If you’ve ever wondered what a P11D is, you're not alone. In simple terms, it's the form UK employers use to tell HMRC about any ‘benefits in kind’ given to employees. These are the perks and expenses that aren't part of their regular salary but still hold a taxable value.

Think of it this way: their monthly salary goes through the normal payroll (PAYE) system. The P11D is like a separate, annual report detailing everything else – from a company car to private health insurance.

Understanding The P11D Form And Its Purpose

The core job of a P11D is to put a cash value on these non-cash perks so HMRC can see what's what. This is vital because it directly affects how much tax everyone pays.

By declaring the value of these benefits, you achieve two key things: HMRC can calculate the right amount of Income Tax for the employee to pay on them, and it determines the correct Class 1A National Insurance Contributions (NICs) your business owes.

To give you a snapshot of what's involved, here's a quick summary of the key information.

P11D at a Glance Key Information

| Component | Description |

|---|---|

| What it is | A tax form detailing non-salary benefits for employees and directors. |

| Who submits it | The employer, to HMRC. |

| Purpose | To report the cash equivalent value of 'benefits in kind'. |

| Impact on Employee | Determines the amount of Income Tax due on the benefits received. |

| Impact on Employer | Used to calculate the Class 1A National Insurance contributions owed. |

| Key Deadline | Must be filed with HMRC by 6th July following the end of the tax year. |

This table covers the basics, but it's important to understand the full picture, including the forms that go with it.

The P11D and Its Companion Form

The P11D form is just one piece of the puzzle. It’s always filed alongside its partner form, the P11D(b).

While the P11D breaks down the benefits for each individual employee, the P11D(b) is the employer’s summary. It totals up all the benefits provided across the entire company and is used to calculate the overall Class 1A National Insurance bill the business needs to pay.

You must submit a P11D for each director or employee who received benefits in kind during the tax year. This ensures complete transparency and compliance, preventing potential issues down the line.

Getting this right is a standard part of running a business in the UK. In fact, an estimated 5 million P11D forms are submitted to HMRC every year, so it's a very common process.

Accurately reporting these benefits ensures your employees aren’t over or under-taxed and that your business meets its obligations. It’s just as important as understanding other key payroll documents, which you can learn more about in our guide to P45s, P11Ds, and P60s.

Who Files a P11D? The Buck Stops with the Employer

When it comes to P11Ds, there’s no grey area: the responsibility falls squarely on you, the employer. If your company provides any 'benefits in kind' or covers certain expenses for your employees or directors, it's your legal obligation to report them to HMRC.

This isn't just administrative fluff; it's a mandatory part of running a compliant UK business. You'll need to fill out a separate P11D form for every single director or employee who received these perks during the tax year, from the CEO right down to the newest team member.

Why It's a Business Obligation

So, why does HMRC insist on this? It’s all about transparency and making sure the tax system works correctly. The details you report on a P11D allow HMRC to figure out two very important things:

- The employee's tax bill: HMRC uses the P11D information to tweak an employee's tax code. This ensures they pay the right amount of Income Tax on the total value of their remuneration package, not just their salary.

- The employer's National Insurance: All the benefits you report are tallied up on a summary form called a P11D(b). This total figure is then used to calculate your company's Class 1A National Insurance contributions for the year.

Think of it this way: a P11D helps you paint the complete picture of what an employee earns, beyond just the cash that hits their bank account. It’s a critical piece of the puzzle that keeps the tax system fair for everyone.

Common Scenarios That Mean You Need to File

What kind of things actually trigger the need to file a P11D? It’s usually the extra perks and benefits you offer to attract and look after your team.

For instance, did you provide a company gym membership to boost well-being? That needs to be on a P11D. Helped an employee relocate and covered expenses over the £8,000 tax-free allowance? That’s reportable too. Other common examples include providing private medical insurance or giving an interest-free loan that goes over £10,000.

Getting your head around P11D obligations is more than just a box-ticking exercise to avoid fines. It's a cornerstone of good financial governance, showing that your business is operating transparently and correctly under UK tax law.

By identifying and reporting these benefits properly, you prevent nasty surprises for both your company and your team when the tax calculations are done. It's a vital step in building trust and maintaining a healthy financial standing with everyone involved.

Identifying Common Taxable Benefits and Expenses

This is where things can get a bit tricky for business owners. Knowing exactly what needs to go on a P11D isn’t always obvious. It’s not just about big-ticket items; plenty of smaller perks can be classed as a taxable ‘benefit in kind’.

The best way to think about it is this: have you provided something to an employee or director that gives them a personal benefit outside of their normal salary? If the answer is yes, you probably need to report it. This could be anything from a company vehicle to a gym membership.

Let’s walk through the most common examples you're likely to come across.

Company Cars and Private Fuel

The company car is a classic—and one of the most complex—benefits. If you provide a car to an employee and they can use it for personal trips, it has to be reported. That includes their daily commute to and from work.

Figuring out its taxable value isn't as simple as just looking at the car's price tag. HMRC uses a specific formula that considers the car's list price, its CO2 emissions, and its fuel type. As a rule of thumb, cars with higher emissions attract a higher taxable value.

And if you also cover the cost of fuel for their private journeys? That’s a separate benefit entirely, with its own calculation that also needs reporting on the P11D.

Because the rules are so detailed, it's a good idea to get some guidance here. You can dive deeper into this topic in our guide on the taxable benefits for the use of a company car.

Private Medical Insurance

Offering private medical or dental insurance is a fantastic perk for employees, but it's also a very common taxable benefit. For P11D purposes, the value you report is simply the cost of the insurance premium you paid on behalf of your employee.

This is an incredibly popular benefit. In fact, back in the 2016-17 tax year, 65% of employees who received benefits had private medical or dental cover. That made it the most frequent perk by a long shot, with company cars trailing at 26%. It just goes to show how central it is to many UK benefits packages. You can explore more of these UK taxable benefits statistics on GOV.UK.

Loans and Living Accommodation

A couple of other significant benefits that need careful handling are beneficial loans and company-provided accommodation.

- Beneficial Loans: If you give an employee or director a loan that's interest-free or has a very low interest rate, it becomes a taxable benefit. This kicks in if the total loan amount tops £10,000 at any point during the tax year. The taxable value is worked out from the difference between the interest they actually paid (if any) and what they would have paid at HMRC's official rate.

- Living Accommodation: Providing an employee with a place to live is also a reportable benefit. The calculation here can get complicated, as it often depends on the property's value and any rent the employee contributes.

The core principle is simple: if a perk provides a personal, monetary advantage to an employee that isn't part of their salary, it likely needs to be valued and reported on a P11D form.

Getting a handle on these common benefits is the first major step. But what adds to the confusion is that some perks are completely exempt.

To help clear things up, the table below gives a quick comparison of common benefits you must report versus those that are generally exempt.

Examples of Taxable Benefits vs Exemptions

This table offers a quick at-a-glance guide to help you distinguish between what needs reporting and what doesn't.

| Must Be Reported on P11D | Generally Exempt (No P11D Needed) |

|---|---|

| Company cars available for private use | Employer pension contributions |

| Private medical and dental insurance | One employer-provided mobile phone |

| Low-interest loans over £10,000 | Work-related training courses |

| Gym memberships | Uniforms required for the job |

| Relocation costs above the £8,000 limit | Business travel expenses within HMRC rates |

Remember, this is just a starting point. If you’re ever unsure about a specific benefit, it’s always best to check the official guidance or ask an expert.

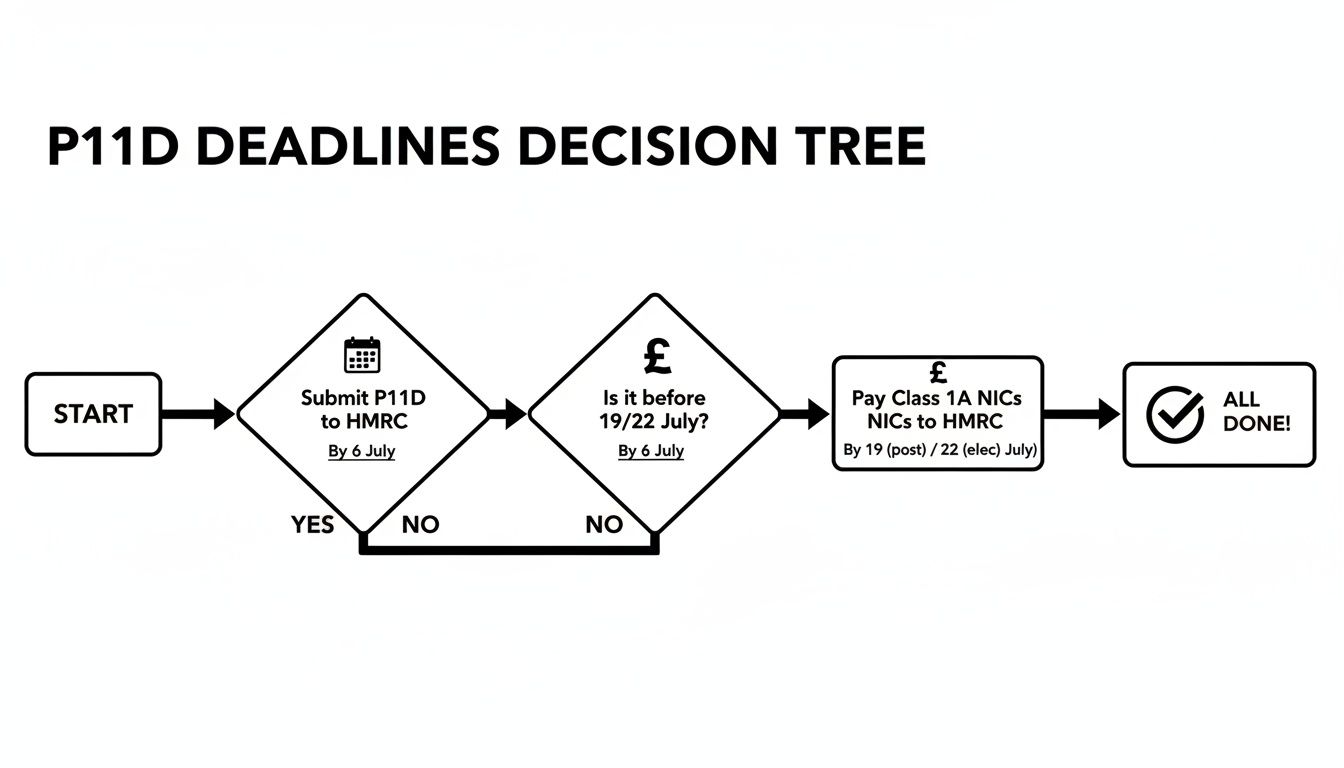

Navigating P11D Deadlines and Avoiding Penalties

When it comes to P11D forms, timing really is everything. Missing a deadline isn't just a minor administrative slip-up; it can trigger immediate and costly penalties from HMRC. The first step to staying compliant and keeping your money in your business is to get these key dates locked into your calendar.

The UK tax year runs from 6th April to 5th April. As soon as one tax year ends, the clock starts ticking on getting your P11D affairs in order for the year that's just closed. There are a few critical dates you simply can't afford to miss.

Key Submission and Payment Dates

The timeline is firm, and HMRC isn't known for its flexibility. It pays to be prepared well in advance.

- 6th July: This is the hard deadline. Your P11D and P11D(b) forms must be with HMRC by this date. Crucially, you also need to have given a copy of the P11D to each relevant employee.

- 19th July: If you’re paying your Class 1A National Insurance by cheque through the post, the payment must arrive at HMRC by this date.

- 22nd July: For most businesses paying electronically, this is the final day for the payment to clear in HMRC’s bank account.

Keeping on top of these dates is vital. To see how they fit into the broader financial landscape, take a look at our UK tax diary for July and August.

The Consequences of Missing Deadlines

Let’s be clear: HMRC enforces these deadlines strictly, and the penalties for being late can stack up surprisingly fast. If your P11D(b) form misses that 6th July deadline, your company is hit with an automatic fine.

The penalty starts at £100 per month (or even part of a month) for every 50 employees who should have had a P11D filed for them. A delay of just a few days will land you in that first penalty bracket.

On top of that, if you're late paying your Class 1A NICs, you'll be charged interest. This is calculated daily from the due date until the moment you pay it off in full. For serious delays or deliberately incorrect returns, HMRC can issue even more substantial penalties based on the tax you owe.

The best way to avoid these pitfalls is to be proactive. Don't wait until June to start pulling everything together. Keep meticulous records of all benefits and expenses throughout the year. Modern payroll software can be a lifesaver here, automating many of the calculations and sending reminders, which dramatically cuts the risk of error. A little bit of planning goes a long way, letting you handle your P11D duties with confidence so you can get back to running your business.

Smarter Alternatives to Annual P11D Reporting

While the yearly P11D form is the traditional route for reporting employee benefits, it’s certainly not the only one. For many businesses, that annual scramble to pull together all the data and file the forms on time feels like a huge administrative headache.

The good news is that HMRC provides a couple of much more efficient alternatives. These methods let you build benefits reporting right into your normal payroll cycle, which cuts down the year-end workload and spreads out the tax impact for your employees. Let's look at how you can pick a strategy that fits your business and makes compliance a whole lot simpler.

Option 1: Payrolling Benefits

One of the most popular and practical alternatives is payrolling benefits in kind. Think of it this way: instead of letting all the tax on benefits build up for a single P11D form in July, you handle it through your regular payroll each month. The tax is dealt with in real-time, exactly like it is for their salary.

To get started, you need to register with HMRC online before the start of the tax year you want to do it for. Once you’re registered, you just calculate the cash equivalent of an employee’s benefits, add that figure to their monthly pay, and the tax is automatically deducted through PAYE.

This approach has some clear advantages:

- No P11D Form: For any benefits you payroll, you can forget about filling out a P11D form. That’s a major bit of admin gone.

- Smoother Tax for Employees: Your staff pay tax on their benefits bit by bit throughout the year, so they avoid a sudden, and often unwelcome, change to their tax code.

- Better Cash Flow Management: Everyone gets a much clearer picture of monthly tax liabilities, which helps both the business and your employees with budgeting.

By payrolling benefits, you’re essentially trading a once-a-year reporting marathon for a much more manageable monthly jog. It brings clarity for your team and seriously reduces the stress of P11D season.

Option 2: PAYE Settlement Agreements

Another incredibly useful tool is the PAYE Settlement Agreement (PSA). A PSA is a formal arrangement where you, the employer, agree to settle the tax and National Insurance bill on behalf of your employees for certain benefits.

This is a lifesaver for benefits that are minor, happen irregularly, or are just impractical to divide up between individual employees. Classic examples include a staff Christmas party that goes over the tax-free limit, or a small gift that doesn’t quite meet the criteria for a trivial benefit.

With a PSA, you make one annual payment to HMRC that covers all the tax and NICs due on these items. It simplifies things enormously because you don't have to put these specific perks on P11D forms or run them through payroll. It's the perfect way to handle those smaller, ad-hoc benefits without drowning in paperwork for every individual.

This flowchart shows the traditional deadlines that you can often simplify or avoid altogether with these alternatives.

By adopting payrolling or a PSA, you can neatly sidestep this annual rush for many of your company's perks.

A Practical Checklist for P11D Compliance

Getting your head around the what and why of the P11D process is the first step. The real challenge, though, is putting it all into practice. To help you move from theory to action, here’s a straightforward checklist to guide you through your annual compliance duties confidently.

Think of this as your roadmap to a stress-free filing season. By following these steps, you can make sure nothing falls through the cracks, protecting your business from common mistakes and the penalties HMRC can issue. Let’s break down what you actually need to do.

Your Step-by-Step P11D Action Plan

One thing to remember is that this isn't a last-minute dash to the finish line. Good P11D management is a year-round activity. The secret to success is staying organised right from the start of the tax year on 6th April.

1. Gather Your Data Systematically

Throughout the year, keep a careful record of every single expense and benefit provided to each employee and director. This means everything from the big-ticket items like company car details and private medical insurance premiums down to the smaller perks that might be taxable. Please, don't wait until May to start digging through a year's worth of receipts!

2. Calculate the 'Cash Equivalent'

For each benefit you’ve provided, you need to work out its taxable value. In HMRC terms, this is known as the ‘cash equivalent’. Some of these are easy to figure out (like a gym membership premium), but others are more complex. Company cars, for instance, require a specific HMRC formula based on CO2 emissions and the car's list price.

Getting the cash equivalent right is absolutely the most critical part of this process. An incorrect valuation leads to the wrong amount of tax being paid by your employee and incorrect National Insurance contributions from your business.

3. Complete the P11D and P11D(b) Forms

You’ll need to fill out a separate P11D form for each employee who received benefits, detailing exactly what they got. Alongside that, you must complete one P11D(b) form. This summarises the total value of all benefits across your entire company and is used to calculate the Class 1A National Insurance your business owes.

4. Submit and Distribute on Time

Finally, it all comes down to the deadlines. You must:

- Submit the completed P11D and P11D(b) forms to HMRC by 6th July.

- Give each employee a copy of their individual P11D form, also by 6th July.

Modern payroll software, like Xero, can take a lot of the headache out of this. It can help track benefits, calculate the values, and even file the forms directly with HMRC. Using these tools is a brilliant way to reduce manual work and minimise the risk of costly mistakes, freeing you up to focus on what you do best – running your business.

Your P11D Questions Answered

Let's tackle some of the most common questions that pop up when business owners are getting to grips with P11D forms.

What if I Didn't Give Any Benefits This Year? Do I Still Need to File?

Good news – if your company didn't provide any benefits in kind during the tax year, you don't have to fill out individual P11D forms for your team.

However, and this is a crucial point, you can't just do nothing. You must let HMRC know that you have nothing to declare, especially if you've filed P11Ds in the past. You can easily do this using HMRC's online services, which stops them from automatically issuing a penalty notice because they were expecting a submission from you.

I've Spotted a Mistake on a P11D I Already Sent. What Should I Do?

It happens to the best of us. The key is to correct it as soon as you realise. If you filed electronically, most payroll software will let you submit an amended version directly to HMRC.

If you went the old-school paper route, you'll need to send in a new, corrected P11D. Just make sure you clearly write 'Amendment' on the top so HMRC knows what it is.

Acting fast to fix mistakes is always the best policy. It shows you're taking your responsibilities seriously and that it was a genuine error, not an attempt to pull the wool over anyone's eyes. This can make a real difference in avoiding or minimising penalties.

Can I Just File My P11Ds Myself?

Absolutely. You can manage the P11D process yourself through HMRC's PAYE Online service or with compliant software. It's perfectly doable.

The catch is that some benefits, like company cars or living accommodation, have notoriously tricky calculations. A small slip-up can easily lead to the wrong amount of tax being paid, which could land you with a fine down the line.

Getting P11Ds right can feel like a bit of a minefield. The team at Stewart Accounting Services handles this for businesses day in and day out. We can take the entire process off your plate, giving you peace of mind that everything is accurate and on time.

Find out how we can help by visiting stewartaccounting.co.uk.