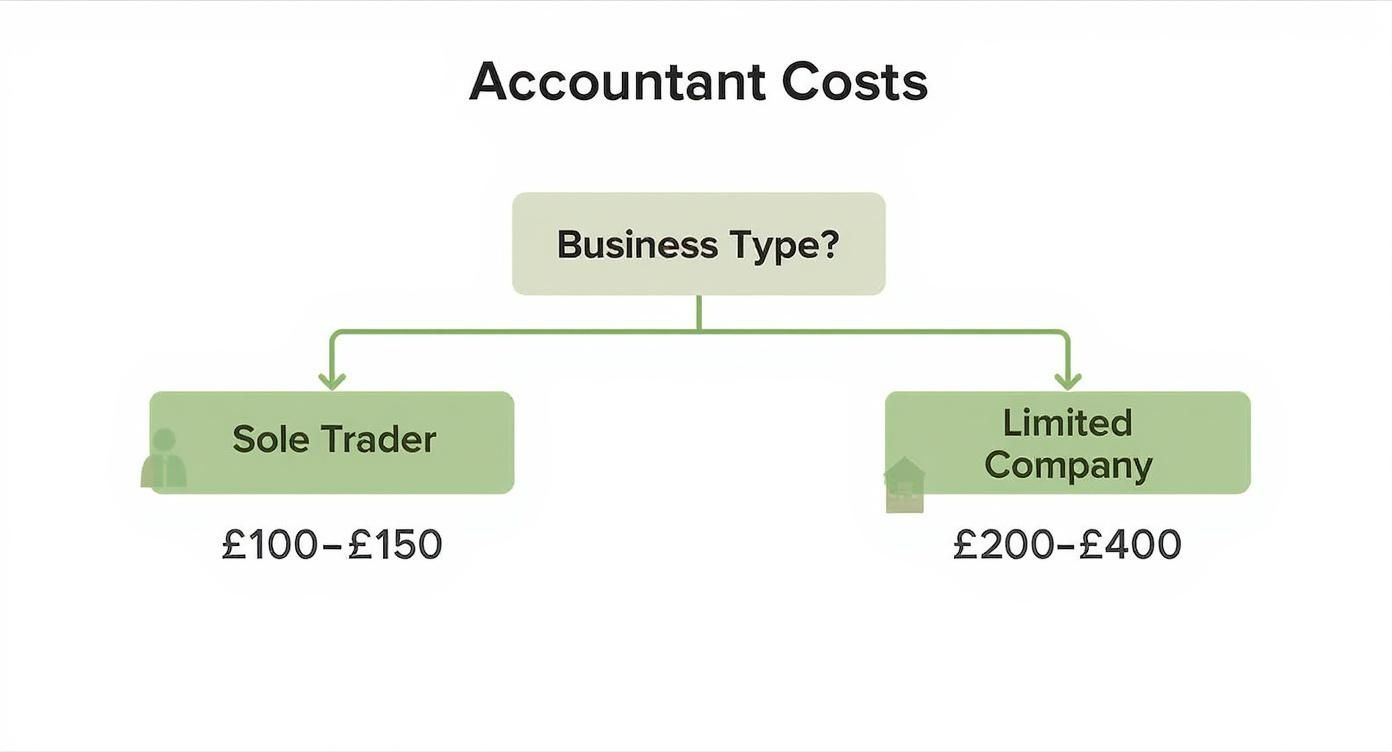

Let’s get straight to the point. If you’re a sole trader, you can expect to pay somewhere between £100 and £150 per month for an accountant in the UK. For a limited company, that figure usually jumps to £200 to £400 per month.

The difference in price all comes down to the amount of work involved for each type of business.

How Much Do Accountants Really Cost in the UK?

Trying to pin down a single price for an accountant can feel a bit like asking, "how much does a car cost?" The answer is always: it depends. A basic runaround is one thing; a high-performance sports car is another beast entirely.

It's the same with accounting. A sole trader's financial affairs are relatively straightforward. The main event is usually a single Self Assessment tax return each year. Simple, clean, and efficient.

A limited company, on the other hand, is the high-performance model. It comes with a whole host of extra legal and financial responsibilities. We’re talking Corporation Tax returns, filing annual accounts with Companies House, managing director's payroll, and often handling VAT returns. All this extra complexity and compliance work naturally means higher fees.

To give you a clearer picture, here’s a quick breakdown of what you can expect to pay based on your business setup.

Typical Monthly Accountant Fee Ranges by UK Business Type

| Business Structure | Typical Monthly Fee Range | Common Services Included |

|---|---|---|

| Sole Trader | £100 – £150 | Annual Self Assessment tax return, basic tax advice, software subscription. |

| Partnership | £150 – £250 | Partnership tax return, individual partner Self Assessments, basic advice. |

| Limited Company | £200 – £400 | Annual accounts, Corporation Tax return, director's payroll, VAT returns. |

These figures are a great starting point, but remember they're just averages. Your final quote will depend on the specifics of your business.

What Determines the Final Price?

Several moving parts influence the final quote you'll receive from an accountant. Understanding these will help you figure out what you really need and how to budget for it.

- Your Business Structure: As we've covered, a limited company has far more compliance hoops to jump through than a sole trader, and the price reflects that.

- The Level of Service: Do you just need someone to handle the year-end basics? Or are you looking for a proper financial partner who provides monthly reports, cash flow forecasting, and strategic advice? The more hands-on they are, the more it will cost.

- How Busy You Are: A business with a handful of transactions each month is much simpler to manage than one with thousands of invoices and expenses. More transactions mean more bookkeeping work.

- The State of Your Records: If your records are a mess, your accountant has to spend time untangling everything. Keeping your books clean and organised can genuinely save you money.

All in all, you could see fees as low as £30 per month for the most basic services or upwards of £400 for a more involved, all-inclusive package.

Think of your accounting fee as an investment, not just another bill. A great accountant does more than just file your taxes; they provide insights that can save you money, spot opportunities, and help you grow your business.

It can be tempting to just go for the cheapest quote you can find, but this is often a classic case of false economy. It’s vital to understand why you should be wary of cheap accountants, because what you save upfront could be lost through missed tax savings or, even worse, costly mistakes.

This guide will walk you through the different ways accountants charge, what services are worth paying for, and how to find a financial partner who adds real value to your business.

Comparing Accountant Pricing Models

Choosing an accountant is about more than just their qualifications; it’s about finding a payment structure that actually works for your business and its cash flow. Think of it like a mobile phone plan. You could opt for a pay-as-you-go deal for occasional calls, or you could get a monthly contract that bundles everything you need for one predictable price.

Accountants generally offer three main ways of charging for their services, each with its own benefits and drawbacks. Getting your head around these is the key to avoiding surprise bills and building a partnership that feels fair and valuable. The right model makes sure the accountant fees for small businesses are a manageable, expected part of your budget, not a source of stress.

This decision tree gives you a quick look at how typical monthly costs can vary depending on whether you're a sole trader or a limited company.

As you can see, limited companies often have a higher starting cost. That's simply because they have more compliance hoops to jump through than sole traders. This fundamental difference is a big factor when deciding which pricing model is the best fit.

Fixed Monthly Fees: The Modern Standard

By far the most common model you'll see these days, especially with modern, forward-thinking firms, is the fixed-fee monthly retainer. This is your "monthly contract" option, where you pay a set amount each month for a clearly defined list of services.

There’s a simple reason this approach has become so popular: predictability. You know exactly what your accounting bill will be every single month, which makes budgeting and managing your cash flow infinitely easier. No more nasty surprises or invoices for a quick five-minute phone call.

So, what’s usually included? A good fixed-fee package often covers:

- Core Compliance: Your annual accounts, Corporation Tax returns, and Self-Assessments.

- Ongoing Support: Regular bookkeeping, payroll runs, and VAT returns.

- Software Access: A subscription to cloud accounting software like Xero or QuickBooks is often part of the deal.

- Basic Advice: The freedom to pick up the phone or send an email with questions throughout the year.

This model really changes the dynamic. It turns a transactional service into a proper partnership. Your accountant is encouraged to work efficiently and be proactive because they're part of your team, not just someone you call when a deadline is looming.

Hourly Rates: For Specific, One-Off Tasks

While it’s becoming less common for day-to-day accounting, the old-school hourly rate still has its place. This is your "pay-as-you-go" option, where you're billed for the exact time your accountant spends on your work. It's typically used for one-off consultations, complex projects, or when you need an expert to help solve an urgent problem.

In the UK, the cost of hiring an accountant by the hour can be anywhere from £25 to £150. Simpler bookkeeping tasks will be at the lower end, while strategic advice or complex tax planning could easily reach £125 to £250 per hour.

An hourly rate might be the right choice for things like:

- Getting initial advice on setting up your business.

- Help with a specific HMRC enquiry or investigation.

- A one-time financial health check or business valuation.

The big downside here is the lack of predictability. A task that seems simple on the surface could uncover complexities, leading to a much larger bill than you budgeted for. It can also make you hesitant to ask for quick advice because you know the clock is always ticking.

Project-Based Pricing: For A Clearly Defined Outcome

Project-based pricing is the perfect middle ground for a single, well-defined job with a clear start and finish. Your accountant will give you a fixed quote for the entire project upfront, and that’s the price you pay, no matter how many hours it ends up taking them. It gives you the same cost certainty as a monthly fee, but for a one-off service.

You'll often see this for tasks like:

- Self-Assessment Tax Return: A fixed price to get your annual personal tax return prepared and filed.

- Company Formation: A set fee to get your limited company properly registered with Companies House.

- Business Plan Creation: A single quote for developing detailed financial forecasts needed for a bank loan.

This model is fantastic when you need expert help with a specific task but aren't quite ready to commit to a monthly retainer. It can also be a great way to "test drive" a firm before engaging them for all your ongoing work. It's crucial, however, to have a very clear scope from the beginning to avoid extra charges if the project grows.

You can learn more about the differences between ongoing and task-based financial roles in our guide comparing an accountant vs bookkeeper. For a broader perspective on how different services, including financial automation tools, are priced, it can be useful to look at examples like ResolutAI's pricing models.

What Actually Drives Your Accounting Bill?

Ever got a quote from an accountant and wondered why it was miles apart from what a friend’s business pays? The reality is, there's no standard price list for accounting. The final figure is shaped by a handful of key variables, meaning accountant fees for small businesses are as individual as the businesses themselves.

Think of it like hiring a builder. A simple patio is one price, but a two-storey extension with custom fittings is a completely different ball game. The same principle applies here. Getting to grips with these factors will help you see where the costs are coming from, budget properly, and maybe even find ways to trim your bill.

Let's pull back the curtain on what really determines the complexity—and the cost—of your accounting.

Your Business Structure

The legal setup of your business is probably the biggest single factor influencing your accounting needs. A sole trader has a much simpler path to follow than a limited company, and the price tag will reflect that difference.

- Sole Trader: This is the most straightforward structure. Your main obligation is usually the annual Self Assessment tax return. With a lower compliance burden, the fees are naturally lower.

- Limited Company: This is where things get more involved. Your accountant needs to prepare and file annual accounts with Companies House, a Corporation Tax return with HMRC, and often deal with things like director's payroll and dividends. These extra legal duties simply take more time and specialist knowledge.

At the end of the day, the more legal and financial hoops your business structure makes you jump through, the more work your accountant has to do to keep everything above board.

The Sheer Volume and Complexity of Your Transactions

Right after your business structure, the amount of financial activity you have is a massive cost driver. An accountant's time is spent processing your data, so more data means more time.

Picture two businesses. One is a freelance consultant who sends out five invoices a month. The other is a bustling e-commerce shop handling hundreds of online sales, refunds, and supplier payments every single day. It’s pretty clear the second business will need a lot more bookkeeping and reconciliation, which pushes the fee up.

It's not just about the number of transactions, either. Their complexity adds another layer. Things that can complicate the picture include:

- Multi-currency transactions if you sell overseas or buy from international suppliers.

- Project-based accounting where you need to carefully allocate costs to specific jobs.

- Handling lots of cash, which always requires meticulous and time-consuming tracking.

The State of Your Financial Records

Now, this is one factor that's completely in your hands, and it can make a huge difference to your bill. An accountant’s job becomes much quicker and easier if your records are clean, organised, and ready to go.

Handing over a shoebox stuffed with crumpled receipts and a year's worth of unsorted bank statements is an accountant's nightmare. A big chunk of their fee will just be for the time they spend sorting out the chaos before they can even start.

On the flip side, if you use good cloud accounting software, keep your books up to date, and have a clear system for everything, you're doing a lot of the heavy lifting yourself. This efficiency almost always results in lower accountant fees for small businesses. Keeping organised isn't just good admin; it's a genuine cost-saving strategy.

Industry-Specific Quirks

Some industries operate under their own special accounting rules and compliance headaches. If your business is in one of these sectors, you'll need an accountant who knows the terrain, which can affect the price.

A classic example is a construction business, which has to navigate the Construction Industry Scheme (CIS). This has its own strict rules for paying subcontractors and reporting to HMRC. Other sectors with unique needs include:

- Solicitors: Need an accountant who understands specialist client account regulations.

- Charities: Face unique reporting standards set by the Charity Commission.

- Property Landlords: Require expertise in areas like Making Tax Digital for Income Tax (MTD for ITSA) and capital gains on property.

Hiring an accountant with proven experience in your field means you're not just paying for compliance, but for valuable, relevant advice. Any extra cost is often a smart investment in getting things right the first time. Understanding these core factors will help you have a much more meaningful chat with potential accountants and truly see the value behind their quotes.

Right, so you've got a handle on the different pricing models. But what services are you actually paying for? Let's peel back the layers and look at the typical menu of services that make up the average accountant fees for small businesses.

Think of this like building a toolkit for your company's financial health. You don’t need every tool in the shed, but you absolutely need the essentials to keep things running and stay on the right side of HMRC and Companies House. Getting a clear picture of what each service involves and its likely cost is the key to creating a package that's a perfect fit for your business, without paying for things you don't need.

Here’s a practical look at the most common services on offer and what you should budget for.

The Essentials: Core Compliance Services

These are the absolute must-haves. The non-negotiables. Getting these tasks wrong can lead to some eye-watering penalties, so this is where a good accountant immediately proves their worth.

-

Year-End Accounts & Corporation Tax Return (for Limited Companies): This is the big one for any limited company. It involves preparing your statutory accounts to be filed with Companies House and submitting your CT600 Corporation Tax return to HMRC. The price tag is usually driven by the number of transactions and how well-kept your records are, typically falling between £500 to £1,500+ per year if handled as a one-off job.

-

Self Assessment Tax Return (for Sole Traders & Directors): This is the main event for sole traders, partners, and company directors each year. The fees for a Self Assessment can vary quite a bit. For a standard return in 2025, you could be looking at anything from £149 to £450. This depends on things like how many sources of income you have and the general complexity of your tax situation. You can find more detail on how accountant fees are determined on tax-wise.co.uk.

-

VAT Return Preparation & Submission: If your turnover crosses the VAT threshold (or you've registered voluntarily), you'll be submitting quarterly returns. An accountant ensures your figures are spot-on and filed on time, every time. Expect to pay somewhere in the region of £100 to £300 per quarter for this peace of mind.

Day-to-Day Support: Ongoing Operational Services

Beyond the big annual deadlines, these are the services that keep your financial engine ticking over smoothly all year round. They give you a real-time view of your finances and make sure your daily operations are all above board.

It's a classic mistake to view bookkeeping and payroll as simple administrative chores. In reality, they are the very bedrock of solid financial management. Clean, up-to-date data from these functions is what empowers an accountant to do clever tax planning and helps you make smarter business decisions.

Bookkeeping is the fundamental job of recording every single financial transaction. Unsurprisingly, the cost is directly linked to the volume of your monthly transactions.

- Basic (up to 50 transactions/month): Typically £50 – £150 per month.

- Moderate (50-150 transactions/month): Usually £150 – £300 per month.

- Complex (150+ transactions/month): Can be £300+ per month.

Payroll Management handles everything from calculating staff pay and deductions to submitting all the required information to HMRC. The price is almost always based on how many employees you have and how often you pay them.

- Director-only payroll: This is often bundled into a monthly package or costs around £15 – £25 per month.

- Small team (2-5 employees): You'll likely pay £25 – £60 per month.

- Larger team (10+ employees): Costs will probably be quoted at £5 – £7 per employee, per payslip.

This breakdown gives you a 'shopping list' of sorts. Once you identify which services your business truly needs, you can have a much more productive chat with a potential accountant and build a realistic picture of your annual spend. It’s all about being proactive to avoid any nasty surprises down the line.

How to Choose the Right Accountant for Your Business

When you're looking for an accountant, it's incredibly tempting to just go for the cheapest quote. But honestly, that's one of the biggest missteps a small business owner can make.

Think of a good accountant as a strategic partner in your business journey, not just a number-cruncher you hear from once a year. Finding the right one means looking past the price tag and focusing on what really matters: their qualifications, experience, and whether they genuinely ‘get’ your business.

The first step is actually a quick look in the mirror. You need to be brutally honest about what your business needs right now. Are you just after someone to handle the basics – filing your annual accounts and tax returns on time? Or are you looking for a more hands-on advisor who can help you forecast your cash flow, shape your business strategy, and proactively plan your taxes?

Figuring this out upfront is a game-changer. It helps you zero in on the right candidates and ask the questions that count, stopping you from either overpaying for services you don’t need or hiring someone cheap who can’t offer the strategic advice to help you grow.

Understanding Different Types of Accountants

Once you’ve got a handle on your needs, you can start looking at the different flavours of accounting support out there. They're not all the same, and the right choice often depends on your business's size and complexity.

-

Traditional High-Street Firms: You’ve probably walked past these firms in your local town centre. They’re brilliant if you value face-to-face meetings and want an accountant who is part of the local business community. The service is often very personal and built on a long-standing relationship.

-

Modern Online Accountants: These firms are built for the digital age, using cloud software to work with clients from all over the country. They’re typically tech-savvy, efficient, and often provide really competitive fixed-fee packages. Perfect if you’re comfortable managing things online and want quick, streamlined support.

-

Independent Bookkeepers: A bookkeeper is your on-the-ground support, handling the daily recording of all your financial transactions. While they won't file your final accounts or devise complex tax strategies, a great bookkeeper is worth their weight in gold. They keep your records spotless, which makes your accountant's job easier (and your bill lower!).

Many business owners get stuck wondering when to make the leap to professional help. For a closer look at this, our guide on whether you need an accountant or can file accounts yourself can help you decide.

Essential Questions to Ask a Potential Accountant

Once you've got a shortlist, it's time to have a chat. This is your chance to go beyond their polished website and see if there’s a real personality and expertise that fits with your vision for your business.

Don't be shy about asking direct, detailed questions. A quality accountant will be more than happy to show you what they know and how they can help. It's not an interrogation; it's a conversation to see if you can build a successful partnership together.

The real goal here is to find someone who speaks your language. They should be able to break down complex financial ideas into plain English, giving you the confidence to make smarter decisions.

Here are a few essential questions to get the ball rolling:

-

What are your qualifications? You’re looking for official chartered status, like ACCA (Association of Chartered Certified Accountants) or ICAEW (Institute of Chartered Accountants in England and Wales).

-

Do you have experience in my industry? An accountant who already understands the quirks of construction, e-commerce, or property is going to give you far more valuable, specific advice.

-

What accounting software do you use? Make sure they’re experts in modern cloud platforms like Xero or QuickBooks. This is non-negotiable for running an efficient business today.

-

How do you like to communicate? Find out if their style matches yours. Do they prefer quick emails, scheduled phone calls, or video meetings?

-

Who will I actually be dealing with? Will you get direct access to the partner, or will you be passed on to a junior account manager? A consistent point of contact is vital for building a strong relationship.

-

Can you walk me through your fees? Ask for a crystal-clear breakdown of what their fixed-fee packages cover and, just as importantly, what they’d bill as an extra.

For a wider perspective beyond just number crunching, checking out dedicated resources for small business can help you make a well-rounded decision. Ultimately, finding the right accountant is one of the best investments you can make, paying you back long after that first invoice is settled.

Right, let's talk about squeezing every last drop of value from your accountant.

It's all too easy to look at your accountant's bill as just another expense, another number in the 'out' column. But that's the wrong way to think about it. The best way to frame it is as an investment in your business's future. A good accountant does more than just keep you on the right side of HMRC; they actively find ways to save you money and spot opportunities, delivering a return that makes their fee look like a bargain.

Think of it this way: anyone can file your taxes. A truly great accountant, however, acts like a financial co-pilot for your business. They're not just looking in the rearview mirror at last year's numbers. They're looking ahead, helping with proactive tax planning to legally minimise what you owe long before any deadlines are even on the horizon. They can offer sharp cash flow forecasts, giving you the foresight to handle quiet periods and the confidence to double down when things are booming. That’s where the magic really happens.

It's a Partnership, Not Just a Service

To unlock this level of insight, you can't just hand over a shoebox of receipts once a year. It has to be a proper partnership. Your involvement is what elevates your accountant from a simple service provider to a genuinely trusted advisor.

So, how do you build that relationship?

First off, keep your own house in order. By using a decent cloud accounting software and keeping your records tidy, you free up your accountant's time. Instead of spending hours on tedious data entry, they can spend that time on high-level strategic thinking that directly benefits you. It's a simple case of helping them help you.

Next, talk to them! Don't just save up all your questions for the mad rush at year-end.

Let your accountant know what's on your mind. Are you thinking about hiring your first employee? Planning a big equipment purchase? Eyeing up a new market? The more they know about your ambitions, the more their advice will be perfectly tuned to help you get there.

Ultimately, if there's one thing to take away, it's that the right accountant is a crucial part of your success story. They bring the financial clarity and strategic guidance that underpins real, sustainable growth. When you find that person, you'll find the accountant fees for small businesses are no longer an expense, but one of the smartest investments you'll ever make.

Answering Your Top Questions About Accountant Fees

When you're trying to figure out accountant fees, a few questions always seem to pop up. Let's tackle some of the most common ones we hear from business owners, so you can feel confident about getting the right financial support.

Can I Just Do My Own Small Business Accounting?

You absolutely can, and many people do when they're first starting out. If you're a sole trader with fairly simple finances, handling the books yourself can be a good way to keep those early-days costs down.

But here's the catch: as your business grows, so does the complexity. The time you sink into bookkeeping starts to add up, and the risk of making a costly mistake with HMRC becomes a real worry. Often, a good accountant will actually save you more money than they cost through smart tax planning and by giving you back the time to focus on what you do best – growing your business.

It's less a question of "can I do it?" and more about "is this the best use of my time?" Your time is your most valuable asset as a business owner.

Do I Have to Pay for Accounting Software on Top of the Accountant's Fee?

That really depends on the accountant and how they structure their packages. It's becoming very common for modern accountancy firms to bundle a subscription to top-notch cloud software, like Xero or QuickBooks, directly into their fixed monthly fee.

This is something you need to ask about right from the start to make sure there are no surprise bills later. It’s always worth mentioning if you already pay for your own software subscription, as some accountants might offer a discount. Just make sure to clarify their policy.

When Is the Right Time to Get an Accountant?

Honestly, the sooner, the better. Bringing an accountant on board right from the beginning can be a game-changer. They can give you crucial advice on setting up your business structure—like whether to be a sole trader or a limited company—and help you get your bookkeeping systems right from day one.

Getting that professional guidance early on ensures you're compliant and helps you sidestep expensive mistakes that can be a real headache to fix down the line. Think of it as laying a solid foundation for your business's financial future.

Ready to build a strong financial foundation for your business? The team at Stewart Accounting Services offers expert guidance on everything from initial setup to long-term growth strategy, ensuring you have more time, more money, and a clearer mind. Get in touch today to see how we can help.