If you’re self-employed in the UK, there’s one date you absolutely have to burn into your memory: 31 January. This is the final day for getting your online Self Assessment tax return filed and for paying the tax you owe. Dropping the ball on this one leads to instant penalties, so getting it in your calendar is the first, simplest step to a stress-free tax season.

Your Guide To Self-Employed Tax Deadlines

Running your own business is incredibly freeing, but it comes with the not-so-freeing task of sorting out your own taxes. When people hear ‘tax return deadline’, they usually just think of that big January date. In reality, it’s better to see it as a timeline with a few important checkpoints throughout the year. Getting to grips with this schedule is fundamental for staying on HMRC's good side and managing your finances properly.

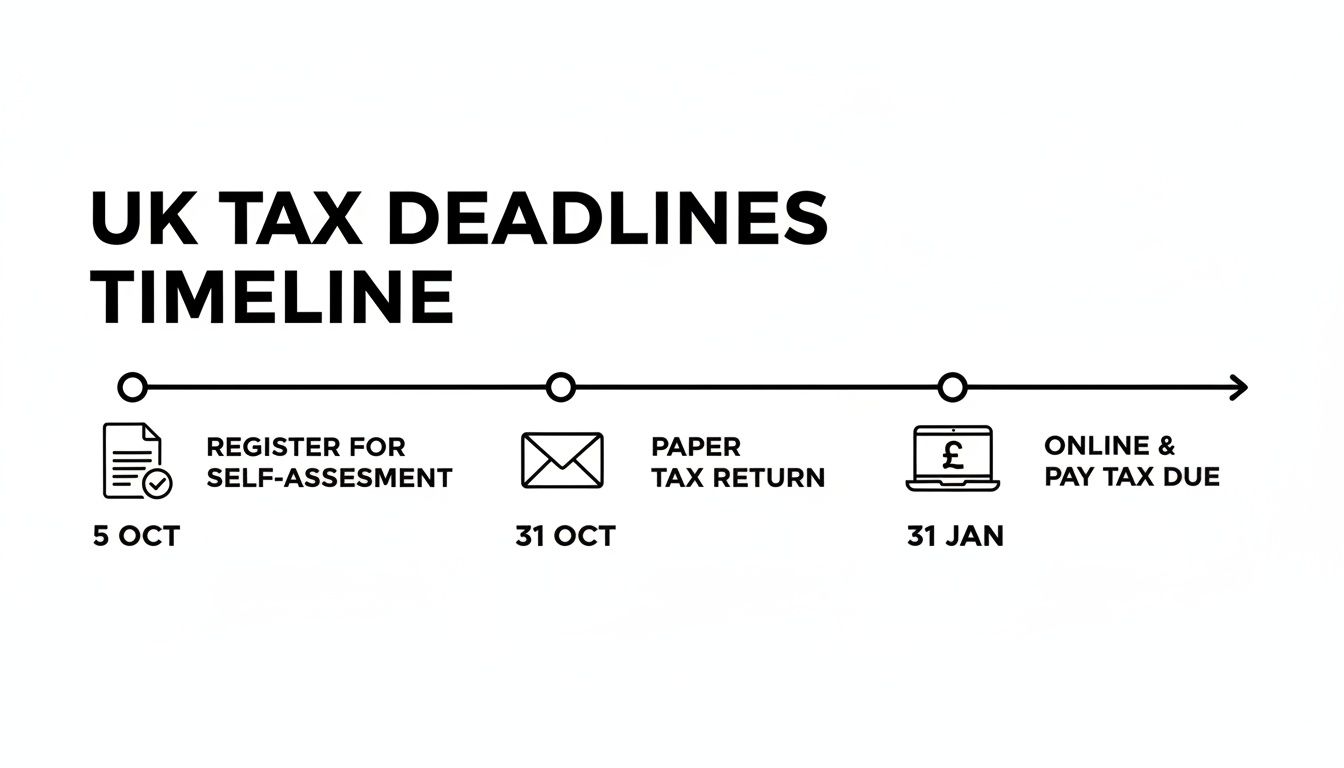

Let's break down the journey. The very first hurdle is registering for Self Assessment. You need to get this done by 5 October following the end of the tax year you first started trading in. Missing this initial step can create a real headache down the line.

To make things easier, here’s a quick overview of the essential dates every self-employed person needs to know.

Key UK Self Assessment Deadlines At A Glance

| Task | Deadline | Method |

|---|---|---|

| Register for Self Assessment | 5 October | Online |

| File a paper tax return | 31 October | Post |

| File an online tax return | 31 January | Online |

| Pay the tax you owe | 31 January | Online/Bank Transfer |

| Make your first 'Payment on Account' | 31 January | Online/Bank Transfer |

| Make your second 'Payment on Account' | 31 July | Online/Bank Transfer |

This table lays out the entire cycle, helping you plan your financial year and avoid any last-minute panic.

The Main Deadlines You Cannot Miss

Once you're registered, you have two main filing dates to choose from, and it all depends on how you want to submit your return. While sending in a paper form is still an option, its deadline is much, much earlier.

- Paper Tax Returns: If you’re going old-school with a paper form, you need to have it sent off by midnight on 31 October.

- Online Tax Returns: The vast majority of people file online, which gives you until midnight on 31 January.

- Payment Deadline: This is the big one. 31 January is also the absolute final day to pay the tax bill for the previous tax year.

This timeline clearly shows the path you'll follow from registering your business to finally filing and paying.

As you can see, filing online buys you an extra three months, which is why it’s the go-to choice for most business owners. It just gives you that much more breathing room.

Understanding Your Full Financial Picture

Just hitting the deadlines is only half the battle. Smart tax planning means you’re also doing everything you can to lower your final bill by claiming all your allowable expenses. For instance, knowing you can make self-employed health insurance deductions can make a real difference to what you owe.

A common point of confusion for the newly self-employed is the concept of 'Payments on Account'. These are advance tax payments made twice a year to spread the cost of the next year's tax bill.

Your first Payment on Account is also due on 31 January, making it a particularly heavy-hitting deadline. The second payment is then due by 31 July. We’ll dive deeper into how these work later on, but for now, just knowing they exist is crucial for managing your cash flow and avoiding any nasty shocks.

Why the 31 January Deadline Is a Big Deal

If you're self-employed in the UK, 31 January is more than just another date on the calendar. It's the main event, a perfect storm of financial obligations that can define your entire year. This isn't just about sending off a form; it's a critical moment where several major responsibilities all land at once.

Think of it as a busy junction where three separate financial roads all meet. On this one day, you’ve got to tackle three significant and distinct tasks. Forgetting even one can trigger instant penalties and a whole lot of stress, so getting your head around what’s due is absolutely crucial.

This convergence is exactly why the tax return self employed deadline feels so high-stakes. It’s the final cut-off for filing your online tax return, the last moment to pay off last year's tax, and the due date for your first big payment towards this year's bill.

A Triple Threat Deadline

So, what exactly makes 31 January such a pivotal day for your business finances? It’s the meeting point of your past, present, and future tax duties.

- Final Filing Day: This is your last chance to get your online Self Assessment tax return submitted for the tax year that ended on the previous 5 April.

- Balancing Payment: Any tax you still owe from that previous tax year has to be paid in full by midnight.

- First Payment on Account: You also need to make your first advance payment towards your next tax bill.

This triple-duty deadline demands some serious financial planning. You need a crystal-clear picture of your previous year’s earnings, but you also need the cash on hand to pre-pay for the tax year you're currently working in. It's a tricky balancing act that catches a lot of people out.

For many self-employed people, it’s the sheer scale of the 31 January deadline that causes the most anxiety. This isn’t just your personal deadline; it’s a national event with millions of others trying to do the exact same thing at the exact same time.

This massive, simultaneous rush puts incredible pressure on HMRC's systems. Just knowing that millions of other people are also logging in, phoning helplines, and trying to make payments shows why leaving it all to the last minute is such a gamble. A simple technical glitch or a forgotten password can quickly escalate from a minor annoyance into a frantic race against the clock.

The Scale of the January Rush

The sheer volume of returns filed in the run-up to this deadline is staggering and really paints a picture of a nationwide financial event. Every year, millions of UK taxpayers are all working towards the same 31 January online filing deadline.

Recent figures from HMRC show just how big a deal this is. For the 2023–24 tax year, over 12 million Self Assessment returns were expected. By the cut-off, more than 11.5 million were successfully received, which thankfully shows most people get it done on time. The data also reveals a huge preference for digital, with 97.36% of returns submitted online. This move to digital highlights just how vital a reliable internet connection is during that January peak. You can dig into these filing statistics on the GOV.UK website.

This huge spike in activity in the final days—and even hours—is a predictable pattern. While technology makes filing easier, human nature often means we procrastinate. Understanding this dynamic is your key to a much smoother experience. By preparing and filing early, you completely sidestep the digital traffic jam, slash your stress levels, and give yourself a crucial buffer to handle any unexpected issues that might pop up.

Making Sense Of Payments On Account

If there’s one part of the self-assessment system that catches newly self-employed people out, it’s ‘Payments on Account’. This is often the culprit behind a nasty surprise when the first big tax bill lands, causing a lot of stress and serious cash flow problems. So, what exactly is it?

Think of it as pre-paying your tax bill in two instalments. Instead of being hit with one huge demand after filing your return, HMRC asks you to pay half of your expected bill in January and the other half in July. The idea is to spread the load, both for you and for the taxman.

Of course, this system doesn't apply to everyone. You’ll generally only need to make Payments on Account if your Self Assessment tax bill is more than £1,000, and less than 80% of your total income has been taxed at source (through something like a part-time PAYE job, for instance).

How Payments On Account Are Calculated

This is where people often get tangled up, but it’s much simpler when you see it in action. HMRC looks at last year’s tax bill to estimate what you’ll owe this year. Each payment is simply 50% of that previous bill.

Let’s walk through a real-world example.

Example: A Freelance Designer's First Big Bill

Imagine you're a freelance graphic designer. For the 2023/24 tax year, your final tax and National Insurance bill works out to £4,000. You get organised and file your return in December 2024. Here’s how the payments play out:

- 31 January 2025 Deadline: First, you have to settle up for the year that's just finished. That’s the full £4,000 you owe for 2023/24. This is known as the 'balancing payment'.

- First Payment on Account: On the exact same day, HMRC also asks for your first advance payment for the next tax year (2024/25). This is calculated as 50% of the previous year's £4,000 bill, so that’s another £2,000.

- 31 July 2025 Deadline: Six months later, you’ll pay the second and final Payment on Account for the 2024/25 tax year. This is the remaining 50%, which is another £2,000.

This means that on 31 January 2025, your total bill is a whopping £6,000 (£4,000 for last year + £2,000 for this year). This is the 'double payment' shock that catches so many off guard.

The shock of the first Payment on Account is a rite of passage for many self-employed professionals. It effectively means that in your first year of significant profit, your January tax payment can be 150% of what you were expecting.

By the end of July 2025, you'll have paid £4,000 towards your 2024/25 tax bill. When you eventually file that return (by January 2026), HMRC will calculate your actual liability. If it turns out to be, say, £4,500, you’ll only have a £500 balancing payment to make, because you’ve already paid the first £4,000.

Managing Your Payments And When They Aren't Required

Getting your head around this system is key to managing your business finances. It’s why every experienced freelancer will tell you to set aside a portion of your income for tax as you go. You can’t afford to wait until the deadline is looming.

A good rule of thumb is to siphon off 25-30% of every payment you receive into a separate savings account. That way, the money is ready when HMRC comes knocking.

It's also worth knowing that these payments aren't set in stone. If your income drops significantly one year, you can ask HMRC to reduce your Payments on Account to better reflect what you actually expect to earn. This is far better than overpaying and waiting months for a refund. It's crucial to understand when you don’t need to make Payments on Account so you're not paying more than you need to.

By planning for these two crucial dates—31 January and 31 July—you can turn Payments on Account from a financial nightmare into a predictable part of your business calendar. It’s a proactive habit that truly separates the stressed-out from the successful in the self-employed world.

The True Cost of Missing a Tax Deadline

Thinking of the tax return self employed deadline as a soft suggestion is a costly mistake. The moment the clock strikes midnight on 31 January, HMRC’s penalty system kicks in automatically. It’s not a case of getting a gentle nudge or a grace period—it’s an immediate financial hit.

The second your tax return becomes overdue, you’re on the hook for an instant £100 fixed penalty. It doesn't matter if you owe £10 or £10,000; the penalty applies just for being late. Think of it as the starting gun for a race you really don't want to be in, where the costs quickly mount up.

What starts as a manageable £100 fine can easily spiral into a debt of thousands. The whole system is designed to get your attention and ensure you treat your tax obligations with the seriousness they deserve.

The Escalating Penalty Timeline

After that first £100 sting, you have a three-month window to get your return submitted. But if you’re still behind after that, things get a lot more expensive, fast.

From the three-month mark, a daily penalty of £10 starts ticking away. This can continue for up to 90 days, adding a potential £900 to your bill. So, if your return is six months late, you’re already looking at penalties of up to £1,000 (£100 initial fine + £900 daily fines). And that’s before you even account for the tax you actually owe.

Still haven't filed after six months? HMRC will add another penalty of either £300 or 5% of the tax due—whichever is higher. The same thing happens again if your return is a full 12 months late.

To make things even clearer, here’s a breakdown of how those penalties stack up.

HMRC Late Filing and Payment Penalty Timeline

This table shows how quickly the fines can escalate if you miss the Self Assessment deadlines for both filing your return and paying your bill.

| Delay | Late Filing Penalty | Late Payment Penalty |

|---|---|---|

| 1 day | Instant £100 fine. | – |

| 30 days | – | 5% of the tax owed. |

| 3 months | £10 per day for up to 90 days (max £900). | – |

| 6 months | £300 or 5% of tax owed (whichever is higher). | Additional 5% of tax owed. |

| 12 months | Another £300 or 5% of tax owed (whichever is higher). | A further 5% of tax owed. |

As you can see, the costs for being late with your return and your payment are separate but can combine to create a significant financial headache.

On top of all the penalties, HMRC also charges interest on any tax you haven't paid, starting from the day it was due. This interest keeps accumulating, turning what might have been a small oversight into a much larger financial burden.

Late Payment Penalties

It's crucial to understand that filing your return and paying your tax are two different things, and HMRC penalises them separately. You can file on time but still get hit with fines if you don't pay what you owe.

The penalties for paying late are structured like this:

- 30 days late: You’ll be charged 5% of the tax you owe.

- 6 months late: An additional 5% penalty is added to the bill.

- 12 months late: You guessed it—another 5% penalty is applied.

These charges are on top of any late filing penalties and the daily interest accruing on your debt. The system is designed to penalise both failures: not providing your information and not paying your dues. If you want to dig into the specifics, you can learn more about penalties for late tax payments and see exactly how the charges are worked out. Staying informed is the best way to keep your business financially healthy.

How To File Your Return and Beat The Deadline

Knowing the key dates for the self-employed tax return deadline is one thing, but actually getting it done on time is another beast entirely. So, let's move from theory to action. This is your practical, step-by-step playbook for getting your tax return filed and paid without the last-minute panic that trips up so many people every year.

The aim here isn't just to tick a box for HMRC. It's about turning a dreaded annual chore into a calm, manageable process. With a clear roadmap, you can cut through the overwhelm and prove to yourself that beating the deadline is entirely possible—it just takes a bit of forward planning. Let's break it down.

Step 1: Assemble Your Financial Paperwork

Before you even dream of logging into the HMRC portal, you need to get your financial records in order. This is the bedrock of an accurate tax return. Trying to file without your documents is like trying to bake a cake without the ingredients – it’s just not going to work.

Start by gathering everything that shows money coming into and going out of your business during the tax year.

- Income Records: Pull together all your sales invoices, records of any cash you've taken, and details of any other payments you received for your work.

- Bank Statements: Your business and personal bank statements are essential for cross-referencing every penny of income and expenditure.

- Expense Receipts: This is a big one. Collect every single receipt for your allowable business expenses. This covers everything from software subscriptions and office supplies to travel costs and a portion of your utility bills.

Having all this information organised and ready to go will make the actual filing process unbelievably smoother and faster.

Pro-Tip: Please don't wait until January to start this. Using a bookkeeping app or even a simple spreadsheet throughout the year transforms tax time from a nightmare into a breeze. A few minutes of admin each week will genuinely save you days of stress later on.

Step 2: Choose Your Filing Method

Once your documents are neatly piled up, you need to decide how you're actually going to submit your return. For most self-employed people, this comes down to two main online options.

HMRC's Online Service

This is the government's free, official portal. It’s a straightforward, no-frills system that guides you through the necessary sections of the tax return. It's a solid choice if your finances are fairly simple – for instance, if you're a sole trader with one stream of income and basic expenses.

Third-Party Accounting Software

Platforms like Xero, QuickBooks, or FreeAgent offer a much more integrated experience. These tools don't just let you file your Self Assessment directly with HMRC; they also help you manage your bookkeeping, invoicing, and expenses all year round. They come with a subscription fee, but they often pay for themselves in saved time and valuable insights into your business's financial health. If your situation is a bit more complex, this is often the better route.

For more on this, check out our guide with more tips for stress-free self-assessment tax filing to help you get prepared.

Step 3: Calculate and Submit Your Figures

With your paperwork gathered and your platform chosen, the final step is to punch in the numbers and get to the bottom line. You’ll enter your total income and then systematically add up all your allowable expenses to work out your taxable profit.

This is where your earlier organisation really pays off. A well-kept record of expenses ensures you claim every deduction you're entitled to, which can make a huge difference to your final tax bill. Once you’ve filled everything in, the system will calculate your tax and National Insurance liability.

Before you hit that 'submit' button, check it. Then check it again. A simple typo can cause major headaches down the line. After you've filed, you'll get an instant confirmation from HMRC. Make sure you save this, along with a PDF copy of your full tax return, for your own records.

And please, don't fall into the trap of leaving it to the last minute. Every year, people get caught out. For the 2022–23 tax year, HMRC recorded a staggering 778,068 returns filed on 31 January alone, with over 32,000 submitted in the final hour! It’s a common habit, but a risky one. You can read more about it in the official government filing statistics.

Common Questions About Tax Return Deadlines

Let's be honest, even with the best intentions, life can get in the way as the tax return self employed deadline looms. Maybe a big project ran over, your income has been all over the place, or something unexpected just threw a spanner in the works. It’s completely normal to have a few nagging "what if" questions.

This section is here to tackle those common worries head-on. We'll get straight to the point, answering the questions that pop up most often around tax deadlines so you can handle tricky situations with confidence and without the stress.

What If I Know I'm Going To Be Late?

That sinking feeling when you realise you won't hit the 31 January deadline is awful. But burying your head in the sand is the absolute worst thing you can do. The key here is to be proactive.

Contact HMRC as soon as you know you’re going to be late. Don't wait for the brown envelope to drop through your letterbox. By getting in touch first, you’re showing them you're taking your responsibilities seriously and aren't just trying to duck the issue. This alone can make a huge difference in how they handle your case.

Explain your situation clearly and honestly. If you need a bit more time to pay, they might offer a 'Time to Pay' arrangement, which lets you spread the cost. While this won't wipe out a late filing penalty, it can stop late payment penalties from piling up and shows goodwill.

Can I Reduce My Payments On Account?

Yes, you can, and this is a vital tool for managing your cash flow. Payments on Account are HMRC's way of getting you to pay your tax bill in advance, based on your previous year's earnings. This works fine if your income is steady, but it's a real problem if your earnings have dipped. You can end up overpaying and waiting months for a refund.

If you’re confident your tax bill for the current year will be lower, you can ask HMRC to reduce your Payments on Account. You’ve got two main ways to do this:

- Through your online account: Just log in to your HMRC Self Assessment account and you'll find an option to reduce the payments.

- On your tax return: If you file your return before the payment deadline, the new, lower calculation will automatically adjust what you owe.

A word of warning: be realistic. If you reduce your payments too much and end up underpaying your tax, HMRC will charge you interest on the shortfall. Make your estimate based on what you’ve actually earned.

What Is A Reasonable Excuse For Late Filing?

HMRC is strict, but they aren't heartless. They will consider cancelling penalties if you had a 'reasonable excuse' for missing the deadline. But be warned, their definition of 'reasonable' is very specific and doesn't cover simply forgetting or being too busy.

So, what actually counts?

- Serious or life-threatening illness affecting you or a close family member.

- The death of a partner or close relative shortly before the deadline.

- An unexpected stay in hospital that stopped you from dealing with your tax.

- Technical issues with HMRC's online services on the final day (you’ll need proof).

- Fires, floods, or other disasters that destroyed your records or severely disrupted your life.

You absolutely must have proof to back up your claim, like a doctor's note or a screenshot of the HMRC service error. You also have to file your return and pay the tax as soon as your situation is resolved. Forgetting your password or blaming an accountant who let you down just won't cut it.

How Far Back Can HMRC Investigate My Taxes?

This is a common worry, but thankfully, there are clear time limits on how far back HMRC can dig into your tax affairs. How long they get depends entirely on your behaviour.

Here's how the enquiry windows break down:

- Careful and Accurate Returns: If you've taken reasonable care to get things right, HMRC usually only has 12 months from the filing deadline to open an enquiry. For a 2023/24 return filed on 31 January 2025, that window slams shut on 31 January 2026.

- Careless Mistakes: If HMRC has reason to believe you've made a careless error, they can look back up to 6 years.

- Deliberate Errors: If they suspect you have deliberately filed an incorrect return or are involved in tax avoidance, the window extends all the way to 20 years.

This really highlights why it’s so important to keep organised, accurate records for at least six years. It's your evidence, your backup, and your peace of mind.

Navigating Self Assessment can be tricky, but you don't have to go it alone. If you're struggling to meet deadlines or just want to be sure everything is managed perfectly, Stewart Accounting Services can help. We provide expert guidance to take the stress out of tax season, giving you more time, more money, and a clearer mind. Visit us at https://stewartaccounting.co.uk to learn how we can support you.