The VAT reverse charge flips the usual way VAT is handled on its head. In a normal transaction, the supplier charges you VAT and is then responsible for paying it to HMRC. With the reverse charge, the responsibility shifts: the supplier doesn't add VAT to their invoice, and you, the customer, account for it directly on your own VAT return.

It sounds a bit strange at first, but it's a clever system designed to tackle tax fraud in specific business-to-business (B2B) sectors.

What Is the VAT Reverse Charge and Why Does It Matter?

Think about it this way. Normally, if you hire a subcontractor, they bill you for their work plus VAT. You pay them the full amount, and they're supposed to pass that VAT on to HMRC.

The reverse charge changes that process. The subcontractor bills you only for their work, and you then report and pay the VAT element directly to HMRC on their behalf.

This mechanism was introduced by HMRC to combat "missing trader" fraud. That's where a supplier charges a customer VAT, pockets the cash, and then vanishes before paying the taxman. By making the customer responsible for the VAT payment, the reverse charge effectively closes this loophole.

The Core Concept Explained

Instead of the VAT flowing from customer to supplier to HMRC, the reverse charge makes it flow directly from the customer to HMRC.

For the customer, this usually works out as a tax-neutral process on their VAT return. They record the VAT as both an output tax (what they owe HMRC) and an input tax (what they can reclaim from HMRC). In most cases, these two entries simply cancel each other out.

The crucial point is that it's not about changing the amount of tax paid, but rather who is responsible for paying it. It’s a seemingly small procedural tweak, but it has significant implications for how you manage your invoicing and accounting.

Who Is Affected by the Reverse Charge?

While it might seem like a niche tax rule, the VAT reverse charge affects a surprising number of UK businesses. Getting to grips with where it applies is the first step to staying compliant. You can brush up on the basics with our guide on Value Added Tax and what you need to know.

The rules are most commonly seen in these sectors:

- Building and Construction Services: This is the big one. The domestic reverse charge for construction is the most common application in the UK, impacting most VAT-registered businesses operating under the Construction Industry Scheme (CIS).

- B2B Digital Services: If your UK business buys services like online advertising from Google or social media ads from Meta, the reverse charge comes into play because these suppliers are based overseas.

- Wholesale Goods: Certain goods that are high-value and easy to transport, like mobile phones and computer chips, are also subject to the reverse charge to prevent fraud.

The key takeaway is that the reverse charge doesn't alter the final VAT amount due on a transaction. Instead, it re-routes the payment obligation from the seller to the buyer to ensure the tax authority receives what it's owed.

Getting this right is vital. It impacts your invoices, your VAT returns, and your cash flow, and getting it wrong can lead to some painful penalties from HMRC.

When Does the VAT Reverse Charge Kick In for Your Business?

Figuring out exactly when to use the VAT reverse charge can feel like navigating a maze. It’s not a one-size-fits-all rule; it's a specific tool HMRC uses in certain situations. For most UK businesses, you'll really only bump into it in two main scenarios, and each has its own distinct set of triggers.

Getting this right is non-negotiable. One wrong move could lead to a messy VAT return and an unwelcome letter from HMRC. The first, and perhaps most talked-about, scenario is the domestic reverse charge for the building and construction industry. The second, which is becoming incredibly common, involves buying services from suppliers based overseas.

The Domestic Reverse Charge for Construction Services

The construction industry has always had a unique relationship with VAT, largely to combat tax fraud. The domestic reverse charge, introduced on 1 March 2021, was a major shake-up aimed squarely at tackling "missing trader" fraud—where a supplier charges VAT, pockets the cash, and vanishes before paying HMRC. This wasn't a small problem; this kind of fraud has contributed significantly to the UK's VAT gap over the years. You can dive into the nitty-gritty by reading the official guidance on the VAT domestic reverse charge from GOV.UK.

So, how do you know if it applies to your job? The reverse charge is triggered when a VAT-registered business supplies specific construction services to another VAT-registered business that isn't the final customer, or 'end user'.

For the reverse charge to apply, all these boxes need to be ticked:

- Both Supplier and Customer are VAT Registered: The rule only ever applies between two VAT-registered businesses.

- Both Parties are CIS Registered: Both you (the subcontractor) and your customer (the contractor) must be registered under the Construction Industry Scheme (CIS).

- It's a 'Specified Service': The work must be on a specific list of construction services, like groundwork, bricklaying, or demolition. It doesn’t apply to things like architect fees or hiring scaffolding without labour.

- The Customer is Not the 'End User': This is the crucial part. An 'end user' is the person or business that the construction work is ultimately for. If your customer is simply passing your services on to their client as part of a larger project, the reverse charge applies. If your customer is the property owner or final developer, you charge VAT as normal.

The Reverse Charge for Services from Overseas

This second scenario is catching more and more businesses out, especially with the rise of digital tools. If your UK-based, VAT-registered business buys services from a supplier located anywhere outside the UK, you have to account for the VAT yourself using the reverse charge. This applies even if the supplier’s invoice doesn't mention VAT at all.

Just think about some of your regular business expenses—chances are, some of them are from international companies.

A Practical Example: Let's say your business spends £500 on advertising with Google (based in Ireland) or pays for a software subscription from an American company. In both cases, the service is being supplied from overseas to your UK business. You won't see VAT on the invoice they send you, but you are still responsible for accounting for the 20% VAT (£100 in this case) on your VAT return as a reverse charge transaction.

This whole process is designed to make sure VAT is paid at the correct UK rate, which keeps things fair between domestic and international suppliers. It also has a sneaky impact on your taxable turnover for VAT registration purposes, but we’ll get into that a bit later.

To help you get a quick read on whether a transaction needs the reverse charge, here's a simple checklist.

VAT Reverse Charge Applicability Checklist

| Scenario | Key Conditions For Application | Who Accounts for VAT |

|---|---|---|

| UK Construction | Both parties are VAT and CIS registered, the service is a specified one, and the customer is not the end user. | The Customer |

| Overseas Services | Your UK business buys services (like software, digital ads, or consultancy) from a supplier outside the UK. | The Customer |

Getting your head around these two core scenarios will give you a solid foundation for spotting when you need to act. The devil is always in the detail, so be sure to check the specifics of every transaction—especially in the construction sector, where correctly identifying the end user is everything.

How To Get Your Invoicing and VAT Returns Right for the Reverse Charge

Getting your head around the VAT reverse charge rules is one thing, but actually putting them into practice on your invoices and VAT returns is where the rubber meets the road. This is where compliance happens, and getting these details spot on is crucial for keeping your records clean and avoiding any costly headaches with HMRC.

The process splits into two sides of the same coin: what you do as the supplier issuing the invoice, and what you do as the customer receiving it. A simple mistake on either end can cause a real mess, so let's break it down.

What Suppliers Need To Put on Their Invoices

If you're a supplier and your services fall under the reverse charge, how you invoice has to change. The single most important thing to remember is that you do not charge VAT. That's right, the responsibility for sorting the VAT now shifts entirely over to your customer.

Your invoice must make it crystal clear that the reverse charge applies. This isn't optional—it's a firm requirement from HMRC.

So, what should your invoice look like?

- It needs all the usual details: your company name, address, and VAT number.

- Make sure you have your customer's name, address, and VAT number on there too.

- A clear description of the services you provided is essential.

- The amount due should be the net value, with no VAT added. The VAT amount should be shown as £0.00 or 0%.

And here's the kicker: you must add a specific note to the invoice. The wording doesn't have to be exact, but it must be unambiguous that the customer is on the hook for the VAT.

A simple, foolproof note is: "Reverse charge: Customer to pay the VAT to HMRC." You might also see phrases like "S55A VATA 94 applies" or simply "Reverse charge applies," which are also perfectly acceptable.

Once that invoice is sent, you just need to report the net value of the sale in Box 6 of your VAT return (the box for the total value of your sales). You don't put anything for this transaction in Box 1, because you haven't charged any output tax.

How Customers Should Process and Report the VAT

As the customer receiving a reverse charge invoice, you have the most important job. You have to account for the VAT, even though you haven't actually paid it to your supplier. You essentially act as both the supplier and the customer in HMRC's eyes. This is the "reverse" part of the charge in action.

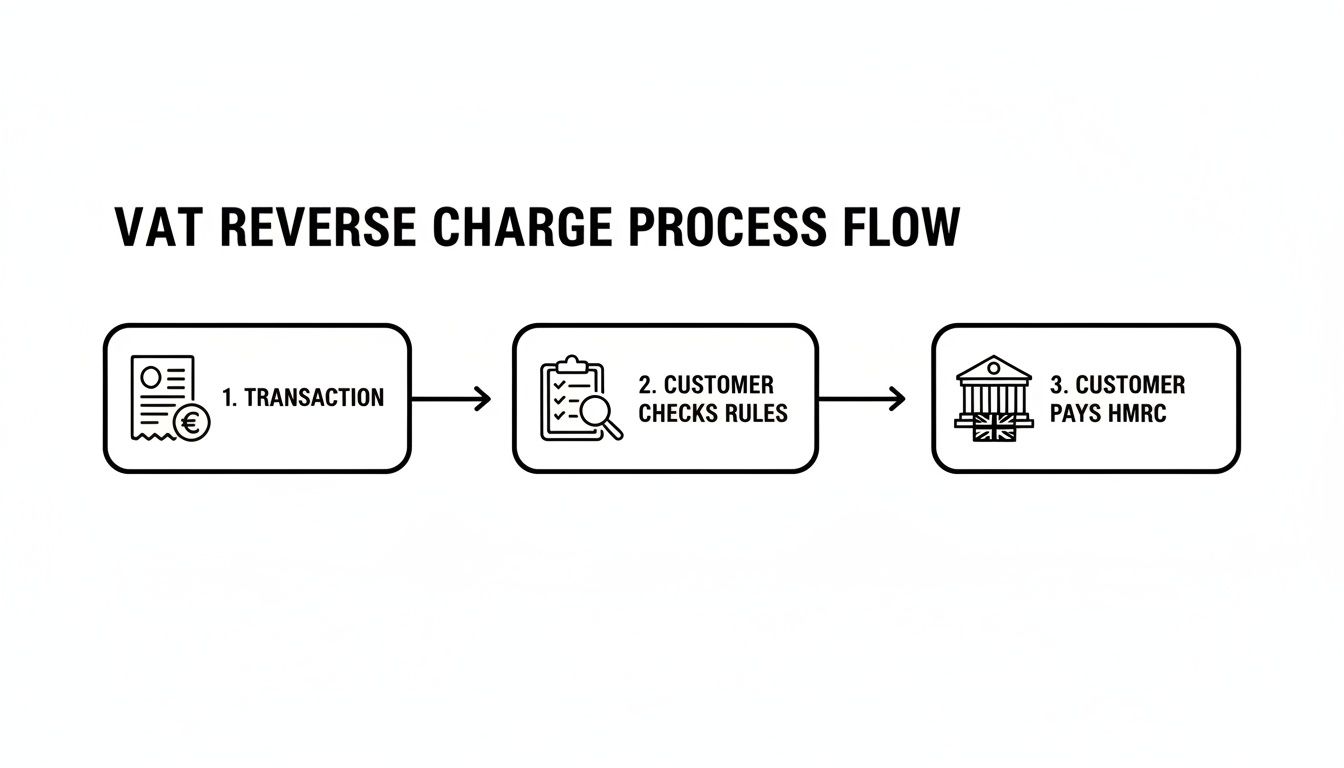

Let's walk through a quick example. Imagine you're a contractor, and you've just received an invoice from a subcontractor for £1,000 for construction services that fall under the rules. The standard VAT rate is 20%.

The flowchart below gives a good overview of how the responsibility flows from the transaction all the way to HMRC.

As you can see, the onus is squarely on you, the customer, to handle the VAT correctly.

Here’s exactly how you’d account for that £1,000 invoice on your VAT return:

- Work out the VAT: On £1,000, the VAT is £200 (20%).

- Box 1 (Output VAT): You must add this £200 to the VAT you owe on your sales.

- Box 4 (Input VAT): You then reclaim the same £200 as input tax, just as you would for any other business purchase you've paid VAT on.

- Box 6 (Total Sales): You don't include the net purchase in this box.

- Box 7 (Total Purchases): You do include the net purchase value of £1,000 here.

For most businesses, the £200 in Box 1 and the £200 in Box 4 cancel each other out, so there's no actual cash impact on your VAT bill. It's a tax-neutral transaction. But make no mistake, failing to report these figures in the right boxes is a compliance failure. To get this right every time, particularly with complex invoices, using a process like 3-way matching of invoices can be a lifesaver.

Let Your Accounting Software Do the Heavy Lifting

Trying to remember and track these double entries manually is just asking for trouble. This is where good accounting software like Xero really proves its worth. These platforms have built-in tax rates designed specifically for the domestic reverse charge.

When you're creating an invoice or entering a bill, you simply select the correct "Domestic Reverse Charge" tax code. The software then automatically posts the correct double-entry journals and makes sure the figures land in the right boxes on your VAT return. It takes human error almost completely out of the equation.

If you want to know more about what goes into a standard VAT invoice, have a look at our detailed guide on https://stewartaccounting.co.uk/what-should-be-on-a-vat-invoice/.

The Hidden Impact on Your VAT Registration Threshold

https://www.youtube.com/embed/f_n8la_ywgis

One of the sneakiest traps with the VAT reverse charge is how it affects your VAT registration threshold. It’s an easy mistake to make. Many small business owners assume the threshold is all about their UK sales, but that assumption can land you in hot water with HMRC.

Here’s the thing: when you buy services from suppliers outside the UK – think Google ads, Facebook marketing, or a software subscription from an American company – the value of those services gets added to your UK turnover for VAT registration purposes. This can tip you over the limit without you even realising it.

How Reverse Charge Pushes You Over the Limit

So, what’s going on here? In HMRC’s eyes, the value of those reverse charge services you buy counts as part of your "taxable turnover". Even though you aren't paying VAT to the overseas company directly, the rules treat it as if you’ve both supplied and received the service yourself.

This creates a kind of ‘notional’ turnover that counts towards the £90,000 registration threshold. It’s a detail buried deep in the regulations, but it has massive implications for any growing business using international digital tools to get ahead.

Let's walk through a common scenario. Imagine a small e-commerce business here in the UK. They aren't VAT registered yet, and their UK sales are climbing but are still safely under the threshold. To keep the momentum going, they're spending a fair bit on online advertising.

Here’s how the numbers stack up:

- UK Sales: Over a rolling 12-month period, they bring in £85,000.

- Overseas Ad Spend: They also spend £10,000 on ads with a big international tech company.

- Turnover Calculation: For VAT purposes, their turnover isn't £85,000. It’s £85,000 (from UK sales) plus £10,000 (from the reverse charge services), which comes to a total of £95,000.

Just like that, they’ve blown past the £90,000 VAT registration threshold and are now legally required to register.

The Consequences of Late Registration

Missing this can be painful. If you fail to register on time, HMRC can hit you with some serious financial penalties. They'll require you to backdate your registration to the day you actually crossed the threshold.

This means you'll owe VAT on all the sales you made from that date forward, even though you never charged it to your customers. On top of that hefty VAT bill, you’re also likely to face penalties for not notifying them on time.

For example, a sole trader in Falkirk with genuine UK sales of £80,000 a year might spend £15,000 on Google Ads in May 2024. Those ads fall under the reverse charge rules. That £15,000 has to be included in their taxable turnover calculation, pushing their total to £95,000 and triggering an immediate need to register for VAT. You can discover more insights about how these tax rules affect businesses on White Rose ePrints.

Proactively monitoring your turnover—including both your UK sales and the value of any services you buy from overseas—is essential. This isn't just good bookkeeping; it's a critical compliance step that protects your business from unexpected financial shocks.

The only way to stay ahead is to check your total taxable turnover on a rolling 12-month basis. Don't leave it until your year-end. A quick monthly review will help you see if you're getting close to the threshold, giving you plenty of time to prepare. For more on the current limits, have a look at our guide on the VAT registration limit in the UK. This proactive approach is the best defence against the severe penalties that come with late registration.

Common VAT Reverse Charge Mistakes and How to Avoid Them

The VAT reverse charge can be a real minefield. Even with the best intentions, a simple slip-up can quickly snowball into a compliance headache and unwelcome questions from HMRC. Knowing where things typically go wrong is the best defence for your business, whether you're the one raising the invoice or the one paying it.

Let's walk through some of the most common pitfalls we see in practice and, more importantly, how to steer clear of them. Think of this as a troubleshooting guide to help you handle these transactions confidently and avoid any costly mishaps.

Supplier Mistake: Incorrectly Charging VAT

This is probably the most frequent error we come across, and it almost always happens on the supplier's side. Out of pure habit or a misunderstanding of the rules, a supplier charges VAT on an invoice when the reverse charge should have been applied. This is especially common in the construction industry's complex supply chains.

- The Scenario: A subcontractor sends an invoice for £5,000 worth of qualifying services but adds £1,000 (20%) VAT on top, making the total bill £6,000.

- The Problem: This creates a mess for everyone. The subcontractor now owes that £1,000 to HMRC, but the customer can't reclaim it as input tax because it shouldn't have been charged in the first place.

- The Solution: The only clean way to fix this is for the supplier to issue a credit note for the full, incorrect invoice. Then, they need to raise a brand-new, correct invoice for the net amount (£5,000) which clearly states that the reverse charge applies and the customer must account for the VAT.

Customer Mistake: Forgetting to Account for VAT

On the flip side, the most common mistake for the customer is simply forgetting to do the reverse charge accounting on their VAT return. When an invoice lands on their desk with no VAT shown, it's easy for it to be processed like any other purchase, which is a major compliance failure.

- The Scenario: A contractor gets a valid reverse charge invoice for £10,000. They pay the supplier but then forget to account for the £2,000 of VAT on their next VAT return.

- The Problem: Because they didn't declare the £2,000 as output tax in Box 1 and as input tax in Box 4, they've filed an inaccurate return. If HMRC spots this, it can lead to penalties and interest charges.

- The Solution: You need a solid process for checking invoices from suppliers in relevant sectors. To catch these issues before they become problems, it's wise to implement robust two-way matching in accounts payable. This forces a check for reverse charge requirements before anything gets posted to your books.

Misidentifying the End User in Construction

In construction, the whole reverse charge system pivots on correctly identifying the 'end user'—the person who the work is ultimately for. If an intermediary contractor wrongly says they're the end user, it breaks the chain for everyone involved.

The onus is on the supplier to check their customer's status. If you have any doubt at all, ask for written confirmation that they are, or are not, an end user. That piece of paper is your proof that you did your due diligence.

Supplier Cash Flow Challenges

This one is less of a direct mistake and more of a painful side effect. Before the reverse charge came in, subcontractors would collect the 20% VAT from their customers and hold onto it until their VAT return was due. For many small businesses, this acted as a short-term cash flow buffer.

With the reverse charge, that cash never hits the supplier's bank account. If your business was relying on that VAT money as working capital, you could be in for a nasty shock. It's vital to re-forecast your cash flow based on receiving only the net amount of your sales, so you can be sure you've still got enough in the bank to cover your own expenses.

Getting Your VAT Reverse Charge Right: Where We Come In

Let's be honest, getting to grips with the VAT reverse charge can be a real headache. It’s a drain on your time and energy that you’d much rather be spending elsewhere. As we've covered, the rules are fiddly. You’ve got to get the invoice wording just right, keep a sharp eye on registration thresholds, and make absolutely sure every number ends up in the correct box on your VAT return. One small slip can lead to compliance headaches, paying the wrong amount of tax, and attracting the kind of attention from HMRC that nobody wants.

The admin side of things is a genuine burden. If you're a supplier, you suddenly have to get used to that 20% VAT not landing in your bank account, which can throw your cash flow forecasting out of whack. If you're the customer, the buck stops with you to account for the VAT correctly – adding another layer of risk to your bookkeeping. It’s one of those systems where a tiny mistake can snowball into a much bigger problem.

Let Us Take the Strain

This is where getting some expert help can turn a major chore into a background task you don't even have to think about. Instead of losing hours trying to make sense of dense technical guides, you can lean on professionals who live and breathe these rules every day. At Stewart Accounting Services, we take the entire compliance burden off your plate.

We mix our in-depth knowledge with the efficiency of top-notch accounting software like Xero. Here’s what that looks like in practice:

- Spot-On Invoicing: We make sure your invoices go out with the precise wording and details required every single time.

- Flawless Returns: Your VAT returns will be prepared and submitted perfectly, with every reverse charge transaction accounted for correctly.

- Keeping Watch: We monitor your turnover, including those overseas service purchases that are so easy to overlook, to ensure you stay on the right side of the VAT registration threshold.

Handing this over to an expert isn’t just about ticking a box. It’s about buying back your peace of mind and freeing up your mental energy to focus on what you’re truly good at – running and growing your business.

At the end of the day, managing the VAT reverse charge isn't just about dodging penalties. It's about having solid financial processes that support your business as it grows. Let our team handle the tricky stuff, so you can have the confidence of knowing your tax affairs are in expert hands.

Your VAT Reverse Charge Questions Answered

Even when you think you’ve got a handle on the rules, the VAT reverse charge can throw up some tricky situations. Here are a few of the most common questions we get from UK business owners, with straight-talking answers to help you stay compliant.

What Happens If I've Wrongly Charged VAT on a Reverse Charge Invoice?

If you're the supplier and you've accidentally charged VAT when you shouldn't have, you need to fix it, and fast. The only proper way is to issue a credit note to cancel the incorrect invoice, then create a new, correct one. This new invoice must show zero VAT and clearly state that the reverse charge applies.

This isn't just a minor admin error; it's a serious mistake. You're still on the hook to pay that incorrectly charged VAT over to HMRC. What's worse, your customer can't claim it back as input tax, which creates a real financial headache for everyone involved. Sorting it out quickly is key to avoiding penalties and keeping your client relationships on solid ground.

A simple refund of the VAT amount won't cut it. You have to follow the correct procedure: credit the original invoice and raise a new one that correctly applies the VAT reverse charge.

Does the Reverse Charge Apply if My Customer Isn't VAT Registered?

It really depends on the context. When we're talking about the domestic reverse charge for construction services, the rules are clear: it only kicks in if both you (the supplier) and your customer are VAT registered. If your customer isn't registered, you just charge VAT as you normally would.

But for services bought from overseas, it’s a different story. In this case, the reverse charge itself can be the very thing that tips a UK business over the VAT registration threshold. The value of those imported services counts towards your UK turnover, and that can easily push you into needing to register.

How Will the Reverse Charge Hit My Cash Flow as a Subcontractor?

For subcontractors, the impact on cash flow can be a real shock to the system. Previously, you'd get paid the full invoice amount, including the 20% VAT, from the main contractor. That VAT money would sit in your bank account, often acting as a useful bit of working capital until your VAT return was due.

Now, with the reverse charge, that VAT payment never reaches you. Your customer accounts for it directly with HMRC. This means a significant drop in the cash coming into your business, which can be a real problem if you haven't prepared. It’s absolutely essential to update your cash flow forecasts to reflect that you’ll only be receiving the net value of your sales. Anyone on the Flat Rate Scheme should also take a hard look at whether it still works for them – it often doesn't.

Getting your head around VAT complexities like the reverse charge can be tough. The team at Stewart Accounting Services is here to give you the expert advice you need, making sure you stay compliant and protect your business’s cash flow. Let's talk about how we can support you.