Running a property portfolio is a business. And like any business, your real profit isn't what you take in – it's what you get to keep after all the costs are paid. Mastering your landlord tax deductions is the single most effective way to protect that profit.

Essentially, any cost you incur "wholly and exclusively" for the purpose of renting out your property can be deducted from your rental income, which lowers the amount of tax you owe HMRC.

Understanding Your Rental Profit Potential

Getting your head around your tax bill is one of the most important parts of being a successful landlord. This guide is designed to be your roadmap, breaking down how HMRC taxes your rental income and, crucially, how you can legally minimise that bill.

The concept you really need to get to grips with is 'allowable expenses'. Don't think of these as a box-ticking exercise. See them for what they are: the most powerful tool you have for shrinking your taxable profit. Every legitimate expense you claim is money that stays in your pocket, improving your cash flow and boosting your overall return. It's not just about compliance; it's a core business strategy.

The Scale of Landlord Deductions

The financial impact of claiming everything you're entitled to is huge. In the 2023–24 tax year alone, UK landlords declared a staggering £55.53 billion in property income. Digging into the official government property rental income statistics reveals something fascinating: on average, expenses can make up around 50% of a landlord's gross rental income. This shows just how vital strategic deductions are for your financial health.

This guide gives you a clear framework for the main types of deductions. It's about moving from simply paying your tax bill to proactively managing your rental finances for the best possible returns.

Key Takeaway: The moment you start treating your property portfolio like a proper business, your mindset shifts. Diligently tracking and claiming every single allowable expense is how you make that business more profitable, turning tax compliance into a genuine strategic advantage.

Getting the fundamentals right on how property rental income tax works is the foundation. From there, this guide will build on those basics to give you a complete picture of your obligations and your opportunities. By the time you've finished, you'll have a clear plan for what you can claim and how to do it properly.

Claiming Your Day-to-Day Running Costs

Think of your rental property as a business. And just like any business, it has running costs – those everyday expenses needed to keep things ticking over, legal, and profitable. These are often the most straightforward tax deductions for landlords, and getting a firm grip on them is the first step to protecting your bottom line.

The golden rule from HMRC is that any expense you claim must be ‘wholly and exclusively’ for your rental business. It’s a simple concept: if an expense also has a personal benefit, you can’t claim for it (or at least, not all of it). Let's break down the main categories you should be tracking.

Professional and Legal Fees

Unless you’re a jack-of-all-trades, you’ll almost certainly pay for professional help. These fees are a core part of running a property business and, thankfully, are valuable tax deductions.

This is a broad category covering the essential services that keep you compliant and your property occupied.

- Letting Agent Fees: Whether you use an agent just to find a tenant or for full-on property management, their fees are deductible. This includes everything from referencing checks to their monthly commission.

- Accountancy Fees: The cost of having a professional prepare your rental accounts and file your Self Assessment tax return is an allowable expense.

- Legal Fees: Paying a solicitor to draft a tenancy agreement or advise on a tenant issue? That’s a running cost. But be careful – legal fees for buying the property in the first place are a capital expense, which is a different beast entirely.

Insurance and Essential Services

Protecting your asset and your tenants isn't just good practice; it's a legal requirement. The costs involved are directly deductible from your rental income.

Make sure you’re claiming for these essentials:

- Landlord Insurance: This isn’t the same as standard home insurance. Your specific landlord policy, covering buildings, contents, and public liability, is an allowable expense.

- Safety Certificates: Keeping tenants safe is paramount, and the certificates to prove it are a deductible cost. Mandatory inspections like Landlord EICR Certificates for electrics, annual Gas Safety checks (CP12), and Energy Performance Certificates (EPCs) all fall into this bucket.

Keep every policy document and renewal notice. These are usually annual costs, making them easy to track and claim year after year.

Managing Bills During Void Periods

No one likes an empty property, but void periods between tenancies are part of the game. The silver lining is that you can claim the running costs you have to cover while the property is empty and available for let.

Crucial Point: You can only claim these expenses if you're actively trying to find a new tenant. If you decide to take the property off the market to use it yourself, the costs are no longer deductible.

When the property is empty, you're back on the hook for the bills. Don't forget to claim for:

- Council Tax: You become liable for the full council tax bill the moment your tenant moves out.

- Utility Bills: Gas, electricity, and water bills needed to keep the property maintained are all claimable.

- Ground Rent and Service Charges: If your property is a leasehold, these charges don’t stop just because a tenant isn’t there. They remain a deductible business expense.

The logic is simple: these expenses are purely to keep the property in a rentable state. That means they sail through HMRC’s ‘wholly and exclusively’ test.

Office and Administrative Costs

Don’t sweat the small stuff—but do claim for it! The little administrative costs of being a landlord might seem trivial one by one, but they really add up over a tax year.

You can claim for things like:

- Stationery and Postage: Buying paper and printer ink for tenancy agreements or stamps to post documents? That’s a business cost.

- Phone Calls: You can claim for the business-related portion of your phone bill. Just be sure you have a sensible way of working out the split between personal and business use.

- Advertising Costs: Any money you spend marketing your property to attract new tenants, whether on Rightmove or in the local paper, is fully deductible.

The absolute key here is to keep your records straight. Every receipt, invoice, and bank statement is your proof. A simple spreadsheet or a bit of software can make tracking these running costs a breeze, ensuring you have the evidence to back up every single claim.

Navigating Repairs Versus Improvements

This is where so many landlords trip up. Getting the difference between a 'repair' and an 'improvement' wrong can be a costly mistake, but it's one of the most fundamental parts of getting your rental property taxes right.

Think of it this way: a repair is all about putting things back to how they were. It’s maintenance. A tile blows off the roof in a storm, and you get a roofer to replace it. That’s a straightforward repair, and you can deduct the cost from your rental income for the year.

An improvement, however, is an upgrade. You’re not just fixing something; you’re making it fundamentally better than it was before. If you decide to add a whole new conservatory or knock down a wall to create a swanky open-plan living space, you’ve crossed into improvement territory. HMRC sees this as a capital expense, which means you cannot claim it against your rental income.

Drawing the Line: Where Does a Repair End and an Improvement Begin?

The crucial question to ask yourself is: am I restoring something, or am I upgrading it?

It often comes down to the materials and scope of the work. For example, if a tenant has wrecked a cheap laminate kitchen worktop, replacing it with a new, standard laminate version is a clear repair. But if you decide to splash out and replace it with a polished granite worktop, that's an improvement. You've significantly upgraded the quality and value of the asset.

The scale of the project is also a big factor. Let's say one of your old wooden windows has started to rot. Replacing that single window with a modern, double-glazed uPVC equivalent is almost always classed as a repair, as you're just using the modern-day standard materials. But if you decide to replace all the windows in the entire property in one go, HMRC is likely to see that as a single capital project to improve the building, not just a series of small fixes.

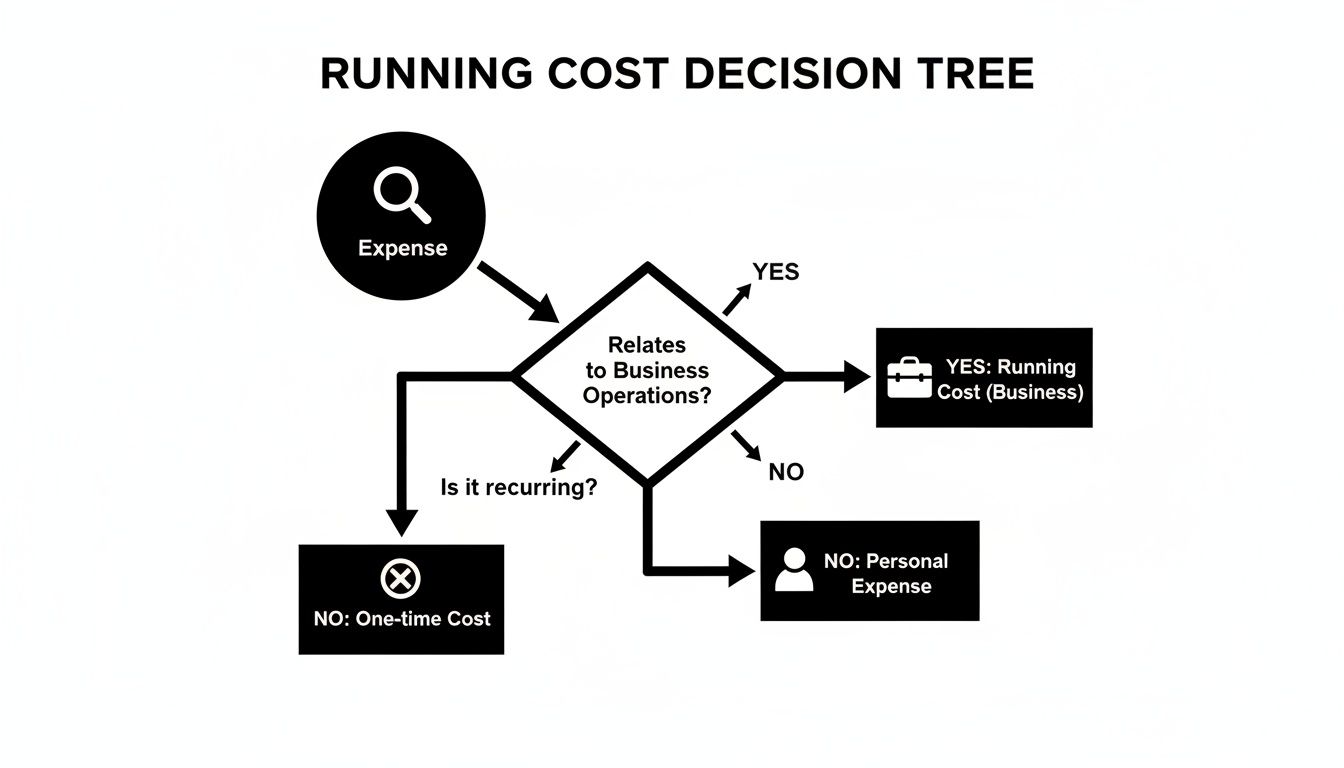

This flowchart can help with your initial thinking, guiding you on whether an expense is even a business cost in the first place.

Once you've established a cost is for the business, the next step is to correctly classify it as a repair or an improvement.

Repair or Improvement: A Landlord's Decision Guide

Sometimes the lines can feel a bit blurry. This table breaks down a few common scenarios to help make the distinction crystal clear.

| Scenario | Classification | Tax Treatment |

|---|---|---|

| A broken boiler is replaced with a new, energy-efficient model. | Repair | The cost is a revenue expense, fully deductible from rental income in the current tax year. Modern efficiency is now the standard, not an upgrade. |

| A damaged fence panel is replaced with a new, identical panel. | Repair | A simple 'like-for-like' replacement. This is a revenue expense, fully deductible from your rental income. |

| The entire worn-out fence is replaced with a higher, more secure brick wall. | Improvement | This goes far beyond restoration. It's a capital expense and is not deductible against rental income. |

| A threadbare carpet is replaced with good quality laminate flooring. | Improvement | This is a material upgrade. The cost is a capital expense and is not deductible against rental income. |

| A leaking tap in the bathroom is fixed by a plumber. | Repair | A classic example of maintenance. This is a revenue expense and is fully deductible from your rental income. |

| The entire bathroom suite is ripped out and replaced with a modern wet room. | Improvement | A major upgrade that enhances the property's value. This is a capital expense and is not deductible against rental income. |

As you can see, the context and scale of the work are everything. It’s all about restoring function versus adding value.

What Happens to the Cost of Improvements?

Just because you can't deduct an improvement from your rental income doesn't mean the money is lost for tax purposes. These capital costs are added to the 'base cost' of your property.

Why does that matter? When you eventually come to sell the property, this higher base cost will reduce your overall profit, which in turn lowers your final Capital Gains Tax bill. So, while you don't get the immediate tax relief, you do benefit later on. This makes it absolutely vital to keep meticulous records and classify every single expense correctly.

Understanding Mortgage Interest Tax Relief

Of all the expenses landlords face, how you treat your mortgage interest has seen the biggest, and frankly most painful, shake-up in recent years. Getting your head around this change isn't just a box-ticking exercise; it’s absolutely fundamental to your bottom line, especially if you're a higher-rate taxpayer.

Not so long ago, things were simple. You treated your entire mortgage interest payment as a standard business expense, just like your insurance or letting agent fees. You simply knocked the full amount off your rental income before working out what tax you owed. Straightforward.

But then came the rule change that sent shockwaves through the landlord community, a piece of legislation commonly known as 'Section 24'. This completely upended the old system for individual landlords. The ability to deduct mortgage interest directly from your profits was phased out, replaced by a far less generous tax credit. The impact on landlords' net income has been huge.

The New System: A Tax Credit, Not a Deduction

So, what's changed? Instead of subtracting your mortgage interest from your income, you now get a tax credit. This credit is fixed at 20% of whatever you paid in mortgage interest for that year.

This might sound like a minor tweak in wording, but the financial consequences are anything but. Under the new rules, your taxable rental income is calculated before you account for your mortgage interest. This makes your income look much higher on paper, which has had the nasty side effect of pushing many landlords into a higher tax bracket.

It's only after your initial tax bill is worked out that you can then apply the 20% credit to bring down the final figure you owe to HMRC.

The Critical Difference: A tax deduction reduces your taxable income, potentially saving you 20%, 40%, or even 45% in tax, depending on your personal tax band. A tax credit, however, only ever reduces your final tax bill by the basic rate of 20%, no matter how much you earn.

A Worked Example: Old vs. New

The best way to see the real-world hit is to crunch the numbers. Let’s take a landlord, Sarah, who is a higher-rate (40%) taxpayer.

- Annual Rental Income: £15,000

- Annual Mortgage Interest: £5,000

- Other Allowable Expenses: £2,000

Here’s how her tax bill shapes up under both systems:

1. The Old System (Pre-Section 24)

- Taxable Profit: £15,000 (Income) – £5,000 (Interest) – £2,000 (Expenses) = £8,000

- Tax Due at 40%: £8,000 x 40% = £3,200

2. The New System (Current Rules)

- Taxable Profit: £15,000 (Income) – £2,000 (Expenses) = £13,000

- Initial Tax Bill at 40%: £13,000 x 40% = £5,200

- Tax Credit: £5,000 (Interest) x 20% = £1,000

- Final Tax Due: £5,200 – £1,000 = £4,200

As you can see, Sarah's tax bill is £1,000 higher under the current rules. That's a £1,000 dent straight out of her net profit. For a deeper dive into these sums, you can read our detailed guide on the mortgage interest deduction for rental property.

The Limited Company Exemption

There is one major get-out clause to all of this: limited companies. The Section 24 mortgage interest restrictions do not apply to properties owned inside a corporate structure.

For landlords operating through a limited company, it's business as usual. They can still deduct their full finance costs from their rental income before calculating their Corporation Tax bill.

This single difference is the main driver behind the huge trend of individual landlords either moving their portfolios into a limited company or choosing to buy all new properties this way. Of course, running a company comes with its own admin and costs, but for many, the tax savings on mortgage interest are just too significant to ignore. It’s a strategic move that’s well worth exploring with an accountant.

Finding Overlooked Tax Deductions

Most landlords are pretty good at remembering to claim for the big things, like letting agent fees or a major repair. But it's often the smaller, less obvious expenses that get missed, and believe me, they can add up to a significant sum by the end of the tax year.

Think of this as a final sweep to make sure you're not leaving any money on the table with HMRC. It's about finding every legitimate claim that can turn a good year into a great one, simply by being thorough.

Mastering Replacement of Domestic Items Relief

One of the most valuable, and often misunderstood, claims is the Replacement of Domestic Items Relief. This is your go-to when you have to replace a freestanding item in a furnished or part-furnished property.

This relief took the place of the old ‘Wear and Tear Allowance’ a few years back. It allows you to deduct the cost of replacing things like sofas, beds, fridges, washing machines, or even carpets. The golden rule here is that the replacement must be ‘like-for-like’.

The mechanics are quite simple: you can claim the cost of the new item, minus any cash you get from selling the old one. If you decide to upgrade to a fancier model, your claim is capped at what a modern equivalent of the original would have cost.

Let’s put that into a real-world scenario. Say the washing machine in your rental property, which has served well for years, finally breaks down for good.

- You buy a new, similar-quality machine for £400.

- You pay an extra £30 for delivery and installation.

- There's also a £20 charge to have the old, broken machine taken away and disposed of correctly.

In this situation, your total allowable deduction is £450. You can claim the full amount, as it includes the cost of the item itself plus the direct costs of getting it installed and removing the old one.

Important Note: You can't claim for the initial cost of furnishing a property from scratch. This relief is purely for replacing an item that was already there.

Uncovering Other Commonly Missed Deductions

Beyond replacing furniture, there are plenty of smaller, day-to-day costs that are perfectly legitimate deductions. They might seem trivial on their own, but they can make a real dent in your final tax bill when you add them all up.

Here are a few of the most frequently overlooked expenses to keep an eye on:

- Vehicle Mileage: Did you drive to the property for an inspection, to let a plumber in, or to do a viewing? You can claim for that. HMRC’s approved mileage rate is 45p per mile for the first 10,000 business miles you do in a tax year.

- Advertising for Tenants: Those fees for listing your property on portals like Rightmove or Zoopla, or even running an ad in the local paper, are all deductible running costs.

- Legal Fees: While the solicitor's bill for buying the property is a capital expense, the fees for things like drafting or renewing a tenancy agreement are an allowable revenue expense.

- Bank Charges: If you run a dedicated bank account for your property business, any monthly fees or transaction charges on that account can be claimed.

A Glimpse into Capital Allowances

For some landlords, there's another, more complex area of tax relief called Capital Allowances. This won't apply to everyone, but it's vital to know about if it fits your situation.

Unlike the everyday running costs we've talked about, Capital Allowances let you write off the value of certain assets—what HMRC calls ‘plant and machinery’—over a period of time. This is a bit of a specialist area and doesn't usually apply to standard residential lets.

However, it becomes very relevant for landlords who own:

- Furnished Holiday Lettings (FHLs): These properties play by a different set of tax rules, and you can claim allowances on furniture, fixtures, and equipment.

- Commercial Properties: If you own a shop, office, or industrial unit, you can claim for items integral to the building, like air-conditioning systems or electrical wiring.

- Common Areas of Residential Buildings: In a block of flats you own, you can claim for items in the shared spaces, such as carpets in the hallway or fire alarm systems.

Capital Allowances can be a tricky field to navigate. If your portfolio includes any of these property types, it’s well worth getting professional advice from an accountant to make sure you’re claiming everything you’re entitled to, and correctly.

Building Your System for Record Keeping and Filing

Knowing which tax deductions you can claim is one thing, but having the paperwork to prove it is where the real work begins. Great record-keeping isn't just about keeping HMRC happy; it's about having a firm grip on the financial health of your property business. An old shoebox stuffed with faded receipts is a one-way ticket to stress and, worse, missed tax savings.

The good news? You don't need a fiendishly complicated system. A simple spreadsheet can work wonders, with separate tabs for your rental income and different expense categories. If you prefer a more hands-off approach, modern accounting software can sync with your business bank account, automatically sorting transactions as they come in.

Your Essential Document Checklist

To make sure every claim is solid, you need a clear paper trail. HMRC can ask to see evidence from several years back, so getting organised from the very start is non-negotiable.

Here’s what your core record-keeping file should contain:

- Proof of Income: Keep copies of all tenancy agreements, bank statements showing rent deposits, and any statements from your letting agent.

- Proof of Expenses: Hold onto every single receipt and invoice for goods and services. Make sure they are dated and clearly show what was purchased, whether it’s a major plumbing job or a bottle of cleaning spray.

- Bank Statements: This includes statements for your buy-to-let mortgage and the bank account you use for all your rental ins and outs.

- Mileage Log: A simple notebook or a smartphone app is perfect for logging the date, reason, and distance of any car trips related to your property.

HMRC requires you to keep your records for at least five years after the 31st January submission deadline for that tax year. So, for the 2023-24 tax year, you'll need to hang onto everything until at least 31st January 2030.

Filing Your Self Assessment Tax Return

Once you've tallied up your numbers for the year, it's time to report them to HMRC on your Self Assessment tax return.

All your rental profits or losses are declared on a specific set of supplementary pages called the SA105 'UK Property' form. This is submitted along with your main SA100 tax return.

The SA105 form has dedicated boxes for different types of income and allowable expenses, like property repairs and professional fees. This is where your meticulous record-keeping truly pays off. You can simply transfer the organised totals straight into the right boxes, which dramatically cuts down the risk of making a costly mistake.

For landlords with a growing portfolio, the admin can quickly start to feel overwhelming. To streamline tracking of assets and expenses specific to your rental properties, you might also want to explore dedicated rental property inventory software for landlords.

However, as your finances get more complex, understanding the advantages of professional accountancy support for landlords can be a game-changer. An expert can handle the entire filing process for you, guaranteeing accuracy and giving you back the time to focus on what you do best—managing your properties.

Common Landlord Tax Questions Answered

When you're dealing with landlord taxes, a few common questions always seem to pop up. Let's tackle some of the most frequent queries head-on to clear up any confusion and help you get your tax return right.

Think of this as your go-to guide for those tricky little "what if" scenarios. Getting the details straight means you can file with confidence, knowing you’ve claimed everything you’re entitled to.

Can I Claim for My Own Labour?

This is a classic. You've spent a whole weekend painting a bedroom or fixing a leaky tap – can you charge for your time?

Unfortunately, HMRC's answer is a straightforward no. You can't put a price on your own time and claim it as a tax-deductible expense. Deductions are only for money you've actually spent.

What you can and absolutely should claim for are:

- The cost of all the materials you bought for the job – every tin of paint, screw, and roll of wallpaper.

- The full cost of hiring any professional tradespeople to help you get the work done.

How Do I Handle Mixed-Use Expenses?

What about something that's part-business, part-personal? Your mobile phone is a perfect example; you use it to call tenants and arrange viewings, but also to chat with friends.

In this situation, you can only claim the business-related portion of the bill. You'll need a fair and logical way to work this out. For your phone, that might mean going through your bill and calculating the percentage of calls that were for your rental business. The key is that you must be able to explain your calculation to HMRC if they ever ask.

The Golden Rule: It all comes down to the 'wholly and exclusively' principle. For any dual-purpose expense, you must make a reasonable split and only claim for the part that is 100% for your property business.

Can I Claim Expenses on an Empty Property?

Yes, absolutely. This is a big one that many landlords miss. You can still claim for expenses during those empty 'void' periods between tenancies.

As long as the property is still on the market and you’re actively trying to find a new tenant, you can continue to deduct the running costs. This includes things like:

- Council tax

- Utility bills

- Landlord insurance

- Ground rent and service charges

How Long Must I Keep My Records?

Good record-keeping isn't just a smart habit; it's a legal requirement.

HMRC requires you to hold on to your records for at least five years after the 31st January submission deadline for that tax year. So, for the 2023-24 tax year, which has a deadline of 31st January 2025, you need to keep your paperwork safe until at least 31st January 2030. This ensures you have all the proof you need if HMRC opens an enquiry into your tax affairs.

Getting your head around landlord tax can feel overwhelming, but you don't have to figure it all out on your own. The experts at Stewart Accounting Services specialise in helping property landlords across the UK handle their tax obligations, making sure no allowable expense is missed. Get in touch to see how we can help you save time, money, and stress. Find out more at https://stewartaccounting.co.uk.