Let’s be honest, the term “reverse charge VAT” can make even the most seasoned business owner’s head spin. But what if I told you it’s simpler than it sounds?

Think of a normal sale. The supplier adds VAT to their invoice, collects it from you (the customer), and then pays it over to HMRC. Simple enough. The UK reverse charge VAT just flips that process on its head.

What Is UK Reverse Charge VAT, Really?

At its heart, the UK reverse charge VAT system is an anti-fraud tool. It was specifically created to tackle a nasty problem called “missing trader” fraud. This is where a supplier charges a customer VAT, pockets the cash, and then vanishes before handing it over to HMRC.

By shifting the responsibility for accounting for the VAT to the customer, the reverse charge mechanism completely removes the opportunity for this kind of fraud.

It might feel complicated, but the logic is actually quite neat. Instead of cash for the VAT changing hands, the entire transaction becomes an accounting exercise on your VAT return. You, the customer, record the VAT you would have paid as both an output tax (what you owe HMRC) and an input tax (what you can reclaim). For most businesses, these two entries simply cancel each other out. The net result? It has a neutral effect on your cash flow for that particular transaction.

Why Does This System Even Exist?

This isn’t some brand-new idea cooked up by HMRC. The reverse charge has been around for a while, first introduced across the EU back in 1993 to combat the very same “missing trader” fraud that was costing governments a fortune. The UK simply adopted and applied it to specific sectors known to be vulnerable. If you’re curious about the backstory, you can dig into the history of reverse VAT in the UK.

In a standard transaction, the supplier is essentially a temporary tax collector for HMRC. The reverse charge cuts out the middleman. The customer deals with the VAT figures directly on their own return, reporting directly to HMRC.

Who Is Primarily Affected?

While the principle can apply in a few different situations, there are two key groups in the UK that need to be on top of the UK reverse charge VAT rules. Figuring out if you’re in one of these camps is the crucial first step.

- Construction Industry Scheme (CIS) Businesses: This is the big one. If you’re a VAT-registered contractor or subcontractor in the building trade, these rules almost certainly apply to you for specified construction services.

- Businesses Buying Services from Overseas: This often catches people out. If your UK company purchases services from a supplier based outside the UK (think US software subscriptions or consultancy from an EU firm), you must apply the reverse charge.

By making this shift, HMRC secures the tax revenue on these high-risk transactions. Once you have the right systems in place, handling it just becomes another part of your financial routine.

To make this clearer, let’s break down the key differences between the standard way of doing things and the reverse charge.

Reverse Charge VAT At a Glance

The table below gives you a quick snapshot of how the two systems compare.

| Aspect | Standard VAT Procedure | Reverse Charge VAT Procedure |

|---|---|---|

| Invoice | Supplier charges VAT on the invoice (£1,000 + £200 VAT = £1,200). | Supplier invoices for the net amount (£1,000) and states the service is subject to reverse charge. |

| Cash Flow | Customer pays the supplier the gross amount, including VAT. | Customer pays the supplier only the net amount. No VAT cash changes hands. |

| Supplier's VAT Return | Declares the £200 as output tax in Box 1. | No output tax is declared on the transaction. The net sale goes in Box 6. |

| Customer's VAT Return | Reclaims the £200 as input tax in Box 4. | Declares £200 as output tax in Box 1 and reclaims the same £200 as input tax in Box 4. |

Seeing it side-by-side really highlights the fundamental change: under reverse charge, the customer handles both sides of the VAT equation on their own return, effectively acting as both the ‘seller’ and ‘buyer’ for tax purposes.

How the Reverse Charge Works in Construction

The construction industry is, without a doubt, the sector most impacted by the domestic UK reverse charge VAT. Its introduction on 1 March 2021 wasn’t just another bit of red tape; it was a direct and forceful move by HMRC to tackle a massive problem: missing trader fraud.

For years, dishonest operators in the labour supply chain would charge VAT, get paid, and then disappear before paying the tax over to HMRC. The reverse charge was designed to shut this down for good by fundamentally changing who pays the VAT.

Instead of the subcontractor charging VAT and paying it to HMRC, the responsibility—or the “charge”—is reversed up the chain to the main contractor. It’s a clever switch that keeps the money out of the wrong hands and ensures it gets to the taxman.

Who Is Affected in the Construction Sector?

Getting your head around this means knowing your role in the supply chain. The rules specifically target VAT-registered businesses that are also part of the Construction Industry Scheme (CIS).

- Contractors: If you hire a subcontractor for a qualifying service, you no longer pay them the VAT. Instead, you pay them the net amount for their work and account for the VAT directly on your own VAT return. The responsibility is now yours.

- Subcontractors: When you invoice a contractor for a service covered by the reverse charge, you must not add VAT. Your invoice should only show the net value of your work, with a clear note stating that the reverse charge applies.

Essentially, the job of handling the VAT has been passed from the subcontractor to the contractor. If you need a refresher on the basics of CIS, our detailed guide on the Construction Industry Scheme (CIS) is a great place to start.

Which Services Are Covered?

The reverse charge doesn’t apply to every single job. It covers a specific list of “specified services” that make up the bulk of typical construction work. Getting this right is crucial to avoid costly mistakes.

Here’s a quick look at some of the services that fall under the reverse charge rules:

- Groundworks and preparing a site for construction

- Building, altering, repairing, or demolishing structures

- Installing systems like heating, lighting, plumbing, and air-conditioning

- Painting and decorating services

- Cleaning services carried out during construction

However, it’s just as important to know what’s not included. Professional services like those provided by architects or surveyors are exempt. Likewise, hiring scaffolding without labour isn’t covered. HMRC provides a comprehensive list, and it’s essential to check it if you’re ever unsure about a particular job.

Crucial Exemptions: End Users and Intermediaries

Not every transaction in a construction supply chain is caught by the reverse charge. There are two very important exemptions you need to be aware of: end users and intermediary suppliers.

An end user is the final customer. They are a VAT and CIS-registered business that will use the building or construction service for themselves, not sell it on as part of their own construction business. A classic example is a supermarket chain hiring a firm to build a new store. The supermarket is the end user.

Key Takeaway: If your customer confirms in writing that they are an end user, the reverse charge does not apply. You must go back to charging VAT in the normal way.

Intermediary suppliers are closely related. They are businesses that buy the construction services and pass them on to a connected end user without making any changes. Think of a landlord who hires a contractor on behalf of their tenant—they too are exempt.

The Cash Flow Impact on Subcontractors

One of the biggest real-world consequences of the reverse charge has been the hit to subcontractor cash flow. It’s a serious issue.

Previously, a subcontractor would receive the VAT payment from the contractor and could use that money as working capital until their VAT return was due. That temporary cash buffer is now gone.

Subcontractors now only receive the net amount, which can put a significant squeeze on day-to-day finances. If you’re a subcontractor, you need to be proactive to manage this:

- Rework your cash flow forecasts: Your projections need to reflect that VAT payments are no longer coming in.

- Negotiate better payment terms: Push for shorter payment deadlines to get your money in the bank faster.

- Consider switching to monthly VAT returns: If you regularly reclaim VAT on materials and expenses, filing monthly can get those repayments from HMRC much quicker, helping to ease the cash crunch.

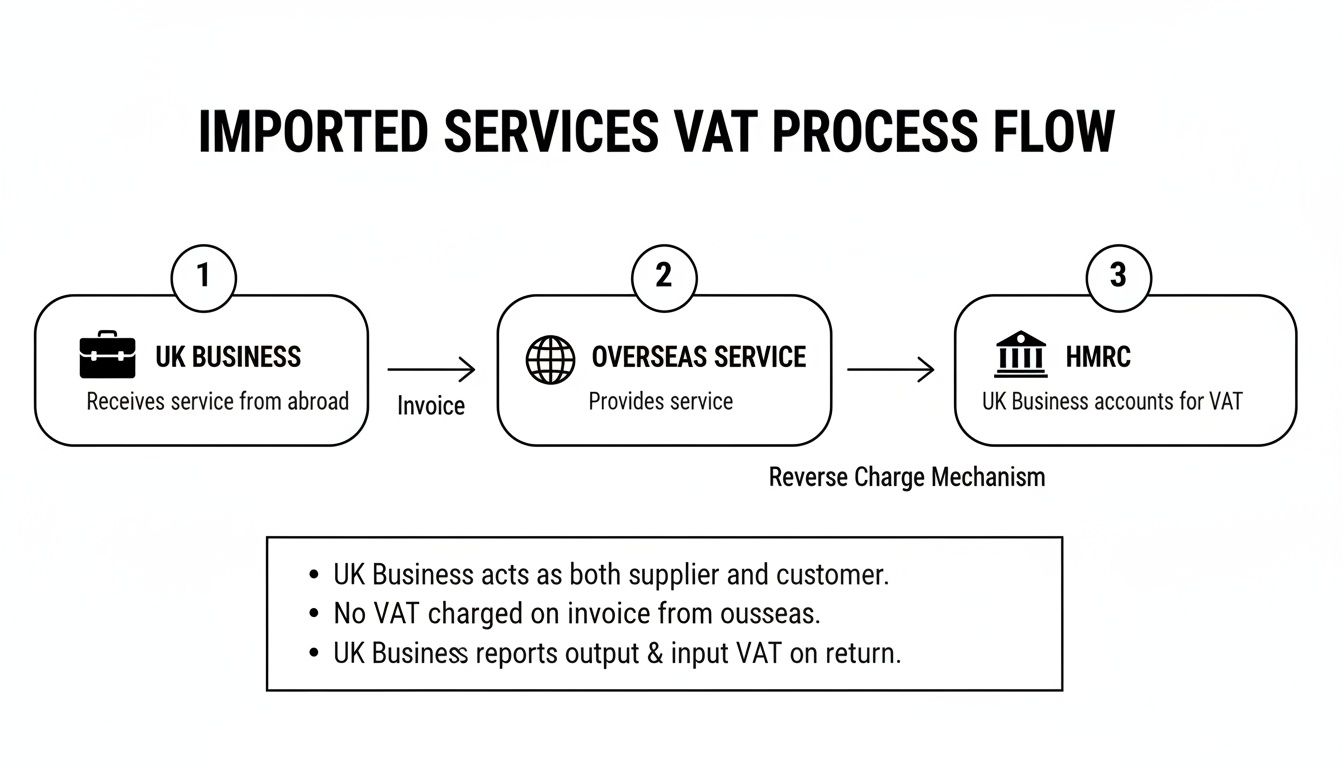

Handling Reverse Charge on Imported Services

The UK reverse charge VAT isn’t just for builders and contractors. It’s a crucial mechanism you’ll encounter when your business buys services from suppliers based outside the United Kingdom. This often catches people out, but the idea behind it is actually quite logical once you get your head around it.

Imagine you import physical goods; you’d naturally expect to deal with import VAT at the border. Well, think of buying a service from overseas in the same way. When you “import” a service—like a software subscription from a US tech company, digital marketing from an Irish agency, or consultancy from a specialist in Germany—the reverse charge acts as the VAT equivalent.

Essentially, for VAT purposes, your UK business has to wear two hats at once: that of the supplier and the customer. It becomes your responsibility to account for the VAT that the overseas supplier would have charged if they were operating in the UK.

The Accounting Two-Step

So, how does this work on your VAT return? It’s a clever bit of accounting that happens simultaneously. You declare the VAT on the service you’ve bought as output tax (in Box 1, as if you’d charged it), and at the very same time, you reclaim that exact amount as input tax (in Box 4, as if you’d paid it).

For most VAT-registered businesses making standard-rated sales, the net effect is zero. It’s a tax-neutral transaction because the output tax and input tax cancel each other out perfectly. No money actually changes hands with HMRC for that specific purchase.

But there’s a catch. If your business is partially exempt—maybe you make a mix of standard-rated and exempt sales—you might not be able to reclaim all the input VAT. This is a vital detail, and overlooking it can lead to a nasty, unexpected tax bill down the line.

Determining the Place of Supply

The golden rule for getting this right is understanding the ‘place of supply’. For the vast majority of business-to-business (B2B) services, the rules state that the place of supply is wherever the customer is based.

This means if your company is in the UK and you buy a service from anywhere else in the world, the place of supply is considered to be the UK. That’s what pulls the transaction into the UK VAT net and triggers the reverse charge for you, the customer.

You probably do this more often than you realise. Here are a few everyday examples:

- Software as a Service (SaaS): Subscriptions to tools like Adobe, Slack, or a specialist US-based project management platform.

- Digital Advertising: Paying for ad campaigns on Google or Meta (Facebook/Instagram), both of which are based in Ireland for their European operations.

- Professional Services: Hiring a freelance consultant from France or getting advice from a law firm in Germany.

- Web Hosting: Using a popular hosting provider whose servers and business are located in the USA or mainland Europe.

The core principle is simple: if you are a UK business buying a service from an overseas supplier, you are responsible for handling the UK VAT via the reverse charge. The overseas supplier does not charge you their local VAT.

This is a complex area, especially as international tax rules can shift. For a more detailed breakdown, you can learn more by navigating the complexities of international trade and taxation.

Practical Steps for Compliance

To stay on the right side of HMRC, you need a solid process. First things first, make sure your accounting software is configured correctly. Systems like Xero have specific tax codes built for the reverse charge, which automatically handle the double-entry posting to your VAT return.

When an invoice lands from your overseas supplier, it won’t have any VAT on it. Your job is to calculate the UK VAT (usually 20%) on the sterling value of that service and make sure it’s accounted for correctly. Getting this wrong is a common mistake that HMRC inspectors love to find, and it can result in penalties and interest charges on the VAT you failed to declare.

A Practical Guide to Accounting and Invoicing

Knowing the theory behind the UK reverse charge VAT is one thing, but putting it into practice is where the rubber really meets the road. This is where the details matter, because getting your invoicing, bookkeeping, and VAT returns right is absolutely non-negotiable if you want to stay on the right side of HMRC.

Think of it as learning a new dance routine. Every step, from raising the invoice to filing your return, has to follow a specific sequence. One wrong move and you could easily trip up.

Crafting the Perfect Reverse Charge Invoice

Your invoice is the starting gun for the entire reverse charge process. It’s your job to give your customer a clear signal that they are the one responsible for handling the VAT. Your standard VAT invoice just won’t do.

An invoice subject to the reverse charge needs all the usual information, but with two crucial differences:

- Don’t Add VAT: You must not add VAT to the total amount. You are only charging for the net value of your work.

- State the Reverse Charge Applies: The invoice must include a specific note to make it crystal clear. HMRC suggests wording like, “Reverse charge: Customer to pay the VAT to HMRC.”

This isn’t just a helpful tip; it’s a firm requirement. For a full rundown on what makes an invoice compliant, you might find our guide on what should be on a VAT invoice useful.

Bookkeeping Entries: Let Your Software Do the Heavy Lifting

Thankfully, modern accounting software like Xero has made managing reverse charge transactions far less painful. These platforms come with built-in tax rates that automatically handle the tricky double-entry bookkeeping that’s required.

When you get a purchase invoice for a service that falls under the reverse charge, you can’t just enter it like a normal expense. Instead, you need to use a specific tax code. In Xero, for example, this is typically “20% VAT on Imports” for services from overseas or “Domestic Reverse Charge CIS @ 20%” for the construction industry scheme.

Using these dedicated codes is the key to ensuring the transaction is reported correctly to HMRC, especially under the Making Tax Digital (MTD) rules. It takes the guesswork out of the process and massively reduces the risk of manual errors.

Navigating Your VAT Return: A Box-by-Box Guide

The reverse charge has a very specific, and sometimes confusing, effect on your VAT return. The customer receiving the service is the one who has to make entries across four key boxes.

Let’s walk through a real-world example. Imagine you’ve received a £1,000 construction service that falls under the reverse charge. The VAT on this is £200 (£1,000 x 20%).

Here’s a breakdown of how this single transaction needs to be reported on the customer’s VAT return.

| VAT Return Box | What to Enter | Value |

|---|---|---|

| Box 1 | VAT due on sales (the output tax you're declaring) | £200 |

| Box 4 | VAT reclaimed on purchases (the input tax you're claiming back) | £200 |

| Box 6 | Total value of sales | £0 (leave blank for this transaction) |

| Box 7 | Total value of purchases | £1,000 |

As you can see, the VAT declared in Box 1 is immediately cancelled out by the VAT reclaimed in Box 4. This makes the transaction cash-neutral for a fully VAT-registered business, but it’s a critical paper exercise that HMRC needs to see.

For those dealing with services from overseas, this flowchart visualises where the responsibility lies. It clearly shows the UK business, not the supplier abroad, is on the hook for calculating and reporting the VAT directly to HMRC.

The rules can get particularly tangled in the construction industry. For instance, when the Domestic Reverse Charge was introduced on 1 March 2021, it completely changed the game for subcontractors and their clients. Suddenly, customers had to start declaring the 20% VAT on CIS-reported services, which caused a lot of confusion, especially for invoices dated around that changeover period.

For a broader perspective on financial admin that complements good VAT management, you might find these useful freelance tax tips worth a read. After all, getting the VAT process right is just one piece of the puzzle in managing your overall tax affairs effectively.

Common Mistakes and How to Avoid Them

Getting to grips with the UK reverse charge VAT rules can feel a bit like walking a tightrope. One small misstep and you could find yourself facing compliance issues and penalties from HMRC. The good news? Most of these common errors are entirely avoidable once you know what to look for.

Let's dive into some of the most frequent slip-ups we see.

Misidentifying the 'End User' in Construction

This is a big one, especially in the construction industry. A contractor might assume their client is the final customer—the ‘end user’—and charge them standard VAT as usual. But what if that client is actually an intermediary, another developer who will be selling those construction services on?

If that's the case, the reverse charge should apply. Getting this wrong breaks the chain and leads to an incorrect VAT treatment right from the start.

Mishandling Mixed Supplies

Another classic tripwire is the mixed supply invoice. Imagine you're a subcontractor providing both labour (which falls under the reverse charge) and materials (which might not) for a single project. If you put both on the same invoice, the entire value of that invoice is subject to the reverse charge.

We often see businesses incorrectly splitting the VAT treatment on a single bill, which is a red flag for HMRC. If it’s on one invoice, the reverse charge rule covers the lot.

Forgetting to Update Your Accounting Software

It sounds simple, but you'd be surprised how often this happens. Businesses get into a routine and continue using their standard VAT codes out of habit. In software like Xero, you need to actively select the specific ‘Domestic Reverse Charge’ or ‘Imported Services’ tax rates.

If you don't, your VAT return is guaranteed to be wrong.

It's crucial to remember that both the supplier and the customer share responsibility here. Just because a supplier sends you an incorrect invoice doesn't let you off the hook. You are still required to account for the reverse charge VAT correctly on your own return.

Failing to set up your software properly creates a messy domino effect. The supplier's invoice is non-compliant, and the customer's VAT return will have errors in Boxes 1, 4, and 7. Modern accounting systems are built to handle this perfectly, but they need you to tell them what to do first.

Invoice and Communication Breakdowns

So much of this comes down to clear communication, yet it’s often the first thing to fall by the wayside. A vague or incomplete invoice creates a headache for everyone involved.

Here are a few invoice-related blunders to watch out for:

- Vague Wording: Invoices with fuzzy notes like "customer to handle VAT" just don't cut it. You must use clear, explicit language stating that the service is subject to the reverse charge.

- Missing VAT Number: An invoice under the reverse charge isn't valid unless it clearly shows the customer's VAT registration number. It’s a small detail that makes a huge difference.

- No Written Confirmation: If you're in construction, not getting written confirmation of your customer's 'end user' status is a major risk. Without that piece of paper, you have no defence if HMRC asks why you didn't apply the reverse charge.

The best way to sidestep these issues is to build a solid process. Create a simple checklist for every reverse charge transaction. Always confirm your customer’s status, use precise wording on your invoices, and make sure your accounting software is set up with the right tax codes before you process anything. A little bit of diligence upfront can save a world of trouble later on.

How Professional Support Simplifies VAT Compliance

Navigating the complexities of the UK reverse charge VAT can feel like a real headache. It's an administrative maze that pulls your focus away from what actually matters: running and growing your business. The rules are fiddly, the stakes are high, and a simple mistake can lead to cash flow issues or an unwelcome letter from HMRC.

Whether you're in construction or buying services from abroad, getting the reverse charge right isn't just about ticking a box—it's fundamental to your financial stability.

This is where getting an expert on your side makes all the difference. Instead of losing hours trying to make sense of dense HMRC guidance or second-guessing every invoice, you can hand the whole problem over. A good accountant can transform what feels like a complex, stressful chore into a smooth, almost invisible process.

The real value of professional support is turning VAT compliance from a reactive, time-consuming firefight into a proactive, managed system that protects your business and gives you back your time.

From Confusion to Clarity and Control

Bringing in an accounting expert delivers immediate and practical results. To get a handle on tricky tax rules like the UK reverse charge VAT, many businesses look to the best outsourced accounting services to get it right from day one. This kind of support zeroes in on the key challenges of the reverse charge.

- Getting Your Software Right: We'll dive into your cloud accounting software, like Xero, and set up the correct tax codes for both domestic and international reverse charges. This simple step automates the calculations and stops manual errors from creeping into your VAT return.

- Building a Solid Process: We help you create a clear, simple system for spotting transactions that fall under the reverse charge. This often involves setting up invoice templates with the exact wording HMRC requires and showing your team how to handle them correctly.

- Managing Your VAT Return: We can take the entire VAT return off your plate. We'll prepare and file it for you, ensuring every reverse charge transaction is correctly declared in Boxes 1, 4, 6, and 7. This protects you from compliance headaches down the line.

Your Next Step Towards Effortless Compliance

At the end of the day, managing the UK reverse charge VAT correctly is about protecting your cash flow and your peace of mind. With the right support in place, you can stop the administrative drain and feel confident that your finances are in safe hands.

If you’re ready to stop worrying about VAT compliance and get back to focusing on your business goals, we’re here to help. Contact Stewart Accounting Services today to see how we can build an efficient, stress-free process for you.

Got Questions About UK Reverse Charge VAT?

Even when you think you’ve got a handle on the rules, tricky situations can pop up. The UK reverse charge VAT system certainly has its quirks, but thankfully, most common questions have pretty clear answers. Let's break down some of the queries we hear most often.

What Happens if I Get the Reverse Charge Wrong?

It happens. If you’ve mistakenly applied the reverse charge to an invoice when you should have charged standard VAT, don't panic. The cleanest way to fix it is to issue a credit note to cancel the incorrect invoice, then simply raise a new one with the proper VAT treatment.

What if you did the opposite and charged VAT when the reverse charge should have applied? Your customer can't reclaim that VAT as input tax, so you need to sort it out. Again, you’ll need to credit the original invoice and reissue a correct one showing the net amount and the required reverse charge note. The key is to act fast and get it right.

Does the Reverse Charge Apply if My Customer Isn't VAT Registered?

In short, no. The reverse charge mechanism—whether for construction work or imported services—is strictly for business-to-business (B2B) transactions where your customer is registered for VAT in the UK.

If your customer isn't VAT registered, you just stick to the standard rules. For a domestic construction job, for instance, you’d charge the standard rate of VAT on your invoice just as you normally would. It’s always on you, the supplier, to double-check your customer's VAT status.

It is absolutely crucial to verify your customer's VAT registration. For construction, you also need to check their CIS status and find out if they're an 'end user'. A quick search on the government's VAT number validation service can save you a world of compliance headaches.

How Does This Work with the Flat Rate Scheme?

This is a big one. If you’re on the VAT Flat Rate Scheme (FRS), the reverse charge can really throw a spanner in the works. When you receive a service subject to the reverse charge, you have to account for the VAT on your return at the standard rate (20%), not your usual flat rate. On top of that, you can’t reclaim this VAT as input tax.

When you supply services that fall under the reverse charge, you must leave the value of these sales out of your flat rate turnover when working out what you owe HMRC. It’s a major shift from the scheme's normal simplicity and something FRS users must get right.

How Do I Prove a Customer Is an End User?

For construction jobs, the only way to prove a customer is an 'end user' is to get it from them in writing. This confirmation needs to be in a permanent format, like an email or a formal letter, and you must keep it with your project records.

The customer needs to state clearly that they are an end user for the specific services you're providing. While HMRC guidance says one declaration can cover an entire project, it's always better to be specific and unambiguous to avoid any arguments later on.

Getting these details right is vital for staying on the right side of HMRC. If you're wrestling with the specifics or just want peace of mind that your systems are set up correctly, Stewart Accounting Services is here to help. Find out how we can support you at https://stewartaccounting.co.uk.