Ever found yourself staring at a surprisingly large Self Assessment tax bill, wondering how you'll pay it all in one go? That’s exactly what HMRC’s ‘Payments on Account’ system is designed to prevent.

Think of them as advance payments towards your next tax bill. It's not an extra tax, but a way to spread the cost, making your tax obligations much more manageable and predictable throughout the year.

What Are Payments on Account Really?

Let’s use an analogy. Imagine you're paying for a big holiday. Instead of a single, hefty payment right before you fly, you pay a deposit and then another instalment closer to the date. Payments on account work in a very similar way, splitting your estimated tax bill into two more manageable chunks.

This system is a standard part of the Self Assessment process for many self-employed individuals, business partners, and landlords in the UK. It’s not a penalty; it’s simply a method of proactive tax planning that helps you stay on top of your finances.

The Core Rules and Dates

So, who actually has to make these payments? HMRC sets out some clear criteria. You’ll usually need to make payments on account if your last Self Assessment tax bill was more than £1,000 and less than 80% of your total tax due was collected at source (for example, through PAYE from an employment). You can read up on the full details on the official government guidance about understanding your Self Assessment bill.

These payments are calculated based on your previous year's bill and are due on two specific dates every year. The idea is to align your tax payments more closely with the time you’re actually earning the income.

A common misconception is that this is an additional tax. In reality, these payments are a credit towards your final bill for the current tax year. Any difference is settled later with a final 'balancing payment'.

To make it even clearer, here’s a quick summary of the key rules and dates you need to have on your radar.

Payments on Account At a Glance

The table below breaks down the fundamental concepts you need to remember.

| Concept | Explanation |

|---|---|

| Tax Bill Threshold | Your previous Self Assessment tax bill must be over £1,000. |

| First Payment Deadline | 31 January (during the tax year). |

| Second Payment Deadline | 31 July (after the tax year ends). |

| Calculation Basis | Each payment is typically 50% of your previous year's tax bill. |

Getting these dates and rules right is the first step to mastering your tax planning and avoiding any unwelcome surprises from HMRC.

Who Needs to Make Payments on Account?

So, does everyone filing a Self Assessment have to deal with payments on account? Thankfully, no. HMRC has a couple of specific rules to figure out who needs to pay their tax this way, and it’s mainly aimed at people whose income isn't already taxed at source.

You’ll be asked to make payments on account only if your last tax return hit two specific criteria. First, your total Self Assessment tax bill for the year was more than £1,000. Second, the tax you paid ‘at source’ (like PAYE from a job) covered less than 80% of your total tax bill.

Think of it this way: if you have a full-time job and a small side hustle, the tax deducted from your salary probably covers most of what you owe, so you likely won’t have to make payments on account. But as soon as your income from self-employment or property starts to grow, you'll almost certainly cross that threshold. For a deeper dive into this, you can learn more about who must send in a tax return on our blog.

The Usual Suspects: Who Typically Pays This Way?

The technical rules are one thing, but it’s often easier to see who this affects in the real world. Certain types of businesses and professions are far more likely to get caught in the payments on account net simply because of how they earn money.

You’ll almost certainly need to make these payments if you fall into one of these camps:

- Successful Sole Traders: As your business takes off, your profits—and the tax bill that comes with them—will probably sail past the £1,000 mark. Think of a freelance consultant, a plumber, or a graphic designer whose business is their main source of income.

- Property Investors and Landlords: Rental income lands in your bank account with no tax taken off. Once your portfolio is bringing in enough to create a tax liability over £1,000, you’ll be brought into the payment on account system.

- Partners in a Business: If you're a partner in a firm, you're taxed on your share of the profits. This isn't taxed at source, so partners almost always have to make payments on account.

- Freelance Creatives: Writers, artists, musicians, you name it. Your income is often project-based and paid gross, which means managing your own tax is part of the deal. Once you’re established, payments on account become a regular fixture.

The core idea is simple: if most of your income doesn't have tax deducted before you receive it, and your annual tax bill is substantial, HMRC expects you to pay in advance for the next year.

Recognising if you fit one of these profiles is the first step. If you do, getting ahead of the game and planning for these twice-yearly payments is absolutely crucial for keeping your cash flow healthy and avoiding any nasty surprises.

How HMRC Calculates Your Payments

Getting your head around the maths behind payments on account can feel daunting, but it’s actually more straightforward than you might think. HMRC isn't trying to catch you out with a complex formula; the calculation is based on a simple assumption about your earnings.

The whole system works on the idea that your income this year will be roughly the same as it was last year. So, HMRC takes your total Self Assessment tax bill from the previous year and simply splits it in half. Each half becomes one of your two payments on account for the current tax year.

The core formula is simple: (Last Year's Total Self Assessment Tax Bill) ÷ 2 = Your Payment on Account Amount. You'll pay this amount twice, once by the 31 January deadline and again by 31 July.

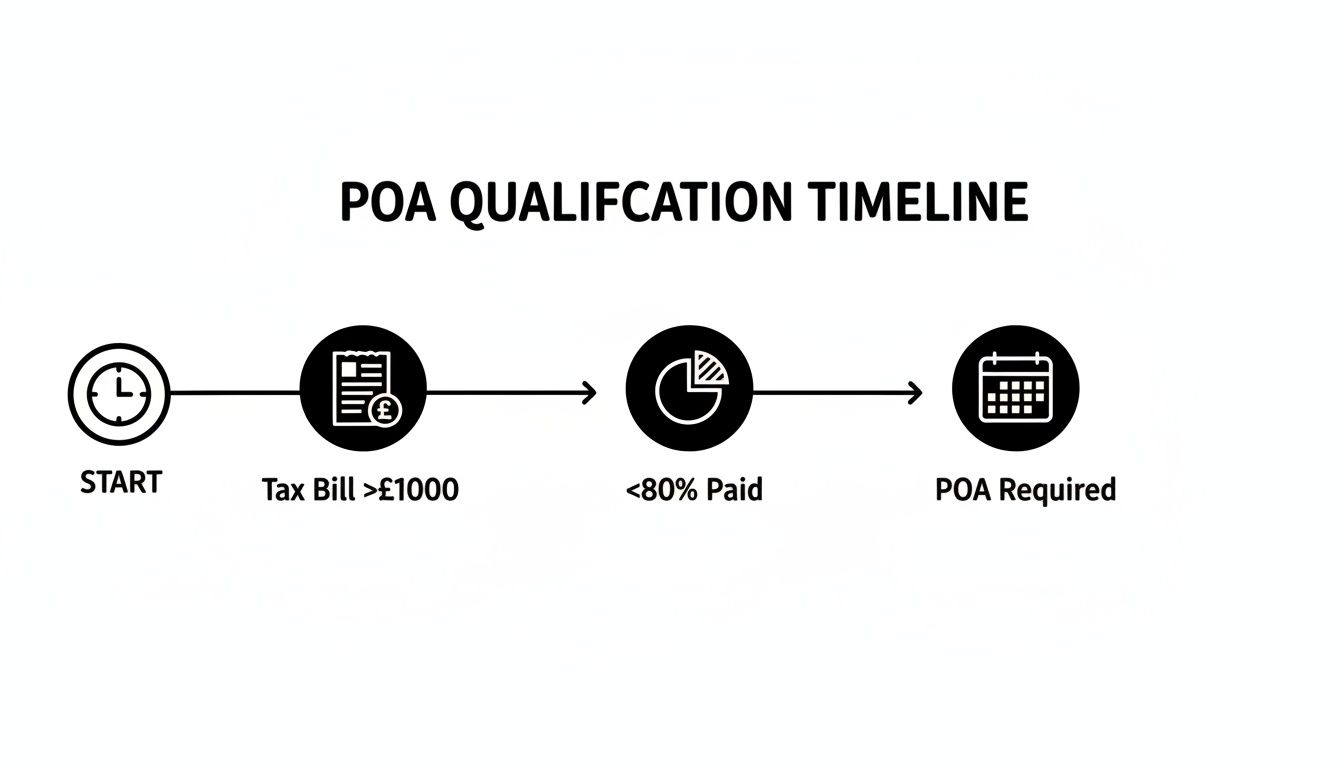

This timeline breaks down the basic trigger points for entering the payment on account system.

As you can see, once your tax bill climbs over £1,000 and less than 80% of it was paid at source (like through PAYE), the system automatically ropes you into making these advance payments for the following year.

A Practical Example Step-by-Step

Let's walk through a real-world scenario to see how this plays out. We'll use a fictional sole trader, Alex the electrician. For the 2023/24 tax year (which ended on 5 April 2024), Alex did well and his final tax and Class 4 National Insurance bill came to £4,000.

Since his bill is well over the £1,000 threshold and he had no tax deducted at source, he now has to make payments on account for the 2024/25 tax year.

Here’s how HMRC calculates what he owes:

- First Payment on Account: Due by 31 January 2025. This is £2,000 (50% of his £4,000 bill from 2023/24).

- Second Payment on Account: Due by 31 July 2025. This is another £2,000 (the remaining 50%).

Now, here’s the bit that often catches people by surprise. On that same 31 January 2025 deadline, Alex also has to settle the full £4,000 he owes for the 2023/24 tax year. This is often called the 'balancing payment'.

This means his total bill due on that one day is a hefty £6,000 (£4,000 for last year + £2,000 for this year's first payment).

To make this crystal clear, let's map out Alex's payment journey over the next 18 months.

Example Tax Year Payment Timeline

| Date | Payment Type | Amount | Notes |

|---|---|---|---|

| 31 Jan 2025 | Balancing Payment (for 2023/24) | £4,000 | This clears his tax bill for the previous year. |

| 31 Jan 2025 | First Payment on Account (for 2024/25) | £2,000 | This is the first advance payment for the current tax year. |

| 31 July 2025 | Second Payment on Account (for 2024/25) | £2,000 | This is the second advance payment. |

| 31 Jan 2026 | Submit 2024/25 Tax Return | – | Alex files his return, and HMRC calculates his final tax liability for the year. |

This timeline shows how the payments are staggered, but also highlights the significant cash outflow on the first January deadline.

This “first-year shock” is a common stumbling block for newly self-employed people and growing businesses. I've seen countless contractors and landlords get caught out when a good year results in a tax bill that's suddenly 150% of what they expected. As many practical UK tax guides explain, once you're in the system, you're expected to stay in it unless your income drops significantly.

By the end of July 2025, Alex will have paid a total of £4,000 towards his 2024/25 tax bill. When he files his tax return for that year (by January 2026), this £4,000 he’s already paid will be deducted from whatever his final liability turns out to be.

How to Reduce Your Payments on Account

Just because HMRC has sent you a bill for Payments on Account based on last year’s profits, don’t assume that figure is set in stone. Your business isn't static, so why should your tax payments be?

Life happens. Maybe you've lost a major contract, decided to take a few months off, or switched from full-time contracting to a part-time venture. If you're confident your income is going to be lower this year, you can—and absolutely should—ask HMRC to reduce what you owe upfront.

This isn’t some loophole; it’s a formal process designed to stop you from overpaying tax and tying up cash you need for your business. It’s all about making your advance payments a more accurate reflection of what you'll actually earn.

Making an Official Claim for Reduction

So, how do you go about it? HMRC gives you two main options to officially request a reduction.

For most people, the simplest way is to log into their Government Gateway account. You can make the claim to reduce your payments any time before the deadline. Just find the Self Assessment section and follow the steps to adjust the figures based on your new, lower profit forecast.

If you prefer the old-school route, you can fill out and post form SA303, 'Claim to Reduce Payments on Account', directly to HMRC. Both methods achieve the same thing: formally telling HMRC that their estimate is out of date.

A Word of Warning: Be careful here. This needs to be a realistic and honest forecast. If you slash your payments too drastically and your final tax bill is higher than what you've paid, HMRC will hit you with interest on the shortfall.

The Consequences of Getting It Wrong

The system works on the assumption you'll make a reasonable estimate, but there are penalties if you get it wrong. If you reduce your payments and it turns out your final tax bill is higher, you'll be on the hook for the difference.

HMRC will charge interest on the amount you underpaid, calculated all the way back to the original payment due dates (31 January and 31 July). The trick is to strike the right balance—reduce the payment enough to help your cash flow, but not so much that you trigger interest charges later.

Getting this right is a crucial part of smart tax management. For more ideas on keeping your tax bill down, our guide on how to reduce business taxes has some great practical tips.

Strategic Cash Flow Planning for Tax Payments

Dealing with payments on account shouldn't feel like a financial fire drill every six months. With a bit of foresight, you can turn these tax obligations from a source of stress into just another predictable business expense. It all comes down to proactive cash flow planning.

Instead of scrambling when the January and July deadlines loom, the trick is to start treating tax as a regular, ongoing cost, just like your rent or supplies. This small shift in mindset is the absolute bedrock of good financial management for any sole trader, landlord, or contractor.

The simplest and most effective first step? Open a separate bank account purely for your tax savings. As soon as a client pays you, get into the habit of transferring a set percentage straight into this account. This one action builds a financial buffer almost automatically.

Building Your Financial Buffer

Having a system to save for tax removes the guesswork and gives you incredible peace of mind. Here are a few practical things you can do today to get ahead of your payments on account.

- Set Up a Dedicated Tax Pot: Open a separate, easy-access savings account. This ring-fences your tax money, making it much less tempting to dip into for other business costs.

- Work Out Your Savings Rate: A good starting point is to look at last year’s tax bill and calculate what percentage it was of your total income. Use that as a baseline. A good rule of thumb is to set aside 20-30% of everything you earn.

- Automate, Automate, Automate: Use your banking app to set up a standing order that moves money into your tax account every week or month. Automation builds consistency without you even having to think about it.

Putting solid financial strategies in place is crucial. For a broader perspective, there are some great guides on effective cash flow management for small businesses that offer a fantastic framework.

Using Technology and Regular Reviews

Modern accounting software is your best friend here. Tools like Xero can give you a real-time estimate of your upcoming tax liability, turning a vague future bill into a clear number you can aim for. If you're looking for more specific tips, we've put together some detailed advice on https://stewartaccounting.co.uk/saving-to-pay-tax/.

By treating tax planning as an ongoing activity rather than a once-a-year headache, you stay in control. Regular financial check-ins—maybe monthly or quarterly—allow you to tweak your savings rate based on how your business is actually doing, ensuring you’re always prepared.

This proactive approach stops any nasty surprises right in their tracks and keeps your business cash flow healthy. You’ll know exactly where you stand, which frees you up to focus on what you do best: running and growing your business.

Common Questions About Payments on Account

Even once you get the hang of payments on account, specific situations can throw up new questions. To help you feel more confident, let's walk through some of the most common queries we hear from business owners and landlords.

What Happens if I Miss a Deadline?

If you miss the 31 January or 31 July deadline, HMRC will start charging interest on the outstanding amount straight away. The clock starts ticking the day after your payment was due.

Leave it too long, and you could be hit with additional late payment penalties on top of the interest. It’s a situation that can quickly spiral, so getting your payments in on time is crucial.

Do I Pay if I Stop Being Self-Employed?

No, not for the tax years after you stop. When you cease trading, your first job is to let HMRC know and get your final tax return filed.

Once that’s done, you can officially ask HMRC to reduce your payments on account to zero. It makes sense – you won't have that income anymore, so there's no tax to pay in advance.

What if I Overpay Through Payments on Account?

This is actually a pretty common scenario, and it’s good news. If your final tax bill ends up being less than what you’ve paid in advance, HMRC owes you a refund.

This refund is processed automatically after you’ve filed your Self Assessment return and your final, lower tax liability has been confirmed. You don’t need to do anything extra to claim it back.

The system is built to handle these kinds of adjustments. HMRC's own figures from 2017-18 show that Self Assessment receipts involved annual adjustments between £5,673 million and £7,076 million, which really shows how often payments are realigned with actual earnings. You can explore more about these UK income tax statistics directly.

Can I Make Voluntary Payments?

Yes, you certainly can. You can make payments towards your tax bill whenever you like using your HMRC online account.

This can be a fantastic way to manage your cash flow. Instead of facing two hefty lump sums, you can chip away at your tax bill with smaller, more regular payments throughout the year.

Taking Control of Your Tax

Payments on account don't need to be a constant headache. Once you get your head around how they work, you can start planning for them, treating your tax bill just like any other regular business cost. That simple shift in mindset is the key to taking control and avoiding any nasty surprises from HMRC.

We've covered a lot of ground here, from the basics of what payments on account actually are, right through to the calculations, deadlines, and practical tips for managing them. Hopefully, you now feel equipped to turn this part of Self Assessment from something you dread into a predictable, manageable part of your financial year.

The Power of Planning Ahead

If there's one thing to take away from all this, it's that being proactive is your greatest ally. Building up a tax pot and keeping on top of your accounts aren't just 'good business practices'; they're absolutely vital for keeping your cash flow healthy and giving you some much-needed peace of mind.

It all boils down to a few simple habits:

- Save as you earn: Get into the rhythm of moving a slice of every payment you receive into a separate tax account.

- Know your numbers: Keep a close eye on your income. This way, you can make a much better guess at what your final tax bill will look like.

- Ask for help: If you're ever feeling out of your depth, don't just guess. A quick chat with a professional can save you a world of stress.

Getting to grips with payments on account is about more than just ticking a box for HMRC. It’s about building a stronger, more financially resilient business. It’s the difference between constantly reacting to tax demands and being in a position to focus on what you do best: growing your business.

With this knowledge, you can face your tax obligations with confidence, knowing you’re well-prepared and in control of your financial health.

If you're a sole trader, landlord, or run a small business in Central Scotland or anywhere in the UK, getting this right can make a huge difference. At Stewart Accounting Services, we're here to bring clarity to these complexities. We work with our clients to manage their payments on account, improve their tax efficiency, and give them back the time to focus on their business.

Get in touch today and let us put your finances in expert hands. You can find out more at https://stewartaccounting.co.uk.