Making Tax Digital (MTD) is HMRC's major push to drag the UK tax system firmly into the digital age. It means businesses now need to keep their records electronically and use special software to send their tax information directly to HMRC.

Think of it like swapping your old paper-based bank statements and manual ledgers for a modern, real-time banking app—but for your taxes.

What Is Making Tax Digital, Explained Simply

At its heart, Making Tax Digital is all about how you record and report your tax information, not about changing the actual amount of tax you owe. The old-school approach of stuffing shoeboxes with receipts and wrestling with a single, massive tax return once a year is on its way out.

MTD brings in a more continuous and, frankly, more accurate way of managing your tax. The big idea is to make tax admin more efficient and much simpler for everyone involved. By getting businesses to go digital, HMRC hopes to cut down on the simple, honest mistakes that often lead to people paying the wrong amount of tax.

And this isn't just a pointless bit of admin. This change is a direct response to a very real problem. The UK loses around £5 billion every year just from errors and compliance issues in the Self Assessment sector. MTD is specifically designed to tackle that head-on. You can dig into the full scale of this issue in government reports on the tax gap problem.

The Two Pillars of Mtd

The whole MTD system is built on two core rules that every business caught by the rules has to follow:

- Keeping Digital Records: You have to record all your business income and outgoings using MTD-compatible software. This could be dedicated accounting software or even a set of digitally linked spreadsheets. The key is that paper ledgers and disconnected documents are no longer enough.

- Submitting Updates with Software: You must use this approved software to send summary updates straight to HMRC. For most people, this happens quarterly. The software talks directly to HMRC’s systems, creating a secure and seamless link for your tax data.

The essence of MTD is simple: it moves tax from a once-a-year headache to a more integrated part of your regular business bookkeeping. This gives both you and HMRC a much clearer, up-to-date picture of your finances.

This structured process helps you avoid that last-minute panic and gives you a much better estimate of your tax bill as you go, which is a huge help for financial planning. We’ve covered more about these important HMRC changes in our other articles if you want to dive deeper.

Making Tax Digital at a Glance

To give you a quick overview, here are the essential parts of the MTD initiative boiled down into a simple table.

| Component | Brief Description |

|---|---|

| Digital Record-Keeping | All business transactions (income and expenses) must be stored electronically using compatible software. |

| Compatible Software | You must use software that is approved by HMRC to connect and submit your tax information directly. |

| Quarterly Updates | Instead of one annual return, businesses submit summary updates of income and expenses every three months. |

| Final Declaration | An end-of-year process finalises your tax position, accounting for all income and confirming final figures. |

This table shows how the different elements work together to create a more continuous and accurate tax reporting cycle.

Who Needs to Follow Making Tax Digital?

Figuring out if Making Tax Digital (MTD) applies to you might seem a bit daunting at first, but it boils down to two things: the type of tax you pay (VAT or Income Tax) and how much you earn. HMRC is rolling this out in stages, so your start date depends on where you fit in.

Let’s break it down.

For most businesses, the MTD story began with VAT. If you're a VAT-registered business, the answer is straightforward: you must already be following MTD for VAT rules. This has been the case for everyone since April 2022, when the old turnover thresholds were scrapped.

It doesn’t matter if your taxable turnover is above or below the £85,000 registration threshold. If you’re registered for VAT, you need to be keeping digital records and filing your returns using MTD-compatible software. The days of manually typing figures into the old HMRC gateway are long gone.

MTD for Income Tax Self Assessment (ITSA)

The next big wave is for sole traders and landlords. Unlike the all-in approach for VAT, MTD for Income Tax Self Assessment (ITSA) is being phased in based on your total annual income from your business and property.

The rollout starts with higher earners first, giving smaller operations more time to prepare.

- From 6 April 2026: If your total annual gross income from self-employment and property is over £50,000, you’ll need to comply with MTD for ITSA.

- From 6 April 2027: The rules will expand to include anyone with a total annual gross income from self-employment and property of over £30,000.

It's worth noting that partnerships will join MTD for ITSA at a later date, which hasn't been announced yet. For now, limited companies are not part of MTD for ITSA, as they handle Corporation Tax separately.

This shift to MTD for Income Tax is huge, affecting an estimated 1.75 million people in the first two stages alone. The 2026 phase will bring in about 780,000 individuals, and the 2027 expansion will add another 970,000, completely changing how a massive part of the UK’s small business community handles its taxes. You can get more details on this from Avalara's 2026 MTD guide.

What Counts as "Qualifying Income"?

To know exactly when you need to start, you have to get your head around "qualifying income." This is your total gross income—your turnover—before you take off any business expenses.

HMRC is very clear about what counts towards the MTD for ITSA threshold. It includes:

- Your turnover from all sole trader businesses you run.

- Gross rental income from any UK or foreign properties you own personally.

Crucially, some income sources are left out of this calculation. Things like your salary from a job (PAYE), dividends, savings interest, and pensions do not count towards the £50,000 or £30,000 MTD for ITSA thresholds. For a full breakdown of what’s in and what’s out, have a look at our guide on understanding MTD qualifying income.

Getting this right is essential. For example, imagine you’re a landlord with £40,000 in gross rental income and you also have a full-time job paying £35,000 a year. Your total income is £75,000, but your qualifying income for MTD is only £40,000. That means you’d join the second phase and need to comply from April 2027, not 2026.

What MTD Actually Means for You

So, you've figured out that Making Tax Digital applies to your business. What now? This is where the theory ends and the practical changes begin. It’s not just a new way to file your taxes; it’s a complete shift in how you manage your financial records all year round.

Think of it less as a single, stressful deadline and more as a continuous, background process. Let's break down exactly what these new rules mean for how you run your business day-to-day.

What “Digital Records” Really Means

Under MTD, the term "digital records" has a very specific meaning. It's no longer enough to just save PDFs of invoices or keep a simple spreadsheet on your computer. HMRC now requires you to use MTD-compatible software to keep track of your business transactions.

Essentially, every sale you make and every expense you incur needs to be logged electronically as you go. The crucial part is that this information must be stored in a way that allows your software to communicate directly with HMRC’s systems. Standalone files and paper ledgers just won't cut it anymore.

Finding HMRC-Recognised Software

Picking the right software is probably the most important decision you'll make to get MTD-ready. HMRC doesn't offer its own software, but it does provide a list of approved providers whose tools are fully compatible with MTD for Income Tax.

Here’s what the official government search page for recognised software looks like.

You’ll find a whole range of options on this list. There are comprehensive accounting packages like Xero, but there are also simpler "bridging" tools designed to connect your existing spreadsheets to HMRC’s platform. There really is a solution for every type of business.

Getting Used to the New Reporting Rhythm

Perhaps the biggest shake-up MTD brings is the end of the single annual Self Assessment tax return. In its place is a new, more frequent reporting cycle that breaks your tax year into quarters.

This new process has three main stages:

- Quarterly Updates: Every three months, you’ll send a summary of your business income and expenses to HMRC using your software. These aren’t tax payments; they’re just regular check-ins to keep your records up-to-date.

- End of Period Statement (EOPS): Once the tax year is over, you’ll submit an EOPS for each business you operate (for example, one for your self-employment income and another for your property rentals). This is where you’ll make final adjustments, like claiming capital allowances.

- Final Declaration: This is the final piece of the puzzle and effectively replaces your old tax return. You'll confirm that all your EOPS submissions are correct and declare any other income you have (like from savings or employment) to work out your final tax bill for the year.

This ongoing process turns tax from a once-a-year headache into a much more predictable and manageable task. It gives you a clearer, real-time picture of your estimated tax bill, making it far easier to budget and avoid any nasty surprises.

Instead of waiting until the following January to find out what you owe, your software will provide a running estimate with each quarterly update. This proactive approach is exactly what MTD is designed to achieve.

For a more detailed look at the new rules, take a look at our guide on what is required for MTD for Income Tax from April 2026. Getting to grips with this new rhythm now will make the transition smooth and keep you compliant from day one.

Key MTD Deadlines and Implementation Timeline

Getting your head around the Making Tax Digital (MTD) timeline is the first step to staying on the right side of HMRC. The rollout has been happening in stages, so it’s essential to know exactly which deadlines apply to you and when you need to act.

The MTD story started with VAT. Since April 2022, every single VAT-registered business, no matter their turnover, has been required to comply. If that’s you, you should already be keeping digital records and filing your VAT returns through MTD-compatible software. The old days of logging into the HMRC gateway to file manually are long gone.

The Staggered Rollout for Income Tax Self Assessment

With MTD for VAT now the standard, HMRC’s attention has turned to Income Tax Self Assessment (ITSA). This next phase will bring sole traders and landlords into the fold. The good news is that, unlike the single hard deadline for VAT, this rollout is staggered based on your total annual income from your business and property.

This phased approach is designed to give smaller businesses and landlords a bit more breathing room to get their digital systems in place.

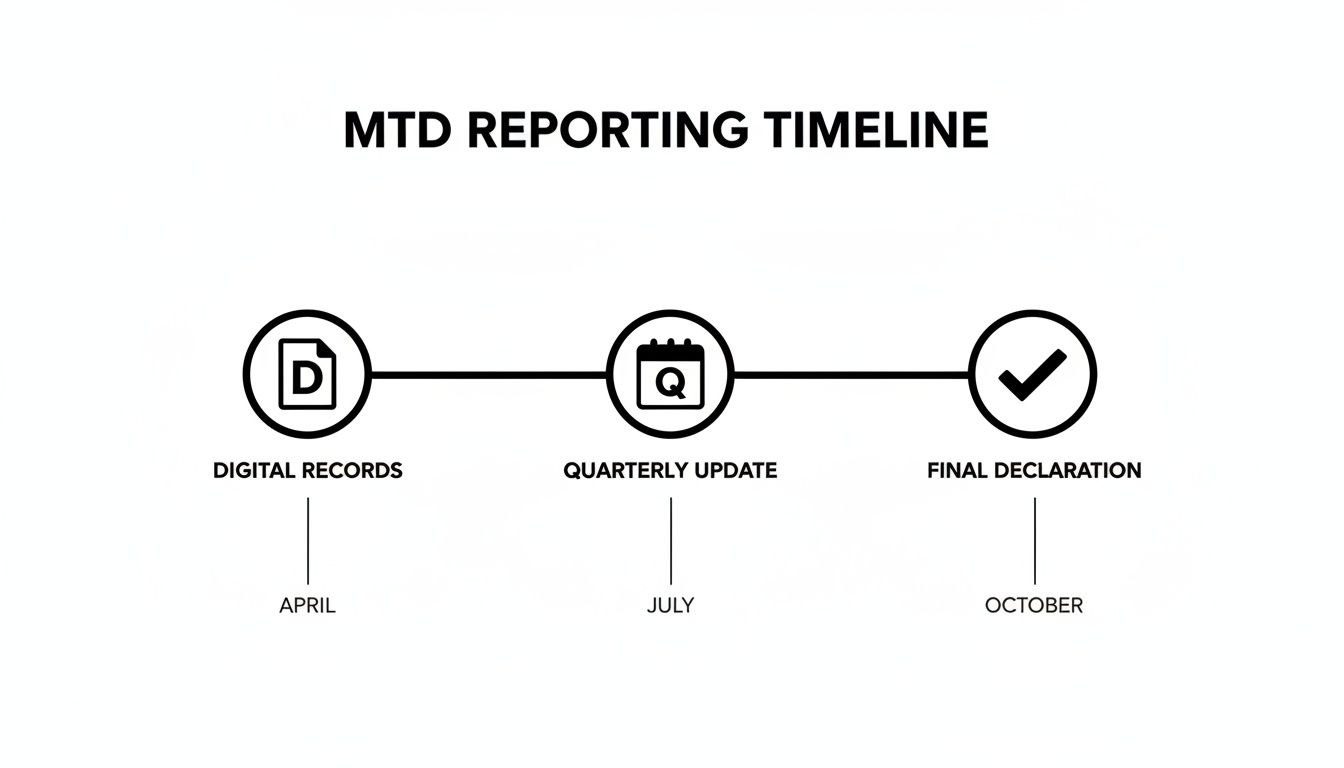

The new reporting cycle under MTD is quite different from the old annual tax return. It's a continuous process. This image below breaks down the new rhythm of keeping digital records, sending quarterly updates, and then finalising everything at the end of the year.

As you can see, it's a move away from the once-a-year scramble. The idea is to give you a clearer picture of your tax position throughout the year, not just after it ends.

Making Tax Digital Implementation Timeline

To make it easier to see where you fit in, here’s a simple table outlining the key dates and who is affected. It covers what’s already happened and what’s just around the corner.

| Effective Date | Who Is Affected | Requirement |

|---|---|---|

| April 2022 | All VAT-registered businesses | Keep digital records and file VAT returns via MTD software |

| 6 April 2026 | Sole traders and landlords with annual gross income from business/property over £50,000 | Comply with MTD for Income Tax Self Assessment (ITSA) |

| 6 April 2027 | Sole traders and landlords with annual gross income from business/property over £30,000 | Comply with MTD for Income Tax Self Assessment (ITSA) |

| To Be Confirmed | General partnerships | The original start date has been delayed with no new date set |

| To Be Confirmed | Limited companies (for Corporation Tax) | MTD for Corporation Tax is still in the early review stages |

Keeping this timeline handy will help you plan ahead and ensure you don’t get caught out by any fast-approaching deadlines.

Upcoming MTD for ITSA Deadlines

For sole traders and landlords, the next couple of years are critical. It all comes down to your 'qualifying income', which is your total gross income for the tax year before the MTD start date. For instance, HMRC will look at your figures from the 2024–25 tax year to see if you fall into the first group starting in April 2026.

Here are the dates to circle in your calendar:

- From 6 April 2026: If your total annual gross income from your business and property is over £50,000, MTD for ITSA is mandatory for you.

- From 6 April 2027: The rules expand to catch anyone with a total annual gross income from business and property over £30,000.

Remember, ‘gross income’ means your total sales or turnover before you take off any expenses. It’s the combined total from all your sole trader businesses and property rentals.

Key Takeaway: Your start date for MTD for ITSA depends on your total gross income, not your profit. You need to calculate this figure carefully to make sure you’re ready for the right deadline.

What About Partnerships and Limited Companies?

Initially, general partnerships were next in line after sole traders. However, the government has since confirmed that partnerships will not be brought into MTD for ITSA in 2027. A new start date hasn't been announced yet, so for now, they remain outside the scope.

It's a similar story for limited companies and MTD for Corporation Tax. The idea is still on the table, but it's in the early stages of review. Right now, HMRC’s focus is firmly on getting sole traders and landlords ready for the 2026 and 2027 deadlines.

The Hidden Benefits of MTD and Common Pitfalls to Avoid

Let's be honest, for many, Making Tax Digital feels like just another piece of administrative hassle. But it’s a mistake to see it purely as a compliance headache. Think of it more as a government-enforced upgrade for your business's financial engine. By nudging you towards digital systems, MTD creates a fantastic opportunity to get a much clearer grip on your finances than the old annual tax return ever could.

The biggest, most immediate win is having a real-time view of your financial health. Once every transaction is logged in your software, you’re no longer guessing how the business is doing. This clarity is a game-changer for managing cash flow, letting you see income and expenses as they happen. That means you can make smarter, more informed decisions about spending and investment on the fly.

This proactive approach also slashes the risk of costly errors. Digital software handles the calculations and cuts down on manual data entry, which is where most mistakes creep in. Having an accurate, up-to-date picture of your tax liability throughout the year means no more nasty surprises in January, which allows for much better financial planning.

The Real Wins of Going Digital

Looking beyond simply keeping HMRC happy, adopting MTD can bring some genuinely tangible improvements to your business. These benefits turn what feels like a regulatory chore into a real strategic advantage.

- Improved Accuracy and Fewer Errors: Compatible software does the maths for you and reduces manual input, massively cutting the risk of simple mistakes that could trigger an investigation or penalty.

- Better Financial Planning: With a running tally of your tax bill, you can budget far more effectively. You'll know exactly what you need to set aside for tax payments well ahead of time.

- Enhanced Productivity: Automating your record-keeping frees up countless hours previously lost to sorting receipts and wrestling with spreadsheets. That’s time you can pour back into growing your business.

- Faster Decision-Making: Live financial data lets you make quicker, more confident business decisions based on what’s happening right now, not what happened last year.

By embracing the digital shift, you're not just complying with tax law; you're building a more resilient and efficient business. The insights gained from real-time data are invaluable for spotting trends, managing expenses, and planning for future growth.

Navigating the Common MTD Challenges

Of course, the transition isn't always seamless. Being aware of the common pitfalls is the best way to sidestep them and make your MTD journey a smooth one.

The most common mistake we see is people choosing the wrong software. Some business owners just grab the cheapest option without thinking about their actual needs, only to find it’s missing key features or is far too complicated. It’s vital to pick a tool that fits your business complexity and your own comfort level with technology.

Another frequent issue is simply carrying over poor record-keeping habits. MTD software is only as good as the information you feed it. If you fall behind on logging transactions, you completely lose the benefit of the system and just create a mountain of work for yourself when a quarterly deadline looms.

Finally, many people underestimate the time it takes to adapt. Switching systems isn't an overnight job. You need to allow proper time to choose and set up your software, migrate your records, and just get used to the new digital workflow. Leaving it all to the last minute is a recipe for stress and, potentially, non-compliance. Tackling these challenges with a bit of forward planning will make all the difference.

How to Make Your MTD Transition Seamless

Knowing the rules of Making Tax Digital is one thing, but getting your business ready is another challenge altogether. The thought of switching to digital records and quarterly updates can feel pretty daunting, but I can assure you that a smooth, stress-free transition is absolutely possible with a bit of planning and the right help.

The first step is always to take a frank look at where you are right now. Are you already comfortable with accounting software, or are you still relying on spreadsheets and paper ledgers? Your starting point determines the path we'll take.

Your Action Plan for MTD Success

Switching to MTD doesn't need to be a last-minute scramble. When you break it down into simple, manageable steps, you can move forward confidently and have everything in place well before any deadlines loom. Having an expert guide you through it means no detail gets missed.

Here’s a snapshot of how we help businesses like yours make the switch:

- Assess Your Readiness: First, we’ll sit down and review your current bookkeeping system. This helps us pinpoint exactly what needs to change to get you MTD-compliant.

- Recommend and Set Up Software: We'll find the right MTD-compatible software for your business, like Xero, and handle the entire setup. We make sure it's configured perfectly for you from the get-go.

- Provide Ongoing Support: We won’t just set it up and leave you to it. Our team is here for the long haul, managing your quarterly submissions and making sure your digital records are always accurate.

Our goal is simple: to take the headache of compliance off your plate. We manage the technical bits and the deadlines, so you can pour your energy back into what you do best—running your business.

From Compliance to Strategic Insight

The real magic of MTD happens when you start to see it as more than just a box-ticking exercise. The real-time data you get from digital records is an incredibly powerful tool for making smarter business decisions. Forget looking at last year's dusty accounts; you can now get a live, up-to-the-minute picture of your company's financial health.

At Stewart Accounting Services, we turn these insights into proactive advice. We can help you spot emerging trends, get a better handle on your cash flow, and identify genuine opportunities for growth. Suddenly, MTD becomes less of a chore and more of a catalyst for building a stronger, more profitable business.

For example, tools like the smartreceipts platform can make the day-to-day record-keeping almost effortless.

We’ve helped businesses all over Central Scotland and the UK find their footing with MTD. When you partner with us, you can rest easy knowing your tax obligations are completely taken care of, freeing you up to focus on the future.

Have a Question About Making Tax Digital?

Getting to grips with the practical side of Making Tax Digital often raises a few common questions. From picking software to understanding what happens to your old tax return, the details really matter. Let’s tackle some of the most frequent queries to give you the clarity you need.

What Software Can I Use For Making Tax Digital?

HMRC doesn't actually produce its own MTD software for businesses. Instead, they’ve approved a whole list of third-party options that are built to work seamlessly with their systems. This is good news, as it means you can shop around for a tool that genuinely fits your business and your budget.

You’ve probably heard of the big names like Xero, QuickBooks, and FreeAgent—all are excellent, MTD-ready choices. The key is to match the software to your specific needs. A straightforward sole trader operation, for instance, won't require all the bells and whistles of a premium package designed for a larger, more complex company.

The right software isn't just a compliance tool; it's a way to make your life easier. An accountant can help you cut through the noise, pinpointing the features you'll actually use so you're not paying for a system that's either too basic or overly complicated.

This way, you end up with a tool that helps, not hinders, making the whole MTD process far less daunting.

Does MTD Replace My Self-Assessment Tax Return?

In a word, yes. For anyone earning income from self-employment or property, MTD for ITSA is set to replace the annual Self-Assessment tax return we've all grown used to. The once-a-year scramble to file a single, massive return is on its way out for those who fall under the new rules.

The new system works to a different beat. You'll send quarterly updates of your income and expenses throughout the year. At the end of it all, you'll submit an End of Period Statement and wrap everything up with a Final Declaration. This last step is what locks in your business's tax position for the year.

But here’s a crucial point: your Final Declaration isn't just for your business income. You still need to include any other sources of income you have. This means things like:

- Salary from a PAYE job

- Interest from your savings accounts

- Dividends from any investments

So, while the process is changing dramatically, the fundamental requirement to declare all your taxable income hasn't gone away. It’s all just managed through your MTD software now.

What Are The Penalties For Missing An MTD Deadline?

HMRC is shifting its approach here, moving away from the old, rigid system of automatic £100 fines for any late submission. For MTD, they're bringing in a new points-based penalty system. The idea is to be a bit more forgiving for a one-off, genuine mistake while still coming down on those who repeatedly miss their deadlines.

It’s a bit like a driving licence. Every time you miss a submission deadline—whether it’s a quarterly update or the Final Declaration—you get one penalty point. There's no immediate fine. Instead, these points add up.

Only when you hit a certain number of points does a financial penalty kick in. This system is really designed to catch persistent non-compliance, not a single slip-up. For quarterly MTD submissions, that penalty threshold is four points.

The best way to steer clear of penalties is simply to stay organised. Honestly, having an accountant in your corner is the surest way to make sure every deadline is hit, your records are spot on, and you never have to worry about penalty points stacking up.

Feeling a bit overwhelmed by the switch to MTD? Don't be. Stewart Accounting Services is here to guide you through it all. From picking the right software to handling your quarterly updates, we can give you the peace of mind that everything is taken care of.

Find out how we can support your business at Stewart Accounting Services.