At its core, Accounts Payable (AP) is the money your business owes to its suppliers, while Accounts Receivable (AR) is the money your customers owe to you. Think of AP as your “to-pay” list for goods and services you’ve already received, and AR as the cash you’re waiting on from sales you’ve made on credit.

The Foundations of Your Business Finances

Imagine your business finances are like a bathtub. The water coming in from the tap is your Accounts Receivable, and the water going out the drain is your Accounts Payable. To keep the water at the right level – not overflowing and not running dry – you need to manage both the inflow and outflow carefully. This balancing act is the key to your company’s financial health.

What is Accounts Payable?

Accounts Payable, or AP, covers all your short-term debts to suppliers. Every time you buy stock, order office supplies, or get a bill from your accountant, the amount of that invoice lands in your AP ledger. It’s essentially a running list of who you owe money to and when it’s due.

On your balance sheet, Accounts Payable is categorised as a current liability. This simply means it’s a debt you’re expected to pay off within the next year, showing what your business owes to its creditors.

Getting this right isn’t just about paying bills on time. It’s about building strong relationships with your suppliers and avoiding costly late fees. To give you a sense of scale, the UK public sector alone had total payables of £34,338,000, which shows just how significant these obligations can be. You can dive deeper into these figures in the UK Statistics Authority’s annual report.

What is Accounts Receivable?

Accounts Receivable, or AR, is the other side of the equation. It represents all the money that your customers owe you for products they’ve bought or services you’ve provided on credit. Each time you send an invoice to a client, you create an AR entry.

Because this is money you expect to collect in the near future, it’s considered a current asset on your balance sheet. Grasping this difference is the first step to truly understanding your business’s liquidity and short-term financial stability.

Accounts Payable vs Accounts Receivable At a Glance

To make it even clearer, let’s break down the key differences between Accounts Payable and Accounts Receivable side-by-side.

| Attribute | Accounts Payable (AP) | Accounts Receivable (AR) |

|---|---|---|

| Cash Flow Direction | Money Out | Money In |

| Represents | Money your business owes | Money your business is owed |

| Balance Sheet Item | Current Liability | Current Asset |

| Goal | Manage and schedule payments strategically | Collect payments as quickly as possible |

| Example | Paying an invoice for raw materials | Sending an invoice to a client for services |

Seeing them laid out like this really highlights how AP and AR are two halves of the same whole, managing the flow of money in and out of your business.

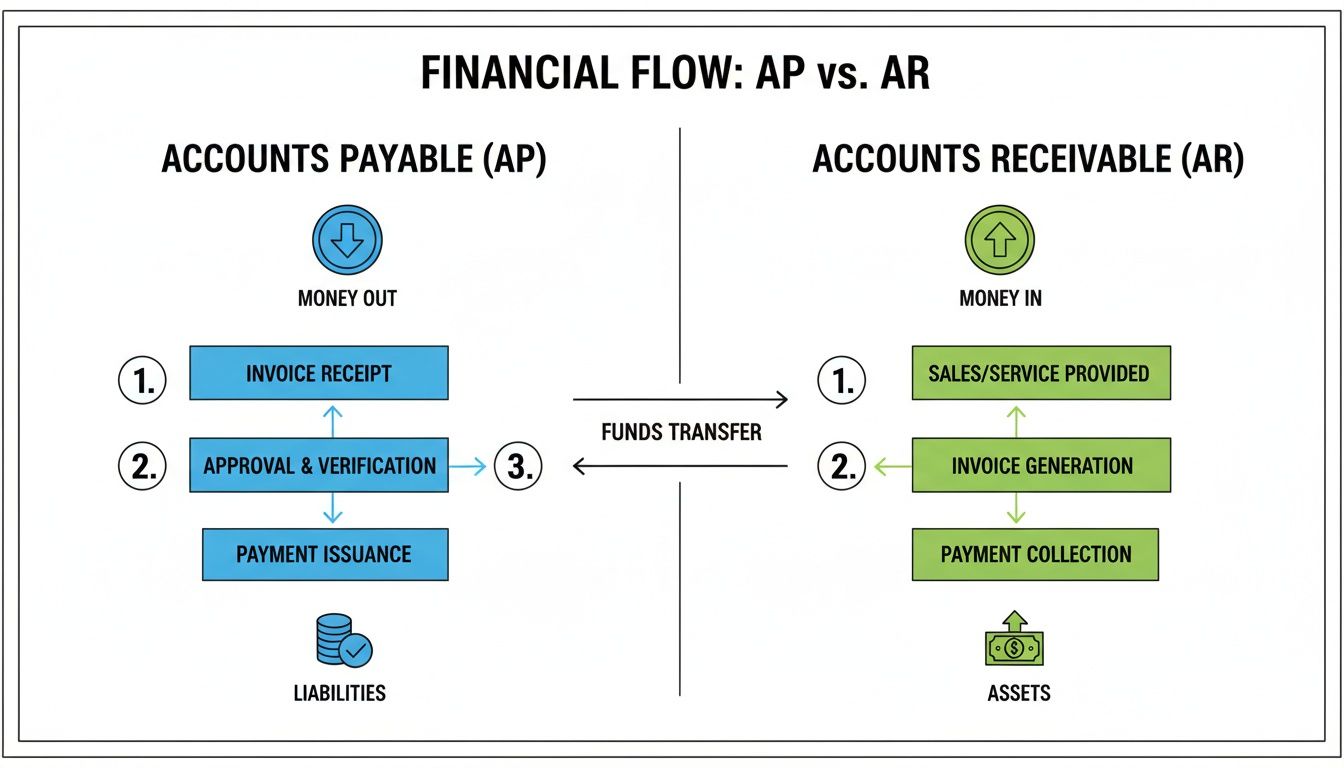

What Happens to a Single Invoice? A Tale of Two Journeys

Every invoice tells a story, but it has two very different endings depending on which side of the transaction you’re on – paying it or getting paid. Getting your head around this dual journey is the key to understanding what accounts payable and receivable really mean for your business.

Let’s start with that moment an invoice from a supplier lands in your inbox. That single document kicks off the entire Accounts Payable (AP) process. It’s more than just a bill; it’s a task that needs to be managed carefully to keep your suppliers happy and control the cash flowing out of your business.

This diagram shows the two sides of the coin: the path money takes when it leaves your business (Accounts Payable) versus when it comes in (Accounts Receivable).

As you can see, while AP is all about timing your payments strategically, AR is about getting paid efficiently. Both have a massive, direct impact on the cash you have on hand.

The Accounts Payable Workflow: Money Out

The minute a supplier’s invoice arrives, it begins its journey through your business. This whole process is a set of checks and balances to make sure you only pay for what you actually ordered and received, and that you pay on time—but not too early.

The typical AP steps look something like this:

- Invoice Arrives & Gets Checked: The invoice is received and immediately cross-referenced with your purchase orders and delivery notes. Did you get what you asked for? Is the price right? This is your first line of defence.

- Internal Sign-Off: The invoice is then routed to the right person—a department head or budget holder—for approval. This step confirms the expense is legitimate and authorised.

- Payment is Scheduled: Once approved, it’s logged in your accounting software and scheduled for payment. Smart cash flow management means paying as close to the due date as you can, letting you hold onto your cash for longer.

If any part of this chain breaks, you could face late payment fees or, worse, damage relationships with the very suppliers you rely on.

The Accounts Receivable Workflow: Money In

Now, let’s flip the coin. When you’re the one sending an invoice to a customer, you kick-start the Accounts Receivable (AR) journey. Here, your goal is the complete opposite of AP: you want that money in your bank account as fast as humanly possible.

For every business managing its Accounts Payable, there’s another business on the other side running its Accounts Receivable. Your sales invoice is their liability, just as their sales invoice is yours.

The AR lifecycle is a race against the clock:

- Invoice Sent: You create a clear, accurate invoice detailing what you provided, your payment terms, and a firm due date. Getting it out the door quickly is the first, crucial step.

- Waiting & Watching: You then track the invoice. As the due date gets closer, a friendly reminder might be needed. You can’t just send it and forget it.

- Cash In & Matched: This is the best part—the payment hits your account. The final step is to mark the invoice as paid and reconcile the payment in your books, closing the loop.

Any friction here directly squeezes your cash flow. A slow AR cycle can mean that even a profitable, growing business finds itself unable to pay its own bills. Truly mastering your finances means getting both of these mirrored workflows running like clockwork.

How AP and AR Directly Impact Your Cash Flow

Profit on paper is one thing, but if you can’t pay your bills, that profit is just a number. This is where getting a grip on your accounts payable and receivable becomes a real business superpower, giving you direct control over the lifeblood of your company: its cash flow.

Think of it as managing the flow of traffic. Your accounts payable is the cash flowing out, while your accounts receivable is the cash flowing in. Your job is to keep both moving smoothly to avoid a pile-up.

Smart management of Accounts Payable isn’t just about paying suppliers; it’s about strategically managing your cash outflow. By using the full payment terms you’ve agreed with your suppliers—say, paying on day 29 of a 30-day term—you keep money in your business for as long as possible. This isn’t about paying late, but about being clever with your timing.

This strategic approach to payments gives you much-needed flexibility. The cash that stays in your account for longer can be used for unexpected opportunities, cover emergency costs, or simply act as a crucial safety net. Handling your payables efficiently is a core part of optimising working capital and keeping your business resilient.

Speeding Up Cash Inflow with Smart Receivables

On the flip side, efficient Accounts Receivable management is all about getting paid faster. The goal is simple: shorten the time between issuing an invoice and seeing that money land in your bank account. This is the fuel your business needs to operate and grow.

A business can be wildly profitable yet still fail because of poor cash flow. Outstanding invoices (your AR) are technically assets, but you can’t pay your rent or staff with an asset. You need cash.

Getting this right involves a few key actions:

- Send clear invoices, fast: The sooner your invoice is out the door, the sooner the payment clock starts ticking.

- Offer easy payment options: Making it simple for clients to pay you can dramatically cut down delays. Think online payments, not just bank transfers.

- Have a consistent follow-up process: A system of polite but firm reminders for overdue invoices is absolutely essential.

A proactive approach here ensures your cash reserves are constantly being topped up, keeping the business healthy.

A Freelancer’s Cash Flow Balancing Act

Let’s look at a freelance graphic designer. Every month, they have Accounts Payable in the form of design software subscriptions, which are due on the 28th. They also have Accounts Receivable from various clients, with invoices that have different due dates.

If the designer’s clients pay late, their bank account could be empty when the software payment is due. Even though they’ve technically earned the money, they face a real cash crunch.

To avoid this, the designer has to manage both sides of the equation. They can chase client payments (AR) a week before the due date, ensuring the cash arrives on time. At the same time, they make sure funds are set aside for the software payment (AP), paying it on the 27th to keep their essential tools running without stress. This simple, coordinated dance between accounts payable and receivable is what keeps their business financially stable.

Measuring What Matters with AP and AR Metrics

You can’t improve what you don’t measure. It’s an old saying, but it’s especially true when it comes to your business’s finances. Moving beyond guesswork means tracking a few simple but powerful metrics that reveal the real health of your cash flow, specifically your accounts payable and receivable.

Think of these key performance indicators (KPIs) as the dashboard in your car. They give you a clear, data-backed view of how efficiently money is moving in and out, helping you make smarter decisions that directly impact your bank balance.

Instead of getting lost in a sea of complicated spreadsheets, focusing on just a couple of core metrics for both AP and AR will give you the most important insights.

Are You Paying Suppliers Too Quickly or Too Slowly?

When it comes to Accounts Payable, the metric you really need to watch is Days Payable Outstanding (DPO).

In simple terms, DPO tells you the average number of days it takes your company to pay its suppliers. A higher DPO means you’re holding onto your cash for longer, which can be great for your working capital. But there’s a catch.

Push it too far, and a DPO that’s too high can start to look like a red flag to your suppliers. They might think you’re in financial trouble, which could damage those crucial relationships. It’s a delicate balancing act between optimising your cash and keeping your partners happy.

The formula looks like this:

DPO = (Average Accounts Payable / Cost of Goods Sold) x Number of Days in Period

This little calculation reveals how well you’re managing the credit terms your suppliers give you.

How Quickly Are Your Customers Actually Paying You?

On the Accounts Receivable side of things, the big one is Days Sales Outstanding (DSO).

This KPI shows you the average number of days it takes for your customers to pay you after you’ve sent an invoice. Obviously, a low DSO is what you’re aiming for – it means cash is flowing into your business quickly.

A high DSO, on the other hand, is a major warning sign. It tells you that your cash is getting tied up in unpaid invoices, which can seriously restrict your ability to operate and grow. It might mean you need to get tougher with your credit control or rethink your collections process entirely.

To get a better handle on this, you can learn more about how to improve your debtor days to boost your cashflow and see what a healthy number looks like in your industry.

Here’s the formula for DSO:

DSO = (Average Accounts Receivable / Total Credit Sales) x Number of Days in Period

Putting It All Together

While DPO and DSO are the headline acts, a few other metrics can give you an even clearer picture of your financial health. Here’s a quick rundown of the essentials.

| Essential AP and AR Key Performance Indicators |

| :— | :— | :— |

| KPI | What It Measures | Why It Matters to Your Business |

| Days Payable Outstanding (DPO) | The average number of days it takes you to pay your suppliers. | Helps you manage working capital. A high DPO means you hold cash longer, but too high can strain supplier relationships. |

| Days Sales Outstanding (DSO) | The average number of days it takes customers to pay you. | A direct measure of cash flow efficiency. A low DSO means you’re getting paid faster, improving liquidity. |

| Cash Conversion Cycle (CCC) | The time (in days) it takes to convert inventory into cash from sales. | This is the big picture. It shows how long your cash is tied up in the entire sales process, from paying suppliers to getting paid by customers. |

| Invoice Processing Time | How long it takes your team to process a supplier invoice from receipt to payment. | A key efficiency metric. Faster processing reduces late payment risks and allows you to capture early payment discounts. |

| Bad Debt to Sales Ratio | The percentage of sales that you have to write off as uncollectible debt. | A critical indicator of your credit control effectiveness. A rising ratio warns you that your credit policies may be too loose. |

By consistently keeping an eye on these KPIs, you gain a factual, real-time understanding of your business’s cash conversion cycle. You can spot the bottlenecks, fix them quickly, and make sure your business stays financially stable and ready for whatever comes next.

How Modern Tools Can Tame Your Invoices

Still wrestling with spreadsheets and an overflowing in-tray? If you’re managing accounts payable and receivable manually, you’ll know it’s not just time-consuming—it’s also a minefield for costly human errors. It’s time for an upgrade. Modern software can transform this financial chaos into a smooth, automated system that gives you back countless hours.

Cloud accounting platforms like Xero and QuickBooks have become the central command centre for today’s businesses. They get your financial data out of static files on a single computer and into a dynamic, accessible online hub. This shift is the first, crucial step towards a much more organised and efficient way of handling your money.

This kind of real-time visibility lets you see exactly what you owe and who owes you at a glance, making financial decisions faster and far more accurate.

Supercharge Your Financial Hub With Add-On Apps

But the real magic happens when you integrate specialised add-on apps that solve specific headaches in your payables and receivables workflow. These tools plug directly into your main accounting software, creating a powerful, interconnected system.

For Accounts Payable (AP), this means saying goodbye to manual data entry for good. Imagine tools that can:

- Scan and Capture Data: Apps like Dext or AutoEntry can automatically read information from supplier invoices—whether they’re PDFs or photos—and create draft bills in your accounting software.

- Automate Approvals: You can set up rules to automatically send invoices to the right person for approval, cutting out endless email chains and delays.

This sort of automation massively reduces the risk of things like duplicate payments and frees up your team to focus on more valuable work. To get the most from these modern solutions, it’s worth learning how to effectively automate invoice processing and take proper control of your outgoing payments.

Get Paid Faster With Automated Receivables

For Accounts Receivable (AR), the name of the game is getting cash in the door faster. Add-on apps make a huge difference here by automating the often-uncomfortable job of chasing payments. You can set up systems that send polite, customised reminders at set intervals—say, a week before the due date, on the due date, and a week after.

A recent study found that automating invoice reminders can reduce the time it takes to get paid by an average of 3-8 days. For a small business, that improvement in cash flow can be a real game-changer.

This consistent, professional follow-up helps you maintain good client relationships while drastically improving your collection times. You can explore our detailed guide on how to automate invoice reminders using accounting software to see exactly how to put this into practice.

By adopting these tools, you’re not just buying software; you’re building a resilient financial system that minimises effort and maximises efficiency.

Knowing When It’s Time to Ask for Financial Help

As your business picks up steam, what started as a manageable pile of paperwork can quickly turn into a mountain. The DIY approach that served you well in the beginning can start to hold you back, becoming a liability rather than a cost-saver.

Recognising the signs that you need a professional hand is key to sustainable growth. Are you spending more time chasing invoices than chasing new leads? That’s a classic signal. Another huge red flag is a constant struggle with cash flow, even when your sales figures look healthy. Maybe the thought of VAT registration keeps you up at night, or you just feel swamped by the sheer volume of financial admin.

Who Does What? Understanding the Roles

It’s crucial to know who to call for what. Think of it this way: a bookkeeper is on the front lines, managing the day-to-day financial pulse of your business. They’re the ones making sure your accounts payable and receivable ledgers are spot-on and everything is recorded correctly.

An accountant, on the other hand, takes a bird’s-eye view. They use the clean, organised data from your bookkeeper to offer strategic advice. They’ll help with big-picture stuff like tax planning, financial forecasting, and making major business decisions.

Deciding to bring in help isn’t admitting defeat; it’s a smart, strategic move towards efficiency. Freeing yourself from daily financial admin lets you get back to focusing on what you do best—growing your business.

Ultimately, knowing when to call in an expert is about protecting your most valuable asset: your time. For business owners who need to get their day-to-day finances in order, looking into organisations of certified bookkeepers is a great first step toward gaining clarity and control.

Answering Your Top Questions About AP and AR

Now that we’ve covered the basics, let’s dig into a few common questions that pop up when business owners start getting to grips with their accounts payable and receivable.

Can the Same Person Handle Both AP and AR?

In a tiny business, it’s not uncommon for one person to wear many hats, including managing both AP and AR. However, as soon as you can, it’s a very good idea to split these roles.

Think of it as having one person in charge of the cash drawer and another in charge of the till roll. By separating the management of money coming in (AR) from money going out (AP), you create a natural system of checks and balances. This simple step is one of the most effective ways to reduce the risk of fraud and catch costly errors before they snowball.

Where Do I Find AP and AR on a Balance Sheet?

These two accounts sit on opposite sides of the balance sheet, which perfectly reflects their different functions in your business finances.

- Accounts Payable (AP): You’ll find this listed under Current Liabilities. It’s a running total of the short-term debts you owe to your suppliers.

- Accounts Receivable (AR): This is located under Current Assets. It represents the money your customers owe you, which you expect to collect soon.

Is Accounts Payable a Debit or a Credit?

This is where a little bit of bookkeeping theory comes in handy. Accounts Payable is a liability, so it normally carries a credit balance.

When a supplier’s bill lands on your desk, your bookkeeper credits the AP account to show that your debt has increased. Once you pay that bill, they debit the AP account to bring that balance back down.

On the flip side, Accounts Receivable is an asset, so it has a normal debit balance. When you send an invoice to a customer, you debit AR to record the money they owe you. When they pay up, you credit AR to clear their debt.

Getting this principle right is the cornerstone of accurate bookkeeping. Every transaction has two sides, keeping your financial records balanced and giving you a true picture of your business’s health.

At Stewart Accounting Services, we turn financial complexity into clarity. If you’re ready to master your cash flow and focus on growing your business, our expert team is here to help with everything from bookkeeping to strategic financial planning. Let us help you achieve more time, more money and a clearer mind.