a loan).

Ultimately, the decision often comes down to one question: How much personal financial risk are you comfortable with? Your answer will likely depend on your line of work, your growth plans, and your own peace of mind.

This simple flowchart breaks down that core consideration.

As you can see, if protecting your personal assets is a top priority, a limited company is usually the way to go.

To help you compare the two structures at a glance, here’s a breakdown of the main differences.

Sole Trader vs Limited Company Key Differences

| Feature | Sole Trader | Limited Company |

|---|---|---|

| Legal Status | You and the business are a single legal entity. | The company is a separate legal entity from you. |

| Liability | Unlimited liability – your personal assets are at risk. | Limited liability – personal assets are protected. |

| Registration | Register for Self Assessment with HMRC. | Incorporate with Companies House and register with HMRC. |

| Admin & Privacy | Simpler accounts, less paperwork. Details are private. | More complex accounts and reporting. Director/company details are public. |

| Tax | You pay Income Tax and Class 2 & 4 National Insurance. | You pay Corporation Tax. You extract profits via salary (PAYE) and dividends. |

| Credibility | Can be perceived as smaller or less established. | Often perceived as more professional or credible. |

This table covers the basics, but there are nuances to each point depending on your specific circumstances.

The sole trader model is still incredibly popular, and for good reason. It's the engine of the UK's small business economy. In fact, sole traders make up about 57% of the entire private sector business population, with around 3.2 million of them operating across the country. It just goes to show how well this structure works for a huge number of people.

If you're still weighing things up, our more detailed comparison can give you the clarity you need. Take a look at our guide on choosing between a sole trader or limited company to help make a fully informed decision. Here at Stewart Accounting Services, we can walk you through the pros and cons for your specific situation to make sure you start out on the right foot.

Getting Registered with HMRC (Without the Headache)

So, you've decided the sole trader life is for you. Great! The next big step is making it official with HM Revenue & Customs (HMRC). This is where your business idea stops being just an idea and becomes a real, recognised entity in the eyes of the taxman. It might sound a bit formal and intimidating, but honestly, it’s more straightforward than you might think.

Registering simply tells HMRC you've started earning money for yourself and that you'll be paying tax on your profits through Self Assessment. It’s a legal must-do, and getting it sorted early sets you off on the right foot.

First Things First: What Are You Going to Call Your Business?

Before you even think about filling in a form, you need a name. As a sole trader, you’ve got plenty of freedom here, but there are a few ground rules to keep in mind.

You could simply trade under your own name – "Jane Smith, Graphic Designer," for instance. It's simple, direct, and does the job perfectly.

Or, you could get a bit more creative with a business name like "Peak Performance Fitness." If you go this route, just be careful not to:

- Use words like "Limited," "Ltd," "LLP," or "PLC." These are legally reserved for specific company types and will get you into hot water.

- Pick a name that’s already a registered trademark. A quick Google search and a check on the Intellectual Property Office website can save you a world of pain later.

- Include 'sensitive' words like 'Bank', 'Royal', or 'Chartered' unless you have the official permission to do so. These suggest official standing you don't have.

- Choose something offensive. This should go without saying!

A good name is clear, professional, and gives people a clue about what you do. It's the first brick in building your brand.

The Registration Process and That All-Important Deadline

The actual registration happens online over at the GOV.UK website. You’ll need to set up a Government Gateway account if you haven’t got one already – this will become your main hub for all things tax-related.

This is the official GOV.UK page where you’ll kick off the process to set up as a sole trader.

As you can see, the government lays out the steps pretty clearly. The key to a smooth ride is having all your information handy before you start.

You'll need a few basic details:

- Your full name and home address

- Your National Insurance number

- The date you officially started trading

- Your business name and a simple description of what you do

Crucial Deadline: You must register with HMRC by 5th October in your business's second tax year. For example, if you start your business in August 2024 (the 2024/25 tax year), your deadline to register is 5th October 2025. Don't put it off!

Missing that deadline can lead to fines, so my advice is always to register as soon as you're up and running. It’s one less thing to worry about.

Say Hello to Your UTR Number

Once you’re registered, HMRC will pop a letter in the post containing your Unique Taxpayer Reference (UTR). This is a 10-digit number that’s yours and yours alone.

Think of your UTR as your business's most important piece of ID. You'll need it for just about everything you do with HMRC, especially when it's time to file your annual Self Assessment tax return. Keep it somewhere safe – you’ll need it every single year. A great way to keep everything organised is to set up your tax app with HMRC, which makes your details easily accessible.

Getting registered is a huge milestone. It’s the moment you become a proper business owner and puts you on the path to managing your taxes correctly from day one. If any part of this feels overwhelming, remember you don't have to go it alone. At Stewart Accounting Services, we guide new sole traders through this exact process every day, making sure it’s all done right, the first time.

Getting to Grips with Tax and National Insurance

Alright, you’re registered. Now it’s time to tackle the money side of things. Honestly, understanding your tax and National Insurance obligations isn't as scary as it sounds. It’s less about crunching complex numbers and more about getting familiar with the rules of the road.

As a sole trader, the profit your business makes is considered your personal income. It's that simple. HMRC taxes you on that profit figure, which is your total business income minus all your allowable business expenses. Getting this concept right from the start is fundamental when you set up as a sole trader, as it directly affects what you actually take home.

Decoding Income Tax for Sole Traders

Every UK resident has a Personal Allowance—that’s the amount you can earn in a tax year before you pay a penny of Income Tax. For the 2024/25 tax year, this figure stands at £12,570. You only start paying tax on profits that go above this amount.

Once your profits exceed your Personal Allowance, they fall into different tax bands, each with its own rate.

Here's a quick look at the rates for England, Wales, and Northern Ireland (Scotland has its own bands, which are a bit different):

- Basic Rate: 20% on profits between £12,571 and £50,270.

- Higher Rate: 40% on profits between £50,271 and £125,140.

- Additional Rate: 45% on any profits over £125,140.

Let's say you make a profit of £30,000. The first £12,570 is tax-free. You'll only pay 20% tax on the remaining £17,430. The system is designed to be progressive, so your tax bill grows as your business succeeds.

Understanding Your National Insurance Contributions

When you're self-employed, you'll generally be dealing with two types of National Insurance Contributions (NICs). Don't just see these as another tax; these payments build your entitlement to the State Pension and other key benefits, like Employment and Support Allowance.

Class 2 National Insurance

This used to be a small, flat-rate weekly payment. For the 2024/25 tax year, Class 2 NICs became voluntary for those with profits over £12,570. However, it's still crucial to pay them if you want to keep your contribution record intact for your State Pension. For those with profits between £6,725 and £12,570, you get the credit automatically without having to pay.

Class 4 National Insurance

This one is directly linked to your profits. You pay a percentage on your annual profits once they cross a certain threshold.

Your Class 4 contributions are calculated based on your profits, meaning you only pay this if your business is performing well. It’s directly linked to your success, unlike the flat-rate Class 2 payments.

For a clearer picture of how Class 4 NICs work and the latest rates, we've broken it down further. You can learn more about paying Class 4 NICs on our dedicated page. Staying on top of these payments is a non-negotiable part of managing your finances well.

The last few years have really driven home how important this system is. During the COVID-19 pandemic, government support like the Self-Employment Income Support Scheme (SEISS) was a lifeline for millions. In the first round alone, there were 2.7 million claims, which shows just how vital this safety net was. You can dig into more data on the resilience of the UK's self-employed workforce on Statista.com.

The Self Assessment Process and Payments on Account

So, how do you actually sort all this out with HMRC? Through Self Assessment. Every tax year, you need to complete a tax return, which is where you declare your income and your business expenses. The deadline for getting this filed online is usually 31st January.

One of the biggest tripwires for new sole traders is a concept called Payments on Account. If your tax bill from Self Assessment is over £1,000, HMRC doesn’t just let you pay it all in one go next year. Instead, they ask you to make advance payments towards your next tax bill.

These payments are split into two instalments:

- First Payment: Due by 31st January.

- Second Payment: Due by 31st July.

Each payment is typically 50% of your previous year's tax bill. While this is meant to help you spread the cost, it can feel like a double whammy in your first profitable year. The single best financial habit you can form is to squirrel away a percentage of every invoice for tax. At Stewart Accounting Services, we help our clients create a clear financial roadmap so there are no nasty surprises when tax deadlines are just around the corner.

Keeping Your Business Finances Organised

Landing your first clients is a fantastic feeling, but the real key to long-term success as a sole trader lies in getting your financial habits right from day one. Good bookkeeping isn't just about being neat and tidy; it’s a legal requirement that forms the very foundation of your business and keeps you on the right side of HMRC.

One of the simplest yet most effective things you can do is open a separate business bank account. While it’s not technically a legal must-have for sole traders, believe me when I say that mixing your business income with your weekly grocery shop is a recipe for an accounting headache. A dedicated account creates a clean, clear line between your personal and business finances, making life infinitely easier when it’s time to fill out your tax return.

What Records Do You Need to Keep?

HMRC has very specific rules about the records you must keep. In short, you need to be able to back up every figure on your tax return with solid proof.

Generally, you’re required to hold onto your records for at least five years after the 31st January submission deadline for the relevant tax year.

Here’s a quick overview of what you'll need to keep on file:

- All sales and income: This means keeping a copy of every single invoice you issue.

- All business expenses: Hold on to every receipt and invoice for things you buy for the business—from software subscriptions and stationery to train tickets for client meetings.

- VAT records: If you’re VAT registered, you'll have extra responsibilities for keeping digital records under Making Tax Digital rules.

- PAYE records: If you decide to take on an employee, all your payroll information must be meticulously kept.

For many service-based businesses, managing bookings is directly tied to income. Looking into a comprehensive booking system guide can help you set up a streamlined process. This not only makes scheduling clients easier but also ensures you have a precise record of the work you've delivered, which is vital for accurate invoicing.

Before we dive into software, let's summarise the essential documents HMRC expects you to have.

Essential Records for Sole Traders

This table provides a simple checklist of the key financial documents you are legally required to maintain. Think of it as your non-negotiable filing list.

| Record Type | What to Keep | Why It's Important |

|---|---|---|

| Sales Invoices | Copies of all invoices you send to clients. | Proof of all your business income and turnover. |

| Purchase Receipts | All receipts for goods and services you buy for the business. | Evidence for every allowable expense you claim. |

| Bank Statements | Statements for your dedicated business bank account. | Provides a clear audit trail of money in and out. |

| Cash Book | If you handle cash, a record of all cash transactions. | To track income and expenses not processed by the bank. |

| VAT Records | VAT invoices, adjustments, and your VAT account (if registered). | Mandatory for calculating and submitting your VAT return. |

| PAYE Records | Employee pay, deductions, and reports (if you have staff). | Legal requirement if you operate payroll. |

Keeping these records organised isn’t just about compliance; it gives you a true picture of your business’s financial health.

Ditching the Spreadsheet for Cloud Accounting

It’s always tempting to start out with a simple spreadsheet to track your finances. It seems easy enough at first, but this approach can quickly become a tangled mess of formulas and errors as your business picks up steam.

This is where modern cloud accounting software really shines. Platforms like Xero, QuickBooks, or FreeAgent are built from the ground up for small businesses and are a game-changer when you set up as a sole trader. They can connect directly to your business bank account, pulling in transactions automatically and making it incredibly simple to see where your money is going.

This screenshot from the Xero UK homepage gives you a feel for how these platforms work.

The dashboard gives you a live snapshot of your cash flow, who owes you money, and your overall financial position at a glance. It turns bookkeeping from a chore into a powerful business tool.

This shift to digital isn’t just a nice-to-have. With HMRC's Making Tax Digital (MTD) initiative continuing to expand, using compliant software is fast becoming non-negotiable for more and more businesses. Getting started with a digital system now is a smart way to future-proof your admin.

By embracing cloud accounting from the outset, you're not just organising your finances; you're creating a scalable system that saves hours of manual work, reduces the risk of human error, and provides invaluable insights into your business's performance.

A Practical Checklist for Financial Organisation

Building good financial habits is all about creating simple, repeatable routines. Here’s a quick checklist to get you on the right track:

- Open That Bank Account: Seriously, do this first. As soon as you decide to start trading.

- Pick Your Accounting Software: Research a platform like Xero and get it connected to your new bank account right away.

- Book a Weekly Money Date: Set aside 30 minutes every week to log in, categorise transactions, and chase any overdue invoices. Consistency is key.

- Snap Your Receipts: Use the mobile app that comes with your software. Take a photo of a receipt the moment it's in your hand. No more faded bits of paper!

- Create a Tax Pot: This is a big one. Get into the habit of moving 25-30% of every payment you receive into a separate savings account. When the tax bill arrives, the money will be sitting there waiting. No nasty surprises.

Staying on top of your finances doesn't have to be a source of stress. At Stewart Accounting Services, we can help you implement robust bookkeeping systems from the very beginning, giving you the peace of mind to focus on what you do best.

Protecting Your Business with the Right Insurance

When you decide to set up as a sole trader, you’re taking a fantastic leap into independence. But that freedom comes with its own set of risks. Getting the right insurance isn't just a box-ticking exercise; it's the bedrock of a professional, resilient business.

Without it, one simple accident, a costly mistake, or an unexpected claim could threaten not just your livelihood, but your personal assets too. Think of insurance as the safety net that lets you focus on what you do best, with complete peace of mind.

Public Liability Insurance Explained

If you come into contact with the public in any way, Public Liability Insurance is non-negotiable. This applies whether clients visit your office, you work at their property, or you meet them for a coffee. It’s there to protect you if a member of the public gets injured or their property is damaged because of something you did.

Imagine you’re a self-employed plumber working in a client's kitchen and you accidentally cause a leak that ruins their new laminate flooring. Without public liability cover, you'd be footing the bill for repairs yourself, which could easily run into thousands.

Or, say you're a personal trainer in a park and a client trips over your equipment. This insurance would handle the legal costs and any compensation if they decided to sue. It’s a vital shield for the day-to-day risks of working with people.

When You Need Professional Indemnity Insurance

While public liability covers physical incidents, Professional Indemnity Insurance is all about protecting you from claims of professional negligence. If your business gives advice, offers a specialised service, or handles client data, this cover is an absolute must-have.

It’s essentially insurance for your expertise. It kicks in if a client claims your advice was flawed, your service wasn't up to scratch, or you made an error that cost them money.

For instance, a marketing consultant whose strategy doesn't deliver the promised results might face a claim. A web developer who writes code with a bug that crashes a client’s e-commerce site could be held liable for all the lost sales.

This insurance is your financial defence when your professional service is questioned. It covers legal fees and compensation, safeguarding both your reputation and your bank balance from an honest mistake.

The Legal Requirement for Employers' Liability Insurance

The moment you hire someone—even a casual or part-time helper—the law says you must have Employers’ Liability Insurance. This isn't a recommendation; it's a legal obligation. The Health and Safety Executive (HSE) can issue hefty fines if you're caught without it.

This policy protects you if an employee gets ill or is injured because of the work they do for you. It covers compensation payouts and legal fees, looking after both you and your team. The legal minimum cover is £5 million, but you'll find most policies provide £10 million as standard. It's a non-negotiable step as soon as you're no longer a one-person band.

The UK's self-employment scene is huge. Recent data shows there are over 4.1 million businesses with no employees, and of those, 93% of sole traders operate completely alone. This highlights just how independent this path is, which makes sorting out your personal and business protections even more critical. You can explore more UK business statistics at Money.co.uk to see the full picture.

Answering Your Top Questions About Being a Sole Trader

Starting out as a sole trader is exciting, but it's completely normal to have a long list of questions. To give you some clarity and confidence, we've tackled some of the most common queries we hear from people just starting their self-employed journey.

Do I Really Need a Separate Business Bank Account?

This is a classic. Legally, no, you don't have to open a dedicated business bank account. You could run everything through your personal current account. But honestly, that’s a recipe for disaster.

Trying to unpick business transactions from your weekly shop or a night out with friends is a bookkeeping nightmare. It makes tracking your expenses and figuring out your actual profit incredibly difficult.

Our advice is simple: Open a separate business bank account from day one. It draws a clean line between your personal and business finances, makes bookkeeping a hundred times easier, and just looks more professional when clients are paying you.

How Do I Pay Myself?

People often overcomplicate this, but it’s beautifully simple. As a sole trader, you and your business are one and the same in the eyes of the law. The profit you make is your income.

There’s no need for a formal payroll system like you’d have with a limited company. You just transfer money from your business account to your personal one whenever you need it. These transfers are called ‘drawings’.

Crucially, you don't pay tax on the drawings themselves. You pay Income Tax and National Insurance on the total profit your business earns over the tax year—regardless of how much you’ve actually taken out. The golden rule is to always keep enough cash aside to cover that future tax bill.

Can I Be a Sole Trader and Have a Full-Time Job?

Yes, absolutely. It's very common for people to start a business as a 'side hustle' while still in full-time employment. There's nothing stopping you from being both employed and self-employed.

The main thing to get your head around is the tax. Your salary from your day job will already be using up some (or all) of your tax-free Personal Allowance. This means you’ll likely pay tax on pretty much every pound of profit you make from your sole trader work.

You'll need to register for Self Assessment and complete a tax return each year. On it, you’ll declare your self-employed income on top of the earnings you’ve already been taxed on through PAYE from your main job.

When Should I Think About Becoming a Limited Company?

The sole trader structure is fantastic for getting started, but there often comes a time when it makes sense to incorporate as a limited company. There's no magic number, but here are the key triggers we tell our clients to watch for.

It's time to consider the switch when:

- Your profits are growing fast: Once your annual profits start climbing towards the £30,000-£40,000 mark, the tax efficiencies of a limited company become very appealing. You can pay yourself a small, tax-efficient salary and take the rest as dividends, which can often lead to a lower overall tax bill.

- You want to protect your personal assets: This is a big one. If you're taking on debt, signing large contracts, or operating in a risky field, a limited company separates your business finances from your personal ones. If the business were to fail, your personal assets (like your home) are protected.

- You need more credibility: For better or worse, some bigger clients, lenders, and suppliers see a limited company as a more stable and professional outfit. Incorporating can sometimes be the key to winning that next big contract or securing a business loan.

Making the leap from sole trader to a limited company is a significant move. It brings more admin and costs, so it’s a decision that needs careful thought based on your specific circumstances.

Getting these fundamental questions answered early on can save you a world of headaches later. It’s all about building your business on a solid, well-informed foundation.

If you're still weighing your options or need a hand with any part of the sole trader process, Stewart Accounting Services is here to help. We offer practical, expert advice to get you started on the right foot. Visit us at https://stewartaccounting.co.uk to see how we can support your new venture.