When you hear the word "depreciation," you might think of a car losing value the moment you drive it off the forecourt. While that’s one meaning, in accounting, it’s something quite different and far more important for understanding a business's health.

In accounting terms, depreciation is the methodical way we spread the cost of a physical asset over its useful life. It’s not about tracking the asset’s real-time market value. Instead, it’s an accounting practice that matches the cost of using an asset to the revenue it helps generate over time. This gives you a much truer picture of your company's profitability.

The Core Concept of Depreciation

Let's make this real. Imagine your business buys a new delivery van for £30,000. If you treated that entire £30,000 as an expense in the month of purchase, your profit and loss statement for that month would take a massive hit. It would look like you had a terrible month, even if sales were strong.

Worse, the following months and years would look artificially profitable because you'd still be using the van to make deliveries and earn revenue, but its cost would be long gone from your expenses. That’s just not an accurate reflection of reality.

Depreciation fixes this mismatch. It lets you spread that £30,000 cost across the van’s expected working life—let's say, five years. By expensing a portion of the van's cost each year, you're accurately reflecting that the asset is being "used up" while it helps your business make money.

This isn't just good practice; it’s a cornerstone of accounting that ensures your financial statements are fair, consistent, and reliable. Without it, you’d never get a true handle on your operational costs or long-term financial performance.

Key Terms You Need to Know

Before we dive into the calculations, let's get a few key terms straight. Think of these as the essential ingredients for any depreciation recipe. Understanding them will make the whole process much clearer.

Key Depreciation Terms at a Glance

| Term | Simple Definition | Example |

|---|---|---|

| Asset Cost | The total amount paid for an asset, including delivery, installation, and any other costs to get it ready for use. | The £30,000 price of the van, plus £500 for signwriting. Total cost is £30,500. |

| Useful Life | The estimated period the business expects to use the asset to generate income—not its total physical lifespan. | The van might physically last 10 years, but you plan to replace it after 5 years of active service. |

| Salvage Value | Also known as residual value, this is the estimated amount you could sell the asset for at the end of its useful life. | After 5 years, you estimate you can sell the used van for £5,000. |

| Book Value | The asset's current value on your balance sheet. It's the original cost minus all the depreciation recorded so far. | After one year, the van's book value would be its original cost minus one year's depreciation expense. |

Getting comfortable with these terms is the first step. They are the foundation upon which all depreciation methods are built, so it's worth taking a moment to let them sink in.

Depreciation is an accounting method of allocating the cost of a tangible asset over its useful life. It is used to account for declines in value and is a cornerstone of accurate financial reporting.

This principle isn't just for private companies; it's applied everywhere, from local councils to major government departments. Public bodies also depreciate their assets to write off the costs over time. For instance, the UK Statistics Authority reported assets like computers and furniture with a net book value of £13,525,000 by March 2024, demonstrating how depreciation gradually reduces asset values on paper. You can find more details like this in official publications like their annual report about UK government accounts.

It's easy to dismiss depreciation as just another box-ticking exercise for the accounts department, but that’s a dangerous mistake. Failing to record it properly can completely warp your view of your company's financial health, leading to some truly awful business decisions. It’s not an optional extra; it's a non-negotiable part of sound financial management for three critical reasons.

First and foremost, depreciation is all about upholding a cornerstone of accounting: the matching principle. In simple terms, this principle says you must match your expenses to the revenue they helped you earn in the same period. By spreading an asset’s cost over the years it's in service, you’re accurately matching a piece of that cost against the income it generates each year.

This gives you a much more honest picture of your profitability. Without it, you'd have a huge expense hit in year one, making it look like you've had a terrible year, followed by several years of artificially high profits. That kind of rollercoaster accounting doesn't help anyone make smart decisions.

Keeping Your Balance Sheet Honest

Beyond the profit and loss account, depreciation plays a vital role in making sure your balance sheet tells the truth. Your balance sheet is supposed to be a snapshot of what your company is worth right now, and an old piece of machinery bought five years ago clearly isn't worth what you originally paid for it.

Depreciation systematically lowers the asset's value on your balance sheet—its book value—over time. This adjustment ensures your financial statements present a realistic and fair picture of your company's total assets.

Ignoring depreciation is like pretending your five-year-old company van is still brand new. Your balance sheet quickly becomes a work of fiction instead of a statement of fact, which can seriously mislead investors, banks, and even you.

Planning for What's Around the Corner

Finally, and perhaps most practically, depreciation is a crucial tool for looking ahead. Your physical assets won't last forever. Your delivery van will eventually give up, your production line will wear out, and your office computers will become relics.

Tracking depreciation acts as a constant, year-on-year reminder of this inevitable decline. By watching the book value of your assets go down, you can start to predict when they'll need replacing. This allows you to plan for those big capital outlays, manage your cash flow, and avoid the sudden panic when a critical piece of equipment dies unexpectedly. It turns a future crisis into a manageable, planned expense.

Choosing the Right Depreciation Method

Deciding how to calculate depreciation isn't just an arbitrary choice; the method you pick should genuinely reflect how your business uses an asset over its lifetime. There’s no single "best" way to do it. Each approach tells a slightly different story about an asset's value, and making the right call ensures your financial statements are as realistic as possible.

Let's break down the most common methods used here in the UK, starting with the simplest and most popular one. Getting to grips with these options will help you choose the one that makes the most sense for your assets and how you operate.

The Straight-Line Method

The straight-line method is by far the most straightforward and widely used way to calculate depreciation. It simply spreads the cost of an asset evenly across each year of its useful life. Think of it as slicing a cake into equal pieces.

This method is perfect for assets that lose value at a steady, predictable rate—things like office furniture, shop fittings, or fixtures. Its biggest advantage is its simplicity. You book the exact same depreciation expense every single year, which makes budgeting and financial forecasting much easier to manage.

The formula couldn't be simpler:

(Asset Cost – Salvage Value) / Useful Life = Annual Depreciation Expense

Let's say you buy new office desks for £10,000. You expect them to last for 5 years, and you reckon you could sell them for £1,000 at the end. The calculation would be:

(£10,000 – £1,000) / 5 years = £1,800 per year. Your business would then record £1,800 as a depreciation expense every year for the next five years.

The Reducing Balance Method

In stark contrast, the reducing balance method (sometimes called the declining balance method) front-loads the depreciation. It allocates a much larger chunk of an asset's cost to its early years and a progressively smaller amount to its later years.

This approach is a much better fit for assets that lose their value fastest right at the start, like vehicles, computers, and other high-tech equipment. Just think about a brand-new company van; its value plummets the moment it's driven off the forecourt, and that first year's drop is far steeper than its fifth.

Here, the formula applies a fixed percentage to the asset's book value (its original cost minus the depreciation already claimed) each year. As the book value shrinks, so does the annual depreciation charge. This often gives a truer picture of an asset's market value and its diminishing usefulness over time.

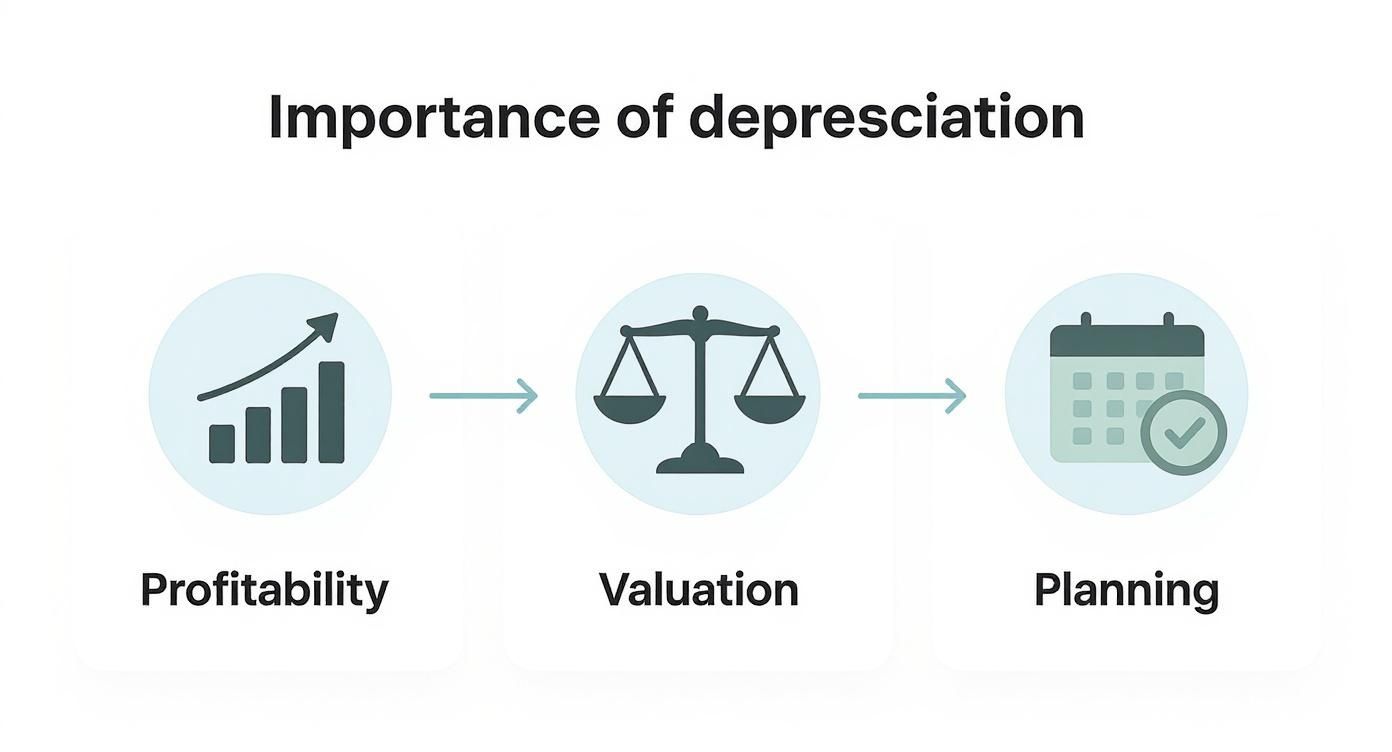

This infographic gives a great visual breakdown of why capturing this decline accurately is so crucial for understanding profitability, valuing your business, and planning for the future.

As you can see, getting depreciation right has a direct impact on how you measure profit, how much your company's assets are worth, and how you plan for future investments.

To make the difference between these two main methods crystal clear, let's look at a side-by-side comparison.

Comparing Straight-Line vs Reducing Balance Depreciation

Imagine your business buys a piece of equipment for £20,000 with an expected useful life of 5 years. With the straight-line method, we'll depreciate it by 20% each year. For the reducing balance method, let's use a more aggressive rate of 40% to reflect a faster initial loss of value.

| Year | Straight-Line Method Annual Expense | Reducing Balance Method (40%) Annual Expense |

|---|---|---|

| 1 | £4,000 | £8,000 |

| 2 | £4,000 | £4,800 |

| 3 | £4,000 | £2,880 |

| 4 | £4,000 | £1,728 |

| 5 | £4,000 | £1,037 |

Notice how the straight-line expense is constant, while the reducing balance charge starts high and drops off significantly each year. This table really highlights how the method you choose can drastically change your annual profit figures.

The Units of Production Method

Finally, there’s the units of production method. This one ties depreciation directly to an asset's actual usage, not the passage of time. It’s the perfect choice for manufacturing machinery or equipment where wear and tear is directly linked to how much work it does.

Instead of depreciating over a set number of years, you depreciate based on output—like the number of units it produces or the hours it runs.

Here’s how it works:

- Work out the depreciation rate per unit: (Asset Cost – Salvage Value) / Estimated Total Units Produced in its Lifetime.

- Calculate the annual depreciation: Rate Per Unit x Actual Units Produced That Year.

This method gives you an incredibly accurate way to match the expense of using an asset with the revenue it generates, which is a core accounting concept known as the matching principle. Even government bodies rely on these principles. For example, HM Land Registry has to account for the depreciation of its own equipment. In its 2021-22 financial year, it reported a depreciation charge of £4,360,000, which reflects the value its assets lost through use. You can dive deeper into how public sector bodies report these figures in their official financial statements.

Of course, how you acquire assets in the first place also has big accounting implications. For more on that, you can check out our guide on whether a hire purchase or lease rental is better for your business. Ultimately, the depreciation method you land on should give the most faithful and honest representation of how an asset contributes to your business over its lifespan.

How To Record Depreciation in Your Books

Once you've worked out the depreciation for a period, you can't just leave that number sitting on a spreadsheet. It needs to be properly recorded in your accounts through a formal journal entry. This is the only way to ensure your financial statements stay accurate and balanced, all based on the fundamentals of double-entry bookkeeping.

To get this right, you need to understand the two key accounts involved. Each one tells a different part of your company's financial story, and knowing their roles is the first practical step.

These accounts are:

- Depreciation Expense: Think of this as an expense account. It lives on your income statement (what many call the profit and loss, or P&L) and its job is to reduce your reported profit for that period.

- Accumulated Depreciation: This one's a bit different. It’s a contra-asset account, which is a fancy way of saying it’s tied to your assets but works in the opposite direction. It sits on your balance sheet, chipping away at the value of your fixed assets over time.

The Journal Entry Explained

The actual process of posting the journal entry is quite simple once you know which accounts to use. In bookkeeping, for every debit, there must be an equal and opposite credit. This is what keeps the whole system in balance. If you're new to this, our guide on the double-entry bookkeeping system provides a detailed example unpacked and is a great place to start.

When it comes to depreciation, the journal entry is always the same, which is handy.

You debit the Depreciation Expense account and credit the Accumulated Depreciation account.

Let's break that down. The debit increases your expenses for the period, while the credit increases the total depreciation that has built up against the asset. The result? The net book value of your asset goes down.

A Practical Example

Let’s put this into practice. Imagine your business has just bought some new office computers for £5,000. You’ve decided to use the straight-line method and calculated that the annual depreciation comes to £1,000.

At the end of the year, you’ll need to make this journal entry:

- Debit: Depreciation Expense for £1,000.

- Credit: Accumulated Depreciation for £1,000.

So, what does this do to your reports? Your income statement now shows a £1,000 expense, which reduces your overall profit. Meanwhile, on the balance sheet, the computers are still shown at their original cost of £5,000, but they're now accompanied by an Accumulated Depreciation account holding a £1,000 balance.

This brings their net book value down to £4,000 (£5,000 Cost – £1,000 Accumulated Depreciation). It's really important to use this separate 'accumulated' account because it keeps the asset's historical cost visible on your books. This transparency is vital for providing a clear audit trail. It’s a standard practice upheld by professional bodies like the Institute of Certified Bookkeepers, which sets the standards for maintaining precise financial records.

Understanding Depreciation and UK Corporation Tax

Here’s where things get a bit tricky for many UK businesses. The depreciation figure you carefully calculate for your accounts is vital for understanding your company's performance, but it plays no direct role in your UK Corporation Tax return. This is one of the most common points of confusion we see.

HMRC has its own, completely separate system for this, known as Capital Allowances. You can't just subtract your depreciation expense to reduce your taxable profit. Instead, the government lays out its own set of rules for how businesses can claim tax relief on the assets they purchase.

It helps to think of it as two parallel tracks: one for your financial reports and another, entirely different one, for HMRC.

Accounting Profit vs. Taxable Profit

The profit you see on your income statement—after you've deducted depreciation—is your accounting profit. It reflects the real-world wear and tear on your assets.

To figure out your taxable profit, however, you have to do something that feels counterintuitive: you must add the depreciation expense back. For tax purposes, it’s as if it never happened.

Only after adding it back can you then deduct the Capital Allowances you are entitled to claim for that year. This system gives the government control over how tax relief is given, often as a way to encourage business investment.

It's absolutely crucial to grasp this difference. Accounting depreciation is all about giving a 'true and fair' picture of your business's health. Capital Allowances, on the other hand, are a specific tax calculation driven by government policy. Confusing the two is a common and often expensive mistake.

A Quick Look at Capital Allowances

So, instead of depreciation, how do you actually reduce your tax bill for asset purchases? This is where Capital Allowances come in. These schemes are much more rigid than accounting depreciation methods.

Here are the main types you'll encounter:

- Annual Investment Allowance (AIA): This is a game-changer for most small and medium-sized businesses. It lets you deduct 100% of the cost of most qualifying plant and machinery in the year of purchase, up to a very generous annual limit. For a deeper dive, check out our detailed guide to the Annual Investment Allowance.

- Writing Down Allowances (WDAs): If your spending goes over the AIA limit, or for assets that don't qualify, you can claim WDAs. These feel a bit like the reducing balance method of depreciation, allowing you to deduct a set percentage of the asset's remaining value each year.

The financial scale of depreciation is enormous, even for the government. For instance, when Network Rail was reclassified as a public sector body, its assets had to follow government depreciation rules. This single accounting change increased total public sector depreciation by roughly £10 billion a year, highlighting just how significant these calculations are. You can read more about how government depreciation is forecast on the OBR website.

Ultimately, successfully running a UK business means you need to manage these two distinct systems—one for your own books and one for HMRC—to stay compliant and financially accurate.

Common Depreciation Questions Answered

Even after getting your head around the basics, depreciation can still throw up some tricky real-world questions. It’s one of those accounting concepts where the theory is one thing, but the practice has all sorts of nuances. It’s completely normal to have a few things you’re still not sure about.

Here, we'll run through some of the most common sticking points we see business owners grapple with. Think of it as a quick-fire Q&A to help you handle depreciation with a bit more confidence.

Can I Depreciate Land?

This is easily one of the most frequent questions we get, and the answer is a straightforward no. In the world of accounting, land is considered to have an indefinite useful life. It doesn't wear out, break down, or become obsolete in the same way a building or a delivery van does.

So, while you absolutely can (and should) depreciate any buildings, structures, or improvements on that land—like a car park or fencing—the land itself stays on your balance sheet at its original cost, forever.

What Happens When I Sell an Asset?

When you sell or get rid of an asset that you've been depreciating, you need to properly close the books on it. This involves a final calculation to work out whether you’ve made a gain or a loss on the sale.

First, you need to calculate and record any final depreciation right up to the date of the sale. Once that’s done, you compare the asset's net book value (what you originally paid for it, minus all the depreciation you've ever claimed) with the cash you got from selling it.

- If the sale price is higher than its book value, you've made a gain on the disposal.

- If the sale price is lower than its book value, you've taken a loss on the disposal.

This gain or loss then gets reported on your income statement. It’s a crucial final step to make sure the asset and all its related accumulated depreciation are removed correctly from your accounts.

Can I Change My Depreciation Estimates?

Yes, you can—and sometimes you have to. Remember, depreciation is built on estimates: how long you think an asset will last (its useful life) and what it might be worth at the end (its salvage value). If new information comes to light suggesting your original guesses were off, you should update them.

For example, you might realise a piece of machinery is proving far more durable than expected and will probably last for eight years instead of the five you first estimated.

The key thing here is that this is treated as a change in accounting estimate, not a correction of an error. You don't go back and fiddle with previous years' accounts. Instead, you adjust the depreciation calculation for the current year and all future years based on the new, more accurate information.

This approach keeps your financial reporting relevant and as true a reflection of the business as possible.

What Is Depreciation Recapture?

While we use capital allowances instead of depreciation for UK tax, the idea of "recapture" is still a relevant concept, particularly in property and investment. Depreciation recapture is essentially a tax rule designed to claw back the tax benefits a taxpayer may have enjoyed from claiming depreciation over the years.

Here’s the gist: when you sell an asset for a profit, tax authorities may decide that part of that profit is only there because you reduced the asset’s book value through depreciation. That portion of the gain can be taxed differently—often as regular income—instead of at the potentially lower capital gains rate.

For real estate, depreciation is often calculated over 27.5 years for residential property and 39 years for commercial property in other tax jurisdictions. If a property is sold for more than its depreciated value, the tax man effectively "recaptures" the benefit you received from those annual deductions. It's a complex area, and it’s always wise to get professional advice before selling any significant assets.

At Stewart Accounting Services, we help businesses across Central Scotland and the UK get to grips with complexities like depreciation and capital allowances every day. If you need clarity on your accounts or a proactive partner to help your business grow, get in touch with us. Learn more about our services at https://stewartaccounting.co.uk.