Filing your company accounts with Companies House is one of those non-negotiable legal duties every director faces. While it might sound complicated, the process is actually quite manageable once you get the hang of it. The easiest route for most is the Companies House WebFiling service—you’ll just need your company authentication code and your financial figures ready to go. Of course, you can also file directly through compatible accounting software or simply hand the whole thing over to an accountant.

Your Quick Guide to Filing Company Accounts

Getting your annual accounts submitted is more than just a bit of admin; it’s a fundamental part of running a limited company in the UK. This is your legal obligation to provide a transparent snapshot of your company’s financial health on the public record. For directors new to the game, it can feel like a daunting task, but breaking it down into a clear journey makes it far less intimidating.

Think of it this way: the filing process doesn't just start the day you log into a government portal. It really begins with solid bookkeeping throughout your financial year and only truly ends when that confirmation email from Companies House lands in your inbox.

The Core Submission Journey

Let's look at the big picture. The entire journey has several key milestones. First up, you need to pinpoint your company’s filing deadline. This is usually nine months after your Accounting Reference Date (ARD), so get that date circled on your calendar. With the deadline in mind, the next job is preparing the accounts themselves, making sure they’re in the right format for your company’s size—whether you qualify as a micro-entity, a small business, or something larger.

Knowing which financial statements to pull together is half the battle. If you're unsure, our guide on what your year-end limited company accounts need to include is a great place to start. Once everything is prepared, you just need to choose how you'll submit them.

To simplify the entire process, here’s a quick overview of the key stages involved.

Key Stages of Submitting Your Company Accounts

| Stage | Key Action | Critical Consideration |

|---|---|---|

| Preparation | Determine your ARD and filing deadline. Gather all financial records. | Don't leave this until the last minute. Good bookkeeping all year makes this stage painless. |

| Accounts Formatting | Choose the correct accounts type (e.g., micro-entity, small company). | Using the wrong format is a common reason for rejection. Double-check your eligibility. |

| Choosing a Method | Decide between WebFiling, software, or using an accountant. | Online filing is generally the fastest and has built-in error checks. |

| Submission | Enter your data into the chosen platform and submit. | Have your Company Number and Authentication Code to hand before you start. |

| Confirmation | Wait for the confirmation email from Companies House. | Don't assume it's done until you get this email. Check your junk folder! |

Following these stages in order will help you stay on track and file successfully.

My advice? Always opt for online filing if you can. It’s faster, more secure, and the built-in checks are brilliant for catching simple mistakes that could get your accounts rejected.

After hitting 'submit,' all you need to do is keep an eye out for that crucial confirmation email. This guide will walk you through each of these stages with practical tips I've picked up over the years, helping you file with confidence and steer clear of any nasty penalties for getting it wrong or missing the deadline.

Understanding Filing Deadlines and Avoiding Penalties

Missing your Companies House filing deadline is one of the easiest and most frustrating ways to lose money as a business owner. Unlike many other compliance tasks, there are no gentle reminders or warning letters. The penalties are automatic, immediate, and can really sting.

Staying compliant is simply a matter of knowing your dates and planning ahead.

For most private limited companies, the rule is straightforward: your statutory accounts must be filed within nine months of your company’s financial year-end. This date is known as your Accounting Reference Date (ARD). So, if your year-end is 31st December, your accounts have to be successfully filed by 30th September of the following year.

Calculating Your Filing Deadline

The first set of accounts you file for a new company works a little differently. You’re typically given 21 months from the date your company was incorporated to file them. This longer initial period is designed to give new businesses a bit of breathing room to get up and running before their first major filing. After that, the regular nine-month cycle kicks in.

A critical point to remember is that the deadline is for receipt, not for sending. Companies House must have accepted your submission by this date. I’ve seen many directors leave it until the last day, only for a minor error or a technical glitch to cause a rejection. That mistake immediately tips them into penalty territory.

For a detailed breakdown of how these dates work, check out our guide on understanding Companies House filing deadlines.

The Real Cost of Filing Late

The penalties for late filing are far from a simple slap on the wrist. They operate on a tiered scale based on how late you are, and—this is the important part—the fines double if you file late for two years in a row.

Here’s a quick look at the penalty structure for a private limited company:

- Up to 1 month late: £150

- 1 to 3 months late: £375

- 3 to 6 months late: £750

- Over 6 months late: £1,500

A real-world example: A small business I know filed its accounts five weeks late and was hit with an instant £375 penalty. The following year, they made the same mistake, and the fine for that second offence jumped to £750. That’s over a grand in completely avoidable costs.

This isn't a rare occurrence, either. Official Companies House data reveals that between 2019 and 2023, roughly 2–3% of active private limited companies faced late-filing penalties each year. These fines are strict and automatically applied, which you can read more about on the UK government's Companies House page.

Beyond the financial hit, persistently failing to file is a criminal offence for directors and can ultimately lead to your company being struck off the register.

The best defence is simple: know your deadline, put it in your calendar with multiple reminders, and start preparing your accounts at least two months in advance. Better yet, work with an accountant who manages these deadlines for you, giving you a crucial safety net and peace of mind.

Choosing the Right Accounts for Your Business Size

Before you even think about filing, the first hurdle is figuring out what to file. Getting this wrong is a common trip-up. The type of accounts you need to prepare isn't just a matter of preference; it's dictated by your company's size, and the rules are quite specific.

This decision sets the stage for everything that follows. It determines how much detail you have to share with the public and, frankly, how much work is involved. Nailing this choice means you stay compliant without oversharing sensitive financial data—a huge plus for most small businesses.

Are You a Micro-Entity?

For the smallest businesses, there's a straightforward option: micro-entity accounts. This is the simplest format available, designed to cut down on the red tape. If you qualify, you can file a much simpler balance sheet and you don't even need to include a directors' report or a profit and loss account. This is great for keeping your financial details private.

So, how do you know if you're a micro-entity? Your business just needs to meet at least two of these three conditions for the financial year:

- Turnover is £632,000 or less.

- Your balance sheet total (your total assets) is £316,000 or less.

- You have an average of 10 employees or fewer.

If that sounds like your company, filing as a micro-entity is almost certainly the way to go. It saves a ton of time and keeps things simple.

Qualifying as a Small Company

What if you've grown beyond the micro-entity stage? You’ll probably fit into the 'small company' category. The reporting here is a bit more involved, but it’s still far less demanding than what larger firms face. You'll need to prepare a profit and loss account and a directors' report, but you can often submit abridged, or simplified, versions.

The goalposts for a small company are set quite a bit wider. You just have to meet two of the following:

- Turnover is £10.2 million or less.

- Your balance sheet total is £5.1 million or less.

- You have an average of 50 employees or fewer.

The vast majority of limited companies in the UK will land in either the micro or small company bracket, so chances are, one of these will apply to you.

What About Dormant Companies?

There’s one other common scenario worth mentioning: the dormant company. Your company is considered dormant if it hasn't had any 'significant accounting transactions' all year. Think of a business you've registered but haven't started trading with yet, or one that's stopped trading but hasn't been officially closed down.

Filing for a dormant company is incredibly simple. You just need to tell Companies House it’s been dormant. The crucial thing to remember is that you still have to file. Don't ignore it, or you'll face the exact same penalties as an active, trading company.

Getting the accounts format right from the start is the foundation of a smooth, successful filing. It makes sure you're doing what you're legally required to do, without creating unnecessary work for yourself.

How to File Your Accounts Online with Confidence

These days, filing your accounts online is the standard, and for good reason. It's worlds away from the old paper-based system – it’s faster, far more secure, and has clever built-in checks that catch the kind of simple mistakes that would get a postal submission rejected straight away.

Let's break down the two main ways you can get this done digitally.

Using the Companies House WebFiling Service

For most directors handling their own filing, the go-to option is the Companies House WebFiling service. It’s a free government portal built specifically for this job. Before you even think about logging in, though, you need two key bits of information ready.

First is your company registration number (CRN). The second, and most important, is your company's six-digit authentication code. This code is like a digital signature for your company; it’s confidential and proves you have the authority to make official filings. Keep it safe.

Once you’re in, the system is pretty intuitive. It walks you through a series of online forms that are tailored to the type of accounts you need to file, whether that’s for a micro-entity or a small company. Your task is simply to transfer the figures from your prepared balance sheet and any other required reports into the correct fields on the screen.

One of the best features is the instant validation. The portal will immediately flag common errors, like a balance sheet that doesn't actually balance, stopping you from submitting a flawed return. This simple check saves thousands of directors from the headache of a rejection notice.

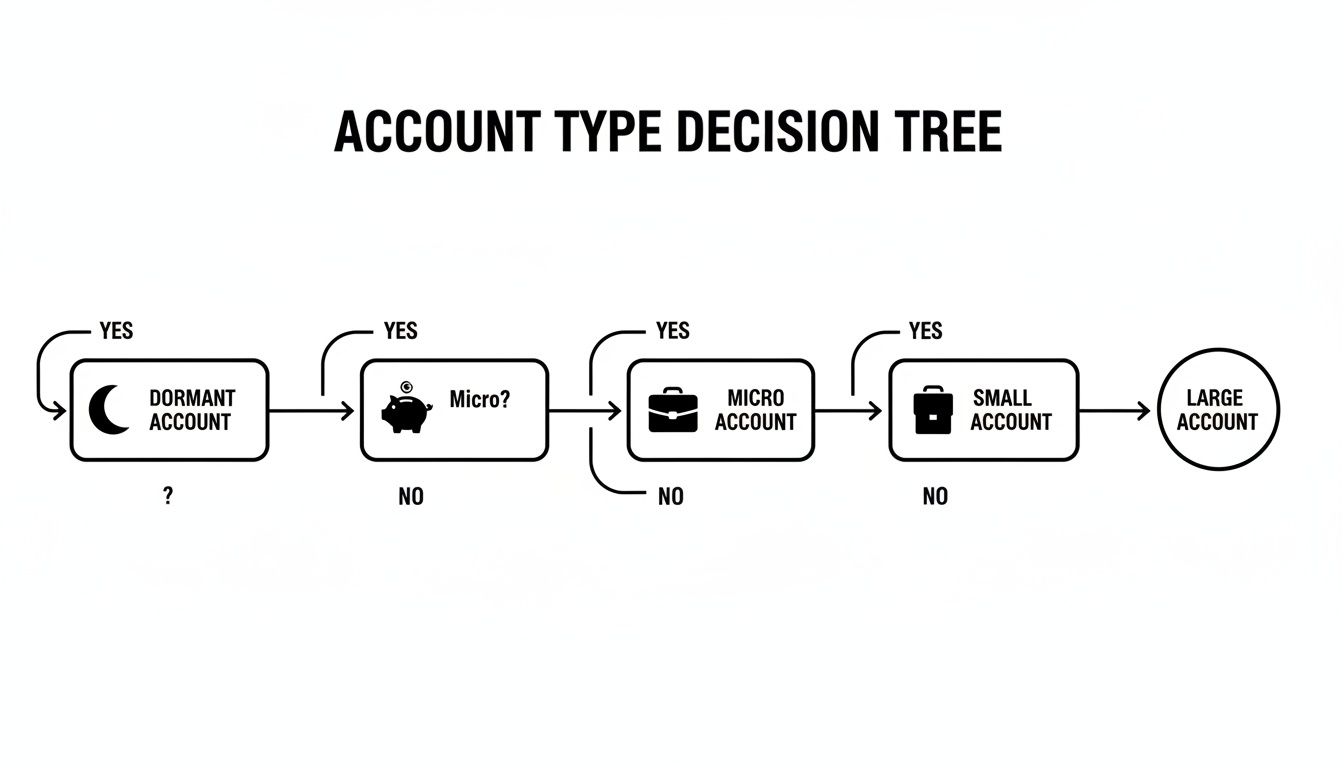

Not sure which accounts you need to prepare? This decision tree can help you quickly figure out where your company fits.

As you can see, it all comes down to whether your company has been trading and, if so, whether it meets certain financial thresholds for turnover, assets, and employees.

A Word of Advice: Have your final, checked accounts open right beside you before you start typing anything into the portal. Rushing this data entry part is where tiny but frustrating mistakes happen. A single misplaced zero can throw everything off and lead to a rejection.

It’s also worth noting a big change on the horizon. Soon, all directors and Persons with Significant Control (PSCs) will need to verify their identity before they can file documents. You can get ahead of the curve by reading our guide on verifying your ID at Companies House. It's a welcome move designed to improve transparency and clamp down on fraud.

Filing Through Accounting Software

If you're already using modern accounting software, there's an even smoother way to file. Platforms like Xero or QuickBooks are often built to talk directly to Companies House, which can turn the entire submission process into just a few clicks.

This method is brilliant because it pulls the numbers directly from your financial records, practically eliminating the risk of typos or transposition errors. It's also incredibly efficient. Instead of preparing your accounts, then logging into a separate system to manually re-enter all the data, you can do it all from one place.

The process generally looks something like this:

- Link your software: You’ll authorise the connection to Companies House by entering your company number and authentication code within your accounting platform. This is usually a one-time setup.

- Run the year-end reports: Use the software’s built-in tools to generate the required financial statements.

- Review and approve: The system will produce a draft of your accounts. It's crucial to review this carefully to ensure everything is accurate.

- Hit submit: Once you're happy, a final click sends the accounts securely and directly to Companies House.

Whether you opt for the direct WebFiling service or use your integrated software, success comes down to preparation. Having your figures finalised and your authentication code to hand will make filing your accounts a quick and painless task.

When to Partner with an Accountant for Your Filing

While you can absolutely file your own accounts, especially when your business is small and straightforward, there’s a tipping point where doing it yourself is no longer the smartest play. Bringing an accountant on board isn't just about handing off a chore; it’s a strategic move that frees you up to do what you do best—run your business.

Figuring out when to make that leap can be tricky. It's rarely a single lightbulb moment. Instead, it's often a slow realisation that your time is far more valuable when spent on generating sales, or that your company's finances are getting a bit too complicated for a simple spreadsheet.

Recognising the Trigger Points

So, what are the tell-tale signs that it’s time to call in a professional? Maybe your business is growing fast. More customers, new team members, and climbing revenue all add complexity to your books. The accounts that once took you an evening to sort out can suddenly feel like a week-long nightmare.

Another big clue is uncertainty. Are you positive you’re claiming every single allowable expense? Do you really understand the tax implications of that big contract you just won? If you're starting to second-guess yourself, that’s your cue. Getting it wrong could mean paying too much tax or, even worse, attracting unwanted attention from HMRC.

Keep an eye out for these common triggers:

- Rapid Business Growth: Your turnover has jumped, you've started hiring staff, or you're now navigating the world of VAT.

- Serious Time Constraints: You're spending more hours wrestling with your accounts than you are talking to customers or working on your next big idea.

- Compliance Jitters: You have a nagging feeling that you might not be ticking every single legal box for your company's size or industry.

- Looking to the Future: You need solid financial forecasts because you're seeking investment, planning a major asset purchase, or thinking about an exit strategy down the line.

If any of these sound familiar, the relatively modest fee for an accountant starts to look like an incredibly smart investment.

The Value Beyond Just Filing

An accountant does so much more than just plug numbers into the Companies House website. Their true value comes from the expertise and advice they provide all year round. Think of them as your first line of defence against expensive errors.

A good accountant won't just file your accounts correctly and on time. They'll actively search for ways to make your business more tax-efficient, help you manage cash flow, and give you the financial clarity needed to make sound strategic decisions.

They are your financial co-pilot. They can spot opportunities you might have missed entirely, like specific tax relief schemes or more effective ways to structure your finances. Above all, they offer peace of mind. Knowing a professional has checked every figure and that your submission is fully compliant frees up a huge amount of your mental energy.

Ultimately, deciding whether to hire an accountant is a classic cost-versus-value calculation. The cost is a clear monthly or annual fee. The value? It's measured in saved time, lower tax bills, avoided penalties, and the sheer confidence you get from having a financial pro in your corner.

A Few Common Questions We Hear All the Time

When you're running a business, juggling different legal duties can feel like spinning plates. It’s no surprise that a few common questions pop up again and again, especially when it comes to filing accounts. Let’s clear up some of the most frequent points of confusion for directors.

One of the biggest mix-ups I see is assuming that one submission covers everything. That’s a trap, and unfortunately, it can be a costly one.

What’s the Difference Between Filing with Companies House and HMRC?

This is easily the most critical distinction to get your head around. Think of them as two separate jobs for two entirely different audiences.

When you file accounts with Companies House, you're fulfilling a legal requirement for public transparency. These documents go on the public record, showing the world—from suppliers to potential investors—that your company is solvent and financially sound.

Your Corporation Tax Return (CT600), on the other hand, is a private conversation between you and HMRC. Its only job is to work out how much Corporation Tax your company needs to pay. The deadlines are often different, and the level of detail required can vary too. You might send full statutory accounts to HMRC but be eligible to file simpler, abridged accounts with Companies House. You have to track both separately.

Can I Change My Accounts After I’ve Filed Them?

Yes, but it’s not as simple as swapping out a document. If you spot a mistake in accounts that have already been filed, you have to go through a formal amendment process.

You can't just delete the old ones. Instead, you must prepare and submit a completely new set of accounts, making sure the balance sheet is clearly marked as “amended.” You’ll also need to add a note explaining exactly what was changed and why. It’s a bit of a hassle and can sometimes draw unwanted attention, so getting it right the first time is always the best strategy.

If you find a major error in a set of filed accounts, my advice is always the same: call an accountant. They'll know exactly how to navigate the amendment process correctly, making sure it’s handled with minimum fuss and no compliance hiccups.

What Happens If I Just Don’t File My Accounts?

Ignoring your filing obligations is far more than a simple admin slip-up—it’s a criminal offence, and the responsibility falls directly on the company’s directors. The consequences are severe and go way beyond the automatic late filing penalties that rack up over time.

Companies House can, and will, prosecute directors personally. This could lead to a criminal record and a potentially unlimited fine. If the failure continues, they have the power to forcibly strike your company off the register. If that happens, your company legally ceases to exist, and its assets can become the property of the Crown. This is one of the most fundamental duties of a director; the accounts must be filed on time, every single year. No excuses.

Feeling the pressure of looming deadlines and complex rules? Let Stewart Accounting Services lift that weight. We can manage all your year-end accounts and tax returns, freeing you up to do what you do best—run your business. See how we can make your life easier at https://stewartaccounting.co.uk.