Getting your head around when your VAT is due is one of the most important parts of managing your business's cash flow and, of course, staying on the right side of HMRC. For most businesses filing their quarterly returns online, the key date to remember is one calendar month and seven days after the end of your VAT period.

Let's break down exactly what that means for you.

Your Guide to UK VAT Return and Payment Deadlines

Running a business in the UK means getting to grips with Value Added Tax (VAT). Missing a deadline isn't just a headache; it can hit you with penalties and cause a lot of needless stress. Getting your dates sorted is absolutely crucial.

Before we jump into the specific deadlines, it's worth making sure you fully understand your core VAT responsibilities. If you need a refresher, this is a great resource on the pros and cons of registering for VAT in the UK.

This guide will walk you through everything you need to know about your VAT return and payment schedule. To make things as simple as possible, the table below gives you a clear, at-a-glance view of the standard deadlines.

Standard UK VAT Return and Payment Deadlines

Here’s a straightforward summary of the standard VAT accounting periods and their online filing and payment deadlines. Think of this as your quick reference guide for staying on track each quarter.

For a deeper dive with more specific examples, you can also check out our detailed guide here: https://stewartaccounting.co.uk/vat-return-due-dates/

Here's how the most common VAT quarters and deadlines line up.

Standard UK VAT Return and Payment Deadlines

| VAT Period End Date | Online Return and Payment Deadline | Payment Method |

|---|---|---|

| 31 March | 7 May | Online / Direct Debit |

| 30 June | 7 August | Online / Direct Debit |

| 30 September | 7 November | Online / Direct Debit |

| 31 December | 7 February | Online / Direct Debit |

As you can see, the "one month and seven days" rule applies consistently, giving you a predictable rhythm for your financial planning.

How to Find Your VAT Accounting Period

Before you can figure out when your VAT is due, you need to know your specific VAT accounting period. Think of it as your business's financial chapter for tax purposes—it's the set timeframe HMRC looks at to see how much VAT you've collected and paid.

When you first register for VAT, HMRC assigns you one of these periods. For the vast majority of businesses, this is a standard three-month cycle, often just called a VAT quarter. This default schedule is really the backbone of the UK’s VAT system.

You're in good company with a quarterly return. Around 95% of all VAT payments in the UK are made this way. It's the standard rhythm for most businesses, with only a small number filing monthly. If you're curious, you can dig into more UK VAT return trends on the ONS website.

Checking Your VAT Period

So, how do you find your dates? The quickest and easiest way is to log into your VAT online account through the Government Gateway. Your dashboard will spell out the start and end dates for your current and upcoming VAT periods. No guesswork needed.

Another place to look is your VAT registration certificate—the document HMRC sent you when you first signed up. It has all your key details, including your accounting period, so it’s a good idea to keep it somewhere safe.

Key Takeaway: Your VAT online account is the most up-to-date and reliable source for your accounting period dates. These dates are the starting block for working out your VAT deadline.

Understanding the Staggered System

One thing that often surprises people is that not every business has the same quarterly dates. To avoid a massive pile-up of paperwork all at once, HMRC cleverly staggers the deadlines throughout the year. Your business will be assigned to one of three main groups:

- Group 1: Quarters ending in March, June, September, and December.

- Group 2: Quarters ending in April, July, October, and January.

- Group 3: Quarters ending in May, August, November, and February.

This staggered approach keeps the system running smoothly. The group you're in dictates the exact rhythm of your VAT calendar.

While it’s far less common, some businesses can apply to HMRC to file monthly or even annually, usually because it better suits their trading patterns or cash flow. But for most, it’s all about the quarterly cycle.

How to Calculate Your VAT Return Deadline

Once you know your VAT accounting period, working out your exact filing deadline is a simple, repeatable process. For nearly all quarterly online filers, there’s one golden rule to remember: the ‘one month and seven days’ rule.

So, what does that actually mean? It’s straightforward: your VAT return and payment are due one full calendar month plus an extra seven days after your accounting period finishes. This handy formula takes the guesswork out of the process, giving you a firm date to work towards each quarter.

The Core Rule: Your VAT return must be submitted and the payment must be in HMRC’s bank account by the 7th day of the second month after your VAT period ends.

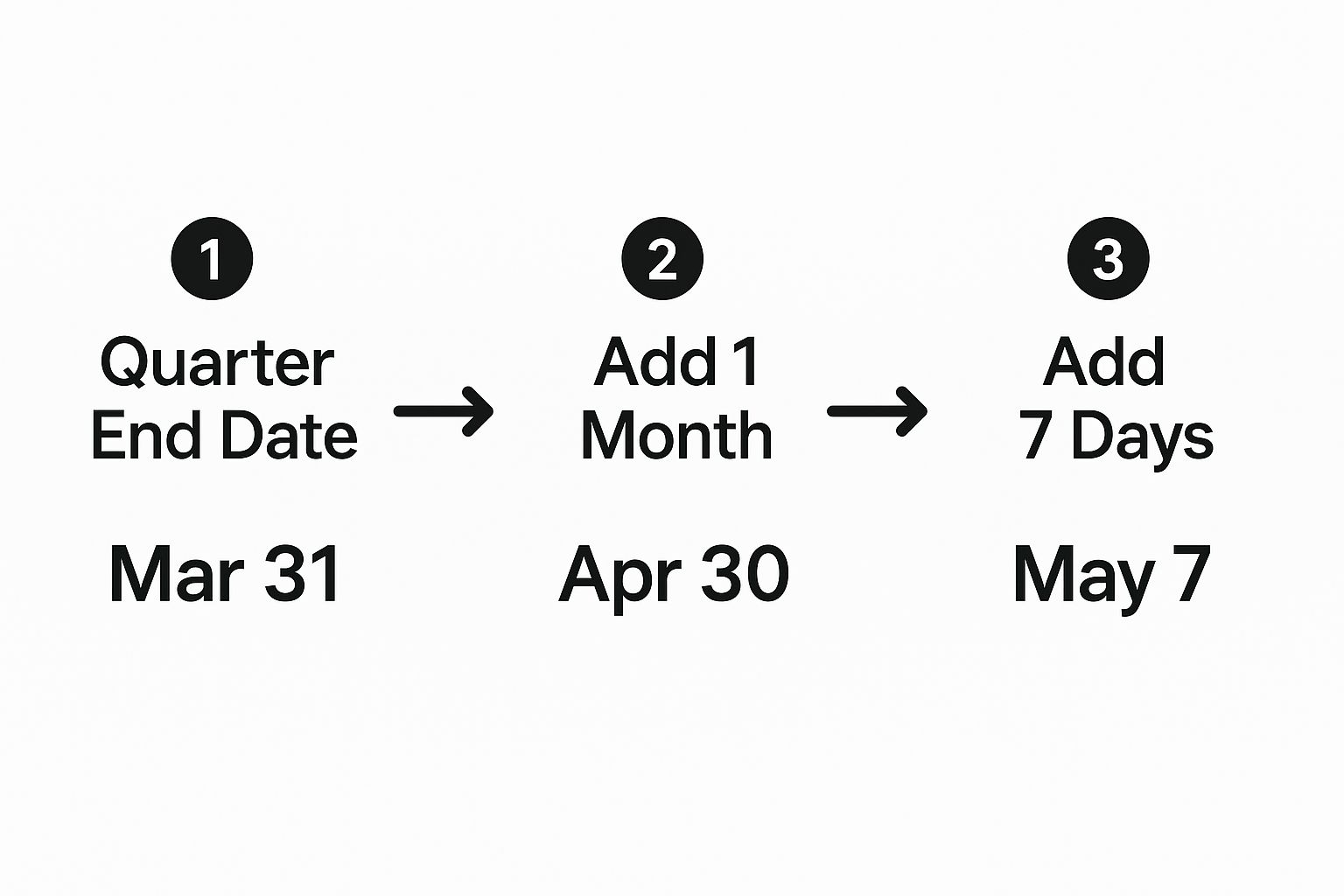

A Quick Example Calculation

Let’s say your business has a VAT quarter that ends on 31 March. How do you figure out when your VAT is due?

- Start with your period end date: 31 March.

- Add one full calendar month: That takes you to 30 April.

- Now, add seven days: This lands you on your final deadline of 7 May.

And that's all there is to it. This method works for any quarterly period, giving you a reliable way to map out your deadlines well in advance. The visual guide below breaks it down even further.

This fixed schedule from HMRC is designed to create a predictable rhythm for businesses. These aren't just arbitrary dates; they’re financially significant. With the standard UK VAT rate sitting at 20% for most goods and services, these quarterly payments can have a major impact on your company's cash flow.

Sticking to this rhythm isn't just about compliance – it's fundamental to smart financial management. As explained in this guide on how business payment deadlines impact financial planning on cashflowfrog.com, getting these dates right is crucial for keeping your finances healthy.

How Your Payment Method Affects VAT Deadlines

While the deadline for filing your VAT return is set in stone, the way you choose to pay HMRC can actually buy you a little extra time. It’s a small detail, but one that’s crucial for steering clear of late payment penalties.

The standard deadline of one month and seven days means your payment must have cleared into HMRC’s bank account by that date—not just been sent from yours. This is a common tripwire for many business owners.

For businesses keeping a close eye on cash flow, choosing the right payment method means you can hold onto your money for as long as possible. This is especially useful for those using the VAT Cash Accounting Scheme to manage their finances.

Comparing Your Payment Options

The method you pick directly affects how far in advance you need to make the payment. For instance, Faster Payments usually clear on the same day, but it’s not guaranteed. A Bacs payment, on the other hand, can take up to three working days to land.

Expert Tip: Setting up a Direct Debit is a great way to get a bit of an extension. You still need to file your return by the standard deadline, but HMRC will typically collect the payment around three working days later. This only applies to the payment, not the filing.

To make things clearer, let’s look at how much time you should allow for each method to ensure your payment arrives on time, every time.

VAT Payment Deadlines by Method

The table below breaks down the most common payment methods and their typical clearing times, helping you plan ahead and avoid any last-minute panic.

| Payment Method | Time to Allow for Payment | Effective Deadline |

|---|---|---|

| Faster Payments | Same or next day (check with your bank) | Standard deadline |

| Bacs | 3 working days | 3 working days before the standard deadline |

| Direct Debit | Mandate must be set up in advance | Payment taken automatically ~3 days after deadline |

Ultimately, choosing a payment method that suits your internal processes is key. Just be sure to factor in these clearing times to guarantee you're always compliant with HMRC's deadlines.

A Closer Look at the Payment on Account Scheme

For most businesses, the standard quarterly VAT rhythm is pretty straightforward. But what happens when your VAT bill gets really big? That’s where HMRC’s Payment on Account (PoA) scheme comes into play, designed to help manage cash flow for larger businesses.

Think of it like making tax 'down payments' throughout your quarter. Instead of facing one huge bill at the end, you pay in instalments. This helps both your business and HMRC avoid nasty surprises and keeps finances on a more even keel.

How Does the PoA Scheme Work?

If your annual VAT liability tips over the £2 million mark, you'll almost certainly be moved onto the PoA scheme.

The core idea is simple: you make two advance payments during your VAT quarter, which are essentially estimates of your final bill. These are followed by a final, balancing payment once you've submitted your actual return. It’s a major timing shift for bigger companies and accounts for a huge chunk of all UK VAT payments, as you can see from quarterly statistics published by the UK government.

The Bottom Line: With Payment on Account, you make two interim payments during your VAT quarter, then a final balancing payment when you file your return.

The payment deadlines are strict. Your first instalment is due by the last working day of the second month of your quarter. The second is due by the last working day of the third month.

Then, when your quarter officially ends, you file your VAT return as normal. The deadline is the same as for everyone else—one month and seven days after the period ends. This is when you'll either pay the remaining balance or claim back a refund if you overpaid with your instalments.

What Happens If You Miss a VAT Deadline?

Getting your head around when VAT is due is one thing, but understanding the real-world consequences of a late return is what really motivates you to stay on top of it. Missing a deadline isn't just a small admin error; it kick-starts an automatic penalty process with HMRC that can get expensive, fast.

For any late submissions, HMRC now operates on a penalty point system. It’s a bit like getting points on your driving licence – each deadline you miss adds another point to your company's record. Once you hit a certain points threshold, you’ll be hit with a financial penalty. The principle of avoiding costly fees for late filing is universal, and you can see a similar approach with these IRS penalties for late tax filing.

Late Payments and Interest

Missing the payment deadline is treated as a completely separate issue, and it comes with its own set of financial penalties. These are calculated based on a percentage of the VAT you owe, and that percentage climbs the longer the bill goes unpaid.

To make matters worse, HMRC also charges daily interest on the overdue amount, starting from the day after it was due right up until you’ve paid it in full.

Key Takeaway: HMRC penalises late filing (the points system) and late payment (financial charges plus interest) separately. A single slip-up can result in multiple charges, so staying compliant is a crucial part of managing your business’s finances.

If you know you’re going to struggle to meet a deadline, the best thing you can do is be proactive. We break down the new points system in more detail in our guide to understanding VAT late filing penalties. It’s often possible to set up a 'Time to Pay' arrangement with HMRC, but you have to get in touch with them before the deadline arrives.

A Few Lingering Questions About VAT Deadlines

Getting your head around the standard VAT rules is one thing, but real-world scenarios often throw up a few tricky questions. Let's tackle some of the most common queries business owners have when it comes to hitting those all-important VAT deadlines.

What Happens If My Deadline Is on a Weekend?

This is a classic "gotcha" for many businesses. If your VAT payment deadline lands on a weekend or a bank holiday, you can't just pay on the next working day. HMRC needs to have the funds cleared in their account on the last working day before the deadline.

Because bank transfers don't always go through instantly on non-working days, you need to plan ahead to avoid a late payment penalty.

Can I Change My VAT Return Period?

Yes, you absolutely can. Many businesses ask to change their VAT accounting cycle to line up neatly with their own financial year, which makes a lot of sense for bookkeeping. You can pop a request through your VAT online account.

Important: Don't jump the gun! You must keep filing and paying based on your old schedule until you get official, written confirmation from HMRC that the change has been approved.

When Is My Very First VAT Return Due?

Your first VAT return is usually a bit different from the rest. It won't always be a perfect three-month period. Instead, it typically covers the time from your official date of VAT registration to the end of your first assigned quarter.

For example, say you register on 15 May and HMRC puts you on a cycle ending in June. Your first return would cover the shorter period from 15 May to 30 June. HMRC will always confirm these specific dates for you in writing, so keep an eye out for that letter.

Trying to keep on top of VAT deadlines and rules can feel like a full-time job in itself. The team at Stewart Accounting Services lives and breathes this stuff, managing every aspect of VAT for businesses just like yours. We give you back your time, help you keep more of your money, and provide some much-needed peace of mind.

Find out how we can help over at https://stewartaccounting.co.uk.