Think of a payment on account as a down payment on your next tax bill. It’s not an extra tax or a penalty; it's simply HMRC's way of helping you spread the cost of your Self Assessment liability throughout the year, rather than facing one huge bill.

So, What Are Payments on Account and Who Actually Pays Them?

If you’ve ever filed a Self Assessment return and been hit with a request for a 'payment on account', you'll know that sinking feeling. For many sole traders, landlords, and even company directors, it can be a real source of confusion and a massive headache for cash flow. But once you get your head around how it works, it becomes much easier to manage.

Essentially, the system is designed to stop you from being clobbered with a single, potentially crippling tax bill every January. It’s an automatic system triggered by two very specific conditions from your last tax return.

The Two Key Conditions That Trigger Payments on Account

HMRC will ask you to make payments on account if both of these statements were true for your last tax return:

- Your total tax bill was more than £1,000.

- Less than 80% of that tax was already paid at source (for example, through your PAYE job).

If you tick both of these boxes, you're automatically in the system for the next tax year. This means you'll need to make two advance payments towards that year's bill. Getting to grips with these thresholds is the first step to staying in control of your tax affairs. You can also find more official details in the government's guide on understanding your Self Assessment tax bill on GOV.UK.

Let's quickly check if this applies to you.

Quick Check: Do You Need to Make Payments on Account?

Use this table to quickly determine if the Payments on Account system applies to you for the upcoming tax year.

| Condition | Yes/No | What This Means for You |

|---|---|---|

| Was your last Self Assessment tax bill over £1,000? | Yes | You've met the first condition. If the next answer is also 'Yes', you'll need to pay on account. |

| No | You won't need to make payments on account, regardless of how your tax was paid. | |

| Was less than 80% of your total tax bill paid at source (e.g., PAYE)? | Yes | You've met the second condition. If your bill was also over £1,000, you're in the system. |

| No | Even if your bill was high, you won't need to pay on account as most tax was already collected. |

If both of your answers were "Yes", then planning for these advance payments is essential for your cash flow.

Who Is Most Likely to Be Affected?

This system really impacts anyone whose income isn't taxed before it hits their bank account. While it can apply to various situations, the usual suspects are:

- Sole Traders: From freelance writers and graphic designers to plumbers and electricians, if your business is doing well, you’ll almost certainly meet the criteria.

- Landlords: Rental income isn't taxed at source, which makes landlords very common candidates for payments on account.

- Partners in a Business: Your share of the business profits is taxed through Self Assessment, often triggering these payments.

- Limited Company Directors: While your director's salary might be taxed via PAYE, any significant income you take in dividends isn't. This untaxed income can easily push you over the £1,000 threshold.

Being asked to make a payment on account is actually a good sign—it means your business or investments are generating a decent income! But it's also the point where you absolutely must start planning your finances proactively. The first step is knowing if you need to file a return at all, which our guide on who must send in a tax return explains in detail.

It's easy to think that a payment on account is just another tax grab from HMRC. But it’s not. It’s crucial to see it as a pre-payment. The money you pay in advance is a credit on your account, which reduces the final amount you’ll owe when you settle up.

By understanding these rules, you can move from worrying about surprise bills to confidently managing your tax deadlines on 31 January and 31 July.

How HMRC Calculates Your Payments on Account

Figuring out how HMRC works out your payments on account can seem a bit mysterious at first, but the calculation itself is surprisingly simple. There’s no complex algorithm running in the background; it’s all based on your tax bill from the previous year.

The basic idea is this: HMRC takes your last Self Assessment tax bill and splits it in half. Each of those halves becomes one of your two payments on account for the upcoming year. So, if your tax bill was £4,000 last year, you’d be asked to make two advance payments of £2,000 each. This predictability is meant to help you plan your finances and avoid a single, massive bill.

But it’s important to know exactly what HMRC includes in that "tax bill" figure. It’s not just a simple calculation based on your total profit.

What’s Included in the Calculation?

HMRC is only interested in your main, income-based tax liabilities when they do this sum. Specifically, they look at:

- Income Tax: The primary tax you pay on your profits from self-employment or rental income.

- Class 4 National Insurance: These are the contributions self-employed people pay, which are directly linked to their profits.

That’s it. These two figures are added together to get the total used for the payment on account calculation. Other things you might owe through Self Assessment, like student loan repayments or Capital Gains Tax, are kept separate and aren’t included. They’re dealt with differently.

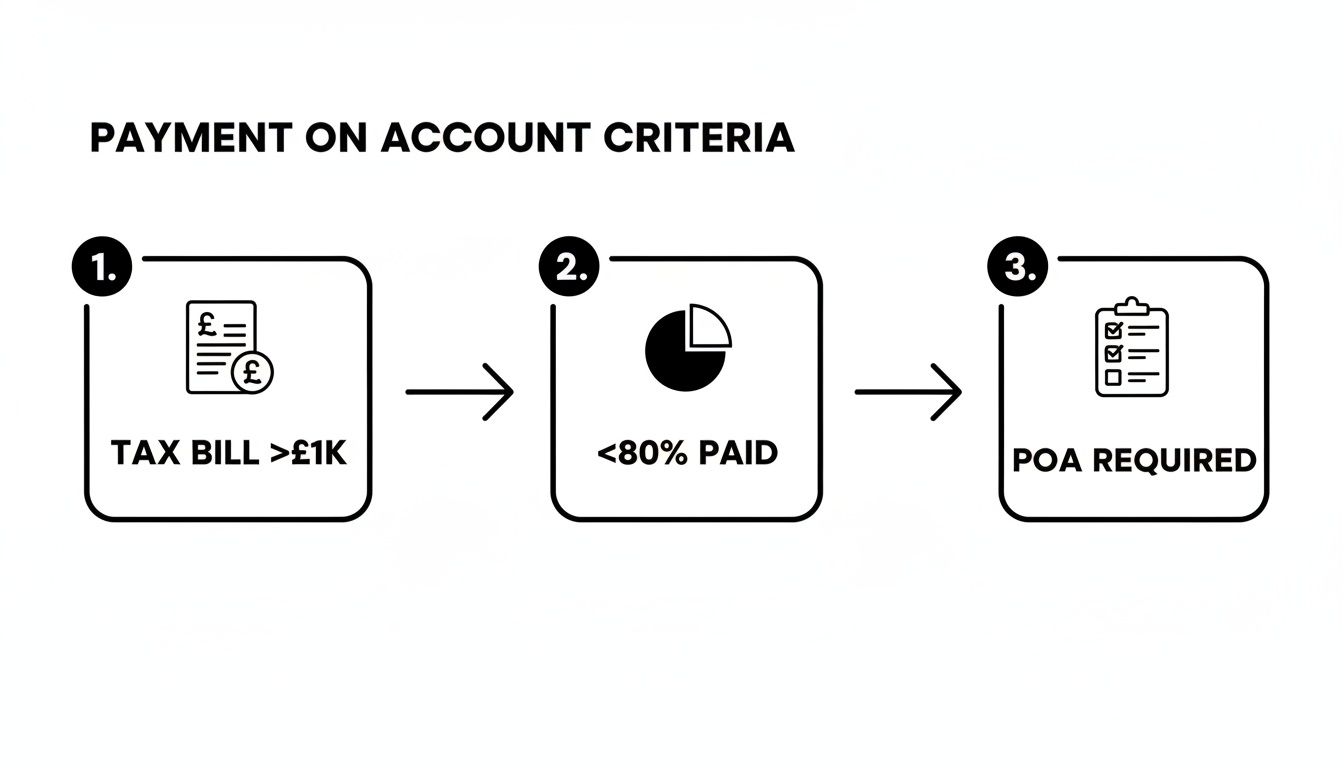

This flowchart breaks down the simple triggers for the system.

As you can see, once your tax bill goes over £1,000 and less than 80% of it was paid at source (like through a PAYE job), you’re automatically brought into the payment on account system.

Introducing the Balancing Payment

Okay, so you’ve made your two advance payments based on what you earned last year. But what if this year is much better and your profits go up? This is where the balancing payment comes into play. It’s the final step that squares everything up.

Think of it like pre-paying for a service. Your payments on account are the instalments you pay upfront. The balancing payment is the final bill that settles the difference between what you’ve already paid and what you actually owe.

The balancing payment is what makes the system fair. It accounts for the fact that income can go up or down, making sure you end up paying exactly the right amount of tax for the year—no more, no less.

This final amount is due by 31 January, the same day you have to make your first payment on account for the next tax year. This overlap is a classic cash flow trap, so it’s something you really need to be ready for.

A Worked Example of the Full Cycle

Let’s walk through a real-world example to see exactly how this works from start to finish.

Meet Freya, a freelance graphic designer.

-

The Initial Bill: For the 2023/24 tax year, Freya works out that her total tax and Class 4 NI bill is £5,000. She files her tax return before the 31 January 2025 deadline.

-

The Big January Payment: On 31 January 2025, Freya’s payment is a double-whammy. She needs to pay:

- The full £5,000 she owes for the 2023/24 tax year.

- Her first payment on account for the next tax year (2024/25), which is 50% of that bill: £2,500.

- This means her total payment on that day is a hefty £7,500.

-

The Summer Payment: Fast forward to 31 July 2025. Freya pays her second payment on account for the 2024/25 tax year, which is the other £2,500.

-

The Final Tally: Now, let’s imagine Freya had a fantastic year in 2024/25. When she does her accounts, her actual tax bill for that year comes to £6,000. She's already paid £5,000 towards it (£2,500 + £2,500).

-

Settling Up: By the next deadline of 31 January 2026, she makes a final balancing payment of £1,000 (£6,000 actual bill minus the £5,000 she’s already paid).

This cycle shows how the system uses your past earnings as a guide for the year ahead, before using the balancing payment to true everything up at the end.

Real-Life Scenarios: Sole Traders, Landlords, and Directors

The theory is one thing, but seeing payments on account play out in the real world is where it all starts to make sense. To really get to grips with how the numbers work, let's walk through the tax year with three different people: a self-employed consultant, a property landlord, and a director of a limited company.

We’ll use some realistic figures to map out their tax bills, work out their advance payments, and see what their final "balancing payment" looks like next January. These examples should give you a much clearer picture of how your profit turns into a tax liability and how HMRC expects it to be paid.

Example 1: The Sole Trader

First up is David, a self-employed IT consultant. He's had a great year and is now sitting down to do his 2023/24 Self Assessment tax return.

His income from consultancy work was £65,000, and after totting up his allowable business expenses, he had deductions of £15,000. This gives him a taxable profit of £50,000. Based on this, his total tax and National Insurance bill for the 2023/24 tax year comes to £9,500.

Because this is way over the £1,000 threshold, HMRC requires him to make payments on account for the upcoming 2024/25 tax year.

- Payment 1 (due 31 Jan 2025): 50% of the £9,500 bill = £4,750

- Payment 2 (due 31 Jul 2025): 50% of the £9,500 bill = £4,750

So, on 31st January 2025, David has to find the cash not just for his £9,500 tax bill from the year just gone, but also for his first payment on account of £4,750. That’s a grand total of £14,250 due in a single day – the classic "first-year shock" that catches so many people out.

Fast forward a year. Let's say David's business performance was pretty similar, and his tax bill for 2024/25 is again exactly £9,500. Since he’s already paid this amount in advance (£4,750 + £4,750), his balancing payment due on 31st January 2026 is £0.

Example 2: The Property Landlord

Now let's meet Sarah, who rents out two properties. For landlords, understanding payments on account starts with getting your income and expenses categorised correctly. It's crucial to understand the different 'Tax Implications For Short Term Rentals' including 'Schedule E Vs Schedule C' classifications, as this affects how your income is treated for tax.

For the 2023/24 tax year, Sarah’s total rental income is £30,000. After deducting allowable expenses like mortgage interest relief, insurance, and repairs, her taxable profit is £22,000.

Her tax liability for the year is calculated at £3,880. As this is more than £1,000, she also needs to make payments on account for 2024/25.

- First Payment on Account (due 31 Jan 2025): 50% of £3,880 = £1,940

- Second Payment on Account (due 31 Jul 2025): 50% of £3,880 = £1,940

Come the 31st January 2025 deadline, Sarah’s total payment to HMRC will be £5,820. That’s the £3,880 for her 2023/24 bill, plus the first £1,940 advance payment.

Now, what if Sarah has an even better 2024/25? A tenant moves out, she refurbishes the property, and manages to increase the rent. Her taxable profit for 2024/25 goes up, and her new tax bill is £5,000.

She has already paid £3,880 towards this bill through her two payments on account. This means her balancing payment on 31st January 2026 will be the difference: £1,120 (£5,000 actual bill – £3,880 already paid).

This is a perfect example of how the system squares up when your income increases year-on-year.

Example 3: The Limited Company Director

Finally, let’s look at Maria. She's the director of her own limited company and pays herself a small salary of £12,570 (which is taxed through PAYE) and takes the rest of her income in the form of dividends.

In the 2023/24 tax year, she draws £40,000 in dividends on top of her salary. The tax on her salary is handled by her company's payroll, so it doesn't factor into her Self Assessment bill. However, the tax due on her dividend income is £2,658.75.

This amount triggers the £1,000 threshold, so Maria also has to make payments on account.

Payments on Account for 2024/25

- Payment 1 (31 Jan 2025): £2,658.75 x 50% = £1,329.38

- Payment 2 (31 Jul 2025): £2,658.75 x 50% = £1,329.38

But let’s imagine things are a bit tighter in the 2024/25 tax year. Maria decides to take lower dividends, and her final dividend tax bill is only £1,500. She has already paid a total of £2,658.76 (£1,329.38 x 2) towards this.

In this situation, she has overpaid her tax by £1,158.76. When she files her Self Assessment return, HMRC will see the overpayment and issue a refund. This shows how the system self-corrects when your income goes down.

Managing Your Cash Flow and Avoiding Common Pitfalls

Let's be honest, the biggest challenge with any payment on account isn't the tax itself. It's the sudden, hefty hit to your cash flow. This is especially true for new business owners who get blindsided by what we call the 'first-year shock'.

Picture this: it’s your first major Self Assessment deadline. You’re suddenly faced with paying your entire tax bill for the previous year, plus your first payment on account for the current year. All at once. This means you could be paying 150% of your previous year's tax bill in a single day, which can cause a serious financial headache if you haven't planned for it.

Mastering the Tax Pot Strategy

To dodge this cash flow crunch, the single most effective thing you can do is open a separate 'tax pot' bank account. This isn't just a nice idea; it's a fundamental habit that buys you peace of mind and keeps your business on solid ground.

The logic is simple. Every time a client pays you, you immediately move a set percentage of that income into your tax pot. A good rule of thumb is to set aside 25-30%, which should comfortably cover your future Income Tax and National Insurance liabilities.

By treating tax savings as an immediate expense, you guarantee the money is ready and waiting when HMRC comes calling. This simple discipline turns a looming tax bill into just another manageable outgoing. You can dive deeper into other cashflow management strategies in our dedicated guide.

Think of your tax pot as a financial firewall. It shields your day-to-day business finances from the heat of your tax obligations, ensuring you always have the capital you need to operate and grow.

Avoiding Common Payment Pitfalls

When it comes to HMRC, being proactive is everything. Knowing the common mistakes can save you a world of stress, not to mention interest charges and penalties down the line.

Here are the most frequent slip-ups we see:

- Forgetting the July Deadline: Everyone remembers the big 31st January deadline, but the second payment on account due on 31st July often catches people out. Missing it means you'll start racking up interest charges from HMRC.

- Underestimating Your Final Bill: Remember, payments on account are based on last year's income. If your business is growing and you're earning more, you'll have a larger balancing payment to make. Keep saving into your tax pot even after you've covered the two advance payments.

- Ignoring a Drop in Income: On the flip side, if your earnings have fallen, you could be overpaying. It's crucial to inform HMRC and get your payments reduced. Otherwise, you're essentially giving them an interest-free loan with your cash.

- Dipping into Your Tax Savings: That tax pot is not a slush fund or an emergency business account. That money belongs to HMRC. Treating it as untouchable will save you from major financial pain later.

Staying on top of your obligations is crucial for your business's health. For more insights, you can explore broader payment management strategies and tools that can help. This planning is especially important when you consider the bigger picture. In the UK, total income tax receipts hit £301 billion in 2024-25, a significant jump from £275 billion the previous year. This upward trend shows just how vital diligent financial management is for every single business owner.

How to Reduce Your Payments on Account

HMRC calculates your payments on account based on a simple, but often flawed, assumption: that you'll earn the same this year as you did last year. But what happens when that's just not true?

If you know your income is going to drop, you’re not stuck paying the figure HMRC has worked out. You can, and should, reduce it. This is a common situation. Maybe a big contract ended, you’ve decided to cut back your hours, or you're even winding down your business to take on a full-time job.

When your earnings fall, your final tax bill will be smaller. It only makes sense that your advance payments should reflect this new reality. If you don't adjust them, you're effectively giving HMRC an interest-free loan with your own cash—money that could be working for you and your business.

How to Officially Reduce Your Payments

You can’t just decide to pay less; you need to formally let HMRC know. Thankfully, they provide two straightforward ways to do this.

The Two Official Methods:

- Through your HMRC online account: This is usually the easiest route. When you're filling in your Self Assessment tax return online, there’s a specific section where you can ask to reduce your payments on account for the upcoming year.

- Using Form SA303: If you’ve already filed your tax return, or if you simply prefer paper, you can download and post Form SA303, 'Claim to Reduce Payments on Account'. You can find it on the GOV.UK website.

Both options get the same job done. They put HMRC on notice that you expect a lower tax bill and allow you to set a more accurate figure for your advance payments. This simple action can free up vital cash and immediately improve your financial position.

A Critical Warning About Over-Reducing

While trimming your payments on account is a smart move when your income drops, it carries a big risk if you get your numbers wrong. HMRC is trusting you to make a fair and honest estimate.

If you reduce your payments too much and your final tax bill turns out to be higher than you predicted, you’ll face the consequences.

HMRC will charge you interest, and potentially penalties, on the amount you underpaid. This isn't a system to be gamed; it's a tool for genuine changes in circumstances.

The trick is to be realistic, not just optimistic. It’s far better to be a little cautious and have a small balancing payment to make later than to slash the payments too aggressively and get hit with extra charges.

If you're unsure about your projections, it's wise to explore legitimate ways to lower your overall tax bill first. Our guide on how to reduce business taxes is packed with practical advice on this. When in doubt, getting professional guidance is the safest way to ensure your claim is both accurate and justified.

Let Us Handle Your Tax So You Can Focus on Your Business

Getting your head around payments on account can feel like a real headache, but that’s where we come in. This guide gives you the theory, but at Stewart Accounting Services, we turn that knowledge into real-world, stress-free action for our clients.

We’re all about proactive tax planning. This means we don’t just look at the tax you’ve just paid; we look ahead to make sure your future bills are accurately forecasted. No nasty surprises. We use modern cloud accounting tools like Xero to get a live view of your income, giving you a crystal-clear picture of your finances all year round. It also means we can confidently handle all HMRC communications on your behalf, whether that’s filing your return or submitting a Form SA303 to reduce your payments if your income drops.

Our main job is to take the weight of tax management off your shoulders. We’ll crunch the numbers so you can get back to what you do best—running and growing your business.

We make the whole process simple, from figuring out if the £1,000 threshold applies to you, right through to helping you manage your cash flow effectively. When you work with us, you’re not just hiring an accountant. You’re getting a strategic partner who is focused on giving you back your time, your money, and your peace of mind.

Ready to make tax anxiety a thing of the past? Get in touch with our team today and let's see how we can help you handle your tax obligations with complete confidence.

Frequently Asked Questions About Payments on Account

Even when you think you've got your head around the system, there are always a few niggling questions that pop up. Let's tackle some of the most common queries we hear about payments on account, so you can feel confident you're on the right track.

What Happens If I Miss a Payment on Account Deadline?

Miss the 31 January or 31 July deadline, and HMRC will start charging you for it immediately. There’s no grace period here.

The day after the payment was due, interest starts racking up on the overdue amount. It won't stop until you've paid the full balance. If the debt drags on, you could also get hit with late payment penalties on top, which can really start to sting.

Do Payments on Account Cover My Class 2 National Insurance?

No, they don't. This is a classic tripwire that catches many people out and can leave you with an unexpected bill.

Your payments on account are calculated based only on your previous year's Income Tax and Class 4 National Insurance. Your Class 2 National Insurance contributions – the flat-rate weekly amount for self-employed individuals – are completely separate. You'll pay that bill in full alongside your final balancing payment on 31 January, so make sure you've budgeted for it.

Think of it this way: Payments on account are a pre-payment for your profit-based tax. Class 2 NI is more like a fixed running cost of being in business, which you settle up once the tax year is over.

What Should I Do If My Income Increases Significantly?

If you have a great year and your income shoots up, your existing payments on account will fall short of what you'll actually owe. You aren’t required to officially tell HMRC about the increase mid-year, but ignoring it is a recipe for a cash flow disaster.

The smart move is to work out a rough estimate of your new tax bill and start putting extra money aside in your ‘tax pot’ to cover the difference. Your two payments on account will still chip away at the total, but you'll be left with a much larger balancing payment than usual. Setting that cash aside as you earn it is far less painful than facing a shock bill the following January. A little bit of planning makes all the difference.

Getting to grips with the ins and outs of your tax obligations can feel like a full-time job. But you don't have to figure it all out by yourself. At Stewart Accounting Services, we're here to give you the expert guidance you need to hit every deadline and keep your cash flow healthy. Contact us today and let's make tax stress a thing of the past.