Effective tax planning isn't about some secret handshake or finding obscure loopholes. It's simply about being smart and deliberate with how you organise your finances to run a more efficient, profitable business. This means making conscious choices about your company structure, how you pay yourself, and where you invest, all with the goal of legally reducing your tax bill.

Ultimately, it’s about keeping more of your hard-earned money in your pocket, where it can fuel your growth.

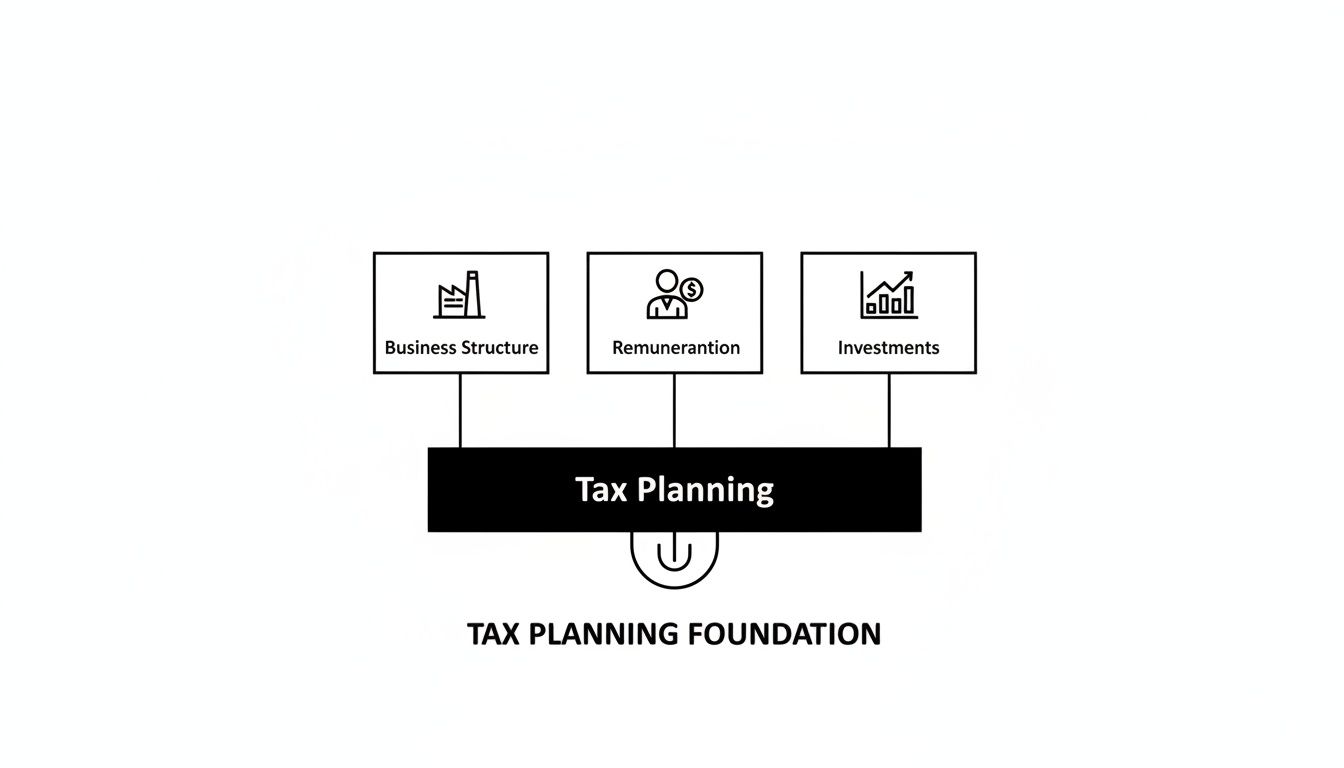

Building a Solid Financial Foundation with Smart Tax Planning

Think of your business finances like building a house. You wouldn't start pouring concrete on soft, unsteady ground, would you? The same goes for your business. Smart tax planning is the solid, reliable foundation that supports everything else you want to achieve, whether that's expanding your team or building a comfortable retirement fund.

This isn't a last-minute scramble to find receipts before the tax deadline. It's an ongoing, proactive process that transforms your tax obligations from a painful cost into a powerful tool for growth. Making the right decisions from day one can have a huge impact years down the line.

Why Planning Ahead is a Game-Changer

Getting on the front foot is crucial for navigating the UK’s ever-changing tax system. Regulations are constantly being tweaked, and waiting until the eleventh hour means you'll almost certainly miss out on valuable reliefs and add a whole lot of unnecessary stress to your plate.

The benefits of planning ahead are crystal clear:

- Boost Your Cash Flow: By legally lowering your tax payments, you keep more cash in the business. This money can be reinvested, used to cover operating costs, or set aside as a much-needed rainy-day fund.

- Minimise Financial Risk: Proper planning ensures you're always compliant with HMRC, helping you steer clear of stressful investigations and hefty penalties.

- Drive Better Business Decisions: When you truly understand your tax position, you can make much smarter choices about big-ticket purchases, hiring new staff, or funding expansion.

The government is certainly focused on its tax take. Recent statistics show UK Corporation Tax receipts are projected to hit a staggering £97.2 billion for 2024-25. This jump is largely down to policy changes like the main rate rising to 25%. For business owners, this number is a stark reminder of just how much is at stake and why tax efficiency is so critical.

When you start looking at tax through a strategic lens, you move from a position of simple obligation to one of genuine control. It’s about making your money work smarter for you, not just harder, to build a truly resilient and profitable company.

To get a broader view of the different methods available, you can explore these comprehensive tax planning strategies. A well-laid financial foundation doesn’t just help your business survive; it gives it the platform it needs to truly thrive.

Choosing the Right Business Structure for Tax Efficiency

The single biggest decision you'll make for your long-term tax bill is your business's legal structure. It’s the very foundation of any smart tax plan, defining not just how you're taxed, but also the personal risk you're taking on and the sheer amount of paperwork you'll face.

Getting this right from day one can save you a world of pain later. Each setup—sole trader, partnership, or limited company—interacts with HMRC in a completely different way. What’s perfect for a freelance copywriter could be a terrible fit for a growing construction firm.

Understanding the Sole Trader Route

Starting as a sole trader is the most straightforward path. Legally, you and your business are one and the same. This is great because all the profits are yours. The flip side? All the debts and liabilities are yours, too, which puts your personal assets on the line.

Tax-wise, it's very direct. You pay Income Tax and National Insurance on your business profits through your annual Self Assessment tax return. There are no complex company accounts, making it a go-to choice for freelancers and small, local businesses.

The Partnership Path

A partnership is much like being a sole trader, but with two or more people in the mix. The business profits are split between the partners, and each partner then settles up with HMRC for their share through their own Self Assessment.

Just like with a sole trader, a standard partnership comes with unlimited liability. This means each partner is personally on the hook for all the business's debts—even those run up by another partner. That shared risk is a massive point to consider before you shake hands on it.

Your business structure isn't just a box to tick on a form; it's the engine that drives your tax efficiency. Get it right, and you control how money and tax flow. Get it wrong, and you could easily end up overpaying and taking on needless personal risk.

The Limited Company Advantage

Setting up a limited company creates a completely separate legal entity from you, the owner. This separation is the game-changer. It provides limited liability, which means your personal assets, like your house, are shielded if the business gets into financial trouble.

This separation transforms how you're taxed. The company itself pays Corporation Tax on its profits. After that, you decide how to extract money, usually through a small, efficient salary and dividends. These are taxed separately on your personal tax return, and this two-step process opens up a huge number of tax planning opportunities. For a deep dive into this, our guide on choosing between a sole trader and a limited company is a fantastic starting point.

This diagram shows how your business structure isn't just one piece of the puzzle; it's the foundational pillar that supports everything else—from how you pay yourself to the investments you make.

As you can see, your choice of legal structure directly influences every other part of your financial and tax strategy.

Business Structure Tax at a Glance

To help you compare, here’s a quick rundown of the main differences between the three main structures.

| Feature | Sole Trader | Partnership | Limited Company |

|---|---|---|---|

| Owner's Liability | Unlimited – personal assets are at risk. | Unlimited – partners are jointly and severally liable. | Limited – personal assets are protected. |

| How Profits Are Taxed | Profits are taxed as personal income via Self Assessment. | Each partner pays personal income tax on their share of profits. | The company pays Corporation Tax; owners are taxed on salary/dividends. |

| Tax Rates | Income Tax rates (20%, 40%, 45%) + National Insurance. | Each partner pays Income Tax + National Insurance on their share. | Corporation Tax on profits, then Income Tax + NI on salary/dividends. |

| Admin & Compliance | Simple. Just an annual Self Assessment tax return. | Moderately simple. Partnership and individual Self Assessments. | More complex. Requires annual accounts, confirmation statements, and a company tax return. |

This table shows that while being a sole trader is simpler, a limited company offers a crucial layer of financial protection and more sophisticated ways to manage your tax.

So, which one is for you? Here's a quick guide:

- Go for Sole Trader if: You're just starting out, freelancing, or running a low-risk business and want to keep things simple.

- Consider a Partnership if: You're launching a business with someone else and are both comfortable with the shared, unlimited liability.

- Choose a Limited Company if: Protecting your personal assets is a priority, you're planning to grow, and you want the most flexibility for tax-efficient planning.

As your business scales up, the tax advantages of operating as a limited company often become much clearer, giving you more strategic options for how you take money out and reinvest for the future. Making the right call now ensures you're building on a solid, secure, and tax-efficient foundation.

Optimising How You Pay Yourself from Your Business

Setting up the right business structure is just the first hurdle. The next, and arguably more crucial, decision is how you take money out of the company. For directors of limited companies, this isn't as simple as just dipping into the cash till. A smart, strategic approach to your remuneration can make a huge difference to your personal tax bill.

The most common and tax-savvy method is to blend a small salary with dividend payments. It’s a bit like mixing a perfect cocktail – the salary is a small but vital ingredient, while the dividends provide the real substance. This combination is all about maximising your take-home pay while minimising what you hand over to HMRC.

The Smart Salary and Dividend Mix

The real genius of this strategy lies in how salaries and dividends are treated differently by the taxman. A salary is a business expense, which means it reduces your company's profit and, in turn, its Corporation Tax bill. But the catch is that both you and your company have to pay National Insurance Contributions (NICs) on it.

Dividends, on the other hand, are paid out from profits after Corporation Tax has been settled. The big win here is that dividends are completely free from National Insurance, making them a much more efficient way to extract the bulk of your earnings.

The game is to find the "sweet spot" for your salary. Typically, you want to set it just high enough to qualify you for state benefits like the State Pension, but low enough that you don't start racking up significant Income Tax or National Insurance bills. For most directors, this means paying themselves a salary right up to the National Insurance Primary Threshold.

A carefully set salary acts as a key, unlocking future state benefits without costing you a fortune in tax today. By keeping it low, you treat it as a functional tool rather than your main income source, letting tax-efficient dividends do the heavy lifting.

This simple move ensures you’re building your National Insurance record for retirement while taking the rest of your income in a way that can save you thousands in NICs every single year. You can dive deeper into the specific numbers in our guide covering the salary versus dividends debate.

Practical Remuneration Scenarios

Let's put this into practice with a couple of real-world examples. For simplicity, we’ll assume the director is the only employee and the company has no other costs.

Example 1: Company Profit of £60,000

- Salary: £12,570 (matching the Personal Allowance and NI threshold for 2024/25). This means no Income Tax or National Insurance is due.

- Corporation Tax: The salary is deducted from the profit (£60,000 – £12,570 = £47,430). Corporation Tax at 19% on this remaining profit is £9,011.70.

- Available for Dividends: The leftover profit is £38,418.30.

- Personal Tax on Dividends:

- The first £500 is tax-free.

- The remaining £37,918.30 is taxed at the basic dividend rate of 8.75%, leaving a personal tax bill of £3,317.85.

- Total Tax Paid: £9,011.70 (Corporation Tax) + £3,317.85 (Personal Tax) = £12,329.55.

Example 2: Company Profit of £100,000

- Salary: £12,570 (again, no tax or NI).

- Corporation Tax: The profit after salary is £87,430. Corporation Tax (now a mix of the 19% and 25% rates) comes to £18,107.50.

- Available for Dividends: The remaining profit is £69,322.50.

- Personal Tax on Dividends: The director has already used their personal allowance on the salary.

- First £500 is tax-free.

- £37,200 is taxed at 8.75% = £3,255.

- The remaining £31,622.50 falls into the higher rate band and is taxed at 33.75% = £10,672.34.

- Total Tax Paid: £18,107.50 (CT) + £13,927.34 (Personal Tax) = £32,034.84.

As you can see, this structured approach allows you to calculate and manage your total tax liability with precision, making sure as much of your hard-earned profit stays in your pocket as legally possible.

Getting Smart With Key Tax Reliefs and Allowances

Once you've sorted your business structure and how you'll pay yourself, the next level of smart tax planning is to make active use of the reliefs and allowances HMRC offers. These aren't sneaky loopholes; they're government incentives designed to encourage you to plough money back into your business. When you understand them, you can start turning a tax bill into a strategic opportunity for growth.

Think of these reliefs as powerful tools in your financial toolbox. Instead of just accepting a tax bill based on your raw profit, you can use these tools to lower that taxable figure by spending on things that make your business stronger, more innovative, and more efficient. It’s a classic win-win: your company gets better, and your Corporation Tax bill gets smaller.

Capital Allowances and the Annual Investment Allowance

For any business that buys physical assets, Capital Allowances are one of the most valuable tools going. When you buy things that last—like machinery, computer equipment, or vans—you can't just knock the full cost off your profits in one go. Instead, you claim capital allowances, which let you write off the value of the asset over its useful life.

The real star of the show here is the Annual Investment Allowance (AIA). This fantastic allowance lets you deduct 100% of the cost of qualifying plant and machinery in the year you buy it, up to a massive limit (currently £1 million). It's a huge tax planning opportunity.

Let’s put it into practice. Imagine your company is heading for a taxable profit of £150,000. Before your year-end, you decide to invest £50,000 in new manufacturing equipment.

- Without the AIA: You’d pay Corporation Tax on the full £150,000 profit.

- With the AIA: You can deduct the entire £50,000 cost from your profit. Your taxable profit instantly drops to £100,000.

Just like that, a single, strategic purchase slashes your Corporation Tax bill, freeing up cash you can put to work elsewhere. This is why timing your big purchases is such a core part of effective tax planning.

Rewarding Innovation with R&D Tax Credits

Does your business try to create new products, improve processes, or develop new services? If you’re spending money to overcome a scientific or technological challenge, you could be eligible for Research and Development (R&D) tax credits. This is one of the most generous reliefs out there, specifically designed to reward innovative UK companies.

And it’s not just for scientists in white lab coats. R&D happens in all sorts of industries, from software development and engineering to food manufacturing and construction.

The relief works by letting you deduct an extra percentage of your qualifying R&D spending from your profit, on top of the 100% you've already accounted for. If your company is loss-making, you can even trade the relief for a cash payment from HMRC—a genuine cash injection when you need it most. So many businesses miss out simply because they don't realise their everyday problem-solving counts as R&D.

Think of tax reliefs not as a discount on your final bill, but as the government co-investing in your success. When you spend on new equipment or innovation, HMRC chips in by reducing the tax you owe, making your growth plans more affordable.

To keep on top of this, dedicated expense management software can be a lifesaver. It helps ensure you have the clean, accurate records needed to successfully claim for reliefs like the AIA or R&D tax credits.

Pension Contributions: A Superb Tax Extraction Tool

Making pension contributions is another incredibly tax-efficient move, especially for directors of limited companies. When your company pays money directly into your personal pension, it’s treated as an allowable business expense.

This creates a powerful double-whammy:

- It Lowers Your Corporation Tax: The entire contribution is deducted from your company's profits before the taxman comes knocking.

- There’s No Personal Tax or NI: Unlike a salary or dividend, the pension contribution is not subject to Income Tax or National Insurance for you or the business.

It’s a brilliant way to shift significant value from the company's bank account straight into your retirement pot without any tax leakage along the way. The funds then get to grow in a tax-sheltered environment.

You get to plan for your future while managing your company's current tax bill at the same time. For a deeper dive, check out our guide on the various reliefs and allowances for Corporation Tax purposes. By using these reliefs intelligently, you can transform your tax return from a simple compliance task into a dynamic plan for business growth and personal wealth.

Getting to Grips with VAT, Payroll, and Employment Taxes

Let’s be honest, day-to-day operational taxes like VAT and payroll can feel like a relentless chore. But seeing them as just a compliance headache is a missed opportunity. When you get smart about managing them, they stop being a reactive task and become a predictable part of your financial rhythm, which is fantastic for your cash flow.

For a lot of businesses on the up, the first big tax hurdle they encounter is Value Added Tax (VAT). The moment your taxable turnover crosses the £90,000 threshold in any 12-month period, you’re legally required to register. The key here is to be proactive – getting this sorted before you’re forced to means you avoid any awkward and expensive penalties from HMRC.

Once you’re in the VAT club, you'll start adding VAT to your sales and, on the flip side, you can reclaim the VAT you spend on business purchases. This does mean a bit more admin, but it’s not all take and no give.

Choosing a VAT Scheme That Works for You

Not all VAT schemes are the same, and picking the right one can make a huge difference to your cash flow and cut down on your paperwork. Under the standard scheme, you owe VAT to HMRC based on the date of your invoices, not when you get paid. This can leave you out of pocket, paying tax on money that hasn't even hit your account yet.

Thankfully, there are better options for many smaller businesses:

- Cash Accounting Scheme: This is a game-changer. You only account for VAT when you actually receive payment from a customer or pay a supplier. It’s a simple, brilliant way to protect your cash flow because you never pay VAT on income you don't have.

- Flat Rate Scheme: If you want to simplify things, this could be for you. You pay a single, fixed percentage of your turnover to HMRC, but you generally can’t reclaim VAT on your purchases. It’s designed to slash the administrative burden for smaller businesses.

Navigating the World of Payroll

Running a payroll is another area where a bit of foresight goes a long way. It's not just a case of paying salaries; you're also juggling Pay As You Earn (PAYE) income tax, National Insurance Contributions (NICs), and auto-enrolment for workplace pensions. Each piece of that puzzle needs to be calculated correctly and reported to HMRC on time.

This is where modern cloud accounting software like Xero really shines. It can handle most of the heavy lifting by automating calculations, creating payslips, and filing the necessary Real Time Information (RTI) reports with HMRC. Using these tools drastically reduces the risk of costly mistakes and saves you from drowning in spreadsheets.

Looking ahead, keeping an eye on employment costs is vital. Employers are facing a significant pinch as National Insurance rates for them rise while thresholds are lowered. This double-whammy is one of the biggest shifts in employment tax we’ve seen in years, making it more critical than ever to plan your payroll costs strategically. You can read up on the latest tax considerations for the upcoming fiscal year on pricebailey.co.uk.

Efficiently managing payroll and VAT isn't just about ticking boxes for HMRC. It's about building a robust financial engine for your business that protects your cash flow and ensures you are never caught out by unexpected liabilities.

Ultimately, keeping a firm grip on these operational taxes is about more than just avoiding fines. It gives you a clear, up-to-the-minute view of what you owe, so there are no nasty surprises. By choosing the right schemes and using the best tools, you can transform what feels like a burden into a smooth, manageable, and predictable part of running your business.

Putting Your Tax Plan into Action with a Proactive Partner

A brilliant tax strategy is worthless if it just sits in a folder. The final, and arguably most important, step in tax planning for business owners is actually doing it—turning those smart ideas into consistent actions that protect your hard-earned cash.

This is all about shifting your mindset. Instead of a mad scramble once a year when the tax deadline looms, think of it as an ongoing, proactive process.

The bedrock of any good plan is solid, meticulous record-keeping. Without clean, up-to-date books, you're essentially flying blind. It's impossible to accurately forecast profits, time your investments, or spot when you’re creeping up to a critical threshold like the VAT registration limit.

This is where getting the right tools in place makes all the difference.

Embracing Technology for Real-Time Clarity

Cloud accounting software is the engine room of modern tax planning. A platform like Xero gives you a live, real-time dashboard showing the financial health of your business. It automates a huge chunk of the bookkeeping that used to eat up hours of your time.

This dashboard from Xero’s UK site shows just how clear your financial data can be, offering an at-a-glance view of your cash flow and who owes you money.

With that kind of clarity, you and your accountant can see your potential Corporation Tax bill building throughout the year. It means you can make strategic moves with confidence, not guesswork.

Having your finger on the financial pulse empowers you to act decisively. You can see when cash flow is strong enough to finally buy that big piece of equipment, or when it’s the perfect moment to make a chunky pension contribution to lower your taxable profit. It turns tax planning from a look in the rearview mirror into a forward-looking strategy.

Knowing When to Call in a Professional

While the right software is a game-changer, it doesn’t replace expert human guidance. There are certain milestones in your business journey that should be a clear signal: it’s time to get a good accountant on your side for strategic advice, not just compliance.

Here are a few key triggers:

- Getting close to the VAT threshold: An accountant can walk you through the best scheme for your business and make sure the registration process is handled smoothly.

- Hiring your first employee: This suddenly brings a world of payroll complexity—PAYE, National Insurance, pension auto-enrolment—that has to be perfect from day one.

- Thinking about a major capital investment: An expert can help you get the most out of reliefs like the Annual Investment Allowance.

- Planning for big growth or your exit: If you're looking to expand or eventually sell, strategic financial structuring is absolutely vital.

Partnering with an accountant isn't an admission that you can't handle your finances. It's a strategic decision to gain a specialist partner who will save you time, reduce your tax bill, and provide the peace of mind needed to focus on growing your business.

This partnership is the final piece of the puzzle. It combines your vision for the business with an expert’s technical knowledge, ensuring your tax plan isn't just well-designed, but flawlessly executed, year after year.

Got Questions About Business Tax Planning?

Even the best-laid plans can bring up a few questions. Let's tackle some of the most common queries I hear from UK business owners, with clear, straightforward answers.

When Should I Really Start Planning My Taxes?

Honestly? Yesterday. But today is the next best thing. Effective tax planning isn’t a frantic dash to the finish line in March; it’s a continuous process, woven into the fabric of your business year.

Think of it as an ongoing conversation about your finances. By keeping an eye on things month by month, you can make savvy moves, like timing a big equipment purchase to get the most tax relief or deciding the best moment to take a dividend. This forward-thinking approach means no nasty surprises and keeps you in control.

Can I Claim for Using My Home as an Office?

Yes, you certainly can. If you're a sole trader, you have a couple of options: either use HMRC's simplified flat rate or work out the actual proportion of your home running costs (like electricity and heating) that relate to your business.

For limited company directors, the rules are a bit different. You can claim a straightforward £6 per week without needing any receipts. If your costs are higher, your company can set up a formal rental agreement to pay you for the space, which could allow for a larger claim. It's always a good idea to chat this through with your accountant to see which route is best for you.

Cloud accounting gives you a live dashboard of your business's financial health. It turns tax planning from a reactive chore into a proactive strategy, letting you see your liabilities build in real-time and make smarter decisions.

How Does Cloud Accounting Actually Help with Tax Planning?

This is where things get really clever. Cloud accounting software, like the popular platform Xero, gives you a real-time, accurate picture of your business's finances. It handles much of the bookkeeping grunt work and churns out reports that let you and your accountant see exactly where you stand.

Imagine being able to watch your potential Corporation Tax bill grow throughout the year. It's powerful stuff. This visibility allows you to make timely decisions—like bringing forward an investment in new kit or making an extra pension contribution—to manage your tax bill before it becomes a problem. You're no longer guessing; you're planning with confidence.

Are you ready to stop reacting to tax bills and start building a proactive strategy? The expert team at Stewart Accounting Services can provide the clarity and guidance you need. Book a consultation with us today and gain the freedom of having more time, more money, and complete peace of mind.