Navigating the world of landlord taxes can feel like a maze, but it all starts with one simple question: how much did you earn? If your gross rental income for the tax year creeps over £1,000, you need to let HMRC know. And if that income is more than £2,500 after you’ve deducted your running costs, then it’s time to fill out a Self Assessment tax return.

Understanding Your Landlord Tax Obligations

.

At its heart, your duty is to give HMRC an honest picture of your earnings. But this isn't just about declaring the total rent you've received. The real task is figuring out the difference between your total income and your actual taxable profit.

Key Concepts for Your Tax Return

Before we get into the nitty-gritty of the numbers, let's get a few key terms straight. You'll see these crop up time and again.

- Gross Rental Income: This is your starting point—the total rent you collected from your tenants before taking anything off.

- Allowable Expenses: Think of these as the legitimate day-to-day costs of being a landlord. They can be subtracted from your gross income, which is great news for your tax bill.

- Taxable Profit: This is the magic number. It’s what’s left after you subtract your allowable expenses from your gross income, and it's the figure you'll actually pay tax on.

Your primary goal is to calculate this taxable profit figure accurately. Forgetting an allowable expense means you will pay more tax than necessary, directly impacting your investment's profitability.

Introducing the SA105 Form

When it comes to filing your Self Assessment, you'll need to get familiar with the SA105 'UK property' pages. This is the specific supplementary form where you'll list all your property income and those all-important expenses. It’s essentially the financial report card for your rental business that you send to HMRC each year.

Getting this form right is the key to a smooth and stress-free tax return. To get the full picture, it's also worth looking into the wider property investment tax benefits that might be available to you. Having a solid grasp of these concepts from the outset gives you a clear roadmap for what's to come as we dive deeper into the calculations and deductions.

Working Out Your True Rental Profit

Getting your profit calculation right is the bedrock of a solid property rental tax return. This isn't just a case of adding up the rent you've received; it's about understanding what HMRC counts as income and then meticulously subtracting every single cost you're allowed to claim.

Nailing this calculation can be the difference between paying the right amount of tax and giving HMRC far more than you need to. Your starting point is always your total rental income. This is the total amount you were due for the tax year, not just the money that actually hit your bank account.

Defining Your Total Rental Income

So, what goes into that headline income figure? It’s absolutely crucial to capture everything you’ve received from your tenants.

- Monthly Rent Payments: The obvious one. This is the core rent set out in the tenancy agreement.

- Non-refundable Deposits: If you've kept any portion of a deposit to cover things like unpaid rent or professional cleaning, that amount now counts as income.

- Other Tenant Payments: Did you recharge a tenant for a repair they caused? Or bill them for services like gardening? These extras all need to be included in your total.

A good rule of thumb is this: if a payment from a tenant isn't a refundable security deposit, it's almost certainly part of your rental income for tax purposes. Keep clear records of these additional charges so nothing gets overlooked.

Subtracting Allowable Expenses to Find Your Profit

Once you have your total income, the next step is where you can really make a difference: subtracting your allowable expenses. These are the day-to-day running costs you’ve paid out purely for the purpose of renting out the property. The figure you're left with is your taxable profit.

The formula itself is simple: Total Rental Income – Allowable Expenses = Taxable Profit.

This final profit figure is what you’ll declare on your SA105 property pages. It's important to remember that mortgage interest is handled differently these days. It's no longer a straightforward deductible expense but instead provides a tax credit. If you need a refresher on how that works, have a look at our detailed guide on the mortgage interest deduction for rental properties.

A Real-World Calculation Example

Let's walk through a typical scenario. We'll use a landlord named Sarah who owns a single buy-to-let flat.

Sarah's Income for the Tax Year:

- She charges £1,200 per month in rent. Over the year, that's £14,400.

- A tenant moved out, and she kept £150 from their deposit to cover the contractual professional cleaning.

- This makes Sarah's Total Rental Income £14,400 + £150 = £14,550.

Sarah's Allowable Expenses for the Tax Year:

- Letting Agent Management Fees: £1,728

- Landlord Insurance: £250

- Annual Gas Safety Certificate: £85

- Minor Repairs (plumber to fix a leaky tap): £180

- The professional cleaning bill: £150

- Total Allowable Expenses: £2,393

Now, we can calculate her taxable profit:

£14,550 (Total Income) – £2,393 (Total Expenses) = £12,157 (Taxable Profit)

This £12,157 is the figure Sarah will report to HMRC. Her final tax bill will be based on this profit, taking into account her personal tax band and the tax credit for her mortgage interest.

Getting to Grips with Allowable Expenses and Reliefs

Successfully lowering your tax bill isn't about finding clever loopholes. It’s about being meticulous and claiming every single expense you're legally entitled to. I’ve seen countless landlords claim the obvious costs but miss out on the smaller, less apparent deductions, which ultimately means they pay more tax than they need to. A thorough and organised approach here is the foundation of an accurate property rental tax return.

The golden rule from HMRC is that an expense must be incurred "wholly and exclusively" for the purpose of renting out your property. You'd be surprised how much this can cover.

The Day-to-Day Running Costs You Can Claim

These are the regular outgoings that keep your rental business ticking over. Think of them as the essential fuel for your property engine. Forgetting any of these can really inflate your taxable profit.

Here’s what we’re talking about:

- Letting Agent and Management Fees: Any fees or commission paid to an agent for finding tenants, collecting rent, or fully managing the property.

- Landlord Insurance: Premiums for your buildings, contents, and public liability insurance.

- Council Tax and Utility Bills: You can claim for periods when the property is empty between tenancies (known as void periods), as long as you’re the one footing the bills.

- Ground Rent and Service Charges: Standard costs if your property is a leasehold.

- Direct Running Costs: This covers everything from paying a regular gardener or cleaner to other direct services needed to maintain the property for your tenants.

A classic mistake is forgetting to claim for costs during void periods. If you're paying the council tax, gas, and electricity while looking for a new tenant, these are fully deductible expenses. Keep every one of those bills organised.

For a deeper dive, our guide on rental income allowable expenses has a comprehensive checklist to make sure nothing gets missed.

To help you get started, we've put together a handy checklist of common expenses you should be tracking throughout the year.

A Landlord's Checklist of Common Allowable Expenses

Use this checklist to ensure you're not missing any potential deductions when calculating your rental profit. We've categorised them for easy reference.

| Expense Category | Specific Examples of What You Can Claim |

|---|---|

| Professional Fees | Letting agent fees, property management fees, accountant's fees (for preparing rental accounts), legal fees for tenancy agreements (up to 1 year). |

| Utilities & Charges | Council Tax, gas, electricity, water rates (during void periods), ground rent, service charges. |

| Insurance | Landlord-specific buildings and contents insurance, public liability insurance, rent guarantee insurance. |

| Repairs & Maintenance | General repairs (e.g., fixing a leak, replacing a broken lock), decorating between tenancies, gas safety certificates, PAT testing. |

| Office & Admin Costs | Phone calls, stationery, postage directly related to managing the property, mileage for property visits (at HMRC's approved rates). |

| Finance Costs | Mortgage interest tax credit (see below), bank charges on your rental-specific account. |

Remember, this isn't an exhaustive list, but it covers the core expenses most landlords can and should claim to reduce their tax bill. Keep your receipts for everything!

The Tricky Line Between Repairs and Improvements

This is one of the most important distinctions to get right, and it’s a common area of confusion. HMRC looks at repairs and improvements very differently.

A repair simply restores an asset to its previous condition. This is an allowable expense that you can deduct directly from your rental income. For instance, replacing a storm-damaged roof tile or swapping a broken-down boiler for a modern, but equivalent, model is a repair.

An improvement, however, is something that upgrades or enhances the property beyond its original state. Building an extension, adding a conservatory, or knocking through a wall to create an open-plan living space are all improvements. These are considered capital expenditure and can't be deducted from your rental income. Instead, you add them to the property’s cost base, which can help reduce your Capital Gains Tax bill when you eventually sell up.

How Mortgage Interest Relief Actually Works Now

The rules around mortgage interest have changed completely in recent years, and it's vital to understand the new system. Landlords used to be able to deduct all their mortgage interest payments as a standard business expense. That's no longer the case.

This has been replaced by a tax credit system equivalent to 20% of your annual mortgage interest. Instead of reducing your taxable income, this credit is now subtracted directly from your final tax bill. This change primarily hits higher and additional-rate taxpayers because the relief is capped at the basic rate (20%), no matter what tax band you're in.

Let's break it down with a simple example:

- You paid £4,000 in mortgage interest over the tax year.

- Your tax credit is 20% of this figure, which works out to £800.

- This £800 is then knocked off your final income tax liability.

Don't Forget These Key Allowances and Reliefs

On top of direct expenses, there are other valuable reliefs designed to simplify things and lower your tax burden.

- Property Income Allowance: If your gross rental income (before any expenses) is £1,000 or less in a tax year, you have no tax to pay and nothing to declare to HMRC. If your income is over £1,000, you have a choice: you can either deduct your actual, itemised expenses or claim the flat £1,000 allowance instead. This is a great time-saver for landlords with very low running costs.

- Replacement of Domestic Items Relief: This allows you to claim tax relief for the cost of replacing furnishings and appliances in a rented home. It covers items like beds, sofas, fridges, washing machines, and carpets. Crucially, the relief is for a like-for-like replacement, not the initial cost of buying the item in the first place.

If you happen to operate short-term holiday lets, the rules can be a bit different. It’s worth exploring specific short-term rental tax deductions as you might be eligible for different reliefs. By being diligent and understanding these rules, you can make sure your tax return is both compliant and as tax-efficient as possible.

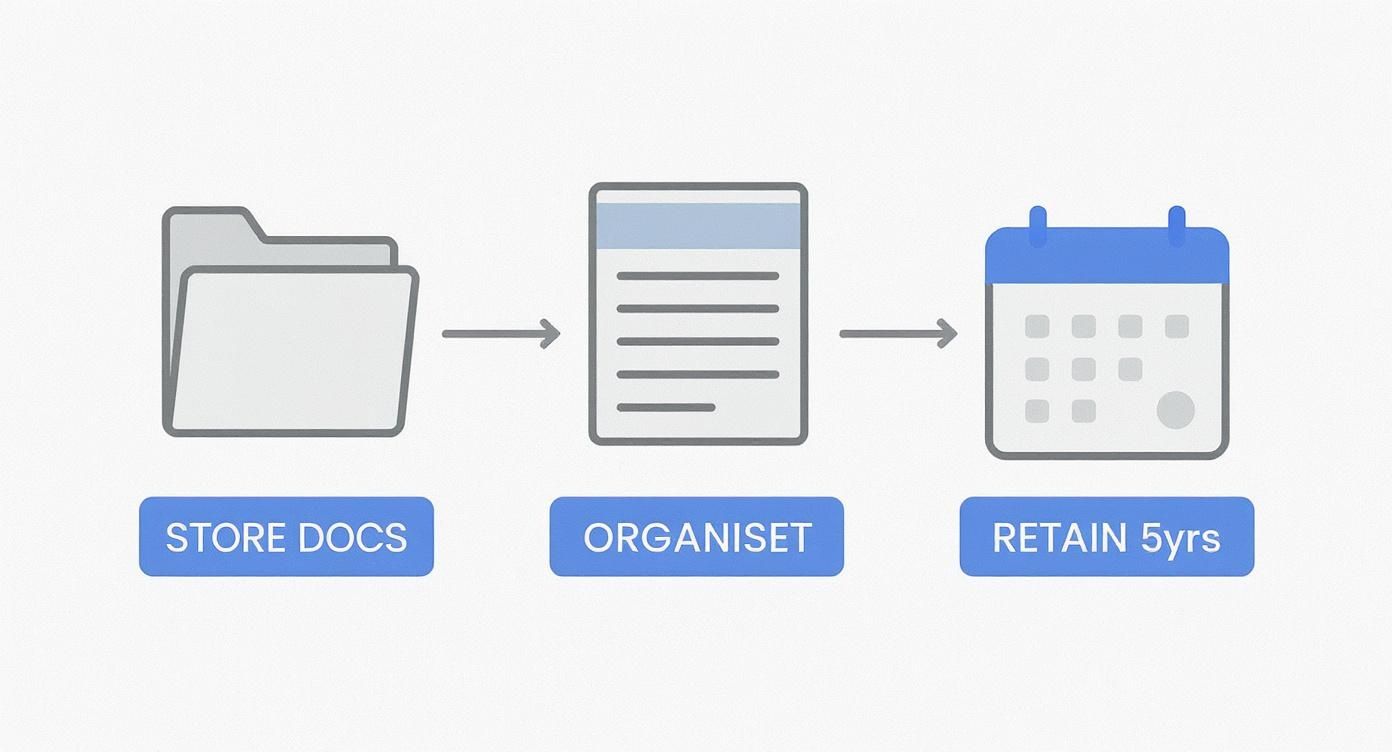

Why Meticulous Record Keeping is Your Best Defence

If there's one habit that separates a stressed-out landlord from a confident one, it's meticulous record-keeping. Think of it this way: solid records are your best friend during tax season and your strongest defence if HMRC ever comes knocking.

Without a clear paper trail, preparing your property rental tax return turns into a frustrating guessing game. You'll inevitably miss out on claiming valuable expenses you're entitled to, which means you'll pay more tax than you need to. Good records transform tax time from a frantic scramble into a calm, methodical process.

The Essential Paper Trail You Must Keep

So, what exactly do you need to hold onto? Building a robust system starts with knowing what to save. An organised file, whether it's a digital folder on your computer or a good old-fashioned ring binder, will save you a world of pain later on.

Here’s a practical checklist of what you should be keeping:

- Proof of all rental income: This isn't just about bank statements showing the rent hitting your account. You'll want copies of all your tenancy agreements too.

- Every single expense receipt and invoice: From the plumber's bill for fixing that leaky tap to your annual landlord insurance certificate and the receipt for a new smoke alarm.

- Mortgage and loan statements: Keep copies of your mortgage statements and any loan agreements related to buying or improving the property.

- Mileage log: If you're driving to the property for viewings, inspections, or to manage repairs, keep a simple log. Note the date, the reason for the trip, and the mileage. It all adds up.

The rule of thumb I always tell clients is simple: if you spent money on the property, keep the proof. If you received money from it, keep the proof. This disciplined approach is what keeps you clear of difficult questions from the taxman.

Finding a System That Works for You

You don't need to invest in a complicated accounting suite to get this right. The best system is the one you'll actually stick with.

For many landlords, a simple spreadsheet is more than enough. Create columns for the date, a brief description of the expense, the category it falls into (like 'Repairs', 'Professional Fees', 'Insurance'), and the amount. This keeps all your figures in one place and gives you a running total, making life much easier when you sit down to complete your tax return.

Others prefer a physical system – a concertina file with labelled sections for each expense type can work just as well. The key is consistency.

How Long to Keep Your Records: The HMRC Rule

Your job isn't done once you've clicked 'submit' on your tax return. HMRC requires you to be able to back up every figure you declare.

In the UK, you must keep all your records for at least five years after the 31st January submission deadline for that tax year. And they can issue penalties if your records are found to be inaccurate, incomplete, or even just unreadable. For the official line, you can read more about how HMRC views rental income and record-keeping on their website.

Let's put that into perspective. For the 2023-24 tax year, which you file by 31st January 2025, you need to hang onto all those records until at least the end of January 2030. It might seem like a long time, but it ensures that if HMRC does open an enquiry, you have all the evidence you need. Being 'audit-proof' isn't about luck; it's all about preparation.

Getting Your Tax Return Filed: A Practical Walkthrough

Right, you’ve tallied up the income and organised all your expenses. You're on the home straight now. The next step is to translate all that careful prep work into your official property rental tax return and get it sent off to HMRC. This bit can feel a little intimidating, but the online system is actually quite logical once you get started.

First things first, if you're a new landlord, you have to register for Self Assessment. This is a crucial first step, and you must get it done by 5th October following the end of the tax year you need to report. After you register, HMRC will post you a 10-digit Unique Taxpayer Reference (UTR). This is your golden ticket to the online filing portal. Don't put this off – it can take a couple of weeks for the UTR to arrive.

Getting to Grips with the HMRC Online Portal

With your UTR in hand and your online account activated, you can finally start your tax return. The system kicks off by asking a series of questions to figure out which sections of the tax return you actually need to fill in. Since you have rental income, you'll need to tick the box for the 'UK property' pages, which is just the online version of the paper SA105 form.

This tailored approach is genuinely helpful. It means you won't get bogged down with questions about employment or foreign income if they don't apply to you, keeping the whole process focused.

The key to a stress-free filing experience is having a solid system for your documents, just like we talked about earlier. This simple workflow is the foundation.

When you have this kind of store-organise-retain process in place, every number you type into the portal is backed by solid proof. It turns tax filing from a guessing game into a straightforward data entry task.

Tackling the SA105 UK Property Pages

The SA105 section is where all your preparation pays off. The online form is essentially a series of boxes, and you just need to fill in the right numbers in the right places. Let's look at the main ones you'll be dealing with.

- Total Rents and Other Income: This is Box 20 on the paper form. It’s for your gross rental income – every penny you received from tenants before taking anything off.

- Property Income Allowance: If you're using the £1,000 allowance instead of itemising your expenses, you'll enter it in Box 20.1. Just remember, it’s one or the other. You can't claim both.

- Property Expenses: Boxes 24 to 29 are where your organised spreadsheet becomes your best friend. They cover different categories like 'Rent, rates, insurance, ground rents etc' (Box 24), 'Repairs and maintenance' (Box 25), and 'Legal, management and other professional fees' (Box 27).

- Residential Finance Costs: Pay close attention to this one (Box 44). This is where you enter the total mortgage interest you've paid. The system then works out the 20% tax credit for you. You don’t deduct it from your income yourself.

I see this mistake all the time. One of the biggest tripwires for landlords is getting the mortgage interest wrong. You must enter the full interest amount in the designated box. Don't subtract it from your rental income – let the HMRC system apply the correct tax credit.

It’s a great idea to have the official SA105 notes from GOV.UK open in another browser tab while you work. Think of it as the official instruction manual to guide you through each box.

The Final Review and Submission

Once you've filled in all the property sections, the portal will generate a full calculation summary. This is your chance to stop and give everything a final, careful review. It will show your total income, all your deductions, and a provisional tax bill based on what you've entered.

Check this summary against your own spreadsheet. Does the taxable profit look right? Does the tax due make sense for your income bracket? If anything seems off, you can easily go back and edit any section before you hit that final submit button.

When you're happy that it's all accurate, you can formally submit your return. You'll get an instant confirmation receipt from HMRC – make sure you save a PDF copy of both this receipt and your full return for your records. And that’s it! Your property rental tax return is filed for another year, with only the payment left to sort out before the 31st January deadline.

When Should You Call in a Property Tax Expert?

For many landlords, especially if you only have one or two straightforward lets, tackling your own property rental tax return is completely manageable. But as your portfolio grows, so does the paperwork and the potential for costly mistakes.

Knowing when to hand things over to a professional isn't about giving up; it’s about making a smart business move. Once you're juggling multiple properties, each with its own income and expense columns, things can get complicated, fast. That's usually the point where getting an expert on board saves you a world of stress and, often, a surprising amount of money.

Navigating Tricky Tax Situations

Some scenarios just aren't straightforward and come with their own set of tricky tax rules. Trying to muddle through these on your own can be a real gamble.

Here are a few common examples where specialist knowledge is invaluable:

- Furnished Holiday Lettings (FHLs): FHLs have some great tax perks, but they also have very specific qualifying rules. An accountant will make sure you’re meeting the criteria to benefit from them.

- Capital Gains Tax: Selling a rental property is a big step. A property tax expert can be crucial here, helping you calculate the gain correctly and making sure you use every single relief you're entitled to.

- Living Abroad: If you're a non-resident landlord, you have a whole different set of rules to follow, like the Non-resident Landlord Scheme. An expert can handle all that for you.

An expert does more than just fill in the boxes on a form. They offer strategic advice, helping you structure your property business in the most tax-efficient way and keeping you on the right side of constantly changing legislation.

Think of partnering with an accountant as an investment in the financial health of your property business. You can learn more about the advantages of professional accountancy support for landlords and see how it can free up your time while potentially reducing your final tax bill.

Answering Your Top Property Tax Questions

Getting to grips with property tax can feel like navigating a maze. Even seasoned landlords run into tricky situations. To help clear things up, let's tackle some of the most common questions that crop up when it’s time to file.

What if My Rental Property Made a Loss This Year?

It might seem counterintuitive, but you should absolutely still file a tax return. In fact, it's a smart move.

When you declare a rental loss on your Self Assessment, HMRC allows you to carry that loss forward. You can then use it to reduce the taxable profit from the same rental business in future years. Think of it as a tax credit you can cash in later.

For instance, say you made a loss of £1,500 this tax year. Next year, your property generates a healthy profit of £4,000. You can deduct the previous year's loss, meaning you'll only pay tax on £2,500 of that profit. It makes a real difference.

How Do We Handle Tax for a Jointly Owned Property?

This is a classic point of confusion. If you own a property with someone else, the rental profit or loss is usually divided based on your ownership share.

For married couples and civil partners, HMRC's default position is a straight 50/50 split, even if one person owns 90% of the property. If you want to be taxed on your actual ownership shares, you'll need to make a joint declaration using a Form 17.

Crucially, each owner must declare their share on their own separate tax return. You'll each need to fill out the SA105 property pages.

A common slip-up is thinking one tax return will cover a jointly owned property. HMRC needs to hear from each owner individually about their share of the income and expenses.

What Are the Rules for Renting Out a Room in My House?

If you're just renting a furnished room to a lodger in your main home, you might be able to take advantage of the government’s Rent a Room Scheme.

This scheme lets you earn up to £7,500 a year completely tax-free. It’s a fantastic relief for homeowners with a spare room.

If your income from the lodger is less than that £7,500 threshold, you have nothing to declare and no tax to pay. If you earn more, you have two choices: you can either pay tax on the income above the threshold, or you can opt out of the scheme and calculate your profit by deducting your actual expenses as normal. You'll want to work out which option leaves you better off.

Working through these specific rules can be challenging, but you don't have to figure it all out on your own. The team at Stewart Accounting Services lives and breathes this stuff, helping landlords across the UK stay compliant and tax-efficient. If you need a hand with your property tax return, visit us at stewartaccounting.co.uk to learn how we can support you.