Ever wondered where all your business's financial transactions actually live? They live in the nominal ledger.

Think of it as the master filing cabinet for your company's money. Every single financial event – from a big sale to buying a coffee for a client – gets its own specific folder, which we call an 'account'. This detailed organisation is the very heart of the double-entry bookkeeping system that all businesses rely on.

Your Business's Financial Command Centre

For SME owners across the UK, getting your head around the nominal ledger isn't just an accounting box to tick; it's a strategic must-do. This is your financial command centre, where all the raw data from your day-to-day trading gets sorted, stored, and eventually turned into reports that actually mean something.

Let's say you just paid your monthly office rent. That single payment is recorded in the nominal ledger under a specific account, like 'Rent Expense'. When a customer pays you, that income is neatly logged in your 'Sales' account. Every transaction is categorised like this, building a complete and detailed history of your business's financial life.

The Core of Financial Reporting

The real power of the nominal ledger comes from its structure. It organises everything so you can generate the critical financial statements that tell you exactly how your business is performing. These reports are the ones that matter:

- The Profit and Loss (P&L) Statement: This tells you if you're making money over a set period.

- The Balance Sheet: This gives you a snapshot of your assets, liabilities, and equity on a specific day.

- The Trial Balance: A vital internal check to make sure all your debits and credits add up perfectly.

Understanding your nominal ledger is the first step towards making truly informed business decisions. It moves you from simply recording history to actively shaping your company's future with data-driven insights.

This isn't some new-fangled idea. The nominal ledger has been central to UK business for centuries, acting as the complete, organised record of every transaction. This principle is so fundamental that its roots in British commerce can be traced back over three hundred years. You can dive deeper into the history of UK financial record-keeping through the Bank of England's research.

Why It Matters for Your SME

For any small or medium-sized business, a well-kept nominal ledger is absolutely essential. It's what ensures your financial reporting is accurate, which is non-negotiable when you're trying to secure a loan, attract investors, or simply comply with HMRC.

Modern cloud accounting software like Xero—which we use every day here at Stewart Accounting Services—handles a lot of the heavy lifting. But even with the best software, knowing the principles behind the nominal ledger empowers you to read your financial data with real confidence. It’s about seeing beyond the numbers and understanding the story they tell about your business's performance, its challenges, and its potential for growth.

Decoding Your Chart of Accounts and Nominal Codes

If the nominal ledger is the master filing cabinet for your business finances, then the Chart of Accounts (CoA) is its index. It’s simply a complete list of every single account—every "folder"—you can use to categorise your financial transactions. Without a decent index, your filing cabinet would just be a chaotic mess of unsorted paperwork.

Think of it like this: when a customer pays you, you don't just chuck the money into a big box labelled "money in". The Chart of Accounts gives you a specific place to put it, say, under an account called 'Sales – Product A'. This simple, structured list is what brings order to your bookkeeping, making your financial data both easy to find and genuinely useful.

The unique labels on each of these folders are your nominal codes. These are just numbers (or sometimes a mix of letters and numbers) given to each account in your Chart of Accounts. They act as a universal language for your finances, ensuring everyone logs transactions in the same way.

The Five Pillars of Your Accounts

Every single transaction your business makes will fit into one of five fundamental account categories. Getting your head around these is the first real step to mastering your finances. To keep things neat, each of these categories is usually given its own range of nominal codes.

- Assets (1000s): This is everything your business owns that has value. Think of your company bank account, your delivery van, or the laptops your team uses every day.

- Liabilities (2000s): This is everything your business owes to other people or organisations. It could be a bank loan, an unpaid supplier invoice, or the VAT you need to pay to HMRC.

- Equity (3000s): This represents the net worth of your business. In simple terms, it's what would be left for the owners if you sold all your assets and paid off all your liabilities. It includes things like the initial capital invested and profits kept in the business.

- Income (4000s): This is the money your business makes from doing what it does best—selling goods, providing services, or even earning a bit of interest from a savings account.

- Expenses (6000s-9000s): These are all the costs you rack up to keep the business running. It's a huge category, covering everything from office rent and staff salaries to software subscriptions and marketing spend.

The Chart of Accounts isn’t just an admin task; it's the very blueprint for your financial reporting. A well-organised CoA is the foundation for clear, accurate, and insightful financial statements.

This structured system is what turns a long list of individual transactions into reports you can actually use, like your Profit & Loss statement and your Balance Sheet.

Putting Nominal Codes into Practice

To show how this all comes together, let's look at a typical UK business—say, a small graphic design agency. Their Chart of Accounts might have specific nominal codes to keep track of all their different activities.

Here’s a simplified look at what their codes might be.

Example Nominal Codes in a UK Chart of Accounts

| Nominal Code Range | Account Category | Example Account Names |

|---|---|---|

| 4000 – 4999 | Income / Revenue | 4001 – Design Services, 4005 – Retainer Fees, 4900 – Interest Received |

| 5000 – 5999 | Cost of Sales | 5001 – Freelancer Costs, 5010 – Stock Photography Purchases |

| 7000 – 7999 | Administrative Expenses | 7001 – Office Rent, 7200 – Software Subscriptions, 7405 – Professional Indemnity Insurance |

| 1200 – 1299 | Fixed Assets | 1220 – Office Equipment (Computers), 1230 – Office Furniture |

Now, when the agency pays its monthly Adobe Creative Cloud subscription of £50, the bookkeeper (or the accounting software) doesn't just record it as a "cost". They post that transaction to nominal code 7200 – Software Subscriptions.

It's this level of detail that allows the business owner to later run a report and see exactly how much they’re spending on software each year. For a deeper dive into setting these categories up, have a look at our detailed guide on the Chart of Accounts.

Ultimately, this system of codes creates a direct link between your day-to-day business activities and your high-level financial reports. Your total income is just the sum of everything in the '4000' range, while your overheads can be calculated from the '7000' range and beyond. Getting this structure right is the key to unlocking real financial clarity.

How Journal Entries Tell Your Financial Story

We've covered the structure—the nominal ledger and its index, the Chart of Accounts. Now it’s time to see how it all works in the real world. This is where the story of your business gets written, transaction by transaction, using a method called double-entry bookkeeping.

Every single financial event, from paying a supplier to receiving a client's payment, is captured as a journal entry. You can think of a journal entry as a short, formal note that describes a transaction: what happened, when, for how much, and which specific accounts in your nominal ledger were affected.

This system has been the bedrock of accounting for centuries. The practice of categorising financial records has deep roots in UK history, evolving from the detailed logs kept by merchants. In fact, research into British mercantile trade from 1662 to 1809 shows just how vital this kind of structured ledger-keeping was for managing the nation's commerce and building the foundations for the systems we use today.

The Logic of Debits and Credits

The fundamental idea behind double-entry bookkeeping is that every transaction has two equal and opposite effects. We record these effects as debits (Dr) and credits (Cr). It’s a common sticking point for many, but the concept is surprisingly simple once you get the hang of it.

First, forget any notion that 'credit' is always good and 'debit' is always bad. In accounting, they simply refer to the two sides of a ledger account.

- A debit is an entry made on the left side of an account.

- A credit is an entry made on the right side of an account.

Whether a debit or credit increases or decreases an account depends entirely on the type of account we're talking about (asset, liability, income, etc.). The one unbreakable rule is that for any journal entry, the total of the debits must equal the total of the credits. This is what keeps your books perfectly balanced.

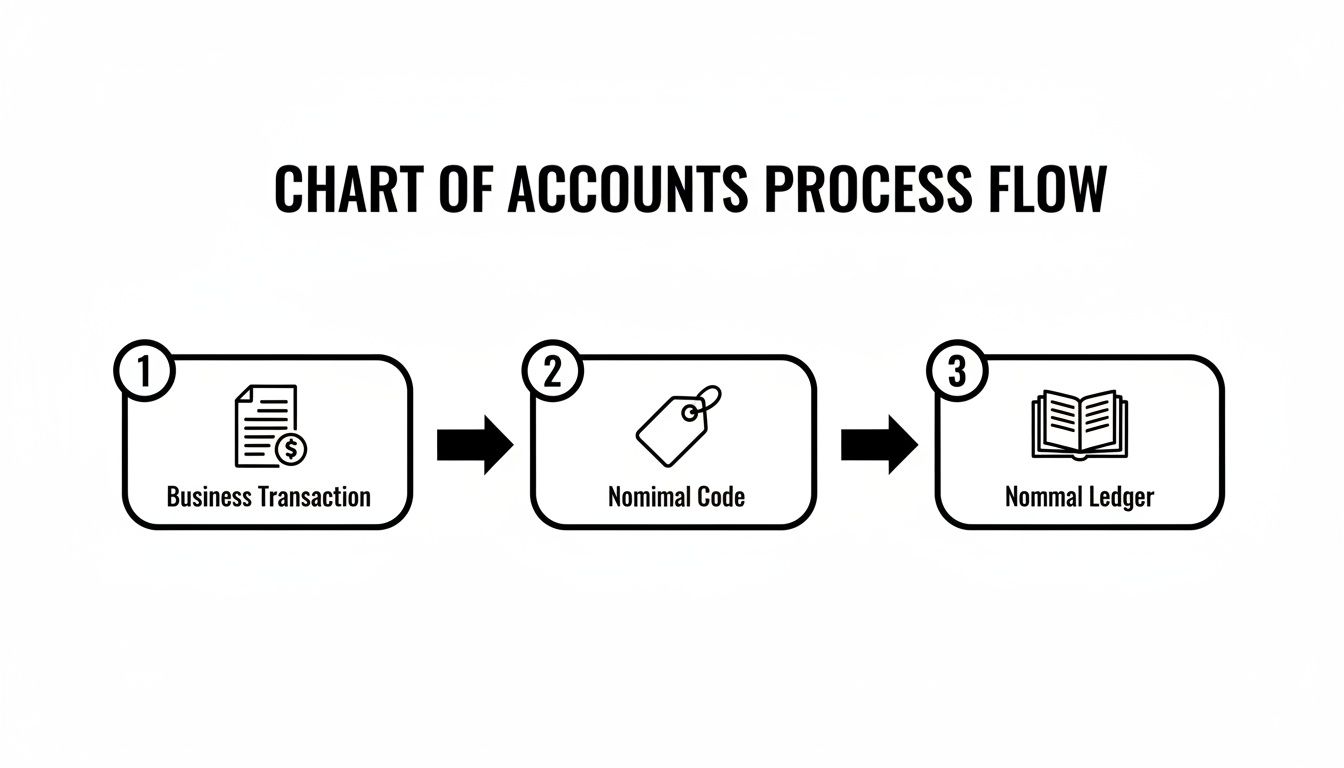

This diagram shows the journey from a business transaction all the way to its final home in the nominal ledger.

As you can see, every transaction is first assigned a specific nominal code from your Chart of Accounts before being recorded. This little step ensures everything is organised correctly from the very beginning.

Real-World Journal Entry Examples

Let's walk through a few common scenarios for a UK small business to see how this all works in practice.

Scenario 1: You Pay Your Monthly Office Rent

You pay your landlord £1,000 for the month's rent. This single event affects two accounts in your nominal ledger: your Bank Account (an asset) and your Rent Expense account (an expense).

- The Bank Account (Asset): Your cash has gone down. A decrease to an asset account is recorded as a credit.

- The Rent Expense Account (Expense): Your expenses have gone up. An increase to an expense account is recorded as a debit.

The journal entry would look like this:

Debit: Rent Expense (7001) – £1,000

Credit: Bank Account (1200) – £1,000

The debits (£1,000) equal the credits (£1,000), so the transaction is balanced. Simple.

Scenario 2: You Buy a New Laptop

Your company buys a new laptop for £1,500 using the company debit card. This transaction involves your Bank Account (an asset) and your Office Equipment account (another asset).

- Office Equipment (Asset): The value of your equipment has increased. An increase to an asset account is a debit.

- Bank Account (Asset): The cash in your bank has decreased. A decrease to an asset account is a credit.

The resulting journal entry is:

Debit: Office Equipment (1220) – £1,500

Credit: Bank Account (1200) – £1,500

Again, the entry is perfectly balanced.

Scenario 3: You Invoice a Client for Services

You finish a project and send an invoice for £5,000 to your client. At this point, you haven't received the cash yet, but you have earned the income. This affects your Sales account (income) and an account called Trade Debtors or Accounts Receivable (an asset representing money owed to you).

- Trade Debtors (Asset): The amount of money owed to you has increased. This is a debit.

- Sales (Income): Your income has increased. An increase to an income account is a credit.

The journal entry to record the sale is:

Debit: Trade Debtors (1100) – £5,000

Credit: Sales (4001) – £5,000

Each of these entries tells a small but vital part of your business's financial story. The information for them often comes from source documents; for small, recurring expenses, using a standard petty cash receipt template can be a great way to ensure accuracy. By consistently applying the rules of double-entry bookkeeping, you ensure every part of that story contributes to an accurate, complete, and balanced picture of your company's performance.

Turning Ledger Data Into Strategic Business Reports

Your nominal ledger is far more than just a dry record of transactions. Think of it as the raw material for building a clear picture of your business's performance. Every single journal entry, carefully filed under its nominal code, is a piece of that puzzle. The real magic happens when you pull all this data together, transforming a long list of numbers into strategic financial reports that actually help you make smart decisions.

This all starts with a crucial internal check called the Trial Balance. It’s your first quality control step, ensuring everything adds up before you go any further. The trial balance simply lists the final balance of every account in your nominal ledger—assets, liabilities, equity, income, and expenses. Its one and only job is to confirm that the total of all the debit balances equals the total of all the credit balances.

If they match, brilliant. Your books are balanced, and you can move on with confidence. If they don't, it’s a red flag. It means there’s an error somewhere in your bookkeeping that you need to find and fix before you can produce accurate reports.

From Trial Balance to Profitability Insights

Once your Trial Balance gives you the green light, the data is split out to create your main financial statements. The first one most business owners look for is the Profit and Loss (P&L) Statement, which you might also hear called the Income Statement. This report tells the most important story of all: is your business actually making or losing money?

The P&L statement focuses purely on your income and expense accounts over a set period, like a month or a quarter. Here’s how it works:

- It totals all your income: The report sums up the balances from all nominal codes in your income range (usually the '4000s' in your chart of accounts) to get your total revenue.

- It totals all your expenses: Next, it adds up the balances from every expense code—like the '5000s' for cost of sales and the '7000s' for overheads—to calculate your total costs.

- It calculates the difference: Finally, it subtracts your total expenses from your total income. The result is your net profit or loss for the period.

This report is the ultimate summary of your trading, showing you exactly where your money came from and where it all went. To see how these figures can be used to inform strategy, take a look at our guide on what is involved in management reporting.

Building a Snapshot of Your Company's Health

While the P&L tells you about performance over time, the Balance Sheet gives you a snapshot of your company’s financial health on a specific day. It doesn't care about income or expenses. Instead, it pulls in the remaining accounts from your nominal ledger: assets, liabilities, and equity.

The Balance Sheet is built around the unbreakable accounting equation:

Assets = Liabilities + Equity

This formula must always balance, giving you a crystal-clear picture of what your business owns (its assets) and how you've paid for them—either with debt (liabilities) or with the owners' own funds (equity). It’s essential for understanding your company's net worth and overall financial stability.

This systematic approach to record-keeping isn’t just a modern fad; its importance has been understood for centuries. In fact, the data from individual SME nominal ledgers today is aggregated to help shape UK economic policy. Initiatives between the Bank of England, the Economic Statistics Centre of Excellence (ESCoE), and the Office for National Statistics preserve historical financial data, showing just how long this discipline has been valued. You can even explore the vast UK Historical Data repository to see how these trends have been tracked through time.

Ultimately, these reports are the entire point of maintaining a nominal ledger. They transform thousands of individual transactions into clear, actionable information, giving you the clarity you need to spot trends, manage your cash flow, and make the big decisions that will move your business forward.

Streamlining Your Bookkeeping With Cloud Software

The days of scribbling in dusty, oversized ledger books are well and truly over. Technology has turned the nominal ledger from a manual, time-consuming chore into a smart, automated digital engine that sits at the heart of modern business finance. Today, cloud accounting software is the command centre for your financial story.

Platforms like Xero have completely changed the game for SMEs. They cleverly tuck the complex principles of double-entry bookkeeping into the background, so you don't need to manually wrestle with debits and credits every time you make a sale or pay a bill.

Automation Behind the Scenes

The real magic of this software is its automation. When you create and send a sales invoice, the platform does much more than just email a PDF. Behind the scenes, it automatically generates the correct journal entry, debiting your Trade Debtors account and crediting your Sales account without you having to lift a finger.

It works just as smoothly for expenses. Log a payment for your monthly software subscription, and the system instantly debits the correct expense account while crediting your bank account. This built-in logic drastically cuts down the risk of human error, which can be costly and a nightmare to fix. In fact, modern AI-driven accounting platforms can correctly auto-book over 93% of transactions, saving business owners countless hours.

By automating journal entries, cloud software ensures your nominal ledger is always balanced and up-to-date. This gives you a real-time, accurate view of your financial position, empowering you to make faster, more informed decisions.

This level of automation provides a solid foundation for financial clarity. To get the most out of these tools, it's worth exploring our guide on cloud accounting for small business to understand how they fit into your wider operations.

Making Categorisation Effortless

Another huge benefit is the direct integration with your business bank accounts. Live bank feeds pull in transactions automatically every day, meaning you can finally stop manually typing in every single line from your bank statement. From there, you can create rules to automatically categorise recurring payments.

For instance, you could set a rule that every payment to "British Gas" is always coded to your 'Utilities' expense account. This turns what used to be a daily headache into a quick, simple review process. For businesses in specialised sectors like property management, checking out a detailed property management software comparison can help find tools with these time-saving integrations.

Ultimately, cloud software gives SME owners immediate access to a precise, live nominal ledger. It frees you from the drudgery of data entry, minimises mistakes, and delivers the instant financial insights you need to focus on what really matters—running and growing your business.

Gaining Financial Clarity with Expert Guidance

Keeping your nominal ledger organised is the bedrock of good financial control. But as your business grows, so does the financial complexity. Honestly, knowing when to ask for help is a massive part of what separates businesses that just get by from those that really take off. Bringing in a firm like Stewart Accounting Services isn't just about tidying up the books—it's about giving your business the platform it needs to thrive.

The signs that it's time to call in an expert are usually pretty clear. Maybe your business is expanding quickly, and you're simply drowning in transactions. Or perhaps you're getting tangled up in the tricky worlds of VAT, payroll, and CIS returns, where one tiny slip-up can mean a painful letter from HMRC.

From Bookkeeper to Strategic Partner

A good accountant doesn't just record what happened last month; they help you figure out what to do next month. They take all that raw data sitting in your nominal ledger and turn it into a powerful tool you can use to make smart decisions about the future.

For any ambitious business owner, that shift is everything. It means you can stop spending your precious time fighting with spreadsheets and start focusing on your strategy, your growth, and, most importantly, your customers.

Handing over your bookkeeping isn't about losing control; it's about gaining clarity. It frees you up to lead your business, armed with accurate, timely financial insights prepared by a dedicated expert.

How Professional Guidance Drives Growth

The benefits of working with a professional accountant aren't just theoretical; they have a real, tangible impact on your business. An experienced hand at the tiller will help you:

- Optimise Cash Flow: They'll dive into your income and expense patterns to find ways to improve your cash position. After all, cash is the lifeblood of any small business.

- Ensure Flawless Compliance: Forget about sleepless nights worrying about deadlines. They manage all the filings with Companies House and HMRC, ensuring everything is accurate and on time. That peace of mind is priceless.

- Make Data-Driven Decisions: With regular, easy-to-understand management reports pulled directly from your nominal ledger, you can see what's working and what isn't, helping you make confident choices for the road ahead.

For many business owners I speak to, the biggest win is simply getting their time back and cutting down on stress. Letting a professional handle your nominal ledger and other financial tasks allows you to step back from the nitty-gritty and focus on the big picture. It’s the next logical step to turning your business vision into a profitable, sustainable reality.

Frequently Asked Questions About the Nominal Ledger

Even when you’ve got the basics down, a few questions always pop up when you start putting it all into practice. Let's tackle some of the most common queries we hear from UK business owners about the nominal ledger.

Is the Nominal Ledger the Same as the General Ledger?

This is probably the most common point of confusion, and for good reason—the terms are thrown around so much they often seem to mean the same thing. In today's world of accounting software, they pretty much do.

Historically, there were subtle differences. You'll find the term General Ledger (GL) used more often in the US, while here in the UK, we've traditionally favoured Nominal Ledger. Both refer to the same central hub where all your financial transactions are recorded and sorted.

Think of it this way: for all practical purposes in your day-to-day bookkeeping, especially if you're using a platform like Xero, the nominal ledger and general ledger are two names for the same thing.

To clear up any lingering confusion, here’s a quick breakdown of how the terms are often perceived, even if they function identically in modern systems.

Nominal Ledger vs General Ledger: A Quick Comparison

| Feature | Nominal Ledger | General Ledger |

|---|---|---|

| Primary Focus | Contains the detailed "nominal" accounts (income, expenses, assets, etc.). | The complete collection of all ledgers, including sales and purchase ledgers. |

| Common Usage | The preferred term in traditional UK accounting. | The more globally recognised term, common in the US and modern software. |

| Modern Context | Often used interchangeably with General Ledger. | Considered the master ledger that the nominal ledger is part of. |

Ultimately, whether you call it a nominal or general ledger, its job is to give you a complete, organised picture of your company's finances.

How Often Should I Review My Nominal Ledger?

You really should be checking in on your nominal ledger accounts regularly. For most small businesses, setting aside time for a review once a month is a fantastic habit to get into. It’s your chance to catch any transactions that have been put in the wrong place before they snowball into a much bigger headache at year-end.

A quick monthly check helps you:

- Make sure every transaction is assigned to the correct nominal code.

- Spot any unusual spikes in spending or dips in income straight away.

- Keep a real-time, accurate view of your financial health, which is vital for making smart decisions.

Keeping on top of this makes preparing your VAT returns and annual accounts a far smoother and less daunting task.

Can I Change My Nominal Codes Later?

Yes, you absolutely can, but it's something to do carefully. Your Chart of Accounts, which is the list of all your nominal codes, should be tailored to your business. For instance, you might decide to add a new, more specific expense code for "Social Media Advertising" instead of lumping it in with general "Marketing".

The key is to avoid making constant or major changes. Doing so can mess up your reporting, making it difficult to compare performance from one year to the next. If you feel your codes need an update, it's always a good idea to have a quick chat with your accountant first. They can help you make logical changes and ensure your historical data is handled properly.

What Is a Suspense Account in the Nominal Ledger?

A suspense account is essentially a temporary parking spot in your nominal ledger. It’s used for transactions when you’re not immediately sure where they belong. A classic example is receiving money into your bank account, but you don't have an invoice to match it against right away. You can post it to the suspense account to keep the books balanced while you figure it out.

The golden rule of good bookkeeping is to clear out your suspense account regularly. Its purpose is purely temporary. Ideally, the balance should be back to zero by the end of every month or reporting period.

A well-kept nominal ledger isn't just about good admin; it's the bedrock of financial clarity and strategic decision-making. At Stewart Accounting Services, we specialise in turning your raw financial data into insights that help you save time, boost profits, and sleep better at night. Find out how our expert bookkeeping and accounting services can help your business thrive.