When your company has a tough year and posts a trading loss, it can feel like a major setback. But what if that loss could actually put cash back into your business right now? That's exactly what loss carry back corporation tax is designed to do.

It’s a UK tax relief that allows a limited company to take a trading loss from the current year and offset it against profits made in a previous accounting period. This isn't just a paper exercise; it often results in a direct corporation tax refund from HMRC, giving your business a much-needed cash injection.

Understanding How Loss Carry Back Works

Think of the loss carry back corporation tax system as a kind of financial shock absorber built into the UK tax rules. It’s a practical acknowledgement from the government that business isn’t always a smooth, upward journey. Profits fluctuate, whether due to market shifts, major new investments, or just an unexpectedly rough trading period.

Instead of just letting you use a loss to reduce tax bills in the future (known as carrying forward), this relief lets you look over your shoulder. You can take the trading loss from your difficult year and apply it to the taxable profits of a more successful, earlier year. The result? A direct cash refund of corporation tax you've already handed over to HMRC.

Turning a Current Loss Into a Past Refund

The idea at the heart of this is both simple and incredibly powerful. A loss you've made today becomes the key to unlocking cash from a more profitable yesterday. This gives your business immediate liquidity, which can be the difference between struggling and stabilising.

Here’s a quick summary of the core features and benefits.

Loss Carry Back Corporation Tax at a Glance

| Feature | Standard Rule | Key Benefit |

|---|---|---|

| Carry Back Period | 1 year (temporarily extended to 3 years) | Offset losses against the most recent profitable period first. |

| Claim Type | Trading Losses | Applies directly to core business trading activities. |

| Outcome | Corporation Tax Refund | Generates an immediate cash injection for the business. |

| Flexibility | Claim 'all or part' of the loss | Allows for strategic tax planning alongside other reliefs. |

This table highlights just how valuable this relief can be for managing your company's financial health through challenging times.

Key benefits of this approach include:

- Immediate Cash Flow: Unlike carrying losses forward (which only reduces a future tax bill), carrying back generates actual cash.

- Financial Stability: This refund can be put straight to work covering overheads, paying staff, or reinvesting in a recovery strategy.

- Supports Investment Cycles: It helps businesses that make a big investment, causing a temporary loss, by clawing back tax paid on earlier profits.

The ability to carry back a loss transforms it from a negative entry on your accounts into a proactive financial tool. It's about recovering past tax payments to fund your company's present needs and future growth.

This relief is a fundamental part of the UK's tax framework. As per HMRC’s own guidance, a company that makes a trading loss can carry it back for one year to reduce the taxable profits of that earlier period, generating a refund. You can review HMRC's official guidance on interpreting corporation tax statistics for 2025. With upcoming discussions around raising corporate taxes, staying on top of these reliefs is more important than ever for smart financial planning.

Eligibility Rules and Claim Deadlines

Getting a tax refund by carrying back a loss isn't automatic; it all comes down to meeting HMRC's criteria and, crucially, acting within the set timeframes. It's a common misconception that any financial dip qualifies. The first thing to get right is that this relief is specifically for UK limited companies that have suffered a trading loss—meaning the loss must come directly from your main business activities.

The core eligibility requirements are quite clear:

- Your business must be a company that pays UK Corporation Tax.

- You need to have a genuine trading loss in a particular accounting period.

- Critically, you must have made taxable trading profits in a previous, eligible accounting period to offset the loss against.

This distinction is important. Losses that come from other areas, like investment activities or capital losses from selling assets, are handled under different rules and won't qualify for this specific relief. It’s all about the operational health of your business.

Navigating Time Limits and Claim Periods

When it comes to making a claim, the clock is always ticking. The standard rule is that a company can carry a trading loss back against profits made in the preceding 12 months. So, if you made a loss in your accounting year ending 31 December 2024, you can set it against the profits you made in the year that ended on 31 December 2023.

You might remember more generous rules being available a short while ago. To help businesses through the pandemic, the government brought in a temporary extension that allowed trading losses to be carried back for up to three years. This was a lifeline for many, but it's vital to know that this extension has now finished. We are firmly back to the standard one-year carry-back rule.

Crucially, the deadline for making a loss carry-back claim is two years from the end of the accounting period in which the loss occurred. Miss this window, and the chance for a refund is gone for good.

Let's put that into practice. For a loss made in a financial year ending 31 December 2023, your company would have until 31 December 2025 to get the claim into HMRC. This is a hard deadline. It really highlights why staying organised with your accounts is so important and links directly to your responsibilities for the limited company tax return deadline. Meeting these dates ensures you don’t leave valuable cash on the table.

Seeing Loss Carry Back in Action

Theory and regulations can feel a bit abstract. To really get a feel for how powerful a loss carry back claim can be, it’s best to walk through a real-world scenario. Let's see how this tax relief translates into a direct cash injection for a struggling business.

Let’s imagine a UK tech company called ‘Innovate Ltd’. They’ve had a cracking year of trading, but now they're investing heavily in the future, which has pushed them into a temporary loss.

The Financial Picture

To paint the picture, here are the simplified trading results for Innovate Ltd over two years:

- Year 1 (Ending 31 March 2024): A fantastic, profitable period. Innovate Ltd reported taxable profits of £150,000.

- Year 2 (Ending 31 March 2025): A year of big investment. The company pumped cash into R&D for a new product, resulting in a trading loss of £80,000.

Back in Year 1, Innovate Ltd would have worked out its tax bill based on that £150,000 profit. Let's say the corporation tax rate for that year was 25%.

Year 1 Corporation Tax Paid: £150,000 (profit) x 25% = £37,500

They paid this £37,500 over to HMRC, all above board. Now, fast forward to the end of Year 2. The company is looking at an £80,000 loss on its books. This is where the opportunity lies.

Making the Loss Carry Back Claim

Instead of just carrying that £80,000 loss forward to reduce future tax bills, Innovate Ltd needs a cash boost right now to keep the development project going. So, the directors decide to carry the loss back against the profits from the bumper Year 1.

The process is essentially a do-over of the previous year's tax calculation. Here’s the step-by-step:

- Start with Year 1's Original Profit: We begin with the £150,000 profit from that successful year.

- Deduct the Year 2 Loss: The £80,000 loss is carried back and set against the previous year's profit.

- Find the New, Adjusted Profit: £150,000 (Original Profit) – £80,000 (Carried-Back Loss) = £70,000 (New Taxable Profit).

This simple adjustment means that, in HMRC's eyes, Innovate Ltd's profit for Year 1 is now treated as if it were only £70,000 all along.

Calculating the HMRC Refund

With this new, lower profit figure, the corporation tax for Year 1 gets recalculated. Crucially, you use the tax rate from the year the profit was actually made—in this case, the 25% rate from Year 1.

Revised Year 1 Corporation Tax Bill: £70,000 (Adjusted Profit) x 25% = £17,500

Now for the best part. Innovate Ltd originally paid £37,500 in tax for Year 1, but its revised liability is just £17,500. The difference is what HMRC owes them back.

- Original Tax Paid: £37,500

- Revised Tax Due: £17,500

- Total Refund Claim: £37,500 – £17,500 = £20,000

By making a successful loss carry back claim, Innovate Ltd gets a £20,000 cash refund paid directly into its bank account from HMRC. This is immediate, debt-free cash that can be used to fund operations, meet payroll, or push on with its investment plans. This example shows perfectly how a tough year can unlock cash from a previous success story.

Comparing Your Loss Relief Options

When your company makes a loss, the ability to carry it back for a quick tax refund is a powerful tool in your financial toolkit. But it's not the only one. Understanding your options is key, as the choice between looking to the past for a refund or saving the loss for the future can make a huge difference to your cash flow and long-term health.

The two main alternatives to a loss carry back corporation tax claim are carrying the loss forward against future profits or, if you're part of a group, using group relief. Each serves a very different strategic purpose.

Carry Back vs Carry Forward

Think of a loss carry-back as an immediate cash injection. You're essentially asking HMRC for a refund on tax you've already paid in a previous, profitable year. This is a lifeline for businesses needing a quick liquidity boost to cover immediate overheads or simply to steady the ship after a tough trading period.

Carrying a loss forward, on the other hand, is more of a long-term play. Instead of getting cash now, you hold onto the loss and use it to shield profits in a future accounting period. It won't generate a refund today, but it's an incredibly valuable way to reduce your tax bill when the business is back on its feet and making money again. This is a smart move if you're forecasting strong future growth and your current cash position is stable.

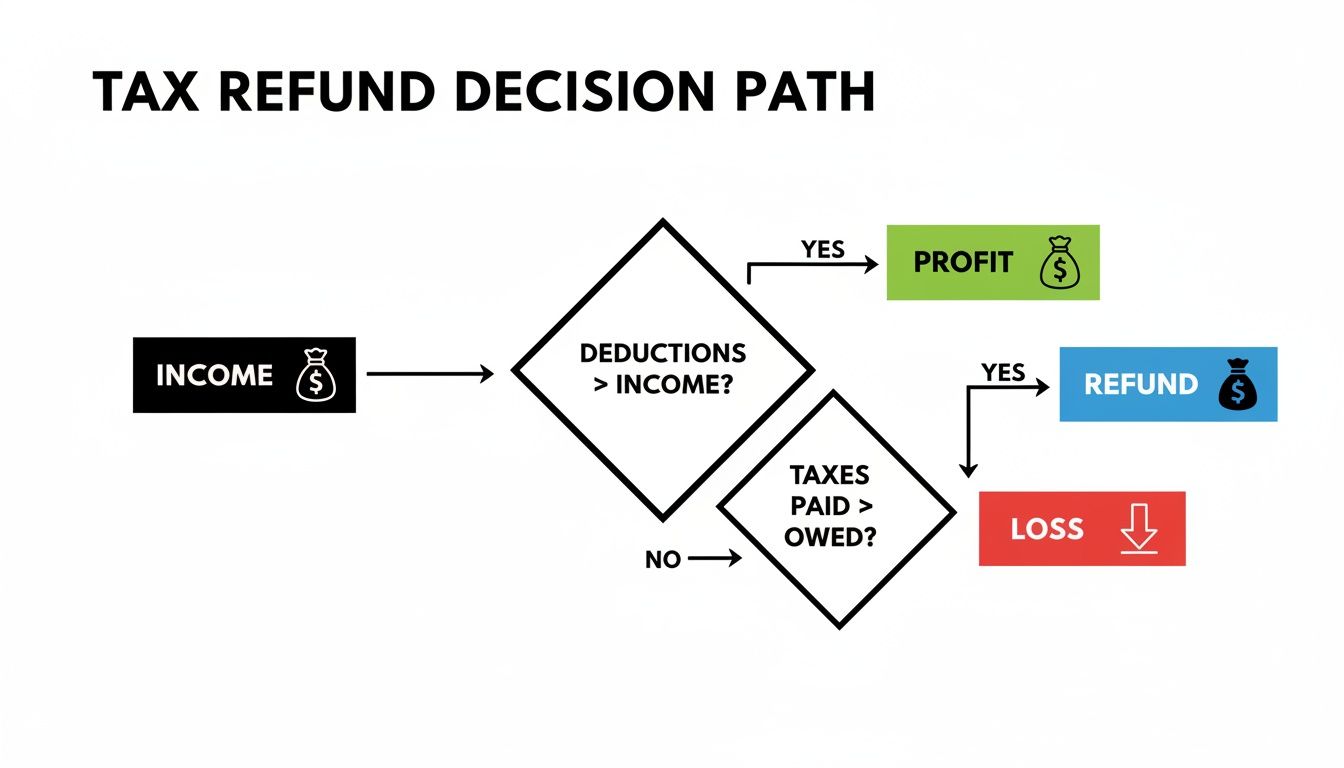

This flowchart neatly illustrates the logic of turning a current-year loss into a valuable tax refund from a prior year.

As you can see, when a profitable company hits a period of loss, the carry-back mechanism creates a direct path to reclaiming tax, putting cash back into the business.

Understanding Group Relief

If your company is part of a corporate group, you have a third, very useful option: group relief. This allows a company that has made a trading loss to effectively hand it over, or "surrender" it, to another profitable company within the same group.

The profitable company can then offset this surrendered loss against its own profits for the same accounting period, thereby reducing its own Corporation Tax bill. It’s a fantastic way to manage the group's overall tax burden efficiently, keeping cash within the wider corporate family where it's needed most.

To help you see how these options stack up against each other, here’s a straightforward comparison.

Comparing UK Corporation Tax Loss Relief Options

When deciding how to use your trading losses, it helps to see the core features of each relief side-by-side. The right choice depends entirely on your company's specific situation—whether you need cash now, want to save on tax later, or need to optimise tax across a group.

| Relief Type | Direction of Relief | Timing of Tax Benefit | Best Used For |

|---|---|---|---|

| Loss Carry Back | Past profits (preceding year) | Immediate cash refund | Boosting short-term cash flow and stabilising the business after a difficult year. |

| Loss Carry Forward | Future profits (indefinite) | Future tax saving | Reducing tax liability during periods of anticipated high growth and profitability. |

| Group Relief | Sideways to another group company | Current-year tax saving | Optimising the overall tax position for a corporate group in the current financial year. |

As the table shows, there's no single "best" answer. Choosing the right path is a strategic financial decision that requires you to weigh your company's current cash needs against its future profit forecasts.

For a deeper dive, you can learn more about the various reliefs and allowances for corporation tax purposes to see how they all fit together. Making the right choice ensures you get the maximum value from your losses, helping to turn a challenging period into a real financial advantage.

How Do I Actually Claim the Relief from HMRC?

You've done the calculations and confirmed that carrying back a loss makes sense for your business. So, what's next? Getting your claim officially lodged with HMRC is a crucial step, and doing it correctly will save you a lot of back-and-forth later on.

There are two main ways to go about this. The right choice for you will probably depend on how quickly you need the tax refund in your bank account.

The Standard Route: Amending Your Previous Tax Return

For most businesses, the go-to method is to amend the Company Tax Return (CT600 form) for the profitable year you're carrying the loss back to. Think of it as officially re-doing the maths for that past year, this time with the benefit of the new loss figure.

You'll need to go back into that return and fill in the specific boxes for claiming relief. The key spot is the "Claims to relief from corporation tax" section, where you'll enter the loss amount you are carrying back from the later period.

This is the most thorough and formal way to do things, creating a clear paper trail for both you and HMRC. If you aren't in a desperate rush for the cash, this is usually the best approach. If the nuts and bolts of the CT600 are a bit hazy, our guide on how to file company tax returns is a great refresher.

The Fast Track: Making a Standalone Claim

But what if you need that tax refund, and you need it now? Waiting for a full amended return to be processed can take time. Recognising this, HMRC offers a faster, more direct route: making a standalone claim.

This usually involves writing a formal letter directly to HMRC, completely separate from the CT600 filing process. It’s designed to get the claim into the system quickly, but you absolutely have to include the right details, or it will just cause delays.

When writing to HMRC, you must state clearly that you are making a claim for relief under section 37 of the Corporation Tax Act 2010. This is the official signpost that tells them exactly what you're doing and why.

To give your standalone claim the best chance of a speedy resolution, make sure your letter includes all of the following:

- Your Company Details: Full company name and your Unique Taxpayer Reference (UTR).

- The Loss Itself: State the exact amount of the trading loss and the accounting period it happened in.

- Where It's Going: Clearly specify the profitable accounting period you are carrying the loss back to.

- Getting Paid: Provide your company's UK bank account number and sort code so HMRC knows where to send the refund.

Since claiming often means adjusting figures you've already submitted, having a grasp of general guidance on amending past tax returns is always a good idea. Whichever route you take, accuracy and clarity are your best friends in getting that refund approved without a hitch.

Common Mistakes to Avoid

Navigating the rules for a corporation tax loss carry-back claim can be a bit of a minefield. It's easy to make simple errors that lead to frustrating delays or, even worse, a flat-out rejection from HMRC. Knowing what to watch out for is the best way to get it right the first time and get that vital cash refund back into your business.

One of the easiest traps to fall into is simply missing the deadline. HMRC is incredibly strict on this. You have exactly two years from the end of the accounting period where the loss happened to make your claim. Miss that window, and the chance for that immediate tax refund is gone for good.

Another classic blunder is getting the numbers wrong on the loss itself. You can only carry back trading losses. People often mistakenly try to include things like capital losses, which just won't fly. This will get your claim thrown out and you'll have to start all over again, wasting precious time.

Forgetting Key Calculation Details

It's also surprising how often the small details in the calculation can trip people up, especially when tax rates change. A massive error we see is using the wrong corporation tax rate for the refund calculation.

Remember, your refund is always calculated using the corporation tax rate of the profitable year you're carrying the loss back to. It’s not based on the rate from the year you made the loss. This can make a huge difference to the amount of cash you get back.

Finally, you can’t be selective about how you use the loss. You have to set the carried-back loss against the entire available profit of the preceding year. You can't just 'slice off' a bit to get a refund now and save the rest to carry forward. It's an all-or-nothing deal against that year's profit.

When to Seek Professional Advice

For a simple, one-off claim, you might be able to handle it yourself. But some situations are genuinely complex and trying to DIY it could cost you dearly. It's probably time to call in an accountant if:

- Your company is part of a group: Juggling group relief rules alongside a carry-back claim is a specialist skill. It's very easy to get wrong.

- The business is closing down: When a company ceases to trade, it can use 'terminal loss relief', which has its own unique set of rules.

- You're unsure what's best: Is it better to carry the loss back for a quick refund or carry it forward to reduce future tax bills? An expert can run the numbers and model the different outcomes, helping you make the smartest financial decision for the business.

In these cases, getting some expert help isn't an expense; it's an investment to make sure your claim is solid and you get the maximum benefit you're entitled to.

Frequently Asked Questions

When it comes to carrying back corporation tax losses, a few questions pop up time and time again. Let’s clear up some of the most common points of confusion.

Can I Choose How Much of the Loss to Carry Back?

This is a big one, and the short answer is no. You don't get to pick and choose the amount.

When you make a carry-back claim, you have to use the maximum available loss to wipe out the entire profit from the preceding 12 months. You can’t, for instance, just carry back enough loss to reduce last year’s profit to the small profits threshold. The rule is you must reduce that profit to zero before you can do anything else with the leftover loss, like carrying it forward.

What if My Accounting Period Isn't a Standard 12 Months?

Things can get a bit trickier if you have an accounting period that's shorter or longer than the usual 12 months. The core principle of carrying back the loss still stands, but the calculations need careful handling.

You'll need to apportion the profits and losses correctly to match the specific timeframes. It’s certainly doable, but this is one of those areas where getting a bit of professional advice can save you a major headache and ensure you get it right.

Does the Corporation Tax Rate Affect My Refund?

Yes, it absolutely does. The refund you receive from HMRC will be calculated based on the corporation tax rate that was in effect during the profitable year you are carrying the loss back to.

It's not based on the tax rate from the year you actually made the loss. This is a crucial detail, especially when tax rates change between years.

Navigating the rules for loss carry back corporation tax is all about careful planning and understanding the details. For expert guidance that’s specific to your company's situation, get in touch with Stewart Accounting Services today to make sure you're maximising your claim. You can find us at https://stewartaccounting.co.uk.