When you're self-employed, three dates should be permanently etched in your calendar: 5 October for registering with HMRC, 31 January for filing your online tax return and settling your tax bill, and 31 July for your second payment on account. These aren't just suggestions; they’re the core dates that keep you on the right side of the tax man.

A Quick Guide to Self-Employment Tax Deadlines

Getting to grips with your tax duties can feel like a maze at first, but knowing the key deadlines is your best starting point. Everything revolves around the UK tax year, which runs from 6 April to 5 April of the next year. From telling HMRC you've started your business to filing your return and paying what you owe, all deadlines are tied to this cycle.

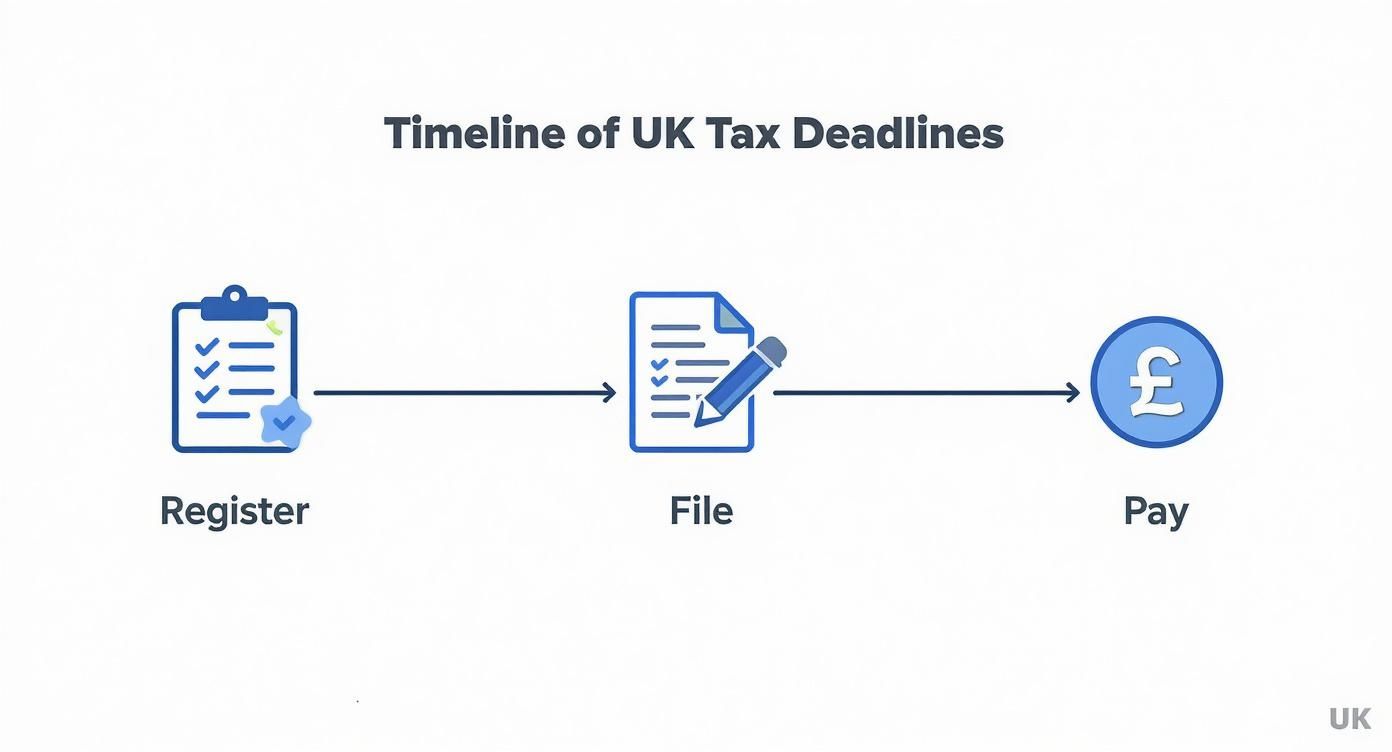

To give you a clearer picture of how these dates fit together across the year, this simple timeline lays out the main deadlines you can't afford to miss.

As you can see, your tax responsibilities are spread out – it's not all a last-minute rush in January. To make it even easier, I've put together a quick-reference table below. Following that, we'll dive deeper into what each deadline actually means for you, helping you stay compliant and avoid any nasty surprises or penalties.

Key UK Self-Employment Tax Deadlines at a Glance

Here’s a snapshot of the most important dates every self-employed person in the UK needs to know for a typical tax year. Think of this as your cheat sheet for staying organised.

| Deadline Date | Task to Complete | Who It Affects |

|---|---|---|

| 5 October | Register for Self Assessment with HMRC. | Anyone who became self-employed during the previous tax year. |

| 31 October | Deadline for submitting your paper tax return. | Individuals who choose to file by post instead of online. |

| 31 January | Deadline for online Self Assessment tax returns. | All self-employed individuals filing their tax return online. |

| 31 January | Pay any tax you owe (balancing payment) and your first payment on account. | Everyone who owes tax for the previous tax year. |

| 31 July | Pay your second payment on account. | Self-employed individuals whose tax bill was over £1,000 the previous year. |

Keeping these dates handy is the first step to managing your finances with confidence and avoiding unnecessary stress. Now, let's explore what each of these deadlines involves in more detail.

Getting to Grips with Your Core Tax Duties

Before we dive into the specific self-employment tax deadlines, it’s really important to get a clear picture of what HMRC expects from you. When you're self-employed, you're in charge of telling them about your income through a system called Self Assessment. This involves filling out a tax return each year, where you lay out your total earnings and any business expenses you can claim.

You're legally required to file a return if you earned over £1,000 from your self-employment activities during the last tax year. Keeping your financial records straight is half the battle; for a deeper dive into managing your books, this UK accounting and finance outsourcing guide is a great resource. The main taxes you'll be dealing with are Income Tax and National Insurance Contributions.

The Main Taxes You'll Pay

As a self-employed individual, you'll mainly come across two types of National Insurance:

- Class 2 NICs: This is a fixed weekly amount you pay if your profits are above a certain level, known as the Small Profits Threshold.

- Class 4 NICs: This is calculated as a percentage of your profits once they go over a specific annual limit.

Then there's the concept of 'payments on account', which can catch people out. Think of these as advance payments towards your next tax bill. HMRC splits them into two chunks, due in January and July. You'll usually have to make these payments if your last tax bill was more than £1,000 and less than 80% of it was already paid through other means (like PAYE). Getting your head around these duties is the first, most crucial step to staying on top of your taxes and avoiding any nasty surprises or penalties.

Meeting the HMRC Registration Deadline

Before you can even think about filing a tax return, your first official step into the world of self-employment is letting HMRC know you exist. This means registering for Self Assessment, and getting this first deadline right is crucial to avoid any headaches down the line.

The key date for your diary is 5 October. This is the deadline to register for Self Assessment in the tax year after the one you started trading in.

Let’s break that down. If you started your business anytime between 6 April 2023 and 5 April 2024 (the 2023/24 tax year), you need to tell HMRC by 5 October 2024. This gives them plenty of time to get you set up on their system well before the tax return is actually due.

How to Get Registered

The quickest and easiest way to register is online. You'll just need to have a few basic details ready to go:

- Your full name and home address

- Your National Insurance number

- The date you officially started your business

After you've submitted your details, HMRC will post you a Unique Taxpayer Reference (UTR) number. This usually arrives within 10 working days. For a more detailed guide on the whole process, we've covered everything you need to know about how to register as a sole trader.

Make sure you keep that UTR number somewhere safe – it's your main identifier for anything and everything to do with your tax affairs.

Key Deadlines for Filing Your Tax Return

When you're self-employed, you've got a couple of ways to file your Self Assessment tax return, and each comes with its own firm deadline. Getting these dates straight is absolutely essential if you want to steer clear of penalties.

First up is the traditional paper tax return. If you're going old-school and posting your forms, you need to have it submitted by midnight on 31 October. Honestly, this is becoming a pretty rare choice these days, mainly because it gives you a much tighter window to get everything organised.

The Online Filing Deadline

The vast majority of people now file online, and for good reason. The big draw is the later deadline: you have until midnight on 31 January to submit your return.

The advantages of doing it online are pretty clear:

- Peace of Mind: You get an instant confirmation from HMRC, so you know for sure it's landed safely.

- Fewer Mistakes: The online portal does all the sums for you, which seriously cuts down the risk of making a costly error.

- Extra Time: Crucially, you get a whole extra three months to sort out your paperwork and file.

It's no surprise that most people choose this route. For the 2022 to 2023 tax year, a massive 11.5 million people filed online before the January cut-off. If you're interested in taxpayer trends, you can read more about it on the official government website.

Expert Tip: Whatever you do, don't leave it until the last few days of January. The HMRC website can get incredibly slow under the strain of last-minute filers. Aim to get it done well in advance to give yourself breathing room for any unexpected hitches.

Getting to Grips with Payments on Account

Payments on account are a frequent source of confusion for the self-employed, but the concept is fairly straightforward. Think of them as advance payments on your next tax bill, designed to help you spread the cost instead of facing a single, large payment.

HMRC will ask you to make payments on account if two conditions are met: your last Self Assessment tax bill was more than £1,000, and less than 80% of the tax you owed was collected at source (for example, through PAYE from an employment).

There are two payments, each with a firm deadline:

- First payment on account: Due by midnight, 31 January.

- Second payment on account: Due by midnight, 31 July.

Each of these payments is calculated as 50% of your previous year’s tax bill. It's really important to remember that these are just prepayments based on what you earned last year, not the final amount you'll owe for the current year.

How are Payments on Account Calculated?

Let's walk through a quick example. Say your tax bill for the 2023/24 tax year came to £3,000. HMRC works on the assumption that you'll probably earn a similar amount in the 2024/25 tax year.

Based on this, your payments on account would be:

- First Payment: You'd pay £1,500 (50% of the previous £3,000 bill) by 31 January 2025.

- Second Payment: You'd pay the other £1,500 by 31 July 2025.

These two instalments total £3,000. Once you complete your 2024/25 tax return (which is due by January 2026), HMRC will calculate your actual tax liability. If it turns out your bill for 2024/25 is actually £3,500, the £3,000 you've already paid is deducted. This leaves a balancing payment of £500 left to clear.

You don't always have to make these advance payments. If your income has dropped, or you expect it to, you can ask HMRC to reduce your payments on account. For a deeper dive into this, see our guide on when you don't need to make payments on account.

The Real Cost of Missing Tax Deadlines

Getting your head around the consequences of missing self employment tax deadlines is probably the best incentive you'll get for staying on top of your paperwork. HMRC has a pretty strict penalty system that kicks in automatically, so any delay can start to hurt your wallet almost immediately.

The second the clock ticks past midnight on the 31 January filing deadline, an instant £100 penalty is slapped onto your account. What’s crucial to understand is that this fine applies even if you have no tax to pay or have already paid everything you owe. It’s purely for the late submission, and it’s just the start.

Escalating Penalties for Late Filing

If your tax return continues to go unfiled, the costs really start to snowball. HMRC’s penalty structure is designed to get progressively more severe to strongly encourage you to file.

Here’s how it breaks down:

- After 3 months: They can start charging a daily penalty of £10 for up to 90 days. This can quickly add another £900 to your bill.

- After 6 months: An additional penalty is applied. This will be 5% of the tax you owe or £300, whichever figure is higher.

- After 12 months: You guessed it – another penalty. It’s a further 5% of the tax due or £300, again, whichever is the greater amount.

When you add it all up, being a full year late could see you facing at least £1,600 in late filing penalties. And remember, that’s before they even start charging interest on the actual tax you haven't paid.

It’s easy to see how these costs can become a real worry. If you find yourself in a difficult position, take a look at our guide on what happens if you cannot pay your tax bill for some practical advice on what to do next.

Common Mistakes and How to Sidestep Them

Navigating the world of self-employment tax can feel like a minefield, and a few common tripwires catch out even seasoned business owners. One of the biggest, without a doubt, is under-reporting income. It's usually an honest mistake, but it can land you in hot water with HMRC.

Research shows just how common this is. While about 36% of all Self Assessment taxpayers under-report what they owe, that number skyrockets to nearly 60% for the self-employed, according to analysis of HMRC's own audit data. You can dig into the full findings on this tax gap yourself. More often than not, it simply comes down to messy or incomplete records.

Another classic blunder is not putting enough money aside for your tax bill throughout the year. Getting hit with a large demand on 31 January is a nasty shock if you haven't been saving, leading to immediate cash flow problems and the panic of finding a lump sum you weren't prepared for.

Getting Ahead of the Game

Thankfully, you can steer clear of these issues with a bit of forward planning. It's all about building good financial habits from the get-go, making sure your tax return is spot-on and you're ready when it's time to pay.

Here are a few practical steps that make a huge difference:

- Embrace Accounting Software: Using a tool like Xero or QuickBooks is a game-changer. They automatically track your income and help you categorise expenses, which seriously cuts down the risk of errors and forgotten details.

- Get a Separate Bank Account: This is non-negotiable. Have all your business income and outgoings flow through one dedicated account. It makes it infinitely easier to see exactly what you've earned and spent when the time comes.

- Start a 'Tax Pot': Every time a client pays you, immediately move a percentage—a safe bet is 25-30%—into a separate savings account. Think of it as HMRC's money, not yours. That way, the funds are ring-fenced and ready for you when the payment deadline hits.

Putting these simple systems in place doesn't just reduce the stress of tax season; it minimises your risk of an HMRC enquiry and lets you manage your finances with confidence.

Your Top Questions Answered

When you're self-employed, tax deadlines can throw up a few tricky questions, especially when your circumstances aren't straightforward. Here are some clear answers to the queries we hear most often, helping you stay on top of your tax affairs with confidence.

What If I Can't Afford to Pay My Tax Bill?

The minute you realise you can't pay your tax bill, the absolute best thing you can do is get in touch with HMRC. Don't bury your head in the sand. Ignoring the problem will only make it worse, as interest will start piling up on whatever you owe.

HMRC can often help by setting up a ‘Time to Pay’ arrangement. This is simply an agreement that lets you pay what you owe in manageable instalments over a few months. Remember, even if you can't pay, you must still file your return on time. The penalties for late filing are completely separate from the interest charged for late payment.

Do I Have to File a Tax Return If I Made a Loss?

Yes, you definitely still need to file. Once you're registered for Self Assessment, the legal requirement is to submit a tax return every single year, regardless of whether you made a profit or not.

In fact, there's a good reason to report a loss. You can carry that loss forward to offset against profits in future years. This means you’ll end up paying less tax down the line when your business starts turning a healthy profit.

It's crucial to remember this: failing to file a return, even when you owe nothing, triggers an automatic £100 late filing penalty from HMRC. It always pays to file on time and report the situation correctly.

I've Made a Mistake on My Tax Return. How Do I Fix It?

Don't panic—mistakes happen, and HMRC has a pretty simple process for putting things right. You can amend your tax return online for up to 12 months after the original filing deadline has passed.

Just log in to your HMRC online account, go to the right tax year, and choose the option to make a change. If you spot an error after that 12-month window has closed, you'll need to write to HMRC directly. In your letter, you'll have to explain the mistake and provide the correct figures.

Feeling bogged down by all the dates and details? The team at Stewart Accounting Services can take the entire Self Assessment process off your hands, making sure you stay compliant and stress-free. Pop over to https://stewartaccounting.co.uk to see how we can help.