Auto enrolment is one of those phrases you hear a lot as a business owner. But what does it actually mean for you? In a nutshell, it's a government initiative that makes it compulsory for UK employers to put their eligible staff into a workplace pension.

The idea is simple: you and your employee both pay in, building a savings pot for their retirement. It's designed to get more people saving for the future, and as an employer, you're at the heart of making it happen.

What Auto Enrolment Pension Means for Your Business

Getting to grips with your employer duties can feel like a bit of a minefield at first. But understanding the core concept of auto enrolment makes everything else fall into place. It’s essentially a mandatory workplace savings plan, rolled out because the government realised far too few people were putting money aside for their later years.

Think of it as a three-way savings partnership. Your employee contributes a portion of their salary. You, as their employer, are legally required to contribute too. And to top it off, the government chips in through tax relief, giving your employee's savings a welcome boost. This isn't a 'nice to have' – it's the law for pretty much every single employer in the UK, whether you have one employee or one thousand.

Your Fundamental Role as an Employer

As the business owner, the responsibility for getting this right lands squarely on your shoulders. You’re legally required to choose a compliant pension scheme, enrol the right people, and do it all on time. It's more than just a bit of admin; it’s a core legal duty you have to your team.

Your main responsibilities boil down to a few key actions:

- Assessing your workforce: You need to work out exactly who is eligible for auto enrolment.

- Choosing a pension provider: Selecting a suitable scheme that meets all the government's rules is one of your first big decisions.

- Making contributions: You must calculate and pay the minimum employer contributions every single pay period, without fail.

- Communicating with staff: There are specific, formal letters you have to send to your team explaining how it all works and what their choices are.

Fulfilling these duties is about more than just staying on the right side of the law; it's about playing a crucial part in your employees' long-term financial wellbeing. Get it wrong, and The Pensions Regulator can issue some hefty penalties. Getting it right from day one is always the smartest, and cheapest, option.

Understanding Which Employees You Must Enrol

It’s a common misconception that every single person on your payroll needs to be put into a pension scheme. The reality is a bit more nuanced. Your legal duties as an employer hinge on a worker's age and how much they earn, which neatly sorts them into a few distinct groups.

Getting this right from the start is absolutely crucial. The system is designed this way to ensure you're enrolling those who are most likely to benefit from long-term saving. This means your obligations for a full-time manager will look very different from those for a part-time student working summer holidays.

The Three Main Worker Categories

When you assess your team, each person will fit into one of three categories. Each one comes with a specific, non-negotiable action you need to take.

-

Eligible Jobholders: This is the core group. You must automatically enrol them into your workplace pension. They are aged between 22 and the State Pension age and earn more than £10,000 a year. No ifs, no buts.

-

Non-Eligible Jobholders: This group has the right to opt in. They meet one of the criteria (age or earnings) but not both. If they ask to join, you must let them in and contribute to their pension just as you would for an eligible jobholder.

-

Entitled Workers: These employees can ask to join a pension scheme, and you have to give them access. The key difference here is that you are not legally required to make employer contributions, although you can certainly choose to do so. These are typically your lowest earners, making less than £6,240 a year.

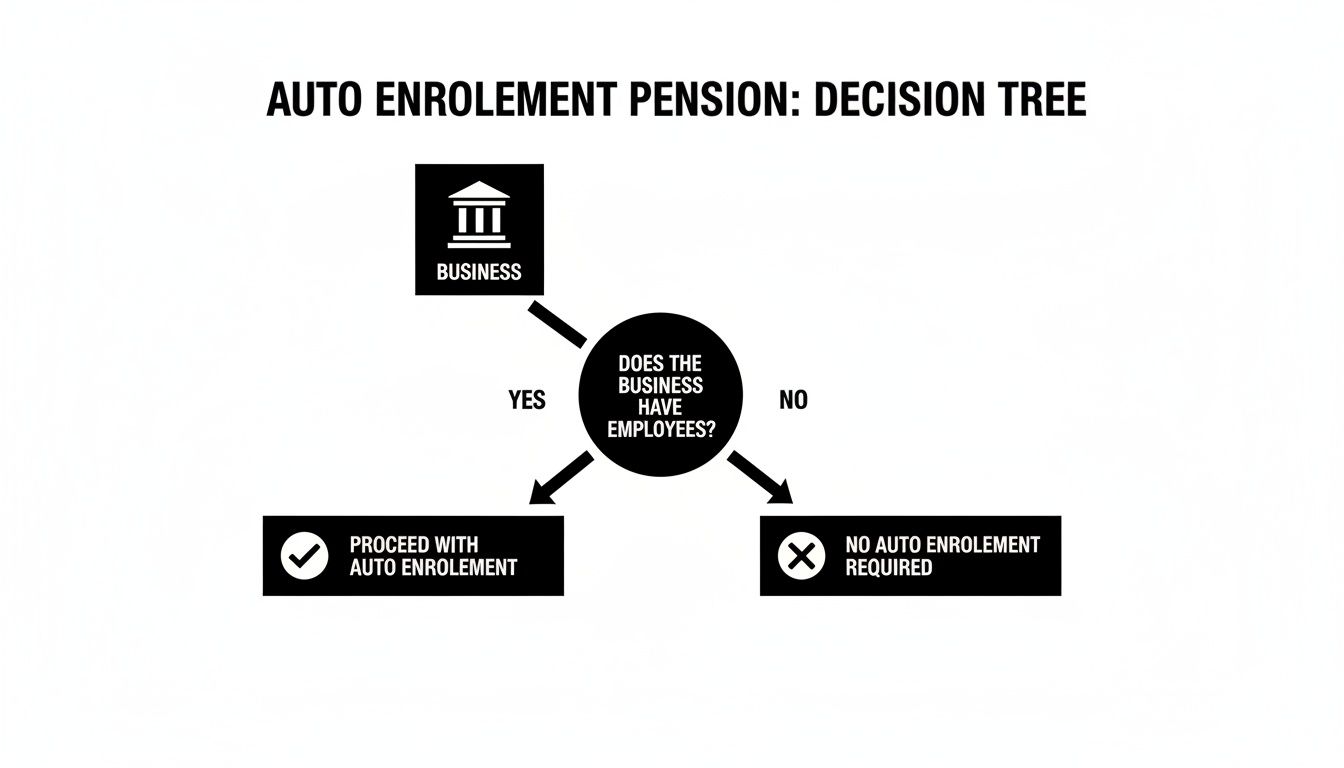

This decision tree gives you a great visual road map for figuring out who belongs where.

Think of the flowchart as a quick guide to get you from an employee's status to your specific legal duty—whether that’s mandatory enrolment or simply providing the option to join.

Employee Categories and Your Auto Enrolment Duties

To avoid any confusion (and potential fines from The Pensions Regulator), it’s vital to categorise your team correctly. This table breaks down your obligations for each type of worker, cutting through the jargon.

| Worker Category | Age Range | Qualifying Earnings | Your Legal Duty |

|---|---|---|---|

| Eligible Jobholder | 22 to State Pension Age | Over £10,000 | Automatically enrol and contribute. |

| Non-Eligible Jobholder | 16-21 or State Pension Age to 74 | Over £10,000 | Must offer the option to opt in. If they join, you must contribute. |

| Non-Eligible Jobholder | 16-74 | Between £6,240 and £10,000 | Must offer the option to opt in. If they join, you must contribute. |

| Entitled Worker | 16-74 | £6,240 or less | Must provide access to a pension scheme if they ask, but you are not required to contribute. |

Remember, this isn't a one-and-done task. You need to keep an eye on your employees' circumstances every single time you run payroll.

A birthday or a pay rise could easily push an employee from one category into another, triggering new auto enrolment duties for you. This is why ongoing assessment is so important.

How to Calculate and Manage Pension Contributions

Getting your head around the numbers is a crucial part of your auto enrolment duties. It’s not just about ticking the box to enrol your staff; it’s about making sure the correct amount of money lands in their pension pot, on time, every time. This involves a three-way partnership: you, your employee, and the government (chipping in with tax relief).

At the moment, the legal minimum contribution into an employee's pension is 8% of their 'qualifying earnings'. This isn't all on you, though. The cost is split. As the employer, you're required to put in a minimum of 3%, while your employee covers the remaining 5%. This shared approach is what makes the whole system work.

This setup has been a game-changer for pension saving in the UK. Research shows that while most stick close to the 8% minimum, employers’ contributions actually make up around 62% of the total funds paid in. It really highlights the vital role businesses like yours play in securing their team's future. You can dig deeper into these trends by exploring the latest findings on pension contribution rates in the UK.

Understanding Qualifying Earnings

So, what are these contributions actually calculated on? The calculation isn't based on an employee's entire salary. Instead, it applies to a specific slice of their earnings known as qualifying earnings.

For the 2024/25 tax year, this is the band of earnings between £6,240 and £50,270 a year.

Essentially, you only calculate pension contributions on the money an employee earns within this window. The first £6,240 they make is ignored for pension purposes, and so is anything they earn over the £50,270 upper limit. It’s a system designed to keep contributions fair and manageable for everyone, from lower-paid staff to high earners.

A Practical Payslip Example

Let's break it down with a quick, real-world example. Say you have an employee, Sarah, who earns £28,000 a year (which is £2,333 per month). Here's how the maths works:

- Work out her qualifying earnings: First, we take her annual salary and subtract the lower threshold: £28,000 – £6,240 = £21,760. This is the figure we use for all the pension sums.

- Calculate the total 8% contribution: £21,760 x 8% = £1,740.80 per year.

- Figure out your 3% employer contribution: £21,760 x 3% = £652.80 per year (or £54.40 a month). This is what it costs your business.

- And finally, the 5% employee contribution: £21,760 x 5% = £1,088 per year (or £90.67 a month). This amount is deducted from Sarah’s gross pay.

This calculation has to be run for every eligible employee, every single pay run. It’s precisely why modern, integrated payroll software has become a necessity, not a luxury. It ensures you stay accurate and compliant without the headache of manual calculations.

The Power of Tax Relief

One of the best perks of auto enrolment is tax relief. Think of it as a government-funded top-up for your employee's pension pot.

Here’s how it works: the money an employee contributes is taken from their gross pay, before income tax is applied. The government then adds the tax they would have paid on that amount directly into their pension.

For a basic rate taxpayer, this means they only need to physically contribute 4% of their qualifying earnings to see the full 5% land in their pension. The extra 1% is the tax relief bonus. It’s a brilliant way to boost their savings, and it doesn't cost your business a penny more. For a closer look, check out our guide on pension contributions and their tax benefits for employers.

Meeting Your Ongoing Employer Responsibilities

Getting your auto-enrolment pension scheme up and running is a great start, but it's really just the beginning. Your duties don't stop once the system is in place. Think of it less as a one-time task you can tick off a list and more as a continuous cycle of responsibilities that becomes part of your regular routine.

Staying compliant means creating a solid, repeatable process to manage these legal duties throughout the year. If you manage these tasks proactively, you’ll avoid last-minute panic and, more importantly, protect your business from hefty penalties issued by The Pensions Regulator (TPR). It's a non-negotiable part of running a payroll and employing people in the UK. When you're managing a pension scheme, you also need to be aware of your fiduciary responsibilities to always act in your employees' best interests.

Your Year-Round Compliance Checklist

To stay on the right side of the law, there are several key actions you need to perform regularly. The smartest way to handle this is to build these tasks directly into your existing payroll process. For a broader look at how this all fits together, our guide on https://stewartaccounting.co.uk/what-is-paye-for-employers/ is a great resource.

Here are the core duties you'll be managing on an ongoing basis:

- Monitoring Staff Eligibility: Every single time you run payroll, you have to check if any employees now qualify for auto-enrolment. This could be due to a pay rise that pushes them over the earnings threshold or because they've had a birthday that makes them eligible.

- Managing Contributions: You're responsible for calculating and deducting the correct employee contributions, adding your own employer contribution, and then paying the full amount over to your pension provider on time.

- Processing Opt-Outs and Opt-Ins: Staff have the right to leave the scheme or ask to join it. You must handle these requests promptly and accurately, making sure payroll is adjusted correctly from the very next pay run.

- Keeping Accurate Records: The law says you must keep detailed records of everything related to auto-enrolment. This includes proof of communications sent to staff, contributions paid, and opt-out notices received.

The Declaration of Compliance

Within five months of your staging date (the official day your duties started), you absolutely must complete a Declaration of Compliance. This is an online form you submit to The Pensions Regulator (TPR) to formally confirm that you've met all your legal obligations.

This declaration isn’t just paperwork—it’s a legal requirement. Missing the deadline will automatically trigger a fine, so treat it as a critical, non-negotiable step in your setup process. It's your official statement that you've done everything by the book.

Re-enrolment Every Three Years

Auto-enrolment is designed to be a long-term system, which includes a crucial three-year cycle called re-enrolment. Roughly every three years, you have to put any eligible staff who previously opted out back into your pension scheme. It gives them another chance to start saving for retirement.

You get to choose a re-enrolment date that falls within a six-month window—that's three months before or three months after the third anniversary of your original staging date. Once you've re-enrolled the relevant staff, you have to complete a re-declaration of compliance to let TPR know you've fulfilled your duties all over again.

Choosing the Right Pension Scheme for Your Company

Picking a workplace pension provider is one of the biggest hurdles you'll face when setting up auto enrolment. This isn't just about ticking a box for compliance. The right scheme can make your life easier by slotting neatly into your payroll and offering a decent service to your team. Get it wrong, and you could be dealing with the fallout for years.

For most small and medium-sized businesses, the choice often boils down to a handful of well-known providers geared up for auto enrolment. You’ve got the government-backed NEST (National Employment Savings Trust), alongside other popular master trusts like The People’s Pension or Smart Pension. Each has its own way of charging and a different set of features, so it really pays to look under the bonnet.

Key Factors to Compare

When you start comparing your options, it's easy to get bogged down in the finer details of investment funds. My advice? Park that for a moment and focus on the practical stuff that will impact your day-to-day business. Simplicity and efficiency should be your priority.

Here are the crucial things to look for:

- Setup Simplicity: How easy is it to actually get started? A provider with a clear, guided setup process will save you a world of pain and make sure you don't miss any critical steps.

- Payroll Integration: This one is non-negotiable. Does the pension provider talk to your payroll software? Good integration is a game-changer; it automates all the calculations and data transfers, which massively cuts down on human error.

- Administration Costs: Are there any setup fees or ongoing management charges for you, the employer? Some schemes are completely free for businesses, but others have hidden costs, so read the fine print carefully.

- Employee Charges: It's also worth understanding what fees your staff will be paying, as this directly eats into their retirement pot. You'll typically see an annual management charge and sometimes a fee on each contribution they make.

Choosing a provider is a huge step, but it’s also a fork in the road. You can decide to handle the entire administrative load yourself, or you can choose to outsource it. For most busy business owners, getting a professional to manage it is simply the most sensible path.

The Advantage of Outsourcing Pension Management

Auto enrolment has been a massive success since it rolled out in 2012. We now have 89% of eligible workers paying into a pension—that’s 21.7 million people. But while that’s great news for savers, it’s also added a significant administrative burden for SMEs. You can read more about the findings on auto enrolment's success and challenges.

This is where outsourcing your pension management to a specialist, like your accountant, really pays off. It frees you from getting tangled up in compliance. An expert can help you pick the best provider for your specific needs and then take over all the ongoing tasks, from communicating with employees to processing contributions.

Ultimately, it’s a strategic decision that buys you back your most valuable asset: time. You get to focus on growing your business, not wrestling with complex pension rules. To make this work for you, take a look at our guide on how to get the most out of your pension strategy.

How We Make Auto Enrolment Simple and Stress-Free

While this guide shows that auto enrolment is manageable, let's be honest—it’s another complex layer of admin you have to deal with when you're trying to run your business. Our goal is to lift that weight completely off your shoulders. We turn this legal headache into a smooth, background process you barely have to think about.

Think of us as your dedicated auto enrolment partner. We handle every single detail, starting with helping you choose and set up the right pension scheme for your company. From there, we take care of all the legally required employee communications, making sure your team is kept in the loop correctly from the very beginning.

Seamless Integration and Ongoing Compliance

Where we really make a difference is by plugging your pension scheme directly into your payroll. This connection ensures every calculation is spot-on and every contribution is paid on time, every time. It’s the best way to eliminate the risk of making costly mistakes and getting hit with fines.

We handle the entire ongoing cycle for you—assessing new and existing staff, processing any opt-outs, and keeping the meticulous records that the regulator demands.

By handing your auto enrolment duties over to us, you get total peace of mind. You can relax, knowing everything is being managed correctly, efficiently, and in full compliance with The Pensions Regulator.

To truly simplify the complexities of auto enrolment and alleviate administrative burdens, consider leveraging modern AI in accounting solutions that automate tedious financial tasks, including pension management.

Ultimately, our job is to give you back your time and mental energy. That way, you can get back to focusing on what you do best: growing your business with confidence.

Common Questions About Auto Enrolment

Even with the best plan in place, you're bound to run into a few specific questions as you get to grips with your auto enrolment duties. Let's tackle some of the most common queries we hear from UK employers to help you handle the process with confidence.

What Happens if an Employee Wants to Opt Out?

So, you’ve enrolled a team member, and they tell you they want out. What’s your role?

An employee has a one-month window, starting from when they’re enrolled, to opt out and get a full refund. Crucially, they have to do this directly with the pension provider. You, as the employer, can’t be involved. In fact, you're legally forbidden from encouraging or even helping staff to opt out.

Once the provider confirms they've opted out, you must stop deductions immediately and refund any contributions they’ve already made in their very next payslip. If they decide to leave the scheme after this one-month window, they can stop paying in, but they won't typically get back what they've already contributed.

Your only job in the opt-out process is to act on the official notice from the pension provider. That means stopping deductions and processing a refund. Nothing more, nothing less.

Can I Delay Auto Enrolment for New Staff?

Yes, you can. This is called 'postponement', and it allows you to delay enrolling new or newly eligible staff for up to three months. It’s a handy tool for dealing with short-term or probationary staff, or simply to line up enrolment with your payroll run.

But you can’t just quietly delay it. You have to send a formal written notice to the employees within six weeks of their start date (or the date they became eligible), explaining what's happening. If they’re still working for you and meet the criteria at the end of the postponement period, you absolutely must enrol them then.

What Are the Penalties for Getting Auto Enrolment Wrong?

The Pensions Regulator (TPR) doesn't mess around with this. They take non-compliance very seriously, and the penalties can be steep.

It usually starts with warning letters, but if you don't sort things out, the fines kick in. You could be hit with a £400 fixed penalty notice just for failing to meet your basic duties. If the problem persists, daily fines are applied, ranging from £50 to £10,000 per day, depending on how many employees you have. It’s always, always cheaper to get it right from the start.

Juggling payroll and auto enrolment can easily become a major headache and a drain on your time. Stewart Accounting Services can take all of this off your plate, ensuring you’re fully compliant so you can focus on running your business. Find out how we can help at https://stewartaccounting.co.uk.