The UK VAT reverse charge can feel a bit counter-intuitive at first. It’s an accounting mechanism that essentially flips the normal VAT process on its head. Instead of the seller charging VAT and paying it to HMRC, the responsibility shifts directly to the buyer.

The buyer accounts for the VAT on their own VAT return as both a sale (output tax) and a purchase (input tax). For most VAT-registered businesses, these two entries cancel each other out, making the whole transaction cash-neutral. The system is primarily used in specific sectors, like construction, as a clever way to clamp down on tax fraud.

What the UK VAT Reverse Charge Really Means

Let’s break it down with a simple analogy. Normally, when you buy something, the VAT works like a service charge at a restaurant. The restaurant (the supplier) adds the charge to your bill, you pay it, and they're responsible for passing that money on to the taxman. Simple.

The reverse charge changes the game entirely. Using our restaurant example, it’s like being handed the bill for your meal with a note attached saying, "Please calculate the 20% service charge yourself and pay it directly to the authorities." The responsibility has been reversed from the seller to you, the buyer.

At its core, the reverse charge isn't about creating new taxes. It's about changing who is responsible for sending the VAT payment to HMRC.

To get a quick overview of how this differs from the standard process, let's compare them side-by-side.

Standard VAT vs Reverse Charge VAT At a Glance

| Process Step | Standard VAT Procedure | Reverse Charge Procedure |

|---|---|---|

| Invoicing | Seller issues an invoice showing the net amount plus VAT (e.g., £1,000 + £200 VAT). | Seller issues an invoice showing just the net amount (e.g., £1,000) with a note stating the reverse charge applies. |

| Payment | Buyer pays the full gross amount to the seller (e.g., £1,200). | Buyer pays only the net amount to the seller (e.g., £1,000). |

| VAT Return | Seller declares £200 as output VAT. Buyer reclaims £200 as input VAT. | Buyer declares £200 as output VAT and simultaneously reclaims £200 as input VAT on the same return. Seller makes no VAT entry. |

As you can see, the reverse charge fundamentally alters the flow of cash and the accounting responsibilities for both parties involved.

The Relay Race Analogy

Here's another way to think about it – imagine a relay race.

- Standard VAT: The supplier is the sole runner. They take the "VAT baton" from the starting line (the sale) and carry it all the way to the finish line (paying HMRC).

- Reverse Charge VAT: The supplier starts the race but immediately passes the VAT baton to the buyer. It's now the buyer's responsibility to complete the race and get that baton to the finish line by accounting for it on their VAT return.

This switch has a real impact on day-to-day business. For suppliers, not receiving that 20% VAT upfront can squeeze your cash flow. On the flip side, buyers get a cash flow advantage by not having to pay the VAT out immediately.

Why Was It Introduced?

So, why go to all this trouble? The reverse charge was specifically designed to tackle a type of tax evasion known as "missing trader" fraud.

This was a particularly big problem in high-risk industries like construction and electronics. Unscrupulous companies would charge VAT, collect the cash from their customers, and then vanish without a trace before paying what they owed to HMRC. This was costing the government a fortune—in some sectors, losses were estimated to be as high as 5% of total VAT revenue.

By shifting the responsibility to the buyer, the reverse charge closes this loophole. There's no VAT cash for a fraudulent seller to collect and run away with. You can read more on the background of the VAT reverse charge in the UK on getmoss.com.

Getting your head around this system is crucial because it changes the very mechanics of how you invoice and account for certain sales and purchases. We cover the specifics of this in our guide to the difference between output and input VAT. While it might sound complicated, once you understand the logic, it's perfectly manageable.

When Does the VAT Reverse Charge Apply?

Knowing exactly when to use the UK VAT reverse charge is absolutely critical. It’s not a one-size-fits-all rule; HMRC designed it to target specific business-to-business (B2B) supplies in high-risk sectors to clamp down on tax fraud. Getting this right protects everyone involved—both supplier and customer—from some pretty costly mistakes.

The place most UK businesses will run into this is in the construction industry. But it doesn't stop there. The reverse charge also covers a specific list of goods and certain cross-border services, which can easily trip up growing businesses if they're not careful. Let's break down where you'll find it in practice.

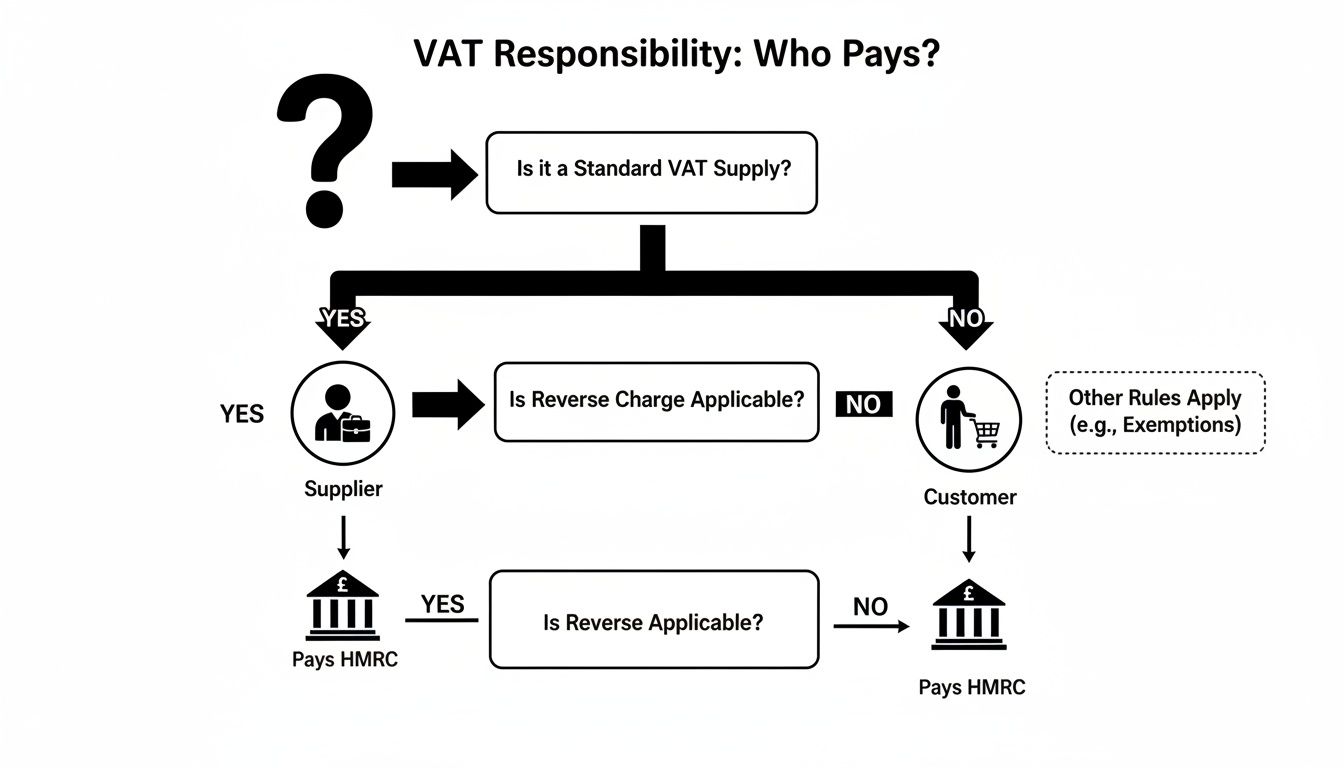

This flowchart neatly shows how the responsibility for paying VAT to HMRC shifts from the supplier to the customer when the reverse charge kicks in.

As you can see, the reverse charge essentially reroutes the VAT payment. Instead of the supplier collecting it and passing it on, the customer pays it directly to HMRC.

The Domestic Reverse Charge for Construction Services

The construction sector is ground zero for the domestic reverse charge. It was brought in on 1 March 2021 and applies to a specific list of building services when they are supplied between two VAT-registered businesses, especially where payments fall under the Construction Industry Scheme (CIS). The whole point was to tackle "missing trader" fraud—a tactic where subcontractors would charge VAT, pocket the cash, and vanish before paying their tax bill. You can find more on the legislative background of the VAT reverse charge on Wikipedia.

So, what kind of work is actually covered? It’s a pretty broad list, covering most of the services you'd expect on a building site:

- Site Preparation: Think demolition, clearing a site, excavation work, and laying foundations.

- Building Work: This includes any construction, alteration, repair, or extension of buildings and other structures.

- Internal Installations: Putting in systems for heating, lighting, air-conditioning, drainage, and fire protection is covered.

- Finishing Touches: Painting and decorating, both inside and out, also fall under the reverse charge.

But knowing what's not on the list is just as important to avoid applying the rules where you shouldn't.

Key Insight: The reverse charge doesn't apply if you're supplying services to an 'end user'. This is a business that receives the construction services for its own use, not to sell on as part of its trade—like a retailer having their shop refitted. It's vital that you get written confirmation of your customer's end-user status.

Services Excluded from the Construction Reverse Charge

Not every single job on a construction project is subject to the reverse charge. HMRC has a clear list of exemptions, and getting this wrong can land you in hot water.

Services that are NOT covered include:

- Professional Services: The work of architects, surveyors, and other consultants is completely excluded.

- Installation of Specific Items: If you’re just installing security systems like burglar alarms or CCTV, standard VAT rules apply.

- Artistic Works: The creation and installation of artworks, such as murals or sculptures, fall outside the scheme.

- Manufacturing and Delivery: If your business only manufactures or delivers building components to a site but doesn't install them, you'll use the normal VAT process.

This distinction is crucial. If you issue an invoice that includes a mix of reverse charge services and standard services, the entire value of that invoice is usually subject to the reverse charge.

Specified Goods and Cross-Border Services

While construction gets most of the attention, the UK VAT reverse charge also applies to a handful of goods known to be targets for fraud. These are almost always B2B sales and include things like:

- Mobile phones

- Computer chips

- Wholesale gas and electricity

These rules are there to stop fraudsters from buying up high-value, easy-to-move goods, selling them on with VAT, and then disappearing before paying the tax they owe HMRC.

The reverse charge also plays a huge role when you buy services from overseas. If your UK-based, VAT-registered business buys digital services—like advertising from Google or Meta, or a software subscription from a US company—you are responsible for accounting for the VAT yourself via the reverse charge.

This is a massive tripwire for growing businesses. These international service purchases count towards your VAT registration threshold. We've seen countless small businesses and sole traders get caught out because they didn't realise these costs pushed their turnover above the £90,000 threshold, landing them with an unexpected VAT registration and bill.

How to Handle Invoicing and VAT Returns

Knowing the theory behind the UK VAT reverse charge is a great start, but the real test comes when you have to apply it to your invoices and VAT returns. Getting the paperwork right isn't just a matter of admin; it's a critical part of staying on the right side of HMRC and keeping the cash flowing smoothly between you and your business partners.

So, let's get practical. Here’s a breakdown of exactly what you need to do, whether you're sending the invoice as a supplier or processing it as a customer.

Creating a Compliant Supplier Invoice

If you're the supplier of goods or services that fall under the reverse charge, your invoicing process has to change. The most significant difference? You don't add VAT to the final amount you're charging. Instead, your invoice needs to make it crystal clear that the responsibility for handling the VAT now lies with your customer.

Your invoice will still need all the usual information, but you must leave the VAT amount off the total. If you need a refresher on the basics, have a look at our guide on what should be on a VAT invoice.

Critically, you must add a note to the invoice stating that the reverse charge applies. HMRC doesn’t demand a specific script, but the wording has to be unambiguous.

Most businesses use one of these phrases:

- "Reverse charge: Customer to pay the VAT to HMRC."

- "VAT Act 1994 Section 55A applies."

- "S55A VATA 94 applies."

This isn't optional—it's a legal requirement. Forgetting this note makes your invoice non-compliant and can cause headaches for both you and your customer if HMRC ever comes knocking.

Processing the VAT Return as the Customer

When an invoice marked with a reverse charge notice lands on your desk, the ball is in your court. You're now responsible for accounting for the VAT the supplier didn't charge you. It sounds more complicated than it is; in reality, it's just a case of making a couple of offsetting entries on your VAT return.

The key thing to remember is that for most businesses, this whole process is cash-neutral. You declare the VAT as if you supplied the service, and you reclaim it as if you paid it—all in one go on the same return.

This bit of accounting footwork is done across four key boxes on your VAT return:

- Box 1 (VAT due on sales): This is where you add the output VAT. It's the amount of VAT you would have been charged if the system worked in the normal way.

- Box 4 (VAT reclaimed on purchases): You enter the exact same amount of input VAT here to claim it back.

- Box 6 (Total value of sales): The reverse charge doesn't affect this box at all. Your supplier will report the net sale on their own return.

- Box 7 (Total value of purchases): You must add the net value of what you bought (the invoice total) to this box.

A Worked Example of the Accounting Flow

Let's walk through a simple scenario to see this in action. Imagine you're a main contractor (the customer) and you've just received an invoice from your subcontractor (the supplier) for construction services worth £1,000. The invoice correctly notes that the reverse charge applies.

The Invoice: The subcontractor sends you an invoice for £1,000. It shows £0.00 VAT and carries the note, "Reverse charge: Customer to pay the VAT to HMRC." You pay your supplier the £1,000.

Calculating the VAT: Your job is to work out the VAT that would have been due. At the standard 20% rate, that’s £1,000 x 20% = £200.

Completing Your VAT Return: On your next VAT return, you’ll make these entries:

- Box 1: Add £200 to your output tax figure.

- Box 4: Add £200 to your input tax figure.

- Box 7: Add £1,000 (the net value of the service) to your total purchases.

See how the £200 you add to Box 1 is immediately cancelled out by the £200 you claim back in Box 4? The net impact on the VAT you owe HMRC is zero. This simple debit-and-credit mechanism is the heart of the reverse charge, stopping VAT from going missing while making sure it's all properly accounted for.

Making Life Easier with Cloud Accounting Software

Trying to manually track the debits and credits for the UK VAT reverse charge is a recipe for disaster. Let's be honest, when you're juggling multiple projects, a spreadsheet is just one tired keystroke away from becoming a mess. This kind of human error can easily lead to an incorrect VAT return, and that’s the kind of thing that gets HMRC’s attention.

Thankfully, there's a much better way. Modern cloud accounting software completely transforms this potential headache into a simple, automated task.

Instead of getting lost in manual sums, platforms like Xero, QuickBooks, and FreeAgent have specific features built in to handle the reverse charge. They do the heavy lifting for you, automating the tricky entries needed on your VAT return. This not only saves a huge amount of time but also ensures you get it right. For any small business looking to get on top of its VAT obligations, choosing the right accounting software is a game-changer.

These systems are ready to go with the correct tax codes, turning what was a complicated, multi-step chore into just a few clicks.

A quick glance at a dashboard in a system like Xero gives you a clear, real-time picture of your finances, making something as complex as VAT feel much more manageable. When you adopt these tools, you can get back to running your business, confident that your compliance is being handled properly in the background.

Finding the Right Tax Codes in Xero

The real magic of this software is how it uses specific tax codes for reverse charge transactions. When you pick the right code for an invoice or bill, the software knows exactly what to do. It automatically makes the correct double entries on your VAT return, putting the figures in all the right boxes without you having to lift a finger.

So, how does this work in practice? Let's take a look at Xero, a popular choice for many small businesses. When you're raising an invoice or entering a bill that falls under the domestic reverse charge, you simply select one of its dedicated tax rates.

Here's a quick breakdown of the Xero tax codes you'll need:

Reverse Charge Tax Codes in Xero

| Transaction Type | Applicable Xero Tax Code | What It Does |

|---|---|---|

| Sales (Supplier) | 20.0% (VAT on Sales) with the reverse charge option ticked, or a custom "Domestic Reverse Charge CIS" rate. | Records the net sale value in Box 6 of your VAT return but, crucially, does not add any output VAT to Box 1. |

| Purchases (Customer) | 20.0% (VAT on Expenses) with the reverse charge option ticked, or a custom "Domestic Reverse Charge CIS" rate. | Adds the notional VAT amount to both Box 1 (as output tax) and Box 4 (as input tax). It also includes the net purchase value in Box 7. |

This automated process is the key to getting it right every time. It pretty much eliminates the risk of forgetting one side of the entry or sticking a figure in the wrong box—mistakes that are all too common with manual systems. If you're thinking about updating your financial processes, our guide to cloud accounting for small business has more detail on the benefits.

The Real Payoff of Automation

Switching to automated reverse charge accounting isn't just about making things easier; it's a smart move to protect your business.

By letting the software handle the VAT return entries, you drastically reduce the risk of compliance errors. This means fewer worries about potential penalties from HMRC and more accurate financial records you can actually rely on for business planning.

Ultimately, this all comes down to freeing up your time and mental energy. Instead of spending hours poring over invoices and manually filling out your VAT return, you can trust the system to do its job. It allows you to shift your focus from tedious admin back to what really matters—growing your business.

Common Pitfalls and How to Avoid Them

The VAT reverse charge system is perfectly logical on paper, but in the real world, it’s surprisingly easy to get tripped up. Even seasoned businesses can make simple mistakes that spiral into compliance headaches, incorrect VAT returns, and unwanted attention from HMRC.

The good news? Most of these errors are entirely avoidable. Think of this section as a heads-up on the most common traps we see businesses fall into. By knowing what to look out for, you can sidestep them completely and handle these transactions with confidence.

Pitfall 1: Incorrectly Charging VAT

This is probably the most frequent mistake, especially in the construction sector. A supplier, working on autopilot, issues an invoice and adds the standard 20% VAT for a service that should fall under the domestic reverse charge. It seems like a minor slip, but the domino effect is significant.

Right away, the invoice is invalid. The customer has to reject it, which delays payment and creates needless admin for both sides. Worse still, if the customer accidentally pays it, they can't reclaim that incorrectly charged VAT as input tax, which means a direct, and often painful, hit to their cash flow.

How to Avoid It:

If you're a supplier, you must check if your service is subject to the reverse charge before you raise the invoice. If it is, your invoice needs to clearly state that the reverse charge applies and show a VAT amount of £0.00. Using accounting software that's set up correctly can almost completely eliminate this kind of human error.

Pitfall 2: Forgetting to Account for the Charge

The next big hurdle is for the customer. You receive a reverse charge invoice, you pay the net amount, and it’s very easy to think, "job done." But the most crucial step is yet to come: actually accounting for the VAT on your own return.

Forgetting this step means your VAT return is wrong, plain and simple. You've failed to declare the output tax in Box 1 and reclaim the corresponding input tax in Box 4. This is exactly the kind of omission that can trigger a compliance check and potential penalties from HMRC.

Crucial Reminder: The VAT reverse charge doesn't make VAT disappear. It just shifts the responsibility for reporting it from the supplier to the customer. Forgetting to do your part breaks the chain and invalidates your VAT submission.

Pitfall 3: Confusion Over ‘End-User’ Status

The idea of an ‘end user’ often causes a lot of head-scratching, particularly in construction. The reverse charge doesn't apply if your customer is the final consumer of the service and won't be selling it on as part of their own construction services. A classic example is a retail business having its shop refitted – they are the end user.

The problem starts when this status isn't communicated. A supplier might assume the reverse charge applies when it doesn’t, leading to an incorrect invoice and all the knock-on issues we've already covered.

How to Avoid It:

It’s all about clear communication. If you are an end user, you have a responsibility to inform your supplier of this in writing. This gives them the proof they need to charge you standard VAT correctly. For suppliers, if you have any doubt, don't guess – ask your customer to confirm their status in writing.

Pitfall 4: Mishandling Mixed Supplies

Things can get complicated when an invoice covers a mix of services – some that fall under the reverse charge and some that don't. The common mistake here is trying to split the VAT treatment on one invoice, which feels logical but is incorrect.

How to Avoid It:

HMRC’s guidance is actually very straightforward on this point. If any of the services on a single invoice are subject to the reverse charge, then the reverse charge applies to the entire invoice value. Don't try to separate the items. To stay compliant, just apply the reverse charge mechanism to the total amount.

Your Questions, Answered

Even when you've got a handle on the basics, the VAT reverse charge can throw up some tricky real-world questions. It’s one of those areas where the devil really is in the detail. Let's walk through some of the most common queries we get from clients, with straight-to-the-point answers.

What Happens If I'm the End User?

This is a big one, especially in construction. If you're the final customer for a service and have no plans to sell that service on, you're what HMRC calls an 'end user'. Good news: the domestic reverse charge does not apply to you.

It's your job, however, to make this crystal clear to your supplier. You need to tell them in writing that you’re the end user. Once you've done that, they’ll simply send you a normal VAT invoice with the usual 20% VAT added, which you pay to them just like any other bill. A classic example is a high street shop hiring a builder to refit their premises – the shop is the end user.

How Is This Going to Affect My Cash Flow?

The impact on your bank balance flips completely depending on whether you’re the supplier or the customer.

If you're the supplier (like a subcontractor): You might feel a bit of a pinch. You're no longer getting that 20% VAT payment from your customer, so the amount hitting your bank account from each invoice is smaller. This can definitely tighten up your working capital.

If you're the customer (like a main contractor): Your cash flow usually gets a welcome boost. You aren’t paying that VAT amount out to your supplier, so the cash stays in your business for longer. On your VAT return, it's a paper exercise—the output tax you declare is cancelled out by the input tax you reclaim—so it’s a cash-neutral event.

Does the Reverse Charge Apply If My Supplier Isn't VAT Registered?

Simple answer: no, it doesn’t. The UK VAT reverse charge only ever kicks in for transactions between two UK VAT-registered businesses.

If your supplier is a small operation and their turnover is below the VAT threshold, they can't charge VAT in the first place. So, the reverse charge is a non-starter. You’ll just get a standard invoice from them with no VAT to worry about.

The Golden Rule: Both you and your supplier must be VAT registered for the reverse charge to even be a possibility. If you're ever in doubt, check your supplier's VAT status. Getting this right from the start saves a world of headaches later on.

Are Materials Included in the Reverse Charge?

This is a massive point of confusion, and it all comes down to how the materials are being supplied.

If the materials are just one part of a bigger job that falls under the reverse charge (like a full construction project), then yes. The entire invoice value, materials and all, is subject to the reverse charge.

But, if you're just a supplier of materials—you're selling bricks or timber with no labour or installation service—then it’s a straightforward supply of goods. In that scenario, normal VAT rules apply. You just charge 20% VAT as you always would. It’s the nature of the whole contract that decides the VAT treatment.

Trying to get your head around the UK VAT reverse charge can be a real challenge, but you don't have to figure it all out on your own. Stewart Accounting Services is here to help SMEs across the UK get their VAT right. We'll make sure you're compliant, help you manage your cash flow, and give you one less thing to worry about. Get in touch with our expert team to see how we can give you more time, more money, and a clearer mind. Find out more at https://stewartaccounting.co.uk.