So, you’re running a limited company and wondering what you should be paying for an accountant. It’s one of the most common questions we get, and the truth is, there’s no single price tag.

Generally, you can expect to pay anywhere from £75 to £250 per month for accounting services in the UK. On an annual basis, that works out to about £900 for the bare-bones compliance essentials, rising to £3,000 or more if you need a more hands-on, all-inclusive service.

What Accountant Fees Should Your Limited Company Expect?

Trying to budget for an accountant can feel a bit like guesswork, but it doesn't have to be. The key is to understand what's behind the price. These fees aren't just plucked out of thin air; they reflect the expertise and time required to keep your company financially healthy and compliant. Think of it less as a cost and more as an investment in a financial partner who has your back.

For most small business owners, this is a non-negotiable part of the budget. It’s what keeps you on the right side of HMRC and frees you up to do what you do best—run your business. The workload can be particularly heavy for busy EOFY accountants, and that year-end rush often makes up a significant part of the annual fee.

To give you a clearer picture, let's break down the costs into a simple table. This shows what you might expect to pay based on your company's size and needs.

Typical UK Accountant Fee Ranges for a Limited Company

| Service Level | Typical Annual Cost | Typical Monthly Cost | Best For |

|---|---|---|---|

| Basic Compliance | £900 – £1,500 | £75 – £125 | Start-ups and micro-entities needing just year-end accounts and tax returns. |

| Standard Service | £1,500 – £3,000 | £125 – £250 | Growing businesses that need bookkeeping, VAT returns, and payroll on top of compliance. |

| Full Service / Pro | £3,000+ | £250+ | Established businesses looking for strategic advice, management accounts, and tax planning. |

As you can see, the more your business grows and the more complex its finances become, the more support you'll need.

Why Do the Costs Vary So Much?

It really boils down to what you need. Most accountants bundle their services into packages, which makes your monthly outgoings predictable.

- A Basic Compliance Package is your starter-for-ten. It’s designed for small companies that just need to tick the legal boxes with HMRC and Companies House.

- An All-Inclusive Growth Package is for businesses that are more established. This goes beyond the basics to include things like bookkeeping, payroll, and regular management accounts to help you make smarter decisions.

The bottom line is simple: as your business scales up, so does the accounting work. The fees reflect that, ensuring you only pay for what you need at your current stage.

Industry-wide, the figures can vary quite a bit. You might find a minimal compliance-only service for as little as £500 a year, while a company needing in-depth strategic support could pay upwards of £6,000. Most small limited companies land somewhere between £500 and £1,200 annually for the foundational stuff like year-end accounts and Corporation Tax returns. If you want the full works—bookkeeping, payroll, management accounts, and proactive tax planning—you should budget for £2,400 to £6,000 or more each year. You can learn more about what you should really expect to pay.

Here at Stewart Accounting Services, we believe in being upfront and clear. We offer fixed-fee packages designed around your specific business needs, so you’ll never get an unexpected bill. We’re here to help businesses across Central Scotland and the rest of the UK find a solution that fits their budget and helps them grow.

Decoding The Services Your Accountant Fees Cover

When you get a quote from an accountant, it's easy to just scan the list of services and jump straight to the price. But what are you actually paying for? The key is to stop seeing your accountant as a business cost and start seeing them as a crucial part of your company's support system.

Think of it like building a house. Some services are the legal foundations—the non-negotiables that keep everything standing. Others are the internal wiring and plumbing that make it a comfortable, functional place to be. Each piece plays a specific role in keeping your limited company compliant, efficient, and financially sound.

Let's break down the core components.

Year-End Accounts and Corporation Tax

This is the big one—the absolute cornerstone of your legal duties as a limited company director. Once your financial year closes, your accountant gets to work preparing a detailed report on your company's performance. This is what gets sent to Companies House. They’ll also calculate exactly how much Corporation Tax you owe and file the return (known as a CT600) with HMRC.

These aren't just admin tasks. They are a legal requirement, and getting them wrong can bring on some serious, and seriously unwanted, penalties from the authorities.

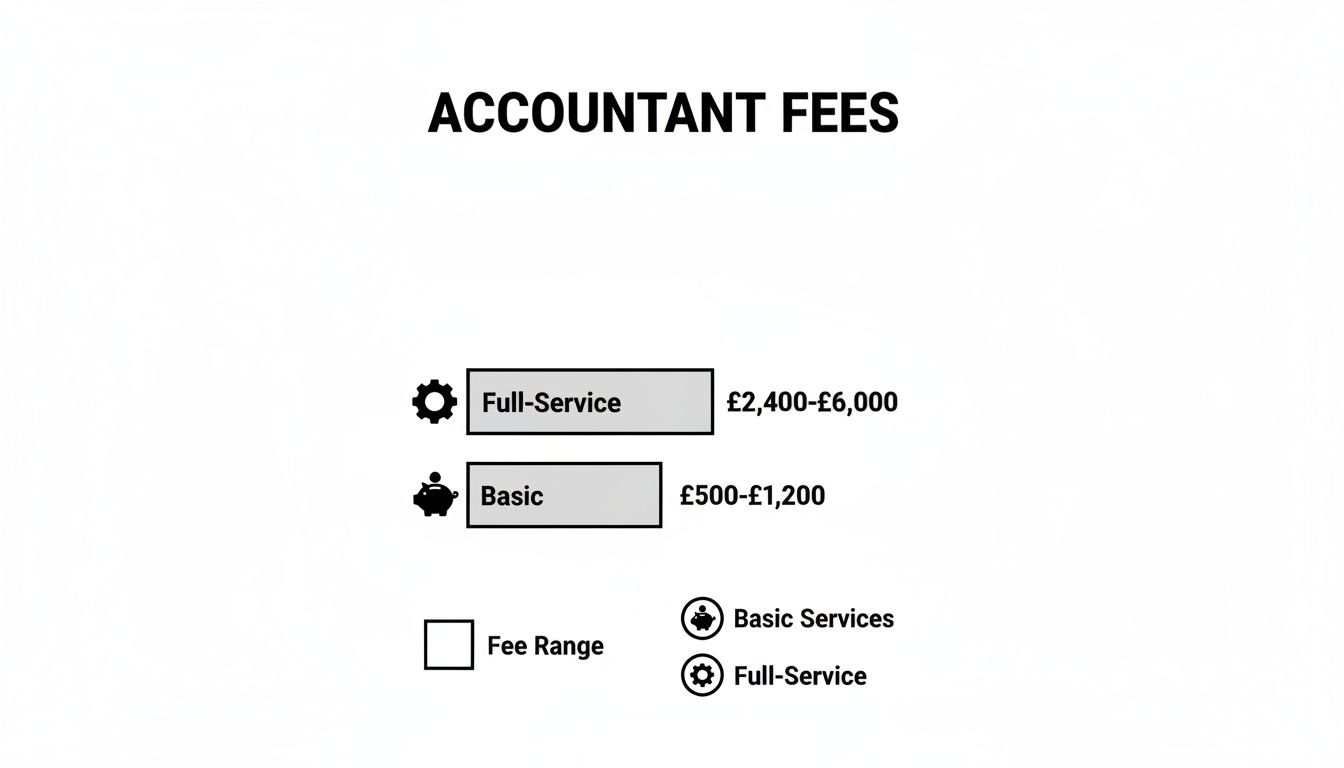

The image below gives you a rough idea of the annual cost for basic compliance versus a more hands-on, full-service package.

As you can see, there’s a noticeable jump in cost when you move from the essentials to a full package. That difference reflects the value of having an expert on hand throughout the year, not just at the finish line.

For just these fundamental year-end and Corporation Tax services, most small limited companies should budget for somewhere between £750 and £2,000 a year. That fee will climb if your finances are a bit more complicated—think significant assets, complex investments, or multiple streams of income—as the work involved naturally increases.

Bookkeeping

If year-end accounts are the annual MOT for your business, then bookkeeping is the regular servicing that keeps the engine running smoothly. This is the day-to-day, meticulous recording of every single financial transaction: every sale, every purchase, every expense, every payment in and out.

Good bookkeeping isn't just about keeping records. It’s about building a clear, accurate story of your company's financial life. This data is the bedrock of every smart business decision you'll make, from setting budgets to applying for a loan.

Without clean, up-to-date books, preparing your year-end accounts becomes a nightmare. It’s a messy, time-consuming, and expensive puzzle to solve, which is precisely why so many accountants bundle bookkeeping into their monthly packages.

Payroll and VAT Returns

As your business grows, you’ll inevitably hit two major milestones: hiring your first employee and crossing the VAT threshold. Both bring fresh layers of complexity.

- Payroll: This is all about making sure your team gets paid correctly and on time. It involves calculating tax and National Insurance, handling pension auto-enrolment, and filing all the right reports with HMRC. It's a minefield of rules and deadlines.

- VAT Returns: Once you're VAT-registered, you have to submit regular returns to HMRC. This means calculating the VAT you've charged on sales and offsetting it against the VAT you can reclaim on your business purchases.

An accountant takes the headache out of both. They navigate the tricky regulations and strict submission dates, saving you a huge amount of time and preventing costly errors.

When you start to understand what goes into each of these components, the accountant fees for a limited company start to feel less like a bill and more like a smart investment in your business's health. To get a fuller picture, you can explore the wide range of services an accountant can provide to help your company thrive.

What Really Drives the Cost of Your Accountant's Bill?

Ever looked at an accountant's quote and wondered how they landed on that exact number? Or why a friend with a similar business pays a completely different amount? It's not a dark art; the price is a direct reflection of the time, skill, and sheer effort needed to get your company’s finances in perfect order.

The biggest factors are usually your annual turnover and the sheer volume of transactions you process. Think about it this way: a local coffee shop with maybe 50 transactions a day is a world away from an e-commerce store shipping 500 orders daily. More sales, more purchases, more bank entries—it all adds up to more work for your accountant to sort through, check, and reconcile.

The State of Your Bookkeeping

This is the one area where you have the most direct control over your costs. Picture this: you hand your accountant a shoebox overflowing with crumpled receipts, unsorted invoices, and scribbled notes. Before they can even start on your accounts, they have to become a financial detective, spending hours piecing together the puzzle of your business year. That investigative work is billable, and it can seriously inflate your final invoice.

Now, imagine the opposite. You're using modern accounting software, your bank feed is connected, and your records are clean and up-to-date. Your accountant can log in, find what they need, and get straight to work. A key part of managing these costs is understanding how to calculate operating expense, as well-tracked expenses make your accountant's job much easier.

A well-organised set of books is the single most effective way to reduce your accountant fees. Clean records mean less manual work for your accountant, which translates directly into lower costs for you. It’s a simple equation with a powerful impact on your bottom line.

Using the right tools makes a massive difference. Learning about cloud accounting for your small business is the first step toward turning that shoebox chaos into a streamlined system that saves everyone time and money.

Other Critical Cost Drivers

Beyond the basics of transaction volume and bookkeeping quality, several other factors can add layers of complexity—and cost—to your accounting. Each of these requires more time, specialist knowledge, or both.

Here’s what else moves the needle on your quote:

- Number of Employees: Running payroll for a couple of people is one thing. Doing it for 20 staff members with different hours, pension schemes, and commissions is a much bigger, more intricate job.

- VAT Registration: Being VAT-registered means regular, deadline-driven VAT returns. This adds a recurring compliance task to your accountant's plate.

- Industry-Specific Rules: Some sectors have their own financial hurdles. If you're in construction (with CIS rules) or finance (FCA regulations), your accountant needs specialist expertise to keep you compliant.

- International Transactions: As soon as you start dealing with different currencies, overseas suppliers, or international customers, things get more complicated with foreign exchange rates and extra reporting.

When you see how these different elements come together, the way your accountant fees for a limited company are built starts to make sense. Better yet, it shows you exactly where better organisation on your part can lead to very real savings.

Fixed Fees vs. Hourly Rates: Which Pricing Model is Right for You?

When you’re looking for an accountant, you’re not just hiring someone to crunch the numbers; you’re choosing a financial partner. A big part of that choice comes down to how they charge for their work, as this can shape your entire relationship and, of course, your cash flow. You’ll generally come across two main ways accountants bill: a fixed monthly fee or a classic pay-as-you-go hourly rate.

Getting your head around the difference is key to managing your accountant fees for a limited company. Think of it like a mobile phone contract: do you want a predictable monthly plan with everything included, or would you rather pay for every single minute you use?

The Fixed Monthly Fee Model

These days, most forward-thinking accountancy firms have moved towards a fixed monthly fee, and it’s easy to see why. You pay one set amount every month for a specific package of services. For any business owner trying to keep a lid on their budget, that predictability is a game-changer.

You know exactly what’s leaving your bank account and when, so there are no nasty surprises. It makes financial planning so much easier. Here at Stewart Accounting Services, this is how we love to work, as it builds a much stronger partnership.

When you're on a fixed fee, the clock isn't ticking. You can pick up the phone and ask that "quick question" without worrying you'll get an invoice for a ten-minute chat. It turns your accountant from a service you pay for into a genuine member of your team.

This approach encourages you to communicate openly and often. It makes your accountant a true advisor who's genuinely invested in helping you succeed, because the focus is on delivering real value, not just logging hours.

The Pay-As-You-Go Hourly Rate Model

The more traditional way of billing is by the hour, where you’re charged for the exact time spent working on your accounts. On the surface, it can seem fair and transparent, especially if you think you’ll only need help every now and then.

But this model has some pretty big drawbacks. The main one is the complete lack of predictability. A complicated question or a snag with your bookkeeping can send costs spiralling, leaving you with a much bigger bill than you ever budgeted for.

Worse, this uncertainty often makes business owners hesitate to call for advice, scared that even a quick query will start the meter running. That lack of communication is where small issues can fester and grow into much bigger, more expensive problems down the line.

Ultimately, the best model for you comes down to what you prioritise. Do you prefer the potential for short-term savings with an hourly rate, or do you value the long-term stability and collaborative relationship that comes with a fixed monthly fee?

Seeing the Numbers in Action: Real-World Pricing Scenarios

Theory is one thing, but seeing real numbers makes budgeting a whole lot easier. To give you a clearer picture of what accountant fees for a limited company actually look like, let's walk through three common business profiles. You'll likely see a bit of your own business in one of them, which will help you estimate what your investment might be.

Think of these as financial snapshots. Each one shows how a firm like ours, Stewart Accounting Services, tailors its support to fit where a company is on its journey, from a simple start-up to a growing enterprise.

Scenario 1: The Solo IT Contractor

Let’s start with Alex. He’s a freelance IT consultant who runs his business as a one-person limited company. His setup is pretty straightforward—he works with a few big clients, has minimal overheads, and doesn’t have any employees.

For Alex, the main goal is simply to stay on the right side of HMRC and Companies House without any headaches.

- Business Snapshot: Low number of transactions, not VAT registered, and no payroll to manage.

- Services He Needs: Annual accounts, Corporation Tax return, the director’s Self-Assessment tax return, and some basic tax advice.

- Estimated Monthly Fee: £80 – £150

Alex just needs the essentials done right. His fee is for a core compliance package that delivers peace of mind, without him having to pay for extras he doesn't use.

Scenario 2: The Growing E-commerce Brand

Next up is Bloom & Co., an online shop that's really taken off in the last year. They now have two part-time employees, are VAT registered, and are juggling hundreds of sales transactions every month. The bookkeeping has become a monster they can no longer tame on their own.

- Business Snapshot: VAT registered, running payroll for two staff, and a high volume of sales transactions.

- Services They Need: Everything Alex gets, plus monthly bookkeeping, quarterly VAT returns, and full payroll management.

- Estimated Monthly Fee: £250 – £400

Bloom & Co.'s fee is higher because their day-to-day operations are much more involved. The cost covers the crucial, time-sensitive work of managing VAT and making sure their staff are paid correctly—both essential for their growth. This figure lines up with wider industry data, which shows that a VAT-registered micro-company with a couple of employees should budget £200 to £400 for a full-service package. You can see how these costs break down in more detail for a broader perspective.

Scenario 3: The Established Consulting Firm

Finally, let's look at Innovate Solutions, a consultancy with five full-time consultants on the team. Their turnover is getting close to seven figures, and the directors need more than just someone to file their accounts; they need sharp financial insights to help guide the business forward.

For a business at this level, accounting shifts from a compliance chore to a strategic tool. The goal is to use financial data to drive growth, improve profitability, and plan for the future.

- Business Snapshot: Higher turnover, multiple employees, more complex expenses, and a clear need for strategic advice.

- Services They Need: All the services from the previous scenarios, plus monthly management accounts, cash flow forecasting, and regular strategic review meetings.

- Estimated Monthly Fee: £500+

For Innovate Solutions, the fee reflects a genuine partnership. The value here isn't just in ticking boxes; it's in the proactive advice that helps the directors make smarter, data-driven decisions to keep the company thriving.

To make these comparisons even clearer, here's a table that lays it all out.

Accountant Fee Scenarios by Company Type

| Company Profile | Key Characteristics | Included Services | Estimated Monthly Fee |

|---|---|---|---|

| Solo Contractor | Low transaction volume, not VAT registered, no payroll. | Annual Accounts, Corporation Tax, Director's Self-Assessment, Basic Advice. | £80 – £150 |

| Growing E-commerce | VAT registered, 2 employees, high sales volume. | All of the above, plus Monthly Bookkeeping, VAT Returns, and Payroll. | £250 – £400 |

| Established Firm | Higher turnover, 5+ employees, complex needs. | All of the above, plus Management Accounts, Forecasting, Strategic Meetings. | £500+ |

As you can see, there's no "one-size-fits-all" price. The right accountant will structure their fees around what your business actually needs to stay compliant and grow effectively.

How To Choose The Right Accountant For Your Business

Knowing what accountants charge is one thing, but finding the right financial partner for your limited company is a completely different ball game. It’s this relationship that can genuinely propel your business forward. Chasing the cheapest quote is almost always a false economy; the real win is finding an expert who delivers tangible value and actively helps you grow.

Think of it less like shopping for a service and more like hiring a key member of your team. You wouldn’t bring someone into your business without doing your homework, and the same principle applies here. First things first, check their qualifications. Look for accreditations like ‘Chartered Accountant’. This isn't just a title; it's a guarantee that they are held to the highest professional and ethical standards. It’s non-negotiable.

Look Beyond The Basics

Next, dig into their experience. Do they get your industry? An accountant who understands the ins and outs of your sector—whether that’s construction, e-commerce, or professional services—is worth their weight in gold. They’ll already know the common financial hurdles and the specific tax efficiencies you can benefit from, offering far more targeted advice than a generalist ever could.

How they handle technology is another massive clue. A modern firm, like us here at Stewart Accounting Services, will be using cloud-based tools like Xero to make life easier for everyone. This isn’t just about making things quicker; it’s about giving you access to your financial data in real-time, so you can make sharp, informed decisions on the fly.

Choosing an accountant is a long-term investment in your company’s future. The right partner provides more than compliance; they offer the strategic insight that turns financial data into a roadmap for growth.

To make sure you’re making the right call, you need to go in armed with questions that go beyond "how much?". It's also worth taking a moment to consider whether you need an accountant or could file accounts yourself, as this really helps you understand the immense value a true expert brings to the table.

Key Questions To Ask A Potential Accountant

Here’s a practical checklist to run through when you’re talking to potential accountants. It'll help you find the perfect fit.

- Communication: How often will we speak? Who’s my day-to-day contact?

- Technology: What accounting software are you experts in? How will you use it to help my business specifically?

- Strategic Advice: Beyond the tax returns, how do you actively help clients grow their business?

- Client Base: Do you work with other businesses in my industry? Can you share any (non-confidential) success stories?

- Fees: Are your prices fixed? What’s included, and what counts as an extra charge?

Your Questions Answered: A Quick Guide to Accountant Fees

When you're running a limited company, figuring out accountant fees can feel a bit like navigating a maze. To help you find your way, we've pulled together straightforward answers to the questions we hear most often from business owners.

Can I Just Do My Limited Company Accounts Myself to Save a Bit of Cash?

Technically, yes, you can. But it’s a path loaded with potential pitfalls. Limited company accounts are bound by a complex web of rules and unforgiving deadlines set by HMRC and Companies House.

Getting it wrong isn't just a minor slip-up; a single mistake could land you with penalties that far outweigh what you would have paid an accountant. Think of an expert’s fee less as a cost and more as an investment in getting things right, staying compliant, and uncovering tax savings you might have missed.

Are There Hidden Costs I Should Be Aware Of?

A reputable accountant will always be upfront about their pricing. They should provide a clear engagement letter that spells out exactly what services are covered in your fee. Here at Stewart Accounting Services, we believe in a no-surprises approach, which is why we offer fixed-fee packages.

That said, it's always smart to ask what isn't included. Services that often fall outside a standard package might include:

- Tax investigation insurance (to cover professional fees if HMRC opens an enquiry).

- Help with mortgage or loan applications.

- In-depth, specialised tax planning projects.

Getting clarity on these from the start builds a strong, honest relationship with your accountant.

How Often Should I Expect to Hear from My Accountant?

This really depends on the level of service you've chosen. If you’ve only signed up for a basic year-end accounts service, you might only speak to them once or twice a year.

However, if you're on a comprehensive monthly plan, your accountant should feel like part of your team. A proactive accountant will be in regular contact, providing management reports and being available to answer your questions as they arise. They become a true financial partner, helping you steer the ship.

Ready to get clear, straightforward accounting support and win back your time to focus on what you do best? The team at Stewart Accounting Services is here to help. Get in touch today for a friendly, no-obligation chat about your business.