Improving your business cash flow comes down to three things: getting paid faster, controlling your spending, and always knowing what’s coming around the corner financially. It often starts with simple, practical steps. Tighten up your invoicing, be systematic about chasing late payers, and take a hard look at every single non-essential cost. For most SMEs in the UK, this hands-on approach is the secret to freeing up cash that's rightfully yours and building a more stable business.

Why Cash Flow Is the Lifeblood of Your SME

It’s a classic, and deeply frustrating, scenario for business owners. Your profit and loss statement looks fantastic, painting a picture of success. But when you check your bank balance, the story is completely different—and frankly, a bit scary. This gulf between the profit you’ve earned and the cash you actually have is where so many good businesses get into trouble.

Profit is an accounting measure, a long-term indicator. Cash, on the other hand, is the fuel in your engine right now. It's what you need to operate day-to-day.

Without actual cash in the bank, you can’t pay your suppliers, run payroll, or jump on a great growth opportunity when it appears. It doesn't matter how profitable you are on paper. This is why getting a grip on your cash flow isn't just a job for your accountant; it's a fundamental survival skill for any business owner.

The Profit vs Cash Misconception

So many entrepreneurs fall into the trap of thinking profit equals cash. Let's break it down with a real-world example.

Say you run a construction firm and you finish a £50,000 project in March. You book that as revenue, and after taking out your costs, you might show a healthy £15,000 profit for the month. Great! But the client is on 60-day payment terms, which means you won't see a penny of that cash until May.

In the meantime, you still have very real bills to pay:

- Your team’s wages at the end of March.

- The materials you bought on 30-day terms back in February.

- Your quarterly VAT bill that’s due in April.

This timing gap is the absolute heart of most cash flow issues. You have a profitable business, but it's cash-poor, which creates a huge amount of stress and risk. Keeping your financial documents up-to-date is the only way to get a clear view of these movements. For a deeper dive, check out our guide on how to prepare a cash flow statement.

Why It Matters More Than Ever

In today's economic climate, you can't afford to be passive about cash flow. Think about running an SME right here in Central Scotland—as many of our clients do in Alloa, Stirling, and Falkirk. Recent figures show that a staggering 57% of UK SMEs are preparing for a massive jump in operating costs this quarter. And 64% of them are seriously worried about how it will impact their business.

Late payments, rising supplier prices, and unexpected bills can hamstring even the strongest companies.

The good news? We’ve seen firsthand that businesses who make cash flow forecasting a priority see their liquidity improve by as much as 30%. This isn't just about getting through a tough patch. It's about building a resilient company that has the financial breathing room to grow and thrive.

Speed Up Your Sales to Cash Cycle

The gap between finishing a job and seeing the money land in your bank account is often where a business feels the most financial strain. If you want to improve your cash flow, shortening this sales-to-cash cycle is the most powerful lever you can pull. This isn't about being pushy; it's about being professional, clear, and consistent.

For countless UK SMEs, cash flow problems are a silent but constant threat. A recent report revealed that 22% of them name it as their biggest challenge. With over 5.45 million small businesses forming the backbone of the UK economy, that statistic is a serious warning sign. Slow payers can squeeze your margins and grind your operations to a halt.

But here’s the good news: the same data shows that businesses who get a grip on their receivables can boost their cash inflows by 20-40%. You can dig into more findings on the UK small business finance markets on the British Business Bank's website.

Optimise Your Invoicing Process

Think of your invoice as more than just a bill—it's a critical piece of communication. A vague or confusing invoice is basically an open invitation for a payment delay. Every single one you send out needs to be crystal clear.

At a minimum, make sure your invoices include:

- A unique invoice number for easy tracking.

- Your full business and contact details.

- A clear, itemised description of the goods or services.

- An explicit due date. Don't just write "Payment due in 30 days." A specific date like "Payment due by 15 July 2024" leaves no room for doubt.

Most importantly, send the invoice the moment the work is done or the product is delivered. Putting it off directly stretches your payment cycle and puts a needless strain on your cash reserves.

Make It Effortless for Clients to Pay You

The easier you make it for customers to pay, the faster the money will hit your account. If you’re still just offering a bank transfer option, you’re missing a huge opportunity. Modern payment gateways are incredibly simple to set up and can slash payment times.

Look at integrating options like GoCardless for direct debits or Stripe for card payments. Cloud accounting software like Xero makes this a breeze. Adding a "Pay Now" button to your digital invoice lets a client settle up in a few clicks, instead of having to manually log into their banking app and type in your details.

Think of it this way: every manual step a client has to take to pay you is another opportunity for them to get distracted and delay. Removing friction is key.

Put Your Credit Control on Autopilot

Let’s be honest, nobody enjoys chasing late payments. It’s awkward, uncomfortable, and takes up time you don’t have. This is where automation becomes your secret weapon.

Modern accounting software lets you create a series of polite but firm reminders that get sent out automatically once an invoice goes overdue. This system handles the initial chasing for you, so you can focus on what you do best. If you're unsure where to start, check out our guide on how to automate invoice reminders using accounting software.

This isn't just about efficiency. It creates a systematic process that ensures no overdue invoice gets missed, all while maintaining a professional tone that protects your client relationships.

For those trickier situations, having a clear, structured follow-up plan is vital. Here’s a timeline I often recommend to clients to keep things moving without burning bridges.

Effective Invoice Collection Timeline

| Timeline | Action to Take | Communication Method |

|---|---|---|

| Day 1 Overdue | Gentle Reminder | Automated email: "Just a friendly reminder…" |

| Day 7 Overdue | Firm Reminder | Automated email: "Invoice [Number] is now 7 days overdue." |

| Day 14 Overdue | Personal Follow-Up | Phone call: "Hi, just calling to check on invoice…" |

| Day 21 Overdue | Final Notice | Email: "Final notice before further action." |

| Day 30 Overdue | Escalate | Consider a formal letter or debt collection agency. |

A structured approach like this shows you're serious about getting paid but gives your client every chance to settle their account amicably.

Build Proactive Payment Strategies

Why wait for an invoice to be sent before thinking about getting paid? For bigger projects or ongoing retainers, you can build cash flow protection right into your agreements from day one.

- Take a Deposit: For any significant piece of work, always ask for an upfront deposit of 25-50%. This secures the client's commitment and gives you the cash to cover your initial costs.

- Use Milestone Payments: Break large projects into distinct phases and invoice as each one is completed. This turns a single, distant payment into a steady, predictable stream of income.

- Incentivise Early Payment: A small discount, maybe 2%, for invoices paid within seven days can be a surprisingly powerful motivator for clients who have the cash on hand.

For an even bigger boost, you can explore solutions like Contract Factoring for Cash Flow Management. This is a type of financing that gives you immediate cash against your outstanding invoices, effectively closing the gap between invoicing and getting paid.

Taking Control of Your Business Spending

Getting paid faster is only half the battle when it comes to improving your cash flow. The other, equally crucial side of the coin is getting a firm grip on your outgoings. When you spend smarter, you free up capital, ease financial pressure, and give your business the breathing room it needs to grow.

This isn't about slashing costs blindly and hurting your operations. It’s about a strategic review to make sure every pound you spend is pulling its weight. The whole process kicks off with a simple but revealing exercise: a proper expense audit.

Conduct a Detailed Expense Audit

The first step is to get forensic. Pull up your last six months of bank statements and categorise every single payment that has left your account. I’m not just talking about the big, obvious costs like rent or payroll. You need to scrutinise every direct debit, subscription, and recurring charge.

Try grouping everything into three buckets:

- Essential: These are the non-negotiables—the costs you have to pay to keep the lights on. Think rent, core staff salaries, and utilities.

- Growth-Oriented: This is spending that directly fuels your growth, like marketing campaigns, new equipment, or training.

- Non-Essential: Here’s where you’ll find the 'nice-to-haves' or legacy costs that have crept in. We’ve all seen them: underused software subscriptions, premium services where a cheaper alternative would do, or memberships that no longer offer any real value.

This audit gives you a clear map of where your money is actually going. It allows you to make informed decisions instead of cutting with a blunt instrument. With this clarity, you can start taking targeted action.

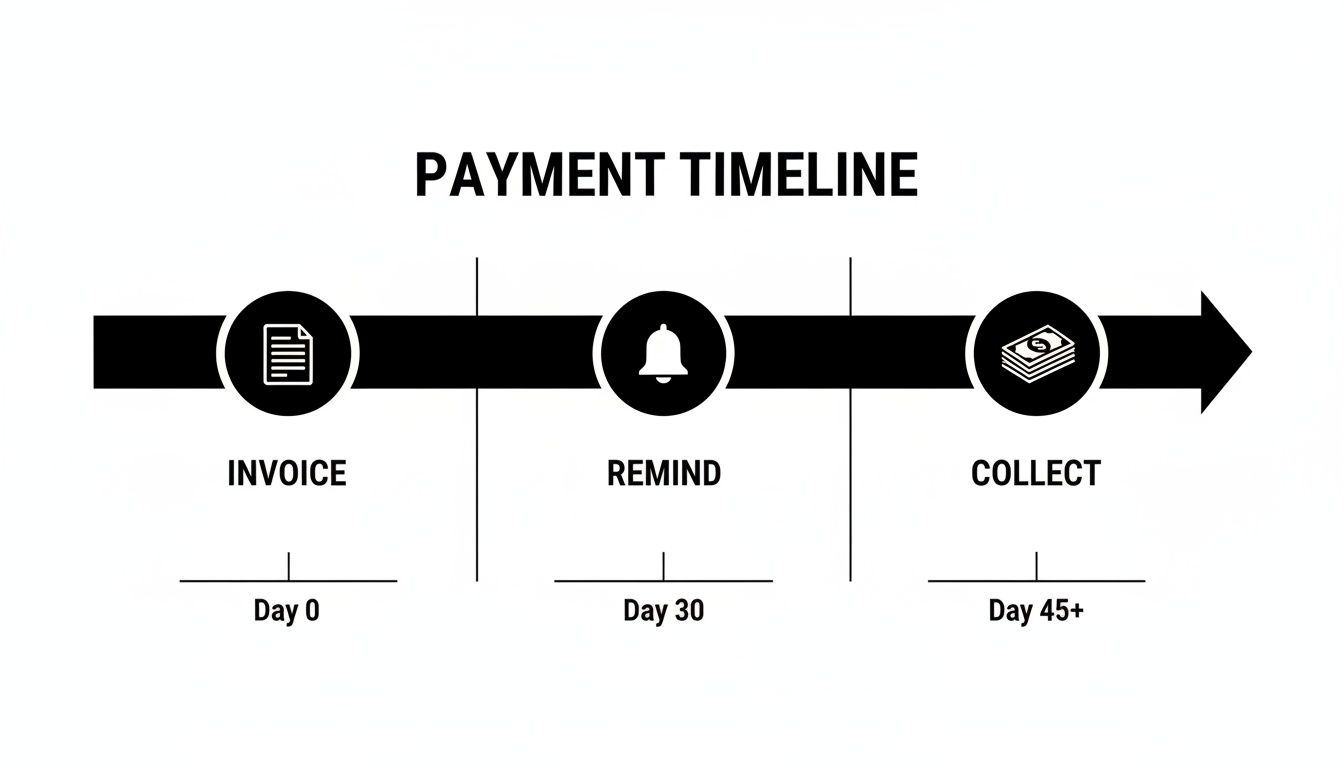

This visualisation shows the ideal journey for getting paid, a process that works hand-in-hand with tight spending controls to make sure cash comes in as efficiently as it goes out.

As the timeline shows, proactive reminders are a crucial step between invoicing and collection, helping you head off delays before they become serious problems.

Implement Strategic Cost-Saving Measures

Once you’ve spotted the areas for improvement, it's time to make practical changes that will have a real impact on your cash position. The key is to be methodical.

Start by tackling the low-hanging fruit. I always tell clients to audit their software subscriptions first. It's incredibly common to find you’re paying for multiple tools that do the same job or for user licences for people who left the team months ago. Consolidating these can easily save hundreds of pounds a year. For businesses running on cloud infrastructure, a good guide to cloud cost optimisation strategies is essential for reining in those specific, often complex, expenses.

Next, take a hard look at your bigger supplier contracts. When did you last renegotiate your terms? Never be afraid to ask for better pricing or more favourable payment terms, especially if you’ve been a reliable customer for years. A small discount from a key supplier can make a huge difference over a twelve-month period.

It's a common misconception that outsourcing tasks like bookkeeping is just another expense. In reality, it can be a powerful cost-saving move. It frees up your valuable time, reduces the risk of costly compliance errors, and often costs less than hiring a full-time employee.

With the number of small businesses in the UK using external finance dropping from 50% in Q3 2023 to 43% in Q2 2024, getting a handle on internal costs has become a critical way to improve cash flow. Lenders are rewarding lean, efficient operators, even with gross bank lending stable at £62 billion. Since 57% of SMEs expect their costs to rise, a focused effort to trim non-essential spending can preserve 10-25% of your operating expenses.

Master Your Inventory and Tax Efficiency

If your business sells physical products, your inventory is probably one of your biggest cash drains. Every item sitting on a shelf represents cash that's tied up and can't be used for anything else. Bringing in a Just-In-Time (JIT) inventory system, where you order stock only as needed to fulfil customer orders, can dramatically reduce how much capital is locked away in unsold goods.

Finally, think about tax. Are you set up in the most efficient way possible? How you manage your VAT, for example, can have a massive impact on your day-to-day cash. It’s well worth looking into using the VAT Cash Accounting Scheme, which lets you pay VAT to HMRC only when your customers have actually paid you. This simple change directly aligns your tax outgoings with your cash inflows.

Building a Resilient Financial Future

Constantly reacting to cash flow problems is just exhausting. If you feel like you're always putting out financial fires, it's time to change tactics. The goal is to move from being reactive to proactive—to stop looking at what’s already happened and start predicting what’s coming next.

This is where a good cash flow forecast comes in. It’s not some dark art reserved for FTSE 100 companies; it’s a practical, essential tool for every business owner. A solid forecast gives you a clear line of sight, helping you spot potential cash crunches weeks or even months down the road.

But it's not just about dodging bullets. A forecast can also highlight opportunities. It might reveal you have the cash surplus to snap up a discounted stock order or to finally hire that salesperson you need to fuel growth. Without that visibility, you’re flying blind.

Crafting a Reliable Cash Flow Forecast

For most small to medium-sized businesses, the sweet spot for planning is a 13-week cash flow forecast. It’s the perfect rolling window—long enough to see what’s on the horizon, but short enough to be genuinely accurate and useful.

Getting started is simpler than it sounds. First, you list all your expected cash inflows for each of the next 13 weeks. This isn’t guesswork; it’s based on real data.

- Confirmed Sales: Money you know is coming in from invoices you’ve already sent.

- Pipeline Projections: This is where you look at your sales pipeline and make an educated guess, maybe weighting potential deals by the probability they'll close.

- Other Income: Don’t forget anything else, like a tax refund, an asset sale, or a grant payment.

Next, you do the same for your cash outflows. Be brutally honest with yourself here.

- Fixed Costs: These are the easy ones—rent, salaries, software subscriptions that don’t change.

- Variable Costs: Things that move with your sales, like supplier payments, raw materials, and shipping costs.

- One-Off Payments: This is crucial. Always factor in those big, lumpy payments like your quarterly VAT bill, corporation tax, or a major equipment purchase.

By subtracting your outflows from your inflows week by week, you build a picture of your closing bank balance. This simple exercise fundamentally changes how you manage your money. You’re no longer just reacting; you’re making strategic decisions that will actively improve your business cash flow.

Tapping into Technology for Real-Time Insights

Let's be honest, manually updating a spreadsheet forecast can be a real pain. It's one of those jobs that easily slips to the bottom of the to-do list. This is precisely why modern cloud accounting software has been such a game-changer.

Platforms like Xero or QuickBooks can connect directly to your bank account, pulling in real-time transaction data automatically. A lot of the heavy lifting is done for you, giving you a live, accurate picture of your company's financial health without the tedious data entry.

The real magic here is having a live pulse on your business. You can see the immediate ripple effect of a customer paying late or an unexpected bill landing on your desk. This allows you to take action long before a small issue snowballs into a full-blown crisis.

Tracking the Metrics That Truly Matter

A forecast is a powerful tool, but it becomes even more potent when you pair it with the right Key Performance Indicators (KPIs). Think of these as the vital signs for your company's financial health. You don't need to track dozens of metrics; just focus on the few that tell you the most important stories.

Your dashboard should be built around these core cash flow numbers.

I've put together a quick table of the essential KPIs every business owner should have on their radar. These give you a quick, measurable snapshot of what's really going on with your cash.

Essential Cash Flow KPIs for Your Business Dashboard

| KPI | What It Measures | Simple Formula | Good Target |

|---|---|---|---|

| Debtor Days | The average time it takes for customers to pay you. | (Receivables / Revenue) x 365 | Under 30 days |

| Creditor Days | The average time it takes you to pay your suppliers. | (Payables / Cost of Goods) x 365 | 30-45 days |

| Cash Conversion Cycle | The time it takes to turn inventory and work into cash. | Inventory Days + Debtor Days – Creditor Days | As low as possible |

| Current Ratio | Your ability to cover short-term liabilities. | Current Assets / Current Liabilities | Above 1.5 |

Keeping a close eye on these figures helps you spot negative trends before they cause real damage. If your Debtor Days start creeping up from 35 to 45, you know it’s time to get tougher with your credit control. If your Current Ratio dips below 1.5, it’s a clear warning that you either need more cash in the bank or need to tackle some short-term debts.

This is what a data-driven approach looks like in practice, and it’s the bedrock of a financially resilient business.

Using Finance and Advice to Fuel Your Growth

Getting your internal house in order is a massive step, but sometimes you need a bit of outside fuel to really get the engine going. A healthy cash flow isn’t just about keeping the lights on; it’s the lifeblood that lets you chase bigger contracts, bring on new talent, or invest in that game-changing piece of kit. This is exactly where smart financing can make all the difference.

But hold on. It’s not as simple as just asking for a loan. Any lender or investor worth their salt will put your business under a microscope, and the first thing they'll look at is your financial health. Your accounts have to be pristine—clean, accurate, and completely current. Messy books are the fastest way to get a "no".

Choosing the Right Financial Tools for Growth

Not all finance is created equal. Picking the wrong kind can create more problems than it solves, leaving you with crippling debt or terms that strangle your flexibility. The real skill is matching the right tool to the specific cash flow challenge you're up against.

For countless UK SMEs, the biggest headache is the gap between sending out a big invoice and the money actually landing in the bank. This is where working capital solutions are brilliant.

Invoice Financing: This lets you borrow against the value of your unpaid invoices. You can typically get an advance of up to 90% of the invoice's value in a matter of days. It’s an incredibly effective way to smooth out those peaks and troughs in your income, giving you cash to cover costs while you wait for clients to pay.

Business Line of Credit: Think of this as your financial safety net. It’s a pre-agreed pot of money you can dip into whenever you need it and pay back as funds come in. It’s perfect for handling unexpected costs or covering short-term gaps without the hassle of a new loan application every time.

One crucial point, though: these tools are designed to fix timing problems, not profitability problems. If the business fundamentally isn’t making money, taking on debt will only pour fuel on the fire.

The Role of a Strategic Financial Partner

Juggling cash flow, chasing growth, and seeking finance can feel like spinning plates, especially when you’re also running the business day-to-day. This is why a modern accountant is so much more than a compliance box-ticker.

Forget just year-end accounts and tax returns. A proactive accountant acts as a strategic partner. They dive into your numbers and help you turn raw data into smart decisions. They can help you build the kind of robust cash flow forecasts lenders love to see, pinpoint the right finance for your goals, and make sure your application is built on solid, credible foundations.

A great accountant doesn’t just report on what happened last year; they help you shape what will happen next year. They provide the clarity and confidence you need to make bold, informed decisions about the future of your business.

Ultimately, this kind of partnership gives you back your three most valuable resources: more time, more money, and more peace of mind.

Building a Business That Lenders Trust

When a lender looks at your application, they’re really only asking one question: "Is this a well-managed business that can comfortably pay us back?" Your financial records are the main piece of evidence you have to prove the answer is "yes".

So, what does a strong financial profile look like from their side of the table?

- Up-to-Date Bookkeeping: Your books are current, and your bank accounts are reconciled every week. It shows you have a constant, real-time grip on your money.

- Clear Reporting: You can instantly pull up a clear Profit & Loss statement, Balance Sheet, and—most importantly—a detailed cash flow forecast for the next 6-12 months.

- Positive Cash Flow: Your history shows that the business actually generates cash from its main operations. This proves your business model is sound.

- Tax Compliance: All your VAT, PAYE, and Corporation Tax returns are filed on time. Lenders won't touch a business that has problems with HMRC.

Getting these things right does more than just prepare you for a funding application. It’s the hallmark of a resilient, well-run business that's ready for proper, sustainable growth. It sends a clear signal to everyone—lenders, investors, even future buyers—that your company is a solid and reliable bet.

Your Top Cash Flow Questions Answered

When you're buried in the day-to-day of running a business, it's easy to get overwhelmed. The same practical money questions seem to pop up again and again. Here, we tackle those common queries head-on with direct, no-nonsense answers to help you get a grip on your cash flow.

Think of this as your go-to guide for making smarter financial decisions with confidence, reinforcing the core ideas we've already covered.

What’s the Very First Thing I Should Do to Improve My Business Cash Flow?

The most powerful, immediate action you can take is to get laser-focused on your accounts receivable. This is the cash you’ve earned but is still sitting in your customers' bank accounts, not yours.

Start by pulling a list of every single overdue invoice. Yes, even the ones that are only a day late. Work out a systematic plan to chase them, starting with the biggest and oldest debts first. You’d be surprised how often a polite email or a quick phone call is all it takes to get things moving.

At the same time, make it a golden rule to invoice the second a job is finished or a product is delivered. Every day you wait to send an invoice is a day you've chosen to delay getting paid. Closing that gap is a foundational fix you can implement today for a near-instant improvement.

How Can I Forecast Cash Flow with an Irregular Income?

Forecasting with a fluctuating income isn’t just possible—it’s absolutely vital. For businesses with seasonal rushes or lumpy sales cycles, a smart approach to forecasting is your best strategic weapon.

First, dig into your sales data from the last 12-24 months. Look for the hidden rhythm in your business—are there seasonal patterns or recurring trends you can lean on? Once you have a feel for this, create three different forecast scenarios:

- Best-Case: An optimistic but still believable picture of what you could bring in.

- Worst-Case: A pessimistic view that forces you to plan for the tough times.

- Most-Likely: Your realistic, middle-of-the-road forecast that will guide most of your decisions.

Run your business based on the 'most-likely' scenario, but use the 'worst-case' to define the absolute minimum cash you need to keep in the bank as a buffer. You’ll want to update this forecast weekly or bi-weekly as fresh sales data rolls in. This is where cloud accounting software like Xero or QuickBooks really shines, as it automates much of this by pulling in real-time info from your bank and invoices.

Is a Business Loan a Good Way to Solve a Cash Flow Problem?

A loan can be a brilliant solution, but only if you're crystal clear on what problem you're actually solving. It’s crucial to know if you're fixing a temporary cash crunch or just plastering over a fundamental flaw in your business model.

If you’ve hit a short-term gap—say, you need to buy a mountain of stock to fulfil a huge, confirmed order—then a short-term loan or line of credit is a smart, strategic move. It's a tool that enables growth you couldn’t otherwise afford.

But be honest with yourself. If your business is consistently losing money and you need to borrow just to cover day-to-day running costs, a loan is only a temporary sticking plaster. It masks the real issues while piling on long-term financial pressure.

Before you even think about external finance, you have to nail the internal strategies we've talked about. This is where a good accountant becomes your most valuable player. They can help you diagnose the root cause of the cash shortage and figure out if debt would be a strategic springboard for growth or just a costly patch for a sinking ship. Getting that clarity is essential.

Navigating these challenges is at the heart of what we do at Stewart Accounting Services. If you're ready to move from reactive fire-fighting to proactive financial strategy, our team is here to provide the clarity and support you need to achieve your goals. Explore our accounting services for UK SMEs and take the first step towards a more secure financial future.