When it comes to lowering your business tax bill, the basic principle is quite straightforward: legally maximise your allowable expenses and make sure you're using every tax relief available to you. For UK business owners, this isn't about last-minute panic at the year-end; it's about proactively managing things like director salaries, pension contributions, and asset purchases throughout the year.

Building a Foundation for Smarter Tax Planning

Let's get one thing straight: effective tax reduction isn't about finding shady loopholes. It’s simply about making smart, strategic use of the legitimate, government-approved schemes designed to help businesses like yours keep more of their hard-earned cash.

Too many business owners treat tax as a chore to be dealt with once a year. But if you shift your perspective, you can turn tax planning into a powerful tool for growth. This guide breaks down the process for UK SMEs, whether you're a sole trader or the director of a limited company. The key is moving from a reactive scramble to a proactive, ongoing strategy built on solid financial habits.

Key Pillars of Tax Efficiency

A solid tax plan is built on a few core areas. Get these right, and you’re well on your way to ensuring you pay the correct amount of tax—and not a penny more.

- Owner Remuneration: How you pay yourself is crucial. Perfecting the mix of salary versus dividends is often the single biggest tax win for limited company directors.

- Allowable Expenses: This is fundamental. Claiming for every legitimate business cost, from software to mileage, directly reduces your profit and, consequently, your final tax bill.

- Pension Contributions: Making company pension payments is an incredibly tax-efficient way to extract profit. They are usually treated as an allowable business expense, cutting your Corporation Tax.

- Capital Allowances: This is HMRC’s way of giving you tax relief when you buy significant assets for your business, like new equipment, vans, or computers.

Thinking about tax throughout the year, rather than just before a deadline, unlocks significant savings. Proactive planning allows you to structure transactions and time investments in a way that maximises reliefs and minimises liabilities, directly boosting your cash flow.

Ultimately, this isn't just a box-ticking exercise for your accountant. It’s a core part of your business strategy. Getting it right frees up capital that can be reinvested into marketing, hiring new staff, or upgrading equipment.

Adopting a structured approach ensures your finances are working as hard for the business as you are. For a deeper dive into this foundational mindset, our guide on smart tax planning and how to get it right offers further insights.

Fine-Tuning Your Director's Pay and Pension

As a director of a limited company, how you take money out of the business is one of the most significant levers you can pull to manage both your personal and corporate tax bills. This isn't just about paying yourself a wage; it's about smart, strategic planning. The classic dilemma is salary versus dividends, but the best answer is almost never one or the other—it's about striking the perfect balance.

By understanding the rules, you can structure your remuneration to legally minimise what you owe in National Insurance Contributions (NICs) and income tax. The goal is simple: keep more of your hard-earned money.

Hitting the Salary Sweet Spot

For most owner-directors, the game plan is to pay a small, highly efficient salary. This isn't a figure plucked from thin air. It’s a specific amount calculated to unlock key state benefits without triggering a hefty tax or National Insurance bill.

The trick is to pay yourself a salary that’s above the Lower Earnings Limit (£6,396 for 2024/25). Crossing this line ensures the tax year counts as a 'qualifying year' for your State Pension, even if you don't actually pay any NICs on it. It’s a crucial box to tick for your future.

A very common and effective strategy is to set your salary at the National Insurance Primary Threshold, which is £12,570 for the 2024/25 tax year. At this level, you pay 0% employee's NICs and the company pays 0% employer's NICs. You still secure that vital qualifying year for your pension, making it a genuine win-win.

Drawing the Rest with Tax-Smart Dividends

Once your salary is set, you can take any further income as dividends. Dividends are distributions of the company's post-tax profits, and their single biggest advantage is that they are completely free of National Insurance.

This is where the serious savings kick in. A higher salary would attract both employee and employer NICs (at 8% and 13.8% respectively, above the thresholds). By using dividends, you sidestep these charges entirely, potentially saving thousands of pounds every year.

On top of that, everyone gets a personal Dividend Allowance. For the 2024/25 tax year, this is £500, meaning the first £500 of dividends you receive are completely tax-free, no matter what your other income is.

The go-to strategy for most UK company directors is combining a low salary (up to the NI threshold) with dividend payments. This mix secures state pension credits while avoiding punishing National Insurance costs.

To really get into the numbers and see how this works in practice, it’s well worth exploring a full guide to the salary versus dividends debate.

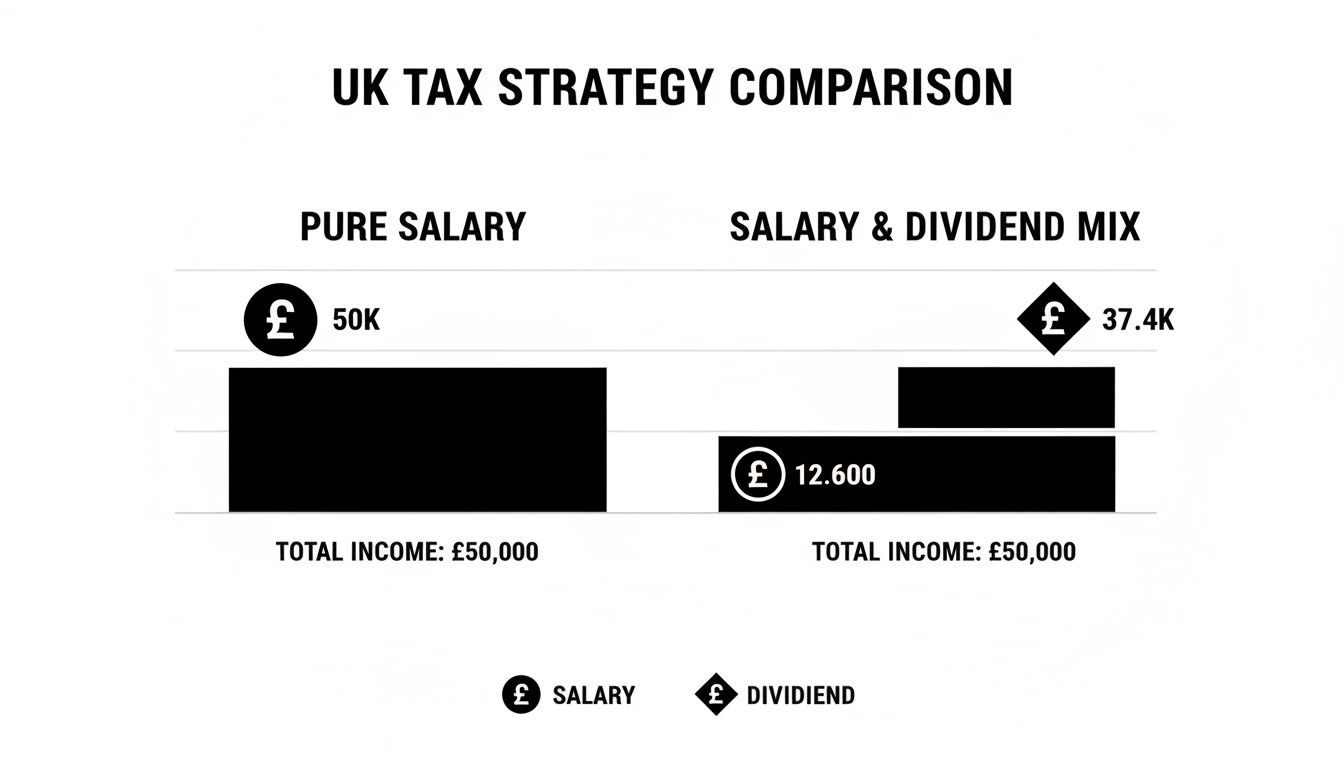

Here’s a quick comparison to illustrate just how powerful this split can be.

Salary vs Dividends: A Tax Efficiency Snapshot

This table shows the difference in your take-home pay when receiving £50,000, first as a pure salary and then as a blended salary-dividend package.

| Metric | £50,000 Pure Salary | £12,570 Salary + £37,430 Dividends |

|---|---|---|

| Gross Amount | £50,000 | £50,000 |

| Corporation Tax | £0 (Salary is an expense) | £9,357.50 (on profits) |

| Income Tax | £7,486 | £2,113.88 |

| Employee NICs | £3,043.44 | £0 |

| Employer NICs | £5,164.74 | £0 |

| Total Tax & NICs | £15,694.18 | £11,471.38 |

| Net Cash in Pocket | £34,305.82 | £38,528.62 |

As you can see, the salary and dividend mix puts over £4,200 more in your pocket for the same gross amount drawn from the company. It's a clear demonstration of why this structure is so popular.

The Hidden Power of Company Pension Contributions

Beyond salary and dividends lies another incredibly effective tool for taking profit out of your business: pension contributions. When your limited company pays directly into your personal pension, it’s a double-win for tax efficiency.

First, the contribution is almost always treated as an allowable business expense. This means the full amount is deducted from your company's profits before Corporation Tax is calculated. With Corporation Tax rates at 19% or 25%, that’s a direct and significant saving for the business.

Second, the money arrives in your pension pot without you paying a penny of personal income tax or National Insurance on it. It’s then free to grow in a tax-sheltered environment until you retire.

Let’s put that into perspective with a quick example.

- Scenario: Your company has £20,000 in surplus profit to extract.

- Option 1 (Dividend): The company first pays Corporation Tax (let's say 19%), which is £3,800. This leaves £16,200. If you take this as a dividend as a higher-rate taxpayer (33.75%), you’ll pay another £5,467.50 in personal tax. You’re left with just £10,732.50.

- Option 2 (Pension Contribution): The company pays the full £20,000 straight into your pension. It’s an allowable expense, so there's no Corporation Tax on it. You also pay no personal tax. The full £20,000 lands in your pension pot.

The difference is staggering. This isn’t just a minor tax tweak; it's one of the most powerful ways to slash your business tax bill while building substantial personal wealth for the future. Every director should have this on their radar.

Claiming Every Allowable Expense and Capital Allowance

Once you’ve sorted out your director's pay, the next big win for cutting your tax bill is to claim every single allowable expense. This is where good bookkeeping really pays off, because every pound you legitimately expense is a pound less profit for HMRC to tax.

It’s easy to claim for the obvious things like stock, rent, and wages. But so many business owners leave serious money on the table by overlooking the less common—but perfectly valid—costs of running their company.

Think about it: for every £100 in unclaimed expenses, a business paying 25% Corporation Tax is just handing over an extra £25 for no reason. It all adds up.

As you can see, structuring your finances smartly makes a huge difference to what you take home. Nailing your expenses is a massive part of that strategy.

Uncovering Overlooked Business Expenses

To make a real dent in your tax bill, you need to think beyond the usual suspects. It's well worth going through your bank statements with a fine-tooth comb, looking for those recurring costs you might have dismissed as too small or personal to bother with.

Here are a few of the most common expenses people miss:

- Working from Home: If your home is your office, you can claim for it. HMRC’s simplified flat rate is £26 a month, which is quick and easy. However, you can often claim more by calculating the actual business proportion of your household bills—things like mortgage interest, council tax, electricity, and broadband.

- Professional Development: That subscription to a trade journal? The membership fee for a professional body? A training course to sharpen your skills? If it’s purely for your business, it’s deductible.

- Mileage: Using your own car for business trips is a big one. You can claim a flat 45p per mile for the first 10,000 miles and 25p after that. This single rate is designed to cover everything—fuel, insurance, wear and tear—so you don't claim for those separately.

HMRC's golden rule here is that an expense must be "wholly and exclusively" for business. This doesn’t mean you can’t get any incidental personal benefit, but the main reason for the spend must be for your trade.

Getting Tax Relief on Your Assets with Capital Allowances

Now, what about the big-ticket items? Things you buy to keep and use in the business—like machinery, computers, or a company van—are treated differently from your day-to-day running costs.

You can’t just write off the full cost as an expense in one go. Instead, you claim what’s known as Capital Allowances. This is the taxman’s way of letting you deduct the asset's value from your profits over its useful life, giving you tax relief as it depreciates.

The two most powerful tools for this are the Annual Investment Allowance and First-Year Allowances.

Accelerate Your Savings with AIA and FYAs

For most small and medium-sized businesses, the Annual Investment Allowance (AIA) is a game-changer. It lets you deduct 100% of the cost of most plant and machinery in the year you buy it, right up to a hefty £1 million limit.

Let’s say your company pays 25% Corporation Tax and you buy a new piece of equipment for £40,000. The AIA allows you to knock that full £40,000 off your taxable profits, giving you an instant tax saving of £10,000 (£40,000 x 25%). It’s a huge boost to cash flow.

On top of the AIA, First-Year Allowances (FYAs) also offer 100% relief in year one for certain types of assets. These are often targeted to encourage businesses to invest in greener technology, like a brand-new, zero-emission electric van.

These allowances are incredibly effective for slashing your immediate tax bill. By planning your big purchases carefully, you can time them to get the maximum relief. It’s also wise to keep an eye on what’s coming down the track—you can read our thoughts on the new First Year Allowance from 1 January 2026 to see how things might change. Understanding these rules is key to making smart investments that also cut your tax liabilities.

Tapping into Specialist Tax Reliefs and VAT Schemes

Beyond the day-to-day tax planning, a whole other layer of savings is available through specialist reliefs. Many business owners see these as overly complex, but getting to grips with the basics can genuinely transform your bottom line, especially if your business is doing anything innovative or you want to get smarter with your VAT.

Diving into these areas is where you can see a proactive approach to your finances really pay off. It’s all about knowing which government schemes you actually qualify for and making sure you’re set up correctly from the get-go.

Are You Missing Out on R&D Tax Credits?

When you hear "Research and Development" (R&D), it’s easy to picture scientists in lab coats. The reality is far broader. HMRC's definition is all about projects that try to make an advance in science or technology.

This could be anything from creating a new software platform to developing a more efficient manufacturing process or even inventing a new food recipe with unique properties. The key question is this: did your project face technical hurdles that an expert in the field couldn't just solve off the shelf? If so, you might have a qualifying R&D project on your hands.

The financial upside here is massive. For a profitable SME, R&D relief gives you an enhanced deduction that slashes your Corporation Tax bill. If your company is loss-making, you could even claim a payable tax credit from HMRC – a direct cash injection straight into your business bank account.

Let's look at a real-world example:

- Scenario: A small software firm spends £50,000 on salaries and materials developing a new project management tool that uses a unique algorithm.

- Outcome: Even if the project ultimately fails, the money spent trying to crack those technological challenges could qualify for R&D tax relief. That could mean a much smaller tax bill or a welcome cash payment from HMRC.

R&D tax relief isn't just for tech giants. I’ve seen small businesses in manufacturing, engineering, and even food production successfully claim it. They were doing qualifying work all along without even realising it. It’s one of the most generous but frequently underclaimed reliefs out there.

Picking the Right VAT Scheme for Your Business

For any business with a turnover above the VAT threshold (currently £90,000), just getting registered is only the first step. The specific VAT scheme you choose can have a huge impact on your cash flow and your admin workload. The standard scheme is the default, but it’s often not the most efficient choice.

The two most common alternatives are the Flat Rate Scheme and the Cash Accounting Scheme. Figuring out which one is the best fit for your business model is crucial for simplifying your bookkeeping and avoiding overpaying tax.

A Quick Comparison of Your VAT Options

Making the right choice here can make a tangible difference to how much you pay each quarter and how much time you spend on paperwork.

| Scheme | How It Works | Who It's Best For |

|---|---|---|

| Standard Scheme | You pay HMRC the VAT from your sales, minus the VAT you can reclaim on your purchases. It’s all based on invoice dates. | Most businesses, especially if you buy a lot of VAT-rated goods and services. |

| Flat Rate Scheme | You pay a fixed percentage of your total VAT-inclusive turnover. The rate depends on your industry, but you can’t reclaim VAT on most purchases. | Businesses with very few expenses (like consultants or IT contractors). It makes the maths much simpler. |

| Cash Accounting Scheme | You only deal with VAT when money actually changes hands – when you get paid or when you pay a supplier, not when you send or receive an invoice. | Any business with a turnover under £1.35 million, particularly if you give customers long payment terms. It’s a game-changer for cash flow. |

Getting this right from the start helps ensure your VAT process is a help, not a hindrance.

This kind of strategic thinking applies elsewhere, too. For example, the UK Budget 2025 announced a £4.3 billion business rates support package. This includes ongoing investment support like the £1 million Annual Investment Allowance and will bring in permanent lower business rates for over 750,000 retail, hospitality, and leisure businesses from April 2026. You can read up on the latest tax support available for businesses on GOV.UK. Keeping an eye on announcements like this is essential for effective long-term tax planning.

The Role of Smart Record-Keeping and Professional Advice

Every single tax-saving strategy we’ve covered, from claiming expenses to fine-tuning director pay, hinges on one critical thing: meticulous financial records. Without solid bookkeeping, even the most brilliant tax plan will simply fall flat. This isn’t just about ticking compliance boxes; it’s about having the right data at your fingertips to make smart, strategic moves.

Treating your bookkeeping as a frantic, year-end chore is one of the most expensive mistakes you can make. In reality, smart record-keeping is your best line of defence in an HMRC enquiry and your most powerful tool for spotting tax-saving opportunities all year round.

Transform Your Bookkeeping with Cloud Accounting

Let's be honest, the days of shoeboxes overflowing with faded receipts and messy spreadsheets are long gone. Modern cloud accounting software like Xero can turn bookkeeping from a dreaded chore into a genuine business asset. By linking directly to your business bank accounts, these platforms give you a live, up-to-the-minute picture of your financial health.

This real-time view allows you to be proactive rather than reactive. You can watch your potential tax liability grow throughout the year, which means you can time asset purchases to maximise capital allowances or make pension contributions when profits are looking strong. To make this work, you need to effectively reconcile bank statements and keep your records immaculate – it’s the bedrock of a reliable set of accounts.

Think of your accounting software as a strategic dashboard, not just a digital filing cabinet. With live data, you can forecast cash flow, track profitability, and spot tax-saving opportunities well before the filing deadline looms.

This proactive approach is essential when you consider the sheer scale of UK business taxes. For 2024 to 2025, total corporation tax receipts are forecast to hit a staggering £97.2 billion. Yet within that, businesses successfully claimed an impressive £157.2 billion in capital allowances. Although this figure dipped slightly after the super-deduction ended, claims for the Annual Investment Allowance shot up by 73% to £20.8 billion, proving just how vital proactive investment is as a tax strategy. You can dig into the full Corporation Tax statistics on GOV.UK.

Ultimately, organised records create a crystal-clear audit trail. It proves that every expense you’ve claimed was legitimate and every figure you’ve reported was accurate. That's true peace of mind.

Knowing When to Call in a Professional

As brilliant as modern software is, it’s no substitute for human expertise. There’s a tipping point in every business’s journey where hiring a professional advisor, like a Chartered Accountant, stops being a cost and becomes a high-return investment.

So, when is it time to pick up the phone?

- Your business structure is changing. Moving from a sole trader to a limited company opens up a whole new world of tax and legal obligations.

- You’re hiring your first staff. Suddenly, you're dealing with payroll, PAYE, and auto-enrolment pensions. These are areas you can't afford to get wrong.

- You're planning a major investment. An accountant can help structure a large asset purchase to get the most out of reliefs like the Annual Investment Allowance.

- Your turnover is creeping towards the VAT threshold. Getting advice on the right VAT scheme and registering at the right time is crucial.

A good accountant does so much more than just file your tax return. They act as a strategic partner, offering proactive advice to help you reach your goals. They’ll spot reliefs you might have missed, offer guidance on managing cash flow, and help you map out a long-term plan for sustainable growth. Their expertise is absolutely vital for navigating the complexities of the tax system and making sure you’re seizing every opportunity to legally reduce your business taxes.

Got a Question About Business Tax? We’ve Got You Covered.

Even with the best strategies in place, the world of tax can throw up some tricky questions. Let's face it, the rules aren't always straightforward, and what works for one business might not be right for another.

Below, I’ve answered some of the most common queries I hear from business owners. Think of this as a practical FAQ to help you navigate those specific situations and make sure you're not leaving money on the table.

Can I Claim for Using My Home as an Office?

Absolutely. This is one of the first things I check with new clients. If you're a sole trader or a limited company director regularly working from home, you should be claiming a portion of your household running costs.

HMRC gives you two ways to do this:

- The Simple Way (Flat Rate): This is a no-fuss option. You can claim a fixed monthly amount based on how many hours you work from home. It's quick, easy, and doesn't require digging through bills.

- The Actual Cost Method: This route takes a bit more effort but often leads to a much bigger tax deduction. It involves calculating the business use of your home. You'd work out what percentage of your home is used for work (e.g., one room out of ten) and then claim that portion of your actual bills – think council tax, mortgage interest, gas, electricity, and broadband.

The key, whichever route you choose, is to be sensible and keep good records. If HMRC ever queries your claim, you need to be able to justify it.

Company Car vs Personal Car: Which is Better for Tax?

This is a classic dilemma, and for a long time, the answer was almost always to use your personal car. The tax implications of a traditional company car were just too high.

Using your own vehicle and claiming mileage is brilliantly simple. Your company can pay you 45p per mile for the first 10,000 business miles (and 25p after that for 2024/25). The company gets to deduct this as an expense, and you receive the money completely tax-free. It’s a clean, efficient win-win.

But things have changed. The rise of electric vehicles has completely shaken this up.

The game-changer is the incredibly low "Benefit in Kind" (BIK) tax rates on fully electric cars. This has made them a hugely tax-efficient option as a company vehicle, especially for business owners who cover a lot of miles.

The only way to know for sure is to do the maths. You need to weigh up the tax-free cash from the mileage allowance against the total running costs and tax implications of putting a specific car through the business.

What’s the Biggest Tax Mistake You See Businesses Make?

Honestly? It's not some complex, technical error. It's simply bad record-keeping.

I see so many businesses miss out on claiming thousands of pounds in legitimate expenses, all because they didn't log them properly. A lost receipt for a supplier meeting, an unrecorded train journey, forgetting to track home office costs – it all adds up. Every time you fail to claim a real business expense, you're willingly paying more tax than you need to.

Another massive own-goal is mixing business and personal finances. The first piece of advice for any new business should be to open a separate business bank account. It keeps your records clean, makes your accountant's life easier, and ensures no genuine expenses get lost in a sea of personal transactions.

Ultimately, the costliest mistake is waiting until the last minute. Tax planning isn't something you do the week before your return is due. It's an ongoing, proactive process.

At Stewart Accounting Services, our job is to be proactive for you. We partner with our clients all year round, providing strategic advice to make sure you’re using every relief you're entitled to. Explore our accounting and tax services to see how we can help your business thrive.