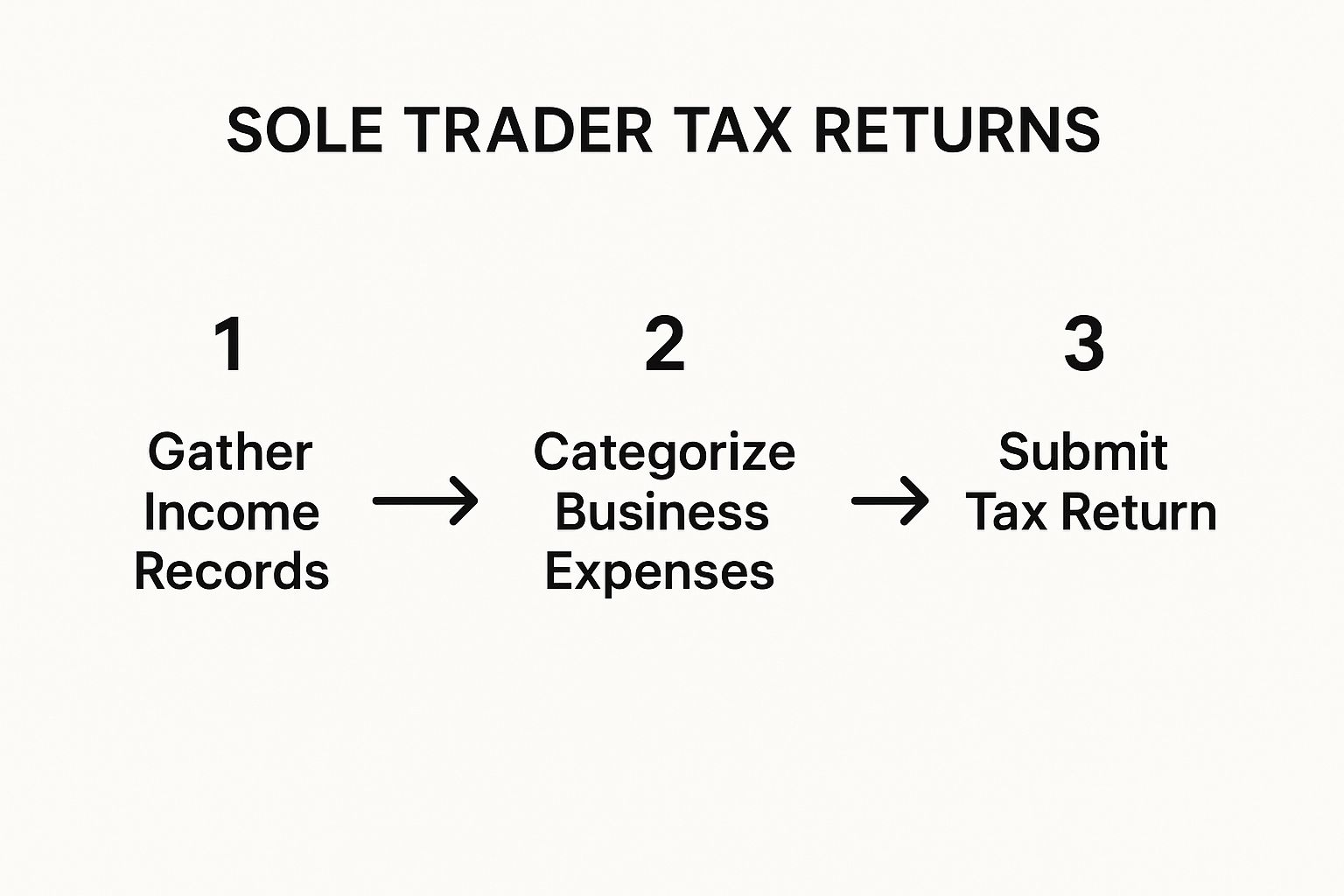

Filing your first tax return as a sole trader is a rite of passage. It's how you officially report your income and expenses to HMRC through the Self Assessment system. The whole process can feel a bit intimidating at first, but trust me, getting your registration and records sorted from day one is the secret to a smooth, stress-free experience.

Getting Set Up for a Painless Tax Return

Launching your own business is a brilliant feeling, but the paperwork that comes with it? Not so much. The good news is that preparing for your first sole trader tax return is actually pretty straightforward. A little bit of organisation now will save you a world of pain when the filing deadline starts creeping closer.

Your very first job is to tell HMRC you’re a sole trader. You need to get this done by 5 October in your business's second tax year. Once you're registered, HMRC will send you a 10-digit Unique Taxpayer Reference (UTR) number. This is your key to the whole tax system, so keep it somewhere safe – you’ll need it for everything Self Assessment-related.

Keeping Your Financial Records in Order

This part is non-negotiable: you have to keep good records. HMRC can ask to see your business's sales and expense records for at least five years after the 31 January submission deadline for that tax year. Don’t worry, this doesn't have to be complicated. A simple spreadsheet or some basic accounting software is all you really need.

Make sure you're tracking these essentials:

- All your sales and income: Every single invoice you issue, paid or not.

- All your business expenses: Keep the receipts for everything you buy for your business. Think software, stationery, travel – the lot.

- Bank statements: Seriously consider getting a separate business bank account. It makes it so much easier to distinguish your business finances from your personal spending.

- VAT records: If you're VAT-registered, you'll need to keep these records meticulously.

Getting this foundation right is the most important part of the entire process, as this image shows.

As you can see, a successful submission is built on a solid base of good record-keeping. While you're getting your business admin in order, it's also a smart move to look into essentials like business insurance to make sure you're properly protected.

Key Deadlines and What You Need to Know

Knowing your dates is absolutely crucial to avoid any penalties. For most sole traders, it all revolves around the UK tax year, which runs from 6 April to 5 April.

To help you keep track, here’s a quick rundown of the most important dates and thresholds you’ll need to remember.

Key Sole Trader Tax Deadlines and Requirements

| Task | Deadline / Threshold | Key Detail |

|---|---|---|

| Register for Self Assessment | 5 October after the end of the tax year you started trading | You must do this to get your UTR and be able to file a return. |

| Online Tax Return Filing | Midnight, 31 January | This is the final deadline to submit your online return for the previous tax year. |

| Pay Your Tax Bill | Midnight, 31 January | The tax you owe must be paid by the same deadline as filing your return. |

| Paper Tax Return Filing | Midnight, 31 October | If you choose to file by post, the deadline is much earlier. |

| Payments on Account | 31 January and 31 July | Advance tax payments if your bill is over £1,000. |

These dates are the bedrock of the Self Assessment calendar. Missing them can lead to automatic fines, so get them in your diary now!

One thing that often catches new sole traders out is 'payments on account'. If your tax bill tops £1,000, HMRC will ask you to make advance payments towards your next year's tax bill. These are due in two chunks, on 31 January and 31 July.

A word of warning from experience: get your head around payments on account as early as you can. It can make your first tax bill feel huge because you’re often paying for the year just gone plus the first instalment for the year ahead. Budget for this from the get-go to avoid a cash flow shock.

Calculating Your Income and Allowable Expenses

This is where the rubber meets the road. Getting your sole trader tax return right boils down to one thing: calculating your profit figure correctly. It’s not just a case of totting up your invoices. The real skill is in meticulously subtracting every single legitimate business cost to make sure you pay the right amount of tax – and not a penny more.

First things first, your income. You need to declare every penny your business has earned. This obviously includes the main payments from clients, but don't forget the smaller bits and pieces. For instance, if you're a freelance graphic designer who also sold a few digital templates on the side, that income counts too. The easiest way to keep track is to have a dedicated business bank account. It gives you (and HMRC) a crystal-clear picture of what's come in.

Now for the part that actually reduces your tax bill: allowable expenses. These are the running costs of your business, and the golden rule from HMRC is that they must be "wholly and exclusively" for business purposes. It sounds simple, but the reality can be a bit murky. Let's clear things up with some practical examples.

Everyday Business Running Costs

Think about the day-to-day things you buy to keep your business ticking over. These are often the easiest expenses to claim on your tax return.

- Office Supplies: This is all the basics, from printer paper and ink cartridges to postage and business stationery.

- Software Subscriptions: Do you pay for accounting software like Xero, a project management tool like Trello, or a subscription to the Adobe Creative Suite? It's all allowable.

- Professional Memberships: If you pay an annual fee to a professional body or trade organisation to do your job, you can claim it. An electrician’s NICEIC registration is a perfect example.

- Marketing and Advertising: This bucket covers everything from your website hosting costs and Google Ads campaigns to printing new business cards.

Don't underestimate these small costs. They add up. A seemingly minor £20 monthly software subscription is a £240 deduction from your profit at the end of the year.

Working From Home Expenses

Loads of sole traders work from home, and thankfully, HMRC allows you to claim for it. You’ve got two main routes to go down here.

The first is HMRC's 'simplified expenses' flat rate. It's a no-fuss option where you can claim a set monthly amount based on how many hours you work from home. Quick, easy, and no complicated maths required.

The other option is to calculate the actual costs. This means figuring out what proportion of your home running costs are down to your business. For instance, if you have a five-room house and one room is used purely as your office, you could claim 20% of your utility bills, council tax, and even your mortgage interest or rent. This method usually gets you a bigger deduction but demands much better record-keeping.

My Tip: Pick a method and stick with it for the whole tax year. You can’t mix and match. Before you start, do a quick calculation to see which approach will be more beneficial for your specific situation.

Travel and Other Significant Costs

Business travel is another big area for expenses, but the rules are very clear. You can claim for journeys you make for business, but your daily commute to a permanent workplace is a definite no-no.

- Vehicle Mileage: If you use your own car for work trips, you can claim a simplified mileage allowance. For cars and vans, that’s 45p per mile for the first 10,000 miles and 25p for every mile after that.

- Public Transport: Train tickets, bus fares, and taxis to client meetings are all perfectly claimable.

- Overnight Stays: If a business trip means you have to stay away from home, the cost of your hotel and reasonable meals are also deductible.

It’s also worth remembering that some personal policies might have business tax implications. For example, when you're going through your allowable expenses, it's a good idea to look into any potential health insurance tax benefits that could help lower your taxable income.

Finally, don’t forget about training. If you take a course to update your existing skills, you can claim the cost. A copywriter taking a course on SEO, for instance, can deduct it. What you can’t claim for is training that gives you a brand-new skill to start a different business. Being thorough and honest about every expense is the key to a fair and accurate tax return as a sole trader.

How to File Your Self Assessment Online

Gathering your income and expenses is one thing; submitting your sole trader tax return online is another. Once your figures are at your fingertips, HMRC’s portal guides you through each question with surprising ease.

You start on the SA100, the main form for everyone filing a Self Assessment. As a sole trader, you’ll then fill in the SA103 self-employment pages, detailing business sales, expenses and any capital allowances.

After you log in with your Government Gateway ID, the system asks targeted questions. You won’t find yourself wading through irrelevant sections—just the bits you need.

Cash Basis Vs Traditional Accounting

One of the earliest decisions on the SA103 is choosing your accounting method. From my experience, freelancers often prefer one over the other:

-

Cash Basis Accounting

Record income when it hits your bank and expenses when you pay them. An invoice sent in March but paid in May goes into the new tax year. -

Traditional Accounting (Accrual Basis)

Log income when you issue the invoice and expenses when they’re incurred, regardless of payment dates. You get a clearer financial snapshot, but bookkeeping must be spot-on.

Most sole traders under £150,000 turnover gravitate towards cash basis. It ties your tax bill to actual cash flow, making it easier to plan.

Key Takeaway: Cash basis is often the most intuitive route for freelancers. You owe tax only on money you’ve received, so budgeting becomes straightforward.

Looking Ahead To Making Tax Digital

Big changes are coming with Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA). The goal is to replace annual paper returns with regular digital updates via approved software.

The rollout is phased by income band:

- From April 2026: Self-employed individuals earning over £50,000 must comply with MTD for ITSA.

- From April 2027: The requirement extends to those with income between £30,000 and £50,000.

In the 2023–2024 tax year, around 7.0 million landlords and sole traders completed a Self Assessment. Among those earning above £50,000, 63% already use software—often alongside an accountant. You can explore the full MTD business population statistics on HMRC’s official page.

Getting to grips now with tools like Xero or QuickBooks means next year’s filing will feel seamless. Beyond tax time, real-time financial insights help you steer your business more confidently throughout the year.

Understanding Your Final Tax Bill And Payments

You’ve triple-checked every receipt, claimed all your expenses and finally clicked Submit on your sole trader return. Moments later, HMRC’s system crunches the numbers and spits out your total bill – a blend of Income Tax plus two flavours of National Insurance. Understanding each piece of that final figure isn’t just bookkeeping; it’s essential if you want to stay in control of your cash flow.

Breaking Down Your Tax Calculation

Right after submission, you’ll see a summary that splits your liability into three main components:

- Income Tax: Charged on your taxable profits (that’s total income minus allowable costs) according to the UK’s tax bands. Only the portion above your Personal Allowance gets taxed.

- Class 2 National Insurance: A flat-rate weekly fee (for 2023/24 it’s payable if your profits exceed the Lower Profits Threshold). This contribution keeps you eligible for state benefits.

- Class 4 National Insurance: A percentage-based charge on profits between the Lower and Upper Profits Limits. You pay more as your earnings rise through each band.

Together, these three items form the total liability for the year you’ve just filed.

The Reality Of Payments On Account

Here’s a scenario that trips up many newcomers. If your total tax bill tops £1,000, HMRC will automatically set up payments on account. Essentially, you pre-pay part of next year’s tax in two instalments.

Say your 2023/24 bill lands at £3,000. Because that exceeds £1,000, you owe:

- The outstanding £3,000 for 2023/24 by 31 January.

- A first advance of £1,500 (50 per cent of this year’s bill) for 2024/25, also due 31 January.

On 31 January you’ll need £4,500 in the bank – the £3,000 balance plus £1,500 forward payment. The second £1,500 follows on 31 July. Budgeting from day one turns this shock into a manageable plan.

How To Pay Your Tax Bill

HMRC provides several straightforward payment channels:

- Online or telephone banking (Faster Payments)

- CHAPS or BACS transfer

- Debit card payment via the portal

- Direct Debit (if arranged before the deadline)

- In-branch at your bank or building society

Every payment must carry your 11-character reference (your 10-digit UTR plus ‘K’). Using the wrong reference can cause delays and headaches. Also, don’t forget that extra income streams—like grants—can alter what you owe. For clarity on this, explore the tax implications of government grants.

Missed deadlines incur interest and penalties right away. Stay organised, set reminders and you’ll keep both your finances and your relationship with HMRC on solid ground.

Common Mistakes to Avoid on Your Tax Return

Getting your sole trader tax return submitted feels like a huge weight off your shoulders. But that relief can be short-lived if a simple, avoidable error brings it all crashing back down, complete with penalties and unwelcome letters from HMRC.

The good news is that most of these mistakes aren't about complex tax law; they're basic oversights often made in the last-minute rush. By knowing what to look out for, you can sidestep these common pitfalls and file with confidence.

Forgetting to Declare All Your Income

It's surprisingly easy to miss something, especially when money is coming in from different places. Maybe you have your main freelance client but also sell a few digital products on the side, or you did a one-off cash job months ago that you've since forgotten.

Every single pound your business earns has to be on that return. Don't be tempted to think a small amount will fly under the radar—HMRC has incredibly sophisticated systems for spotting discrepancies. Keep a detailed log of all income, no matter how minor it seems at the time.

Mixing Business and Personal Expenses

This is probably the number one trap for new sole traders. The rule is simple, but often misinterpreted: you can only claim expenses that are “wholly and exclusively” for your business. When the line between your personal and business spending gets blurry, you’re waving a red flag at HMRC.

A few classic slip-ups I see all the time include:

- Claiming your entire mobile phone bill when you only use it for business 40% of the time. You must work out the business portion and claim only that.

- Guessing at your vehicle mileage instead of keeping a proper log. You need a record of each business journey to back up what you're claiming.

- Trying to claim your weekly food shop as "subsistence" because you work from home. Unfortunately, that’s not an allowable expense.

A Quick Tip From Experience: The best thing you can do is open a separate business bank account from day one. It creates a clear, undeniable line between your personal and business finances, making it infinitely easier to spot legitimate expenses and prove them if you’re ever asked.

Poor (or Non-Existent) Record Keeping

Let's be blunt: you can't file an accurate tax return as a sole trader without good records. A shoebox full of crumpled receipts just won't cut it. Failing to keep organised invoices, receipts, and bank statements is a recipe for disaster.

Not only do you risk making inaccurate claims, but you also won't have any evidence to support your figures if HMRC decides to investigate.

Remember, you're legally required to keep your business records for at least five years after the 31 January submission deadline for that tax year. A simple spreadsheet or basic accounting software can be your best friend, turning chaos into clarity.

This is a bigger issue than you might think. The "tax gap" for the Self Assessment sector was recently estimated at a staggering £5.8 billion—that's 22.7% of the tax that should have been collected. A huge part of this comes down to disorganised finances. You can read more about these UK tax gap statistics on GOV.UK.

Missing Crucial Filing Deadlines

The Self Assessment deadlines are fixed and completely unforgiving. Missing the 31 January online filing and payment deadline means you get an immediate £100 penalty. That applies even if you don't owe any tax.

The penalties then escalate quickly the longer you leave it. My advice? Set multiple calendar reminders and aim to get your return filed well before Christmas. This gives you breathing room to sort out any problems without the last-minute panic that causes so many of the other mistakes on this list. Procrastination is your worst enemy here.

Avoiding Common Sole Trader Tax Return Errors

It's easy to feel overwhelmed, but most errors come down to a handful of recurring issues. Here’s a quick-glance table to help you keep these common mistakes front of mind.

| Common Mistake | Potential Consequence | How to Avoid It |

|---|---|---|

| Undeclared Cash Income | An HMRC investigation, back-taxes, and significant penalties for undeclared earnings. | Log every single payment you receive immediately, whether it's a bank transfer, cheque, or cash. Use an app or a simple spreadsheet. |

| Incorrect Expense Claims | Claim disallowed, leading to a higher tax bill. Repeated errors can trigger a compliance check. | Get a separate business bank account. Only claim for costs that are 100% for the business. If it's mixed-use, work out the business percentage. |

| "Guesstimating" Figures | You'll have no proof if HMRC asks for evidence, and your return will be considered inaccurate. | Keep all receipts and invoices! Scan them or use an accounting app. For mileage, use a logbook or a GPS tracking app. |

| Missing a Deadline | An instant £100 fine, with costs spiralling up the longer you delay. Interest is charged on late payments. | Set calendar alerts for early January. Aim to file before the Christmas break to avoid the last-minute stress. |

By being methodical and organised from the start of the tax year, not just in January, you make the entire process smoother and significantly reduce your risk of making a costly mistake.

Got a Few More Questions About Your Sole Trader Tax?

Even after you’ve waded through the main sections, it’s completely normal to have a few niggling questions left over. I’ve put together this quick-fire Q&A to tackle some of the most common queries I hear from sole traders, so you can file your return with complete confidence.

What if My Business Made a Loss? Do I Still Need to File?

Yes, absolutely. You must complete a Self Assessment tax return even when your business hasn't turned a profit. In fact, reporting a loss can be a smart move. You can carry that loss forward to offset against profits in future years, which ultimately lowers your tax bill down the line.

Let's say your photography business had allowable expenses of £8,000 but your income was only £5,000. That’s a £3,000 loss. By declaring it on your tax return, you can use that £3,000 to reduce your taxable profit next year, saving you real money.

What Happens if I File My Tax Return Late?

You can, but it’s going to hurt your wallet. HMRC issues an immediate £100 penalty if you miss the 31 January online filing deadline. This penalty applies even if you don't owe any tax or have already paid what you thought you owed.

The penalties get steeper the longer you wait:

- Over 3 months late: You could be charged daily penalties of £10 a day, up to a maximum of £900.

- Over 6 months late: Another penalty kicks in – either £300 or 5% of the tax you owe, whichever is higher.

- Over 12 months late: You'll face a further penalty of £300 or 5% of the tax due, again, whichever is the higher amount.

On top of all that, HMRC charges interest on any tax you haven't paid. It’s a costly mistake to make, so getting your return in on time is non-negotiable.

I Run More Than One Business – How Does That Work?

If you're juggling multiple ventures as a sole trader, you'll need to report the figures for each one separately. Say you’re a freelance writer but also run a small online shop selling handmade crafts. You’d need to fill out a separate set of self-employment (SA103) pages for your writing and another for your craft shop.

Each business will have its own dedicated income and expense figures. You then simply add up the net profit (or loss) from each one to get your total self-employed income, which you’ll enter on the main SA100 tax return.

Keeping meticulous, separate financial records for each business is crucial here. It doesn't just make filling out the tax return a thousand times easier; it gives you a much clearer picture of how each part of your self-employed empire is actually performing.

Help! I've Spotted a Mistake on a Return I've Already Sent.

Don't panic – it happens to the best of us. If you realise you've made a mistake after filing, you can easily amend your return online through your HMRC account.

You typically have up to 12 months from the original filing deadline to make any corrections. This gives you a decent window to add a forgotten expense or fix an income figure you typed in wrong. Just log in, find the return you need to edit, and choose the option to amend it. HMRC’s system will then recalculate your tax liability for you.

Tackling your tax returns as a sole trader can feel like a mountain to climb, but you don't have to go it alone. The experts at Stewart Accounting Services are here to manage your self-assessment from start to finish, keeping you compliant and helping you hold onto more of your hard-earned cash. Visit us at https://stewartaccounting.co.uk to see how we can give you back your time and peace of mind.