Stepping into the world of self-employment is liberating, isn't it? You're your own boss, you set the schedule. But with that freedom comes a big responsibility: handling your own taxes. One of the first things you learn is that when it comes to HMRC, deadlines are everything. Missing a key date isn't just a minor slip-up; it can lead to automatic penalties and a whole lot of stress you just don't need.

Your Essential Map to Self-Employed Tax Deadlines

Think of this guide as your personal roadmap to a smooth and painless tax season. We're going to break down every important date you need to have circled in your calendar, covering everything from getting registered with HMRC to filing your return and paying what you owe. It’s your financial compass, designed to help you navigate the tax year with confidence and sidestep any expensive surprises.

The key is to see the tax year not as one single, terrifying deadline, but as a cycle of manageable milestones. Once you understand the rhythm, you'll feel much more in control.

The Most Important Dates

For the majority of self-employed people here in the UK, the entire tax year really boils down to a handful of core deadlines. Getting these locked into your calendar is absolutely non-negotiable if you want to stay on HMRC's good side and avoid penalties.

-

5th October: If you started your business in the last tax year (which runs from 6th April to 5th April), this is your deadline to tell HMRC you need to file a Self Assessment tax return. Don't miss it!

-

31st January: This is the big one. It's the final day to get your online tax return filed and to pay the tax bill you've calculated.

-

31st July: This is when your second 'Payment on Account' is due. In simple terms, it's an advance payment towards your next tax bill.

Try not to see these dates as threats. They’re actually helpful checkpoints designed to spread your tax obligations across the year. This makes everything far more manageable than being hit with one enormous bill out of the blue.

By getting comfortable with this annual rhythm, you can turn tax admin from something you dread into just another predictable part of running your business. Let's walk through what each of these deadlines really means for you, so you can always stay one step ahead.

Navigating Key Self Assessment Dates

The UK tax year can feel like a tangled web of dates, but once you get the hang of it, there’s a clear rhythm. It runs from 6th April one year to 5th April the next, and getting these key milestones into your diary is the first, and most important, step to staying on HMRC’s good side. Forgetting a date isn't just a simple mistake; it's a surefire way to get an unwanted penalty notice in the post.

Your whole Self Assessment journey kicks off with one non-negotiable deadline. You must register for Self Assessment by 5th October after the tax year in which you first started earning self-employed income. This is you officially telling HMRC, "I have untaxed income to declare and I'll be sending you a tax return." It’s a simple but crucial step that trips up a surprising number of new business owners.

The Major Filing and Payment Deadlines

While registration gets you in the system, 31st January is the big one—the main event in the tax calendar for most. This is the absolute final day for filing your online tax return and paying what you owe.

But it’s a bit more complicated than just one payment. This date is actually a triple-threat:

- It’s the deadline for submitting your online tax return.

- It’s when you must pay any leftover tax from the previous year (your 'balancing payment').

- It's also when you make your first 'Payment on Account' for the current tax year.

Think of Payments on Account as pre-paying your next tax bill in two instalments, helping you to spread the cost and avoid a single, massive bill. The second instalment is then due on 31st July. Getting your head around this cycle—file, pay last year's balance, and pre-pay for this year—is the key to managing your cash flow without any nasty surprises.

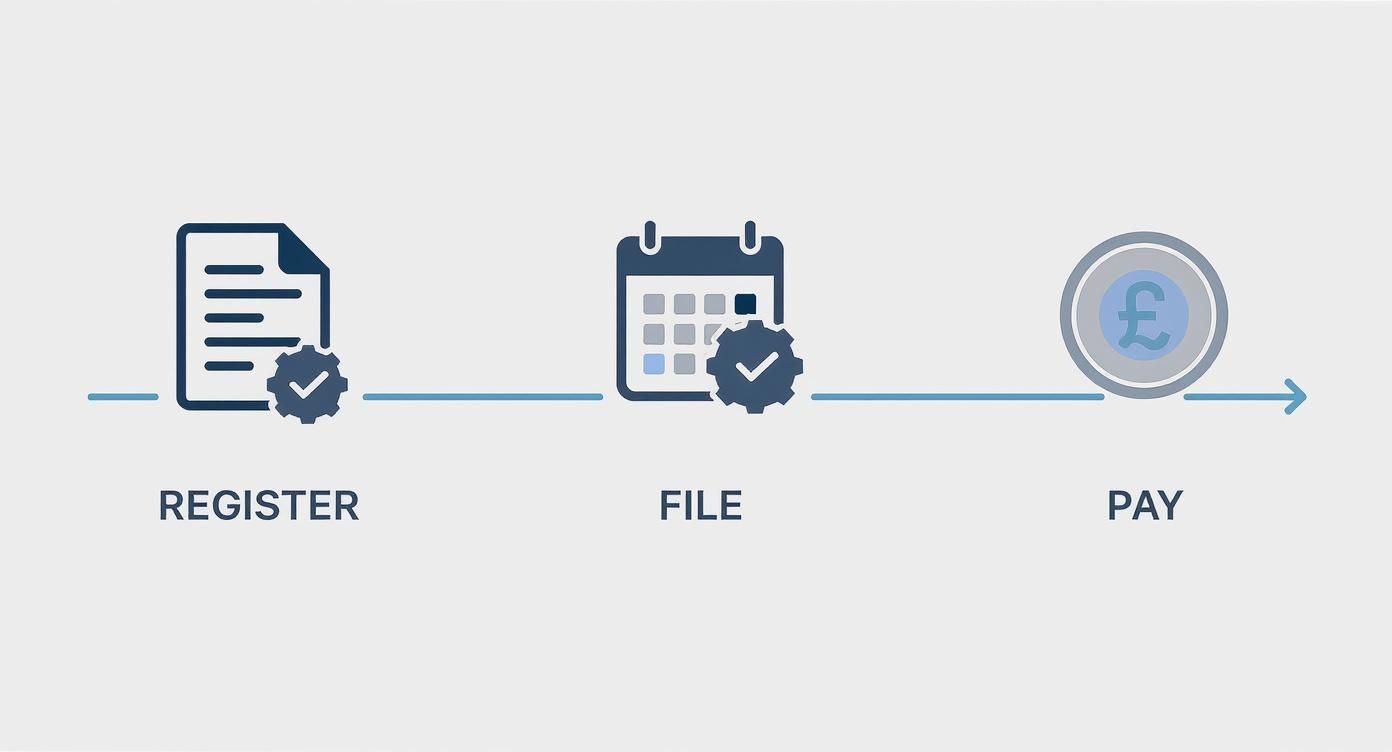

This simple graphic lays out the core journey you'll follow.

As you can see, it's a logical three-stage process: get registered, get your return filed, and get the tax paid. Each stage has its own firm deadline that you can't afford to miss.

Paper vs Online: A Critical Distinction

It’s really important to remember that how you file changes your deadline. That famous 31st January date is strictly for online tax returns.

If you’re one of the few who still prefer to file by post, your deadline is much, much earlier. Paper tax returns must be with HMRC by midnight on 31st October. Because almost everyone files online now, the January date gets all the attention, but be warned: missing the October paper deadline will land you the exact same penalties.

You can find more official dates and guidance on the key deadlines for the UK self-employed on the government's website. Getting these dates firmly marked in your calendar turns the self-employed tax deadline from something to dread into a predictable part of your business routine.

Getting to Grips with Payments on Account and Balancing Payments

One of the biggest financial hurdles for anyone new to self-employment is getting their head around Payments on Account. It can seem confusing at first, but it’s really just HMRC's way of stopping you from getting hit with a massive, unexpected tax bill once a year. Think of it as a "pay-as-you-go" system that helps you spread the cost.

If your last Self Assessment tax bill was over £1,000, HMRC will almost always ask you to make two advance payments towards your next tax bill. It's important to remember this isn't an extra tax—it's just you paying your expected bill in instalments.

How Do Payments on Account Actually Work?

The system is pretty straightforward. Each of the two payments is usually 50% of your previous year’s tax bill. The deadlines are set in stone and are crucial dates to have in your calendar.

- First Payment on Account: Must be paid by midnight on 31st January.

- Second Payment on Account: Must be paid by midnight on 31st July.

The whole idea is to keep your tax payments ticking over throughout the year, much like an employee pays tax through PAYE from their monthly salary. This approach can make managing your business's cash flow a lot less stressful.

Naturally, there are times when you might not need to make these payments, especially if your income has taken a dive. You can find out more by reading our guide on when you don’t need to make payments on account.

What is a Balancing Payment?

Once you've made both advance payments, there’s often one final piece of the puzzle: the balancing payment. This is simply the difference between what you've already paid in advance and what your final tax bill for that year actually is.

This final payment is also due by the 31st January deadline. Yes, that means it's due on the same day as your first Payment on Account for the following tax year, which can sometimes catch people out.

Let's Walk Through an Example

Imagine your tax bill for the 2023/24 tax year comes to £4,000. Because it's over £1,000, you'll have to make Payments on Account for the upcoming 2024/25 tax year.

- Each payment will be £2,000 (50% of £4,000).

- You'd pay the first £2,000 on 31st January 2025.

- You'd pay the second £2,000 on 31st July 2025.

Now, fast forward. You complete your 2024/25 tax return and discover your actual bill for that year is £5,000. You've already paid £4,000 towards it.

This means your balancing payment is the remaining £1,000. This amount is due on 31st January 2026. On that very same day, you'll also have to pay your first Payment on Account for the next tax year (2025/26). Getting this cycle clear in your mind is absolutely key to staying on top of your tax affairs.

Understanding the Real Cost of Missing a Deadline

Let's be clear: HMRC’s penalty system isn't something you can ignore. It's designed to be a serious deterrent, and the costs rack up much faster than most people realise. Missing the self-employed tax deadline by a single day means an instant £100 penalty. That applies even if you have no tax to pay or have already paid everything you owe. This is purely a penalty for filing late, not paying late.

But that initial £100 is just the starting pistol. The financial hit gets much worse the longer you leave it, creating a snowball of charges that can quickly become overwhelming.

The Escalating Penalty Timeline

If your tax return is still missing after three months, HMRC can start imposing a daily penalty of £10, up to a maximum of £900. This is added on top of that first £100 fine. And it doesn't stop there.

- At six months late: You'll be hit with another penalty of 5% of the tax you owe or £300, whichever is higher.

- At 12 months late: Another charge of 5% of the tax due or £300 (again, whichever is greater) is applied. In the most serious cases, particularly where HMRC believes you're deliberately withholding information, the penalties can be far, far higher.

It's crucial to grasp that these are just the penalties for filing your return late. The penalties for paying your tax bill late are a completely separate system and they stack on top of these. Understanding the full picture of penalties for late tax payments is absolutely essential.

Late Payment Surcharges and Interest

On top of everything else, if you haven't paid your bill, late payment surcharges kick in. A charge of 5% of the outstanding tax is levied if your payment is 30 days late. This is repeated with further 5% charges if the tax is still unpaid after six months, and again at 12 months. To add insult to injury, HMRC also charges interest on both the unpaid tax and the penalties themselves, which clocks up every single day.

You might think this is a rare problem, but it’s a surprisingly common and costly mistake. Around 1.1 million taxpayers missed the deadline for the 2023 to 2024 tax year, triggering this very cascade of fines and interest. You can read more about these figures on the official government website. These numbers really drive home how vital it is to treat tax deadlines with the respect they command.

Your Year-Round Plan to Beat the Tax Deadline

A stress-free tax season doesn’t just happen in January. It's the result of good habits built up over the entire year. The secret is to stop thinking of the self employed tax deadline as a last-minute emergency and start treating tax prep as just another part of running your business. This simple shift in mindset turns the whole process from a dreaded scramble into something calm and manageable.

What you need is a simple, year-round system that keeps you organised and firmly in control.

April to June: Starting the New Tax Year Right

When the new tax year kicks off on 6th April, it's the perfect moment to lay down good financial foundations. Instead of just carrying on with last year's shoebox of crumpled receipts, get a proper system in place. This could be a well-organised spreadsheet, a bit of accounting software, or even just a set of clearly labelled digital folders for your invoices and expenses.

The most important thing is to create a clear, consistent process from day one. If you're not sure where to begin, our detailed guide on the best practices for self-employed record keeping is a fantastic resource for building a solid system.

Towards the end of this first quarter, do a quick financial check-in. Tally up your income and add up your business expenses. You're not filing anything yet; this is all about getting an early picture of your profitability. It helps you estimate what your tax bill might look like, so you can start putting money aside straight away and avoid any nasty cash flow surprises later on.

July to September: The Mid-Year Review

By the time summer rolls around, you should have a good rhythm going with recording your transactions. Now is the ideal time for your second quarterly review. How does your income and spending stack up against the first quarter? Are your profits heading up or down? This review is especially crucial if you make Payments on Account.

If it looks like your income is going to be significantly lower than the previous year, you can actually ask HMRC to reduce your payments. On the flip side, if you're earning a lot more, you’ll know you need to be tucking away extra cash for that final tax bill.

Think of these quarterly check-ins like a pilot checking their instruments mid-flight. They aren't just for compliance; they provide vital data that helps you steer your business financially and make better decisions long before the tax deadline arrives.

October to December: Preparing for an Early Submission

Autumn is when you should start gathering all your official paperwork. This means getting together:

- Bank Statements: Make sure you have the full statements for all your business and relevant personal accounts.

- Invoices: Collate every single sales invoice you issued during the tax year.

- Receipts: Round up all your digital and paper receipts for business expenses.

Because you’ve been keeping organised records all year, this step should be straightforward. The aim here is to get your tax return filed in December, not January. Remember, filing early doesn’t mean you have to pay early—the payment deadline doesn’t change. Submitting your return before the Christmas break simply means you get it done and dusted, avoiding the inevitable January website crashes and starting the new year with a clear head.

How Professional Support Simplifies Your Tax Obligations

Trying to run a business while simultaneously keeping track of ever-shifting tax deadlines can feel like spinning plates. For many self-employed people, the constant pressure to stay organised and hit every single date is a huge source of stress. This is where getting a professional on your side can completely change the game, turning tax season from a dreaded chore into a straightforward business task.

At Stewart Accounting Services, we live and breathe this stuff. We specialise in helping self-employed individuals and partnerships navigate the maze of HMRC's requirements with confidence. Our job isn't just to fill in forms; it's about giving you total peace of mind. We take ownership of making sure your records are spot-on and that you claim every allowable expense you're entitled to, which helps keep your tax bill as low as legally possible.

Freeing You Up to Focus on Your Business

Our main goal is simple: to make sure every self employed tax deadline is met without fail. This shields you from those automatic penalties and the financial worry that comes with them. By taking on the detailed paperwork and dealing with HMRC for you, we lift that administrative weight right off your shoulders.

This frees you up to pour your time and energy back into what you’re brilliant at—running and growing your business. Instead of losing hours trying to make sense of tax legislation or stressing about an upcoming payment, you can concentrate on looking after your clients and chasing new opportunities.

By handing over your tax compliance, you're not just buying a service. You're investing in more time, less stress, and the confidence that your finances are being handled with expert care.

Let us take the annual tax headache off your to-do list for good. We can help you stay compliant, get financially organised, and stay focused on your business goals, making sure you never have to worry about a missed deadline again. We’ll manage the dates so you can manage your future.

Common Questions About Tax Deadlines

When you're self-employed, tax deadlines can throw up a lot of questions, especially when your business situation changes from one year to the next. Getting your head around these rules is crucial for avoiding a surprise penalty from HMRC. Let's tackle some of the most common queries we hear.

What Should I Do If I Cannot Pay My Tax Bill on Time?

First things first: don't panic, and definitely don't ignore the problem. If you know you're going to struggle to pay your tax bill, the best thing you can do is get in touch with HMRC straight away, ideally before the self employed tax deadline arrives. Burying your head in the sand will only make things worse, as interest and penalties will start racking up from day one.

HMRC can be surprisingly reasonable if you're upfront with them. They have a system called a 'Time to Pay' arrangement, which could let you break down your tax bill into more manageable monthly payments. If you owe less than £30,000, you might even be able to set this up yourself online. Taking that first step shows HMRC you're being responsible, which goes a long way.

Can I Reduce My Payments on Account If My Income Falls?

Yes, you can, and you absolutely should if your income has dropped. Payments on Account are essentially HMRC's best guess at your next tax bill, based entirely on your last one. If this year has been tougher and you've earned less, it makes no sense to overpay them and leave yourself short.

You can apply to lower your Payments on Account through your government gateway account or by using form SA303. But a quick word of warning: be careful with your estimate.

If you slash your payments too much and it turns out you've underpaid, HMRC will charge you interest on the amount you owe. It’s always better to be a little cautious with your forecast or chat with an accountant to get the numbers right.

Do I Have to File a Tax Return If I Made a Loss?

In a word, yes. If HMRC has told you to file a tax return, you have to do it, even if you made a loss and don't owe a penny in tax. It’s a common misconception, but failing to file will still land you with that automatic £100 late filing penalty.

Besides, reporting a loss is actually a smart move. It means you can carry that loss forward to reduce your tax bill in future, more profitable years. Sometimes you can even use it to lower the tax you owe on other income in the same year. So, think of it less as a chore and more as a vital piece of financial housekeeping for your business's future.

Dealing with these specific situations and making sure every self employed tax deadline is met can feel like a lot to handle on your own. At Stewart Accounting Services, we provide the clarity and support you need. We'll manage your deadlines and keep you on the right side of HMRC, so you can get back to what you do best—running your business. Contact us today to see how we can help.