When you're a sole trader, your tax return is essentially your annual financial report card for HMRC. It’s officially known as a Self Assessment tax return, and it’s the process you use to tally up your business income and expenses to work out how much Income Tax and National Insurance you owe on your profits.

If you’ve earned more than £1,000 from your self-employment during the tax year, you’re legally required to file one.

Understanding Your Sole Trader Tax Obligations

Going self-employed is liberating. You're the boss, you set the hours, and you reap the rewards. But with that freedom comes the responsibility of handling your own taxes. Unlike being on a payroll where tax is whisked away automatically through PAYE, as a sole trader, the buck stops with you. It’s your job to tell HMRC what you’ve earned.

While it might seem daunting, remembering the many benefits of being self-employed can keep you motivated through the admin.

The entire system really boils down to one crucial number: your taxable profit. This isn't just your total sales revenue (your turnover). Instead, it’s what's left after you subtract all your legitimate, allowable business expenses. Your final tax bill is calculated on this profit figure, not your total income.

Key Terms You Need to Know

Getting your head around a few key terms will make the whole process feel a lot less like learning a new language. These are the fundamentals of any sole trader tax return.

- Self Assessment: This is simply what HMRC calls the system for collecting tax from people who have untaxed income, which includes almost all sole traders.

- Turnover: All the money your business has brought in from sales before taking away any costs. It's your top-line revenue.

- Allowable Expenses: These are the day-to-day running costs of your business that you can legally deduct from your turnover. Think office supplies, business mileage, or accountancy fees.

- Taxable Profit: The all-important number you get after subtracting your allowable expenses from your turnover. This is the figure you’ll actually pay tax on.

Your Main Tax Responsibilities

As a sole trader, you'll be paying two main taxes on your profits: Income Tax and National Insurance Contributions (NICs). Both are calculated on a tiered basis, so the more profit you make, the higher the rate you pay.

If you're ever unsure about whether you need to file, our guide on who must send in a tax return breaks it down clearly.

A lot of people think they only need to register with HMRC once they're making a decent profit, but that's a costly mistake. The rule is simple: you must register for Self Assessment by the 5th of October following the end of the tax year in which you started trading. Miss that deadline, and you could be facing penalties before you've even filed your first return.

Organising Your Finances for a Stress-Free Filing

The secret to a smooth tax season isn’t some magic formula; it’s having your records in order long before the January deadline looms. Think of it as a year-long project, not a frantic last-minute scramble. Getting into good habits from day one is honestly the best way to make your sole trader tax return less of a headache.

At its core, record-keeping is about keeping proof of your business’s income and its expenses. This isn’t just good practice; it's a legal requirement. Remember, HMRC can ask to see your records for up to five years after the tax year they relate to.

Essential Documents to Keep

Your filing system doesn't need to be fancy, but it absolutely must be consistent. Whether you prefer a classic shoebox, digital folders, or dedicated software, make sure you hold onto the following:

- All sales invoices you've sent out to clients.

- Receipts and invoices for every business expense, from a £2 coffee with a client to a £2,000 new laptop.

- Bank statements for your business account (and personal ones, if you’ve mixed in any business transactions).

- Records of any personal money you've put into the business.

This paperwork is your evidence if HMRC ever questions an expense claim. Without a receipt, you technically can't claim the cost.

It's a classic mistake to think small cash purchases don't matter. But if you're a builder who buys materials with cash every week, those small amounts add up to a significant deduction that could lower your taxable profit by thousands over the year.

Choosing Your Record-Keeping System

The best system is the one you'll actually stick with. You don't need to splash out on a complicated setup, especially when you're just getting started.

A simple spreadsheet can work perfectly well. Just create columns for the date, a description of the income or expense, the amount, and a category (like 'Office Supplies' or 'Travel'). This method is free and gives you complete control.

However, as your business grows, you might find accounting software more efficient. Tools like Xero or QuickBooks can connect directly to your business bank account, automatically categorising transactions and generating reports. While there's a monthly cost, the time saved and the accuracy gained often make it a worthwhile investment, simplifying your end-of-year calculations massively.

Our comprehensive guide on self-employed record-keeping dives deeper into these options.

Adopting these habits will not only make filing your sole trader tax return faster but also give you solid proof for every single claim you make.

Getting to Grips with Allowable Expenses to Lower Your Tax Bill

Knowing what you can legally claim as a business expense is the single most effective way to lower your final tax bill. This isn't about finding sneaky loopholes; it's simply about understanding the rules so you only pay tax on your actual profit, not your total turnover. Honestly, this is where you can make a real, tangible difference to your bottom line.

Think of it this way: every pound you spend on a legitimate business cost is a pound less of profit that HMRC can tax. From the software subscription a freelance graphic designer relies on, to the new drill a builder needs on-site, these are all considered allowable expenses.

Day-to-Day Costs vs. Major Assets

First things first, it's crucial to get the distinction between two main types of expenses right. Most of your claims will be for the everyday running costs—the things your business consumes just to keep the lights on.

These typically include:

- Office Costs: This covers things like rent for your business premises, stationery, phone bills, and postage.

- Travel Costs: Fuel for business journeys, train tickets to meet clients, or parking fees all count.

- Stock or Raw Materials: The cost of goods you buy to sell or the materials you use to provide your service.

- Professional Fees: Payments to your accountant or solicitor, or the cost of professional insurance.

However, bigger purchases for items you intend to keep and use in your business long-term—like a company van or a powerful new computer—are treated differently. These are known as capital assets. Instead of listing them as a simple expense, you claim for them using 'capital allowances', a process that lets you write off the value of the asset over time.

For a really detailed breakdown, our complete list of sole trader expenses covers pretty much everything you might be able to claim.

The Tricky Bits: Home Office and Vehicle Expenses

Two of the most common—and often confusing—areas for sole traders are claiming for home office use and business mileage. Thankfully, HMRC provides clear methods for calculating these to ensure you claim a fair and proper proportion.

When it comes to your home office, you have two options. You can either meticulously calculate the exact proportion of your household bills (like electricity, gas, and council tax) that relates to your business use. Or, you can use HMRC's 'simplified expenses'—a flat monthly rate based on how many hours you work from home.

It's a similar story for your vehicle. You can track every single cost—fuel, insurance, repairs, MOT—and work out the business percentage. The alternative is the simplified mileage method, which allows you to claim a flat rate of 45p per mile for the first 10,000 business miles and 25p for every mile after that.

A common mistake I see is new sole traders overlooking the simplified methods, assuming they're less valuable. In reality, for anyone who wants to avoid the headache of tracking every last receipt, they provide a straightforward, HMRC-approved way to claim what you're owed and save a huge amount of admin time.

How Expenses Actually Cut Your Tax Bill

So, why is tracking all this so important? Because every single expense directly reduces your taxable profit.

In the UK, sole traders pay tax and National Insurance based on their profits, not their total income. Below is a quick summary of the main thresholds you need to be aware of.

Key UK Tax and National Insurance Thresholds for Sole Traders

| Tax/Contribution Type | Profit Threshold | Applicable Rate |

|---|---|---|

| Personal Allowance | Up to £12,570 | 0% (Tax-Free) |

| Basic Rate Income Tax | £12,571 to £50,270 | 20% |

| Higher Rate Income Tax | £50,271 to £125,140 | 40% |

| Additional Rate Income Tax | Over £125,140 | 45% |

| Class 4 National Insurance | £12,570 to £50,270 | 6% |

| Class 4 National Insurance | Over £50,270 | 2% |

This structure makes every allowable expense claim crucial. A £100 expense doesn't just save you £100; it reduces your taxable profit by £100, which in turn lowers the final amount you owe in Income Tax and National Insurance.

To really understand your business's financial health, it’s essential to know how to calculate net income and maximize profits. By diligently recording every cost, you give yourself the best possible chance of filing an accurate tax return and ensuring you don't overpay a single penny.

Navigating the HMRC Online Filing Process

Right, you’ve got your records in order and your expenses tallied up. Now for the final hurdle: actually filing your tax return. For most sole traders, the HMRC online portal is the way to go. It can feel a bit daunting at first, but once you get the hang of it, it's a surprisingly logical system. Let’s walk through it.

First things first, you'll log in with your Government Gateway ID. The system will then ask you to confirm your personal details and start tailoring your return. This bit is crucial. HMRC asks a series of questions to figure out which sections of the tax return you actually need to fill in.

As a sole trader, you must tick the box that says you've received income from self-employment. This simple action tells the system to add the "self-employment" pages to your return. Miss this, and you won’t have anywhere to declare your business income.

Entering Your Business Details

Once you've done that, you’ll get to the supplementary pages. You won’t see form numbers like SA103S or SA103F, but the online questions are based directly on them. Generally, if your turnover was below the £85,000 VAT threshold, you’ll be answering the "Short" version; if it was higher, you'll get the "Full" set of questions.

You'll start with the basics – your business name, what you do, that sort of thing. Then you get to the numbers. This is where your good record-keeping pays off. You'll need two main figures:

- Your total turnover: This is every penny your business earned before taking off any costs.

- Your total allowable expenses: This is the grand total of all the business costs you've carefully calculated.

You just pop these two figures into separate boxes. The HMRC system does the maths for you, subtracting your expenses from your turnover to work out your taxable profit.

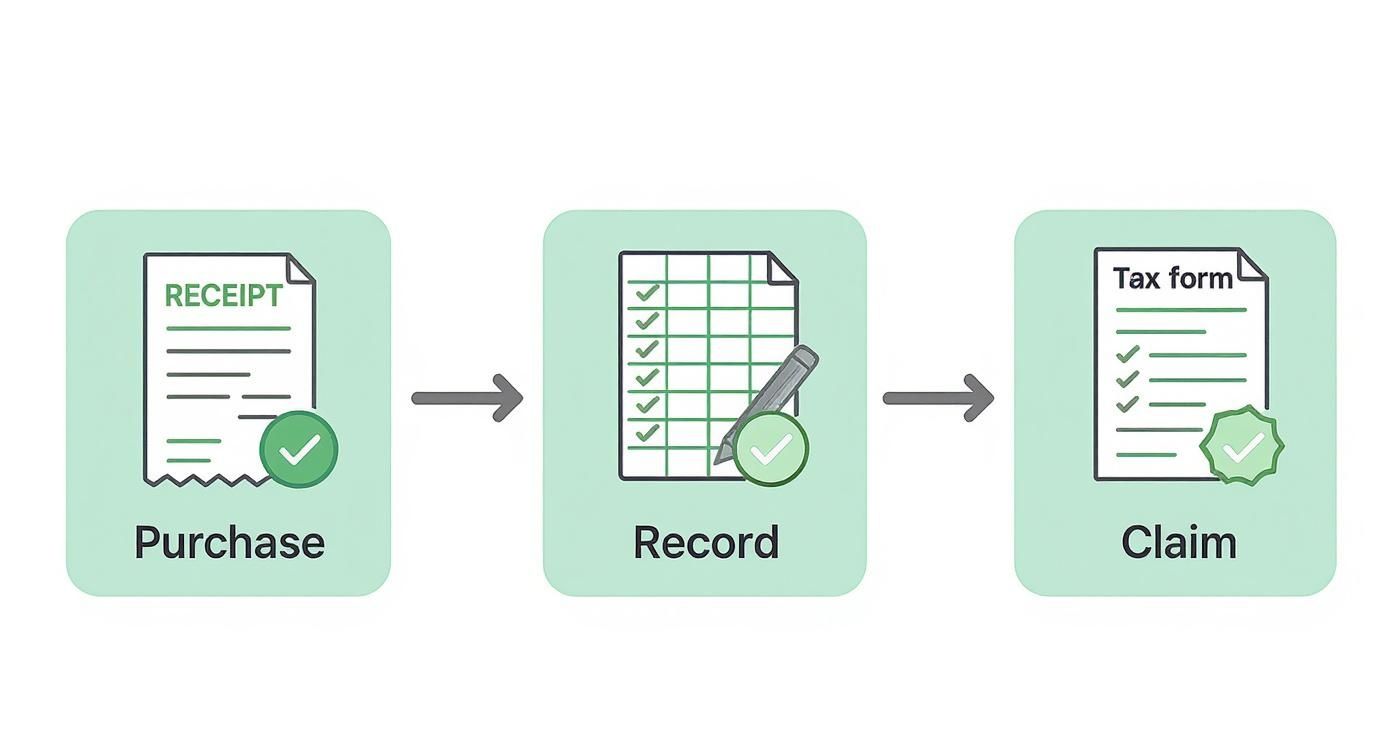

The whole process of claiming an expense is really just a three-step journey, from buying something to getting it onto your tax return.

Getting this right is the absolute foundation of an accurate tax return. Every legitimate cost you claim reduces the amount of profit you pay tax on.

Finalising and Submitting Your Return

After you've entered all your business details, the portal will guide you through any other income you need to declare, like from a PAYE job or rental properties. Once all the relevant sections are complete, you’ll land on the calculation page. Think of this as your final summary. It shows you exactly how HMRC has calculated your final tax and National Insurance bill for the year.

This is all part of a bigger shift. In the 2023-24 tax year, around 7.0 million people in the UK filed Self Assessment returns as sole traders or landlords. And the way they file is changing. Already, 63% of individuals earning over £50,000 are using software to submit their returns. With Making Tax Digital on the horizon, this trend is only going one way. You can read more about the move to digital tax submissions and see what's coming.

Crucial Tip: Don't just click through the calculation screen. Stop and review it. Does it look right? Does the final figure match what you were expecting? If anything seems off, you can go back and amend any section before you hit that final submit button.

Once you’re happy that the calculation is correct, you’re ready to submit. The moment you do, you'll get an instant confirmation receipt with a unique submission reference number. It's absolutely vital that you save a copy of this receipt and the full tax calculation. This is your proof that you filed on time. Don't skip this step

Getting Ready for Making Tax Digital

The old way of doing your tax return once a year is on its way out. HMRC is rolling out a new system called Making Tax Digital (MTD) for Income Tax Self Assessment (ITSA), which is set to completely change how sole traders report their earnings.

Instead of a frantic scramble to find receipts and invoices every January, MTD requires you to keep digital records and send quarterly updates to HMRC using compatible software. At the end of the year, you'll still need to finalise everything with a final declaration, but the bulk of the work will already be done. The idea is to make tax less of a once-a-year headache and more of a manageable, ongoing process.

If this is news to you, you're not alone. A recent survey revealed that almost 45% of UK sole traders feel unprepared for this switch. That's a huge number, and it shows just how important it is to get ahead of the curve. You can explore the full findings on digital tax readiness to see how others are feeling about the change.

Who Will MTD Affect and When?

HMRC is bringing in MTD for ITSA in stages, based on your total annual income from self-employment and property letting—that’s your turnover, not your profit.

Here are the dates you absolutely need to know:

- From April 2026: It’s compulsory for sole traders and landlords with an income over £50,000.

- From April 2027: The rules will apply to those with an income over £30,000.

What about businesses with income below £30,000? HMRC hasn't set a date for that group just yet, but it's safe to assume they'll be next in line.

Don't wait until the deadline is staring you in the face. The best reason to switch to digital software now is the clarity it gives you. You'll get a real-time estimate of your tax bill, which makes budgeting so much easier and helps you avoid that awful shock when the final payment is due.

Preparing for this means finding the right software for your business and getting into the habit of digital record-keeping now. Think of it less as a compliance chore and more as an opportunity. You'll gain a much clearer, up-to-the-minute view of your business's financial health.

Making the move early means you’ll be confident and ready when the rules kick in, avoiding any last-minute stress.

Got Questions? We’ve Got Answers

Even when you think you’ve got everything sorted, a few nagging questions can pop up while you're doing your tax return. It happens to everyone. Below, I’ve tackled some of the most common queries I hear from sole traders, with practical answers to get you over the finish line.

What Happens If I Miss the Tax Return Deadline?

Let’s be blunt: miss the 31st of January online deadline, and HMRC will hit you with an instant £100 penalty. This is automatic, and it applies even if you don't owe a penny in tax.

That’s just the start. The penalties grow the longer you leave it. Fines get added after three, six, and twelve months, and they can spiral into a seriously hefty sum. The key takeaway here is to file on time, even if you can’t pay the bill straight away. HMRC treats late filing and late payment as two separate issues, so getting the form in protects you from at least one set of escalating fines.

Can I Claim Expenses for My Car or Van?

Yes, and you absolutely should. If you use your personal vehicle for business, you can claim those running costs. HMRC gives you two ways to do this.

One method is to claim a portion of the actual running costs. This means you'll need to keep a meticulous record of everything – fuel, insurance, repairs, MOTs, the lot. You then work out the percentage of business use versus personal use and claim that portion of the total cost. It's thorough, but it’s a lot of admin.

The other, much simpler, route is to use HMRC’s ‘simplified expenses’. This is a flat mileage rate – currently 45p per mile for the first 10,000 business miles. You just need to keep a log of your business journeys. One thing to note: once you pick a method for a particular vehicle, you have to stick with it. For many, the mileage rate is a lifesaver when it comes to paperwork.

A question that always comes up is, "Do I really need an accountant?" Legally, no. Plenty of sole traders with simple finances handle their own tax return every year using HMRC's online service without any problems.

But as your business gets bigger or if your accounts start to get a bit more complicated, a good accountant is worth their weight in gold. They're experts at spotting allowable expenses you might never have thought of, making sure you’re fully compliant, and can genuinely save you time, stress, and money in the long run.

How Do I Register as a Sole Trader?

This is non-negotiable: you have to tell HMRC you’re self-employed as soon as you start trading. You can register for Self Assessment quickly and easily on the GOV.UK website.

The crucial deadline to get in your calendar is the 5th of October in your business's second tax year. So, if you started your business in June 2024 (which is in the 2024/25 tax year), you’d need to be registered by 5th October 2025. Don't let this one slip!

Feeling the tax return pressure? The team at Stewart Accounting Services can lift that weight off your shoulders. We’ll make sure your sole trader return is spot-on, you’re claiming every penny you’re entitled to, and you never have to worry about a deadline again. Get in touch with us for expert support.